Just FYI - Promoters have been buying up shares big time recently. Just in the last 34 days, they bought an additional ~900000 shares for an average price of ~85

9 Likes

3 Likes

Could anybody share what would be the market share of manappuram in NBFC gold industry and its growth(mkt shr) in past years.

1 Like

Annual report

Gold loan :

growth forecast :

It also forecasts that the assets under management (AUM) of gold loan NBFCs would experience growth of 6% during FY 2022, and 11.4% during the FY 2023, as a result of the industry’s continued emphasis on expansion.

With our long-term focus, solid business model and brand, we are confident of registering a 10-15% growth in gold loans in the coming fiscal unless any further challenges come up.

competition :Company believe this is a temporary phenomenon as the levels at which

industry players are operating are unsustainable. We foresee the situation

to normalize in the next few quarters.

Gold loan industry :

the major share of gold loan stays with moneylenders and the informal sector. About just a third of India’s US$ 128 billion is under the organised sector.

Credit cost :

On the other hand, it is anticipated that the cost of credit would not change.

Non gold :

We see good potential in our non-gold businesses as well. We have established solid competencies in them, and now with the rural markets improving, our teams are actively reaching out to customers for business development.

Gold loan by MFI :

In the MFI businesses, the regulatory decision to increase proportion of secured loan book (other than microfinance) to 25% of the portfolio is a welcome move. With this, Asirvad Microfinance has initiated gold lending to improve quality of assets and so far, it has opened 320 branches exclusively for this business.

Microfinance outlook :

On the back of a resurgence in industry growth that might reach 30%, India Ratings has revised upwards its outlook on the microfinance industry to ‘neutral’ for FY 2023, moving it up from ‘negative’ in FY 2022. In comparison to the below 10% increase in AUM (assets under management) seen in each of the prior two years, it is expected that the industry will experience growth of 20%-30% in both FY 2022 and FY 202

Automobile industry growth

The volume of domestic vehicle sales has been projected to increase 5%-9% annually in FY 2023, following three consecutive years of constant decline in growth.

Home loan :

In FY 2023, housing finance businesses may increase by 13% annually, compared to 11% recorded in FY 2022, according to India Ratings and Research

OPPORTUNITIES:

Unexplored Potential of gold loan :

The World Gold Council estimates India’s privately held gold reserves to be between 20,000 and 25,000 tonnes. The primary objective of the gold loans business model is to inject liquidity into this inventory, which is currently mostly untapped.

Level Playing Field:

The Reserve Bank of India (RBI) has mandated that a standard restriction on LTV of 75% be applied to both banks and NBFCs. This has created a level playing field, which is beneficial to NBFCs.

unorganised sector :

Despite the expanding network of the formal sector, the informal sector continues to dominate the market for gold loans as a whole, presenting an opportunity to expand the network and acquire the informal sector’s business.

RISKS AND THREATS

AUM growth can be negatively impacted by a decrease in the price of gold.

Greater competition from NBFCs/banks/fintech could harm AUM growth and profits.

6 Likes

Thanks for the good summary.

Management’s unacceptance of banks eating away gold finance company’s share is not good. Or they accept it but they got no proposal to tackle that and hence not even mention that publicly.

Disc: Invested since 2018.

1 Like

My takeaways from Annual report:

- Gold loans at lower yields offered by other companies are not sustainable liquidity gets tighter and funding dries up, especially for loss making competitors.

2)Share of online gold loan decreased from 54% to 44% due to high base in previous years which digital lending increased due to pandemic.

Please read page no. 35 of Annual report to see the competitive strategies of specialised gold loan NBFC to understand how they differ from bank. I am enclosing the screenshot of the same below.

Disclaimer: Holding with average price of 90 rupees. Conviction getting stronger at these valuation and after studying annual report.

3 Likes

CRISIL Ratings has assigned its ‘CRISIL AA/Stable’ rating to Rs 2500 crore non-convertible debentures of Manappuram Finance Limited

Upward factors

-

Continued strong market position in the gold finance business with increasing diversity in AUM into non- gold business without impairing asset quality

-

Sustenance of profitability with RoMA above 5% on a steady state basis, while improving asset quality

Downward factors

- Increase in consolidated gearing to over 5 times

- Steep decline in interest collection in the gold loan business or deterioration in asset quality or profitability in the non-gold loan segments

1 Like

Quaterly Results mostly flatish.

Huge increase in employee expenses Y-o-Y.

Lets wait and see their presentation

Con-Call Recording :

Investor Presentation :

Increase of approximately 55 crore in the total revenue As compared to last quarters. Employees cost increases almost 17 crore from last quarter whose reason is needed to be find. Earning per share increased to 3.43 rupees from 3.19.Imo results will gradually improve. Disclaimer:Invested and biased.

2 Likes

Q1FY23 Concall Notes

- Gold Loan Business

-

“Pressure from banks and fintechs seen easing somewhat in the face of reversal of RBI’s COVID-related LTV relaxation for banks and tighter liquidity conditions for fintechs. Going forward, the Company intends to prune the low yielding, high ticket loans (6.9% teaser portfolio that was introduced during Covid). This is a conscious measure and the income associated with such portfolio is not high.”

-

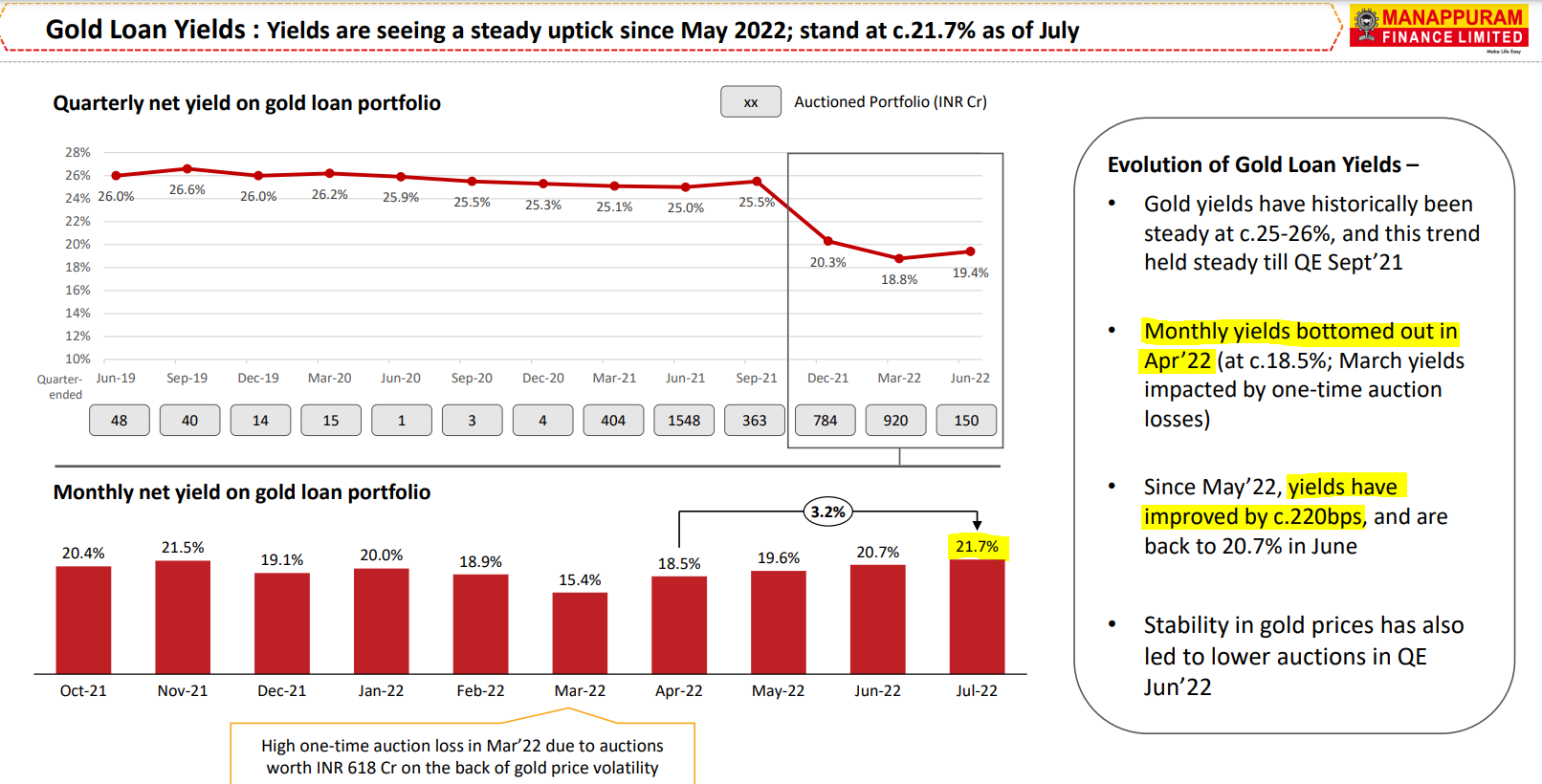

“Net yields on Gold Loans improved from 18.8% in QE Mar’22 to 19.4% in the current quarter. As at the end of July, yields have further increased to 21.7%. Yield improvement largely driven by rationalization of low-yielding schemes.”

-

Yields will settle at around 21-22%

-

- MFI Business

-

collection efficiency for the quarter at 102%

-

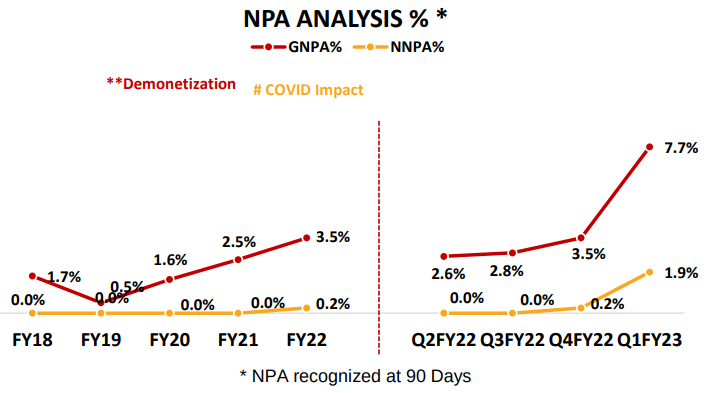

GNPA of new book (disbursals post May’21) is less than 1%

-

320 Gold loan branches under Asirvad as of now.

- Gold AUM currently at Rs.421 crs

- No RBI approval needed here but the cap is at 25% of total AUM

-

Management believes that high provisioning for Asirvad is coming to an end of cycle.

-

Incremental disbursement NIM is around 15%

-

- Cost of borrowing increased by 10 bps on a sequential basis during 1QFY23.

- Central bank hiked the custom duty on 1st July 2022 from 7.5% to 12.5%.

- 10% of book is still under teaser loan.

- Maturity upto December 2022

- Might come back during diwali. (One has to keep eye)

-

Competition is similar to 6 months back.

-

The demand from lower segment has yet to come back to Pre-COVID levels

- Demand picks up sowing season that is from September.

- Demand for gold loan is stagnant as of now

-

The demand from lower segment has yet to come back to Pre-COVID levels

- Guidance of provision:

- half of last year

- Might increase next quarter but would stabilize in second half of the year.

6 Likes

-Flat results but optimistic commentary

Stand-alone profit 290 cr

Consolidated profit 282 Crore

Going forward I feel non gold portfolio will contribute to 20% plus in profits = 60 cr plus

So in q1 22 profits should cross 400cr

GOLD LOANS :

24 lacs live gold loan customers

standalone gold loan portfolio increased by 21.22 per cent to 20K crore compared q1FY22.

-YIELDS : Going forward yields will be around 21-22 % in fy23

I feel all other gold companies will increase the yields and business will normalise to precovid yields soon as no one want to suffer loss or minimal profits

-Bank competition less as high LTV benefit for banks is no more there

- good monsoon and agricultural pickup

-new branches awaiting rbi approval

-gold growth guidance 10%

non-gold loan now account for 34 %

Microfinance

Now 7k Crore as compared to 6k Crore in Q122

microfinance business, is for significant growth in the days to come

Ashirwad turning into mini gold loan NBFC with plan for 25% gold loan

Microfinance turning around ,provisioning going down

Now it’s clean Microfinance portfolio

Out of 7000 crore only 1000 crore is pre covid portfolio

10% spread cap removed by RBI

Credit cost will drop further

other non gold portfolio

good growth expectations > 20%

Home Financ has AUM of 874 cr , which is up by 22%

-good dividend

-positive free cash flow

-clean Management

- soon moving towards well diversified NBFC

And Everything available at price to book of 1

Expecting things to stabilise and improve going forward

Worst seems to be over in terms of pricing pressure in the gold loan business

5 Likes

Interesting article with gold loan interests comparison of different banks and the NBFCs. It says NBFCs will climb back up with market share which they lost to banks.

4 Likes

Could anyone clarify what’s the difference between Stage 1, 2, 3 in ECL Provisions?

Expecting 5-10% gold growth this year

and back to usual growth of 10-15% from next year

I feel it has bottomed out in terms of business as well as valuations

Key trigger will be Ashirwad turnaround or listing

Next 3-4 quarters will be interesting

Beauty of positive free cash flow is that such businesses can survive prolonged downturn

Remain rocksteady whatever comes in their way

Covid ,demonetisation,inflation,competition

Very hard to lose money in such business at this valuation

Muthoot MD George Alexander- infectious smile ![]()

10% growth

Positive outlook

Demand picking up

15 Likes

RATING SENSITIVITIES

Factors that could, individually or collectively, lead to negative rating action/downgrade:

IDRS

The rating may be downgraded in the event of aggressive growth in non-gold lending segments without a corresponding strengthening in risk controls and balance-sheet buffers, higher leverage sustained above 4.5x, or higher-than-expected operational risk losses that materially weakened profitability.

Factors that could, individually or collectively, lead to positive rating action/upgrade:

IDRS

Fitch believes that the ratings have limited upside potential in the near term. In the longer term, evidence of sustained robust regulatory compliance, a strengthened franchise in gold and non-gold lending segments along with a record of maintaining healthy asset quality and profitability metrics may be positive for the ratings.

1 Like

Promoter buying shares in open market!

4 Likes

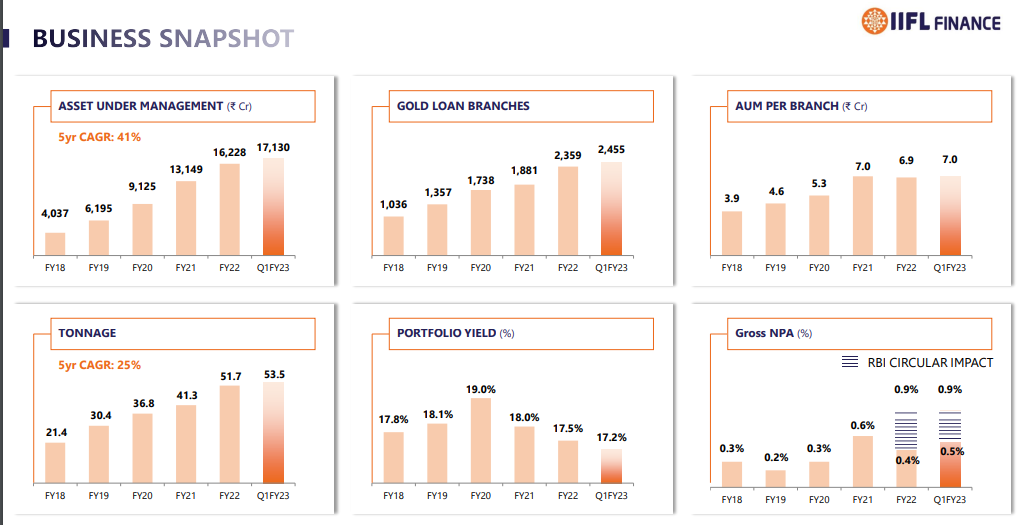

good progress by IIFL in the Gold loan segment. shaping up to be a serious competitor to Muthoot & Manappuram in the urban space

3 Likes

Major difference are the yields:-

Mana and Muthoor Yields vs IIFL Yields is a data point that Gold Loan Financiers investors should think about…

Disc: invested in IIFL Fin.

4 Likes