The rating reaffirmation continues to factor the experience of promoters and professional management, Manappuram Group’s established track record, healthy asset quality, comfortable capitalisation, strong financial profile and adequate risk management and management information systems. The rating is, however, constrained by the inherent risks associated with the gold loan and non-gold loan portfolio, coupled with regional concentration risk.

3 Likes

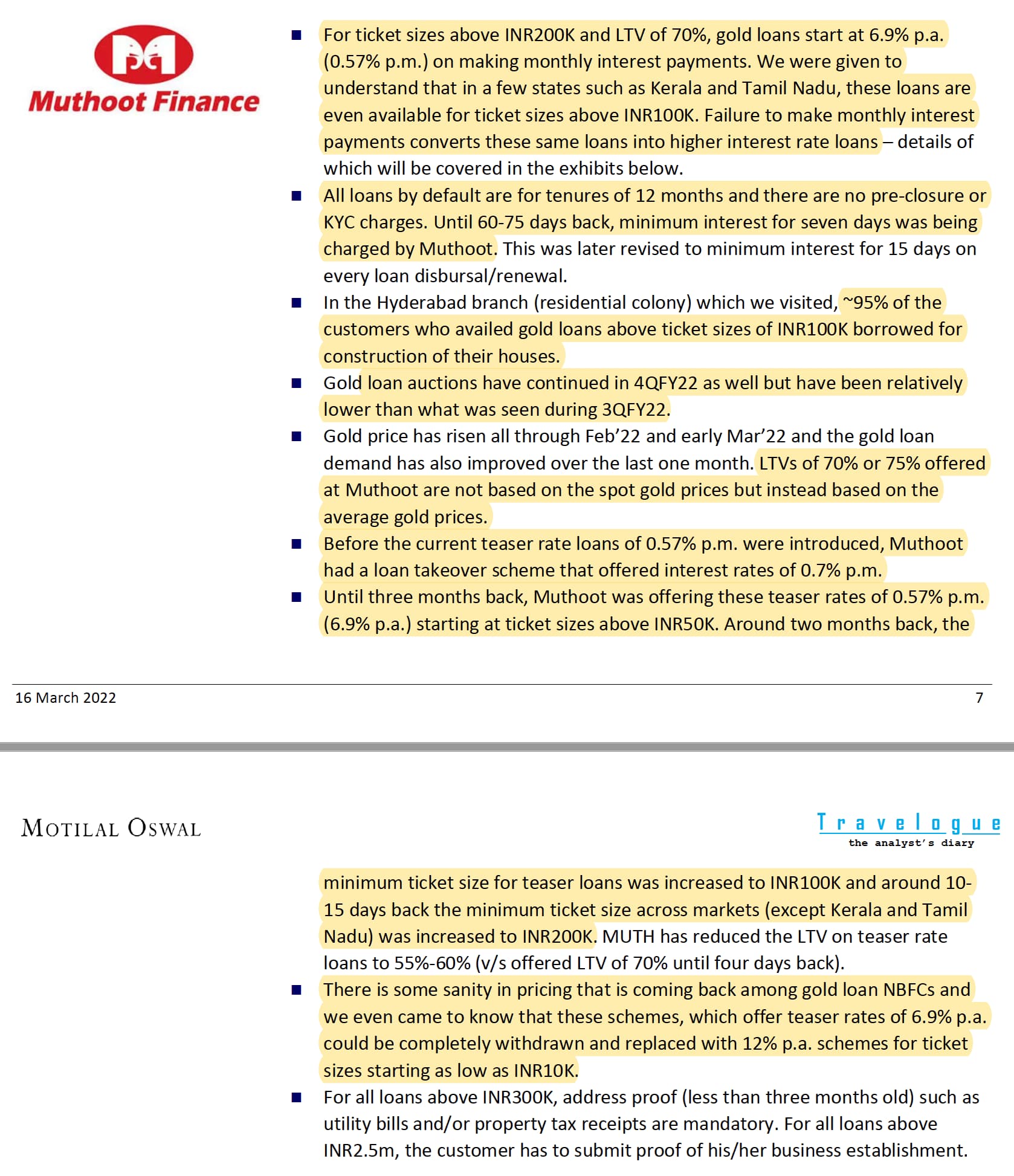

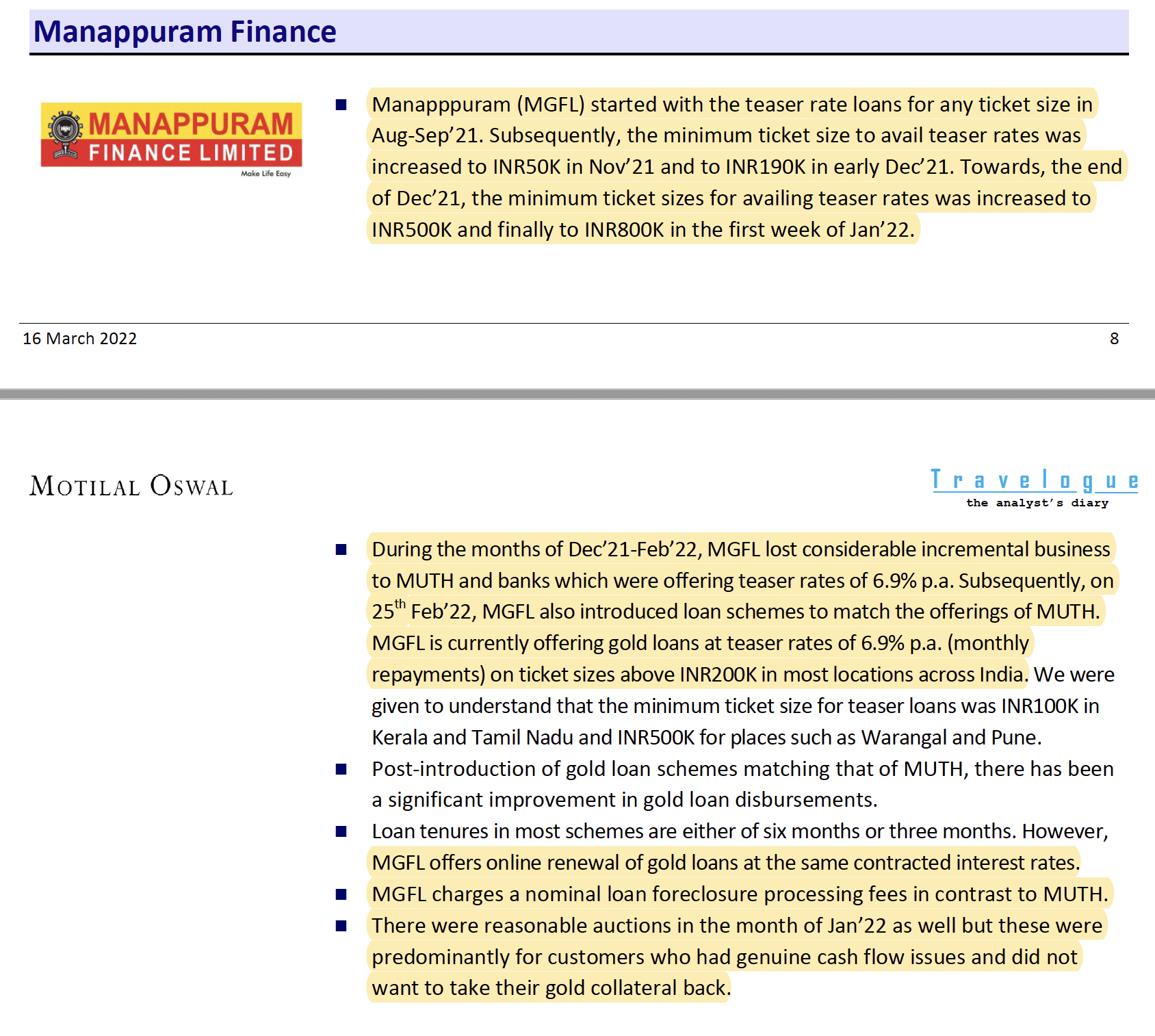

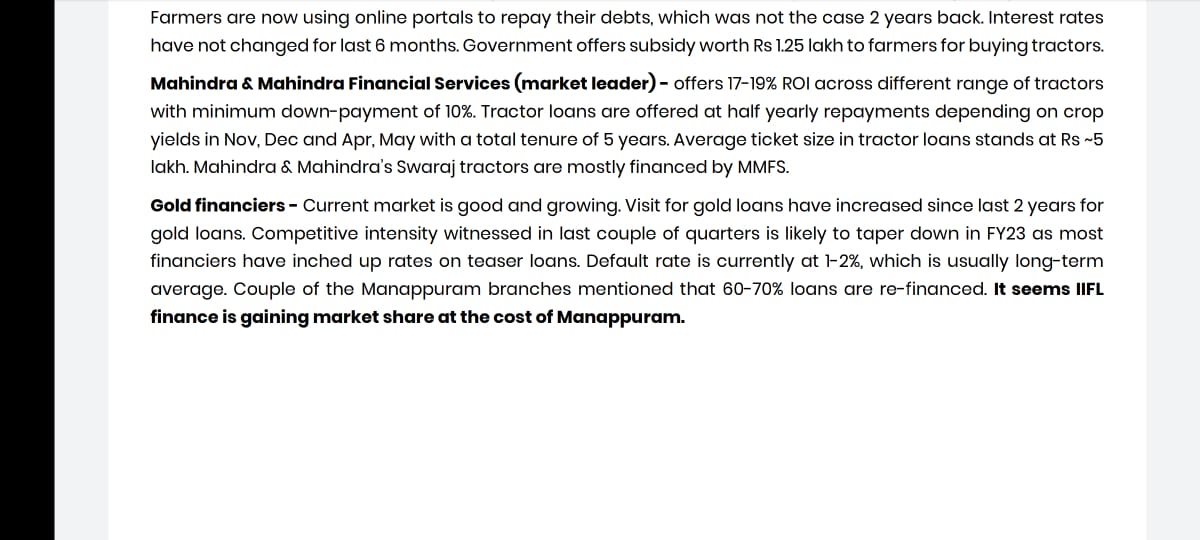

Very interesting field visit report (Hyderabad and Vizag) from Motilal about competition among gold loan NBFCs, I have attached the relevant excerpts at the end.

Summary: Competition is intense between Manappuram, Muthoot and IIFL. Each company is trying to poach high value customers by offering very low teaser rate loans (0.6% monthly interest) which are applicable if one pays monthly EMI. Apparently, 75-80% of customers who take these teaser loans end up not paying monthly interest and are moved to a higher interest rate slab. There is lot of flip flop happening where companies are changing the terms and conditions of these teaser rates abruptly resulting in very high balance transfer for high ticket sizes. Basically, these high ticket customers do not have any stickiness and have a plethora of options to avail loans.

Disclosure: Invested (position size here, no transaction in last 1-month)

11 Likes

Interesting update from B&K–

Seems Manappuram is losing market share. Let’s see if this is a deep value trap for years to come or a deep value buy. Taking decisions and shifting seems to be working out here atm

9 Likes

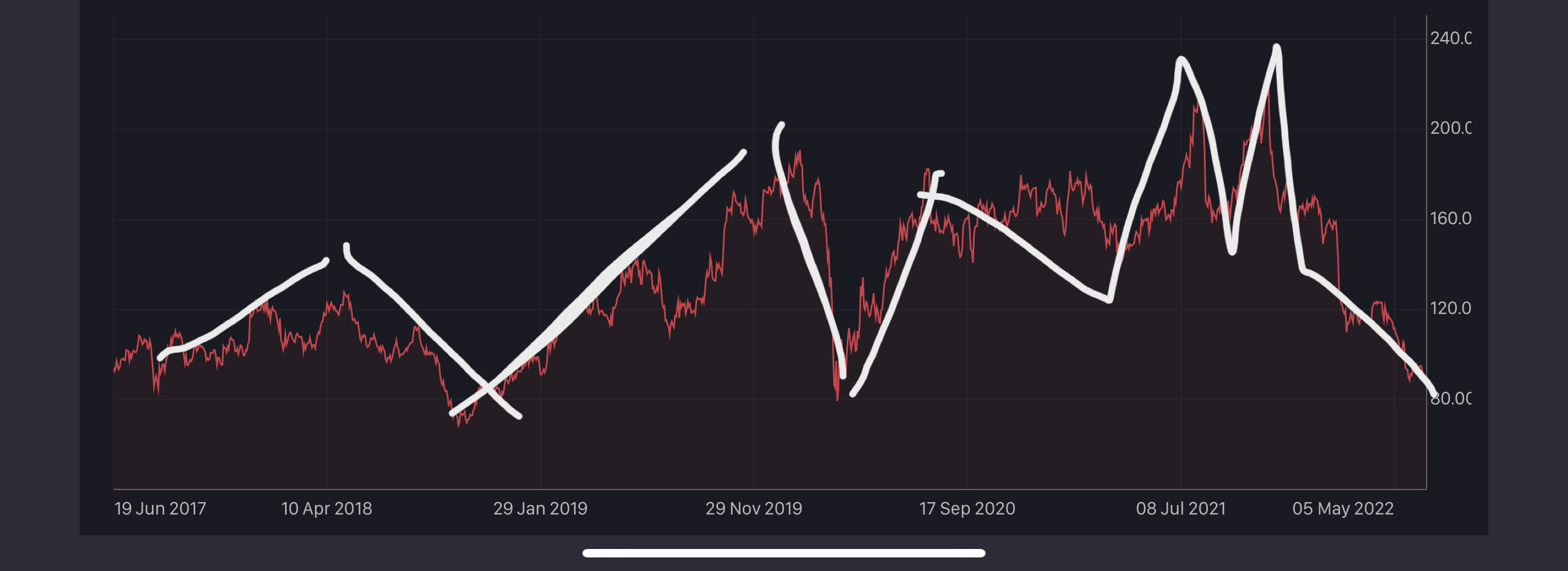

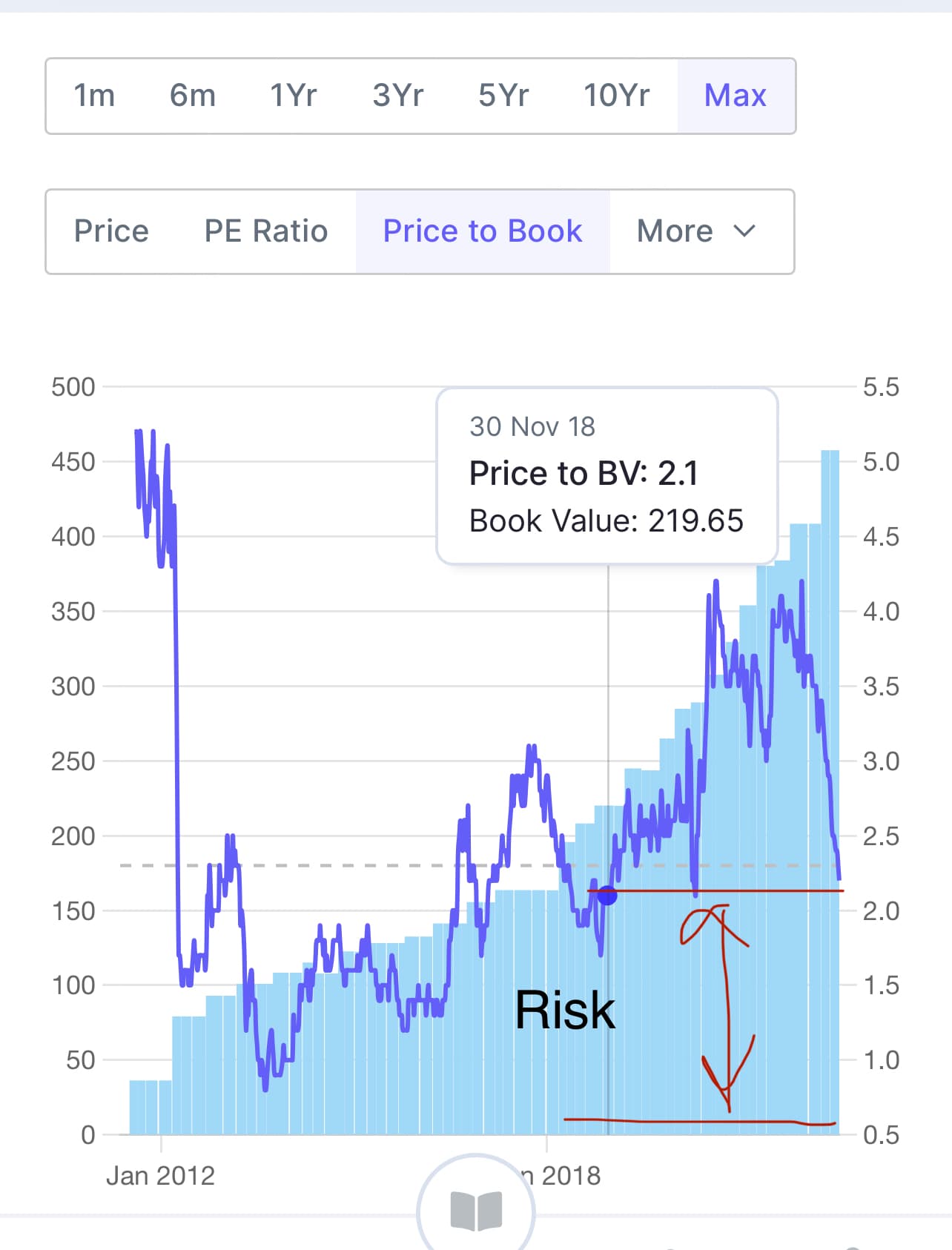

So Manappuram made another 52 week low today at 103. If one looks at the price chart, the company had touched a similar price for the first time in 2016. Let’s compare some numbers between that time and today.

Revenue

2016 - 2369

2022 (Expected) - 6202

Net Profit

2016 - 353

2022 (Expected) - 1536

Book Value

2016 - 2758

Sep 2021 - 7970

So effectively while the Book value has gone almost 3x, Revenue 3x and Net Profit 5x you are getting this business for a similar price. So at 1.1x Book value one gets an NBFC with with consistent 25%+ ROE, 5 year Sales Growth of 22% and PAT growth of 37%. Also, most importantly negligible NPAs over the years (baring exceptional circumstances)

This past year has not been the best for Manappuram and there is talk of it losing market share to other NBFCs but we will need to monitor the situation for a few quarters or a year or two to actually see the long term impact it can have. The unorganized sector of Gold based lending is still so huge that there may be enough room for multiple players to grow. I think at 1.1x book value, a lot of the pessimism is already priced in.

Manappuram is still a strong brand name with years of great execution behind it. The narrative has changed with the fall in stock price (from gold loan being the safest kind of NBFC to suddenly having no moat) but I believe the business quality is still very good. Plus whenever the Microfinance cycle turns, it will benefit a great deal from that as well (Asirvad is one of the largest and well diversified MFIs in the country).

All in all looks like a heads I win, tails I don’t lose much situation.

14 Likes

I would not look at 5 year CAGR as its after COVID when competition got aggressive in the market (losing market share proves that). Past few quarters (barring the last one, even there the growth came at the cost of margins) Manappuram has performed poorly compared to peers, which brings in doubt in execution skills plus doubt on whether its a strong brand or not.

Unorganized market opportunity is huge but it is difficult to track whether management is focusing on the same. They already have more than 4000 branches therefore, even if incremental branches are opened up in tier 3-4 cities to fight unorganized sector there is a barrier of approval from RBI which will not allow it to growth fast.

Disclosure: Invested.

9 Likes

Thanks everyone for great additions to the thread.

Wanted to understand in detail why Manappuram is loosing market share and why are people preferring other Gold loan lenders? One reason I can understand was their gold auction tenure of 3 months which they have bumped up.

2 Likes

Results are out : https://www.bseindia.com/xml-data/corpfiling/AttachLive/bacbfd5f-1543-4a4c-96f2-f89077725e38.pdf

Net profit is same as last quarter. ![]()

Q4FY22 Concall Notes

- Had mentioned about optimism in the economy in last concall, but the recovery has not happened yet.

- Gold loan & MFI did not grow this quarter.

- There is price war going on in the gold loan market.

- They have decided to stick to 21% blended yield.

- Some players have taken their business.

- Management believes that gradually the players will realize that these yields are not sustainable and price war would end.

- There is easy money available in the market which is providing short term pressure in the business as competition is going aggressive.

- Over Rs.2 lakhs ticket size constitutes 33.0% of our AUM

- New MFI regulation: Current yields for MFI: target of ROE of 20%. Yield of 24% currently. 10.3% cost of borrowing.

- People who want short term loan will not waste 2 days at a bank as they might be daily wage people.

- The competition is among NBFCs

- The demand from lower pyramid has not come back might come in next quarter.

- Targeting ROA 5% and above

- MFI business has affected the ratios this time

- Growth target of 20%

- Considering tp raise capital for MFI but parent is also there for backup

- Yields will be above 20% going forward

- No increase in branches for parent company.

- Application for 300 branches to RBI

15 Likes

Pandemic , Slow demand and high competition reasons stated by management for flat growth qoq

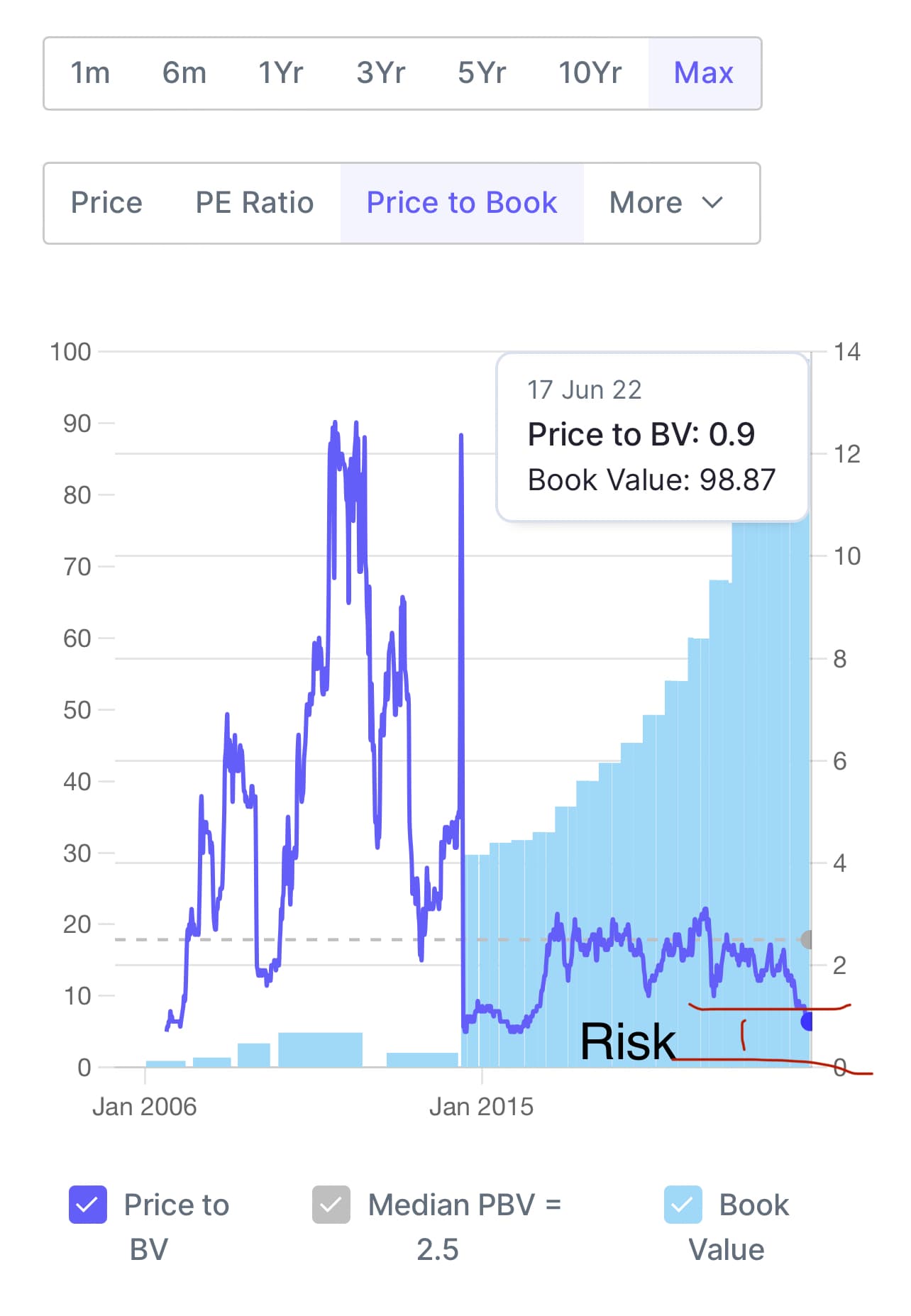

Market didn’t like it and now it’s trading below book value

Concall

Management has guided 10% AUM gold growth and consolidated 15% AUM growth in FY23

1 Like

No point in looking at what the management guides. Markets have rightly punished this one.

Fine line between value trap and value buy. This has been the former for many years now…

4 Likes

Fall & Rises in market & business happens…

It’s just about the sustainability u should be worried about… Market raised it a lot n now punishing as u said …But though growth got impacted still company has a healthy financial strength and earns reasonable for shareholders… Which will again be revalued by market. It’s just expectation got hurt of manappuram well wishers but it’s not the end of MFL. Just a slowdown i would suggest…

8 Likes

Management VP nandkumar:

-it’s one off issue ,even though stress is there postpandemic things are slowly improving

-Demand is picking up at lower end of pyramid post pandemic

-Things are steadily improving

-Microfinance is coming back

All reports are freely available at trendylene.com

Axis securities buy rating with TP 165

Oswal Motilal - buy TP 130

ICICI buy rating 147

Monarch capital buy rating with TP 150

Nirmal bang buy rating with TP 166

Key things to monitor competition ,yield and gold price

3 Likes

Concall transcript

This is the effect of the pandemic. The economy has gone to a standstill situation. Now we see the recovery. So, expecting a recovery, so the lockdown situation is not expected to recur. Because of that, we are expecting 10% growth there. And other businesses are expected to grow over 20%. And the asset quality also would be good. In MFI, we are expecting ROE of over 20%. So, the other businesses also which has already established a strong footing is likely to grow and report would follow. The MFI has come back, so that can help ROE definitely move to 20

During the month, it was rather stagnant, or it was flat. But May, we have seen slight growth. And we hope by June things will further improve. We are showing signs of growth now. So, May, there was a marginal growth and slowly but it is picking up. And towards June what happens is with school reopening, etc, it starts to catch up then. After that once the monsoon is over, sowing season starts, this is how the season for the gold loan comes. So, we hope that this year we are targeting minimum growth of around 10%, not less than 21%

1 Like

. KYC में Muthoot Finance का Management, Q4 में शानदार प्रदर्शन और Future Outlook पर चर्चा - YouTube

Muthoot hopeful of good demand going ahead :

With the economy opening up, small businesses and MSMEs are starting their businesses. We expect the demand for gold loans will start rising in the next quarter and we would see good demand for gold loans in the coming quarters.

I feel market has severely punished both muthoot and Manappuram on valuations front .But if they show some consistent growth than both may soon attain previous high

2 Likes

" [Acquisition of 219,000 equity shares worth Rs 199.10 lacs by promoter & director]"

1 Like

Bitcoin is bleeding ,

initially many were claiming it as an alternative to gold

With recession and inflation gold possibly will go high which will be a plus for Manappuram

At this moment “Bitcoin as an alternative to gold” slogan is hurt

Many were saying with rising inflation Bitcoin will go up and it will act as an hedge against recession and hedge against fed printing dollars

But opposite has happened And it’s crashing like anything

So its sure bitcoins will not be helpful for hedging

So far gold is steady and holding the fort

Still gold standing strong as an asset class unlike Bitcoin

New age investors have realised it hard way after investing it in Bitcoin

If I am right some of crypto money will move to gold

Interesting times ahead for Manappuram as it’s keep trading below book

It’s a T20 player with sharp ups and downs

Usually it achieves 52 week highs and lows ultra fast

Looks like for muthoot another 60% correction required to come close to Manappuram valuations

If we look at the past there is not much difference in the growth between muthoot and Manappuram and they follow the same ups and downs

I feel Given high muthoot base it will grow slower than Manappuram

Value buyers usually start coming below book value and from a strong support zone

Risks to investment is

Gold price fluctuations

Non gold portfolio NPA

6 Likes

Valuations have been attractive over the last two years and still, the stock has delivered negative returns. The major reasons are competition from other NBFCS and Banks. Markets awarded higher multiples to Manappuram due to consistent growth over the years which has stagnated in recent quarters. I don’t see the stock going anywhere from current levels without showing growth. Better to wait for couple of good results to start accumulating further at these prices. Even in last quarter where other banks NBFCs have shown fantastic results, Manappuram’s numbers were underwhelming.

However, positives are very low valuations, positive management commentary on non-gold segments, promoter buying from open market and as you said perceptions and valuations change very quickly on this company. Financial sector on the whole has underperformed the index in recent years. Lets see if this is a value trap (popular opinion and a case study for many famous investors) or a real value stock.

Disc: invested and holding.

4 Likes

Such competition from bank and NBFCs is not new

It happened in past also

This competition is cyclical

Banks will likely compete less aggressively when profit will go down

Manappuram is constantly showing profits

I feel the free float shares is too much

Management has only around 30-40% shares

Most are traders here and hence one of the reason ,it swings heavily

Management usually takes necessary steps to come out of difficult situations

It has proved many times in past

And negative bias adds in falling stocks

I have faith in management and hence I keep adding with every fall below book value .I feel 0.8 book value is not great risk .It May fall further but risk reward looks little favourable

Likely Book value will keep on increasing here

And from past observations,it just need 6-12 months in Manappuram to go from one extreme to other

Hence it usually never gives time to act or to wait couple of quarters to see the growth as it moves too fast

Traders heaven

These are my views

Few questions about business

-

fund raising - not a issue so far

-

is business model flexible - yes they can change the interest rate to adjust returns

-

competition- will always be there ,mostly cyclical

-

cross selling products - yes

-

track record - long

-

management -clean and innovative

Leadership - one man show mainly - risk -

geopolitical risks - yes

8 ) long term sustainability- likely as people always need money

Also 2/3 of gold loan is with unorganised sector so huge scope for organised sector to grow .

10-15% growth achievable in gold loan

On top of that Microfinance,housing and vehicle will keep growing -

bank NBFC and other unorganised sectors - dynamic process with ongoing changes in market share

-

brand value - good

-

easy to replicate business - not easy

-

consistent dividend - yes

-

gold price - likely go up gradually with inflation ,cyclical with upward trajectory

-

disruption by digital players - unlikely as need gold storage

Also Manappuram is also evolving it’s online process -

pricing - below book value - not bad

-

diversification - ongoing

With diversification operating leverage kicks in

As gold loan needs lot of operational cost ,this diversification helps in Cross selling and bringing down the operative cost combined .So with Cross selling profits sum of operative cost comes down for individual portfolio

Although the housing and vehicle are not high yield business but with reduced operating cost as gold loan branch is already there the overall profits go up

It’s complex but fruits come over a period of time -

profits going down further - possible

-

going in loss - possible but not likely

-

market perception - poor so far

-

crashing from here - possible another 20-30%

-

gone through many rough cycles and ongoing issues but so far steady in profit generating

-

non gold portfolio NPA - cyclical

Eg Microfinance had tough last 2 years but the projected growth for cuople of years is very strong with 30% plus growth expected by industry players and it will take care of previous bad years in a go -

gold NPA - good lending practises prevent losses

-

promoter buying - tiny amount

-

analyst view - some exited some waiting to exit some buying - mixed consensus depending on market price

Analysts also find hard to predict the future with certainty every quarter they change their views

26 ) ease of doing business - not easy -

saturated ground - new people still entering to get some pie,so profits getting distributed

-

banks - main advantage low interest

Banks are good for long term loans like housing but gold and Microfinance banks don’t do well

Now main question is why banks can’t concentrate more on gold loan

Gold loans for banks comprises a minuscule percentage of their portfolio while for NBFCs its a major portfolio

Now if it’s minuscule portfolio for banks then they prefer to target it less aggressively. -

NBFC - quick disbursal

They are king in low ticket size

Banks don’t treat low ticket customers well.They will be lost in crowd and big lines

So low ticket customers like NBFCs who can quickly disburse loans ,fill forms for them and reach them locally with a human touch

Banks focus on high ticket customers in all segments including gold ,housing and vehicles -

unorganised sector - high interest rate but connected to people with less exploring capabilities

-

loan duration short - so slight fluctuation in interest not much effect

Yield is the key factor

During intense competition everyone decrease interest rate and so spread And profits are affected

But it’s usually a temporary phenomenon

And gradually everyone increases interest rates improve spreads and profits

Also customer keeps on coming back.It’s a short duration repeat repeat kind of business .Take loan pay take loan pay and cycle repeats -

all risks priced in - don’t know as every year new risks arising so can’t price in

Hence it fluctuates in 2 extremes -

valuations-below book

-

technical - bearish

And never getting stable valuations -

PE rerating or derating - anything possible

-

with the amount of free cash flow can they acquire a new business or they should focus on primary business gold .Can they open new branches will RBI give quick permission- still slow process .Can they increase operative efficiency- ?

-

retaining customer in gold business is hard .People do change and not loyal to anyone .Should they offer discounts to existing old customers .

-

expansion beyond India or India has e pull business .Management says lot of untapped gold .

37 ) it’s so complex dynamics it’s best to leave to the management to evaluate analyse and perform -

Inflation and stagflation effect ,global recession effect - no clarity for short term

But long term it has happened many times in past

We have witnessed many such cycles of inflation and recession

It’s good in a way to clear out the weak players and strong players usually come out more strong with dominance

During inflation gold investment increases and also gold loan will increase

So inflation is good for gold loan -

need robust growth in economy and then it will reflect in profits .When Will economy roar ? .

-

can we do just trading buy at below book and sell at 1.5-2 x book ,retrospectively this strategy has given huge returns .repeat this every 1-2 years and earn 50-100% returns .But can this repeat ?

-

otherwise it’s an opportunity cost for long term investors without trading strategy

-

value trap for fundamental investors and heaven for traders

-

risk of losing from this valuations ( low PE low book value consistent dividend ) vs risk in losing from high PE companies high book .Is there a relation .I guess no ,whoever shows high growth market will reward no matter what PE is and what book value .So does value investing works ? I feel yes as long as there is some growth which is long term . If growth is lost then price crashes same happened here .

-

Last but not the least - what PE such business deserve … who has delivered such a consistent profits in all cycles of economy recession ,covid ,regulations ,gold fluctuations ,many such events .,and still rock solid

…. below book value and single digit PE or some rerating coming soon…that’s a multi million question for few …not me and I am very clear as valuations are on my side

Summary - multiple permutations and combinations possible in short term .

But medium to long term it should grow 10-20% consistently .

For short term Clarity will come only with time and strong will emerge stronger and weak payers will vanish

25 Likes

SBI reported today that they are seeing good traction in the gold loan business and that they expect to grow even faster in FY23. They have crossed Rs 1 lakh crore in gold loans. I am hoping this bodes well for Manappuram as well? Or am i comparing apples to oranges here? Can someone more knowledgeable throw some light on this, thanks.

1 Like

Today my mother visited sbi to withdraw a fd. The concerned person could not do it today along with a lot other fd withdrawal requests. the reason is he was busy with some gold loan related work amd went to other other branch for that.

Disclosure: Not invested. Just tracking the gold loan sector due to investment in IIFL Finance.

2 Likes