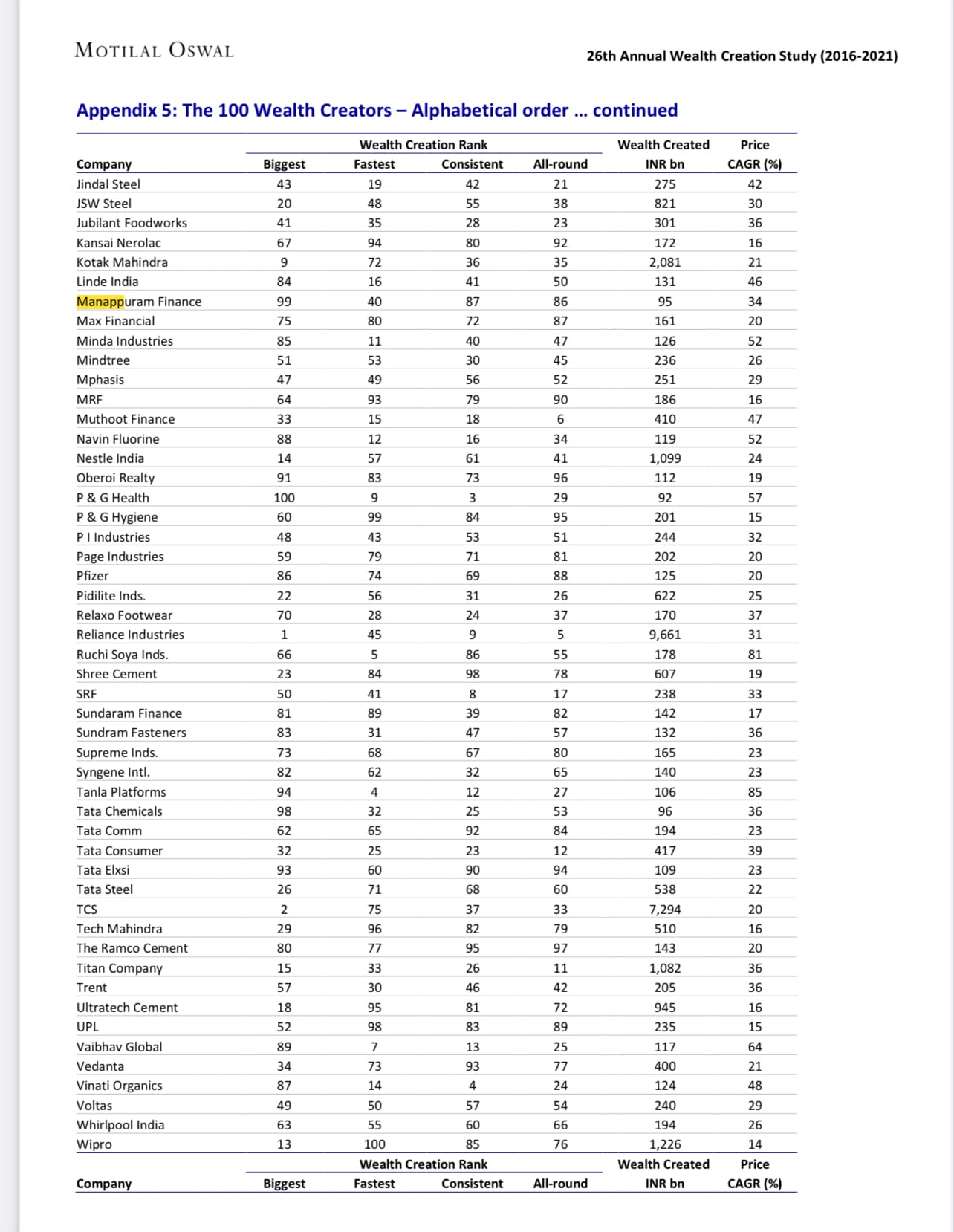

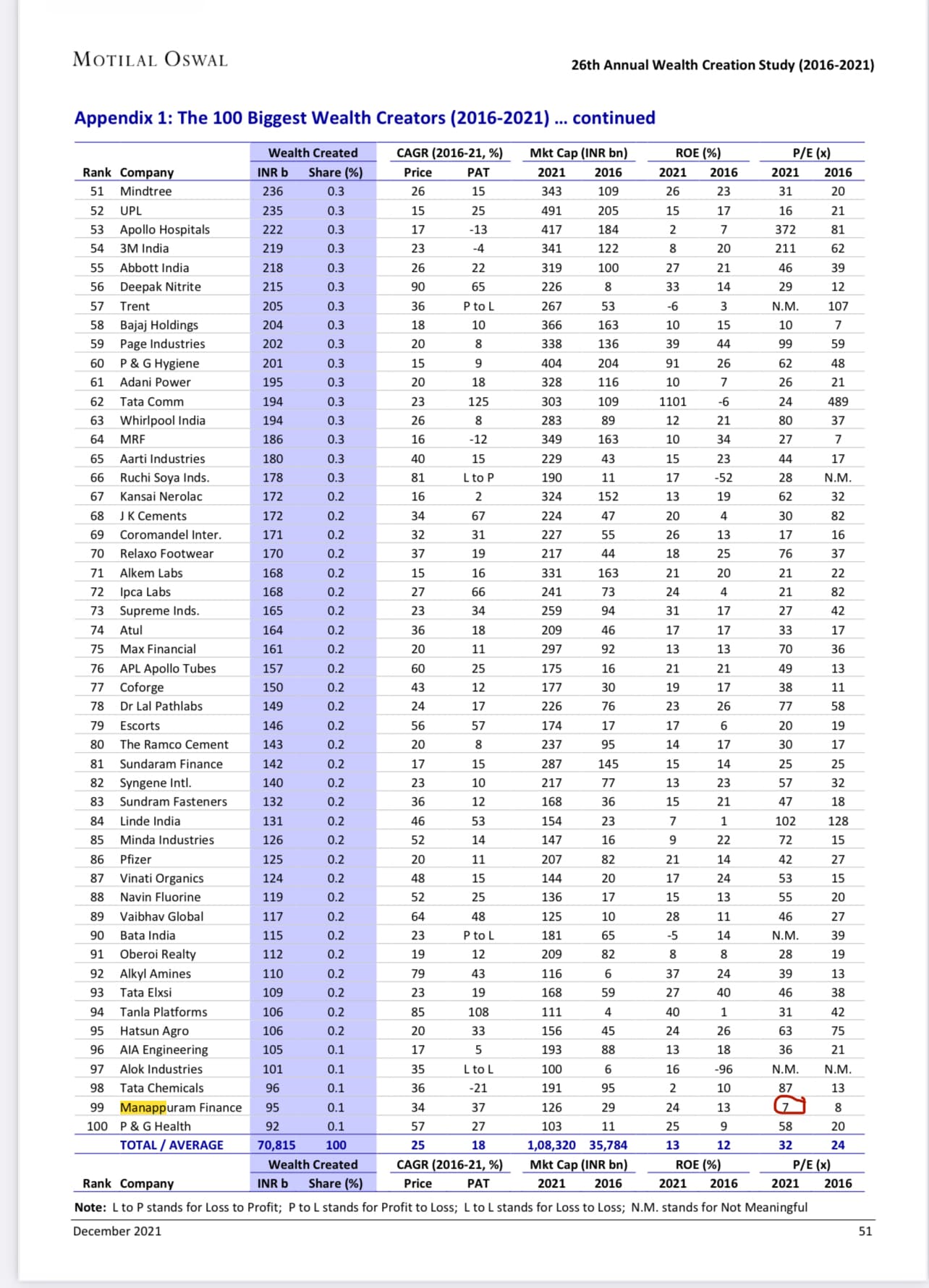

Manappuram in the “Motilal’s 100 biggest fastest and consistent wealth creators

list” with lowest PE

Gold loan by banks have doubled in last 1.5-2 years

Q3 results Not good results

Q3FY22 - Manappuram Finance

-

There was market slow down in December 2021.

-

Numbers:

-

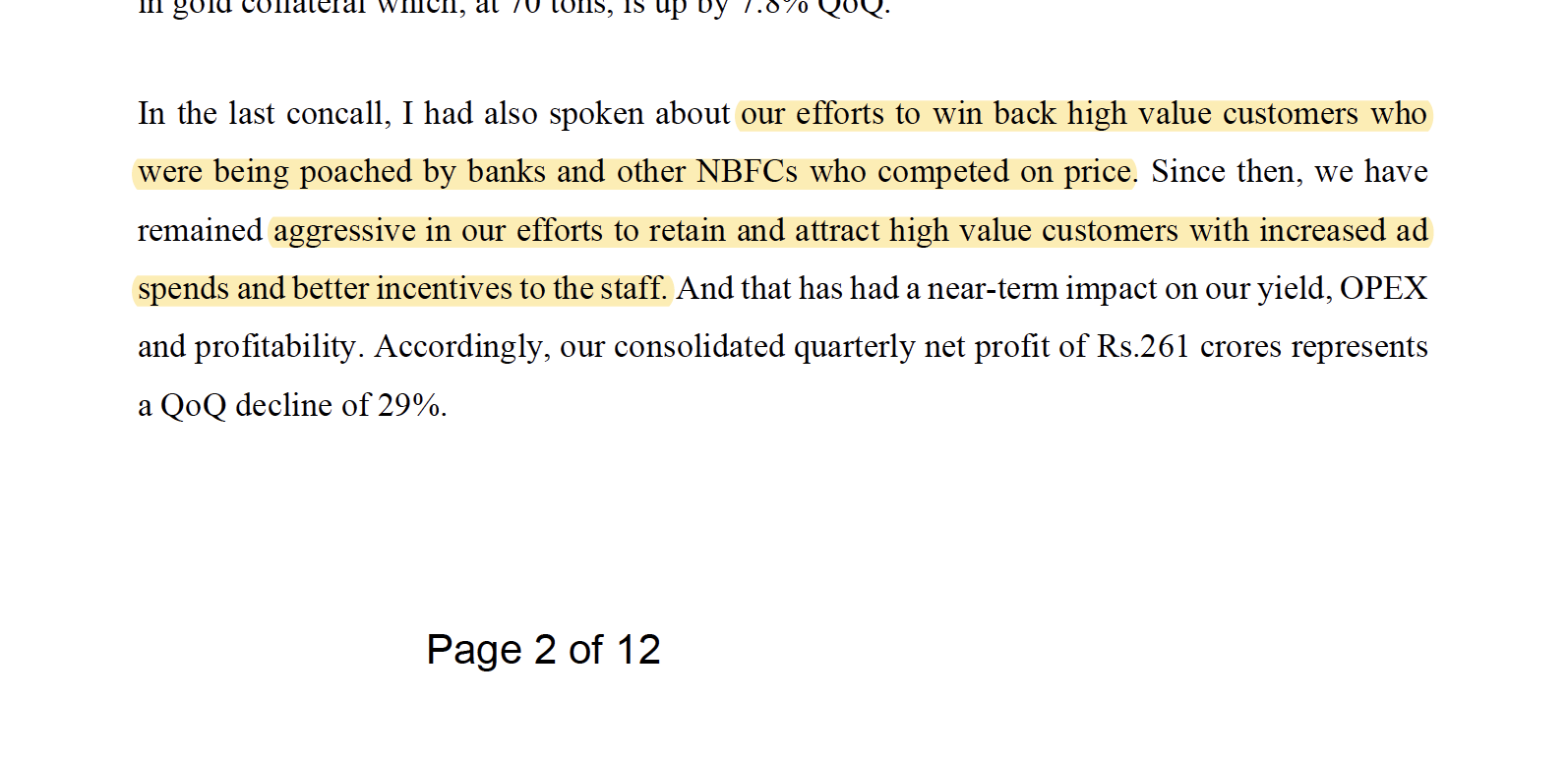

High segment customers which were taken by banks in few last quarters, they have able to retain and gain customer after reducing yield.

-

MFI Segment

- MFI saw a 2.4% decline because of their conscious decision to slow down disbursement in fear of third wave.

- For next 2-3 quarters there will be impact and then it will be normal provided no COVID variant or lockdown.

-

Advertising cost up by 170% QoQ and 300% YoY

- Spent 51cr on advertisement this quarter. (Used to spend 40-50cr annually in FY20 & FY21)

- Management said they felt the need for massive advertisement to provide a booster but it will not continue in coming quarters (not to previous level but lower than this).

-

Yield of Manappuram was higher compared to peers which led to loss of higher ticket customers. To bring them back they brought down the yield.

- Market average yield around 17% (NBFC in public market) and they plan to maintain it around 20-21%.

- Management feels that NBFC can’t sustain such rate and they will have to increase the rate.

- But going back to 25% yield is not ruled out.

- Market average yield around 17% (NBFC in public market) and they plan to maintain it around 20-21%.

-

Target of 10-15% growth but for the time being growth would be 1-2% lower per month because they don’t want to compete in terms of interest rate.

- 15-20% consolidated AUM growth is still possible.

-

In the month of January and February they are not seeing momentum in gold loan.

-

Q: Why would a customer come to Manappuram rather than peers or banks?

- Management’s answer: For long term borrower other players are better.

- But for short term borrower it does not matter and most of their customers are short term.

- The demand for lower ticket group has come down because they were affected the most.

- But for short term borrower it does not matter and most of their customers are short term.

- Management’s answer: For long term borrower other players are better.

-

Management believes competition from banks is temporary. One can check the business cycles for the same.

Thanks for sharing the summary. Appreciate it.

I was listening to Muthoot Con Call yesterday and noticed that they auctioned 2800 cr worth of jewellery (on approx disbursal of 50,000 cr loan book). This auction by Muthoot strengthens the argument that there is still a lot of stress in SME and rural community. Which also in a way corelates with lower growth in Q3 and lower expectations in Q4. The answer I am trying to find here is - is the muted Q3 growth really only due to covid and competition from banks and fintech (as called out by Muthoot management) or their core customer base itself is under enormous pressure and hence a combination of these factors means growth will be structurally muted for gold loan business for coming qtrs?

Also, if you noted loan auction numbers from Manappuram, would be great if you can share the same.

Elevated opex and reduced yields. The quality of growth is extremely important to judge. Not all revenues are created equal

1)Manappuram Finance Shares Drop 13% As Analysts Slash Targets After Q3 Miss

- concall audio

-

VP nandkumar on results

Growth In Non-Gold Loan | VP Nandakumar, Manappuram Finance - YouTube -

Motilal oswal

- Axis report

5)yes report

since last 2 years something or other is going wrong and profits are on declining trend

Here is my observation from Manappuram’s concall. Management mentions that gold loan demand was buoyant until November and then it suddenly disappeared for low ticket sizes (which offer higher yields).

To bring back AUM growth, company had to focus on high ticket size loans which comes at lower yields. On top of this, they offered extra incentive to employees to boost collections and spent additional money on advertising to try to boost demand.

This additional advertisement didn’t bring much fruit as there was no return of demand (for lower ticket segment) until February.

What I found interesting was the stock price movement in this time frame. Stock started falling from mid-November (which coincided with demand evaporation) from 220 levels to 145 in January. The next leg of de-rating below 140 coincided with the results. This probably implies that there are two set of market participants, one who got a whiff of this demand evaporation in November itself and the other ones who reacted post bad results.

Disclosure: Invested (position size here)

When other gold Nbfc is making 17% yield. Why should Manapurram continue to make 25%+ Yields? This is where incremental direction counts. Manapurram is likely to be a value trap as incrementally the return ratios will trend downwards with elevated marketing spends and reduced yields. Valuations are too cheap.

Let’s see how it goes.

Disc;- not invested in manapurram.

Found something interesting on Twitter:

Basic number presentation

Not a video specifically on Manappuram Finance but has its comparison with Muthoot and IIFL from 21:00 onwards. Decent video

Staffers of Manappuram gold finance held for fraud.

The rating reaffirmation continues to factor the experience of promoters and professional management, Manappuram Group’s established track record, healthy asset quality, comfortable capitalisation, strong financial profile and adequate risk management and management information systems. The rating is, however, constrained by the inherent risks associated with the gold loan and non-gold loan portfolio, coupled with regional concentration risk.

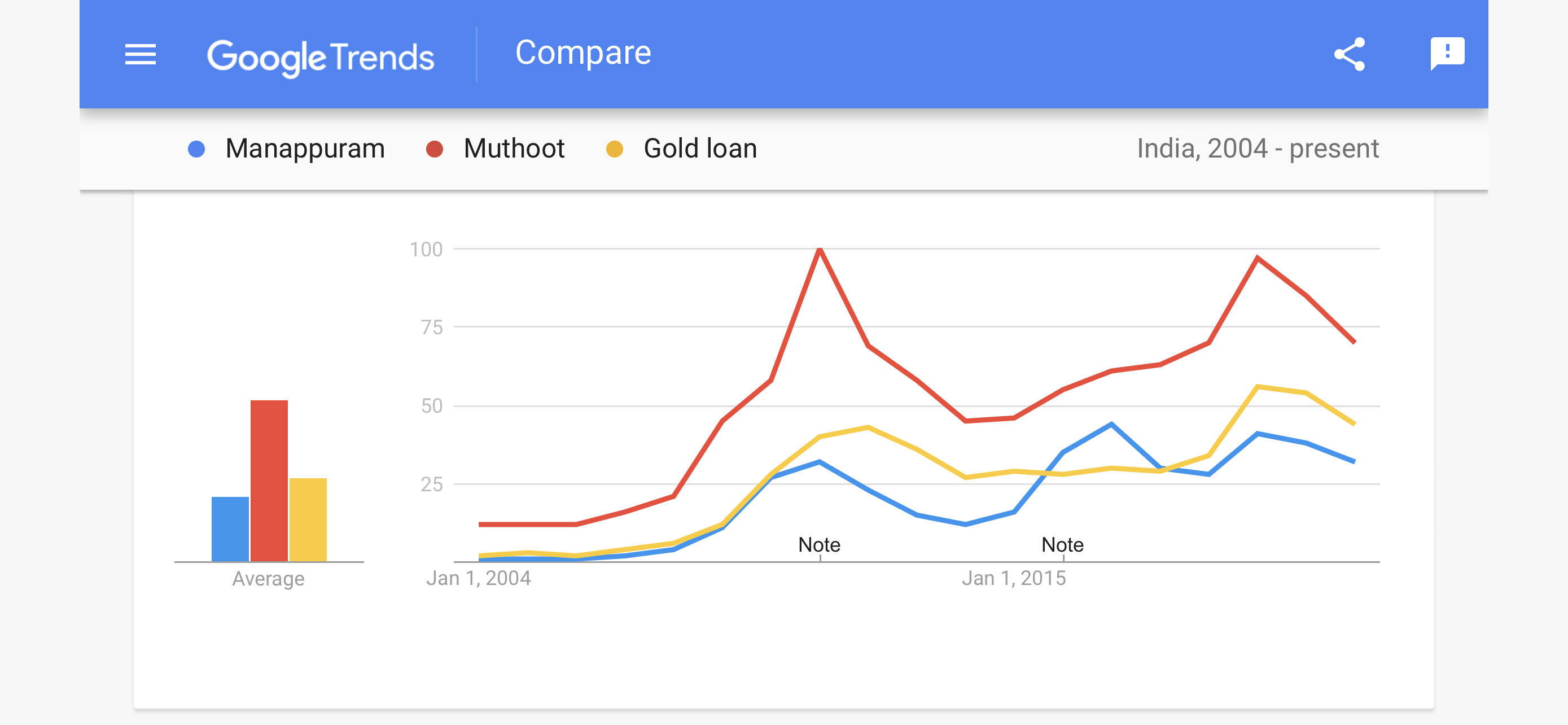

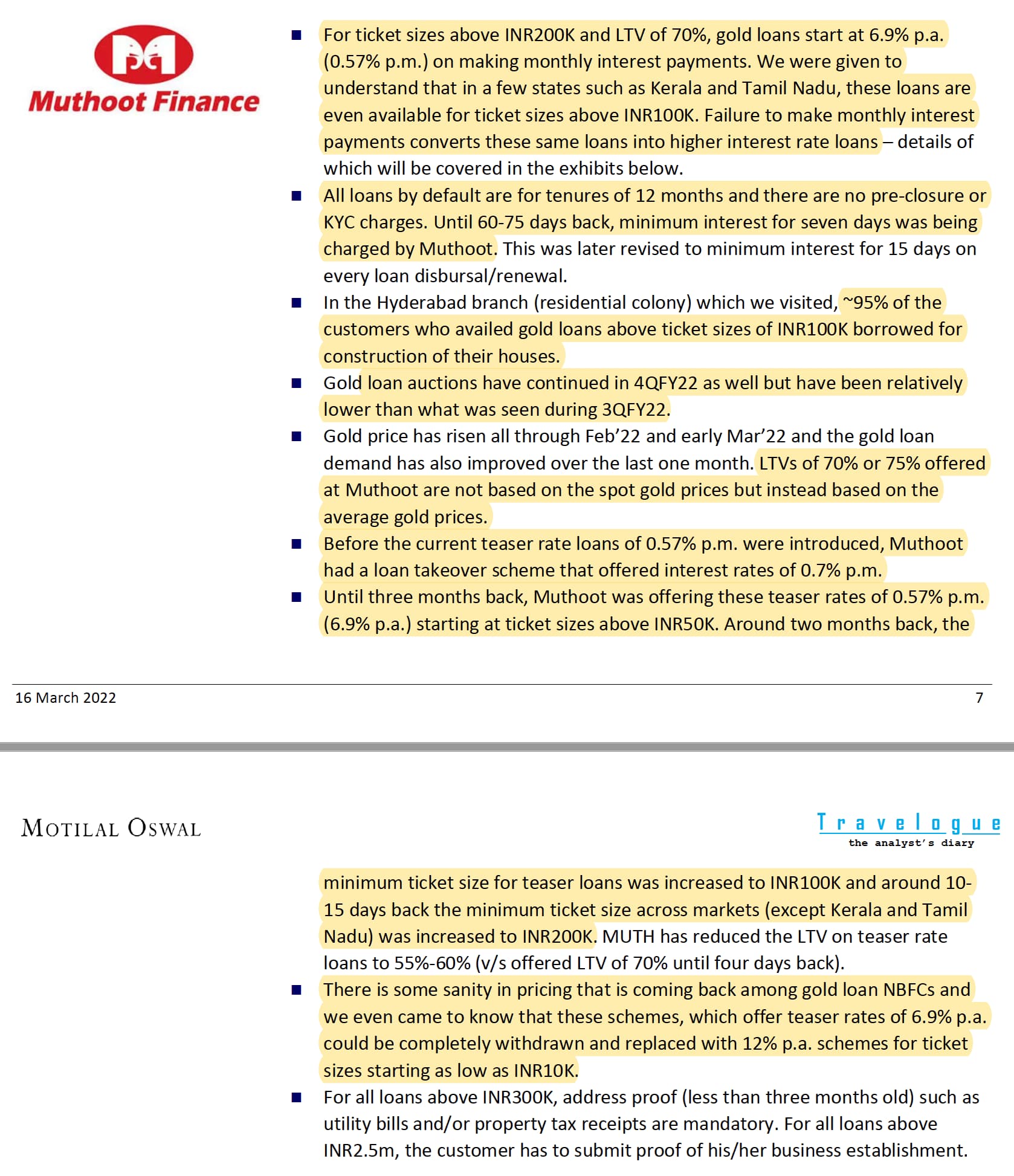

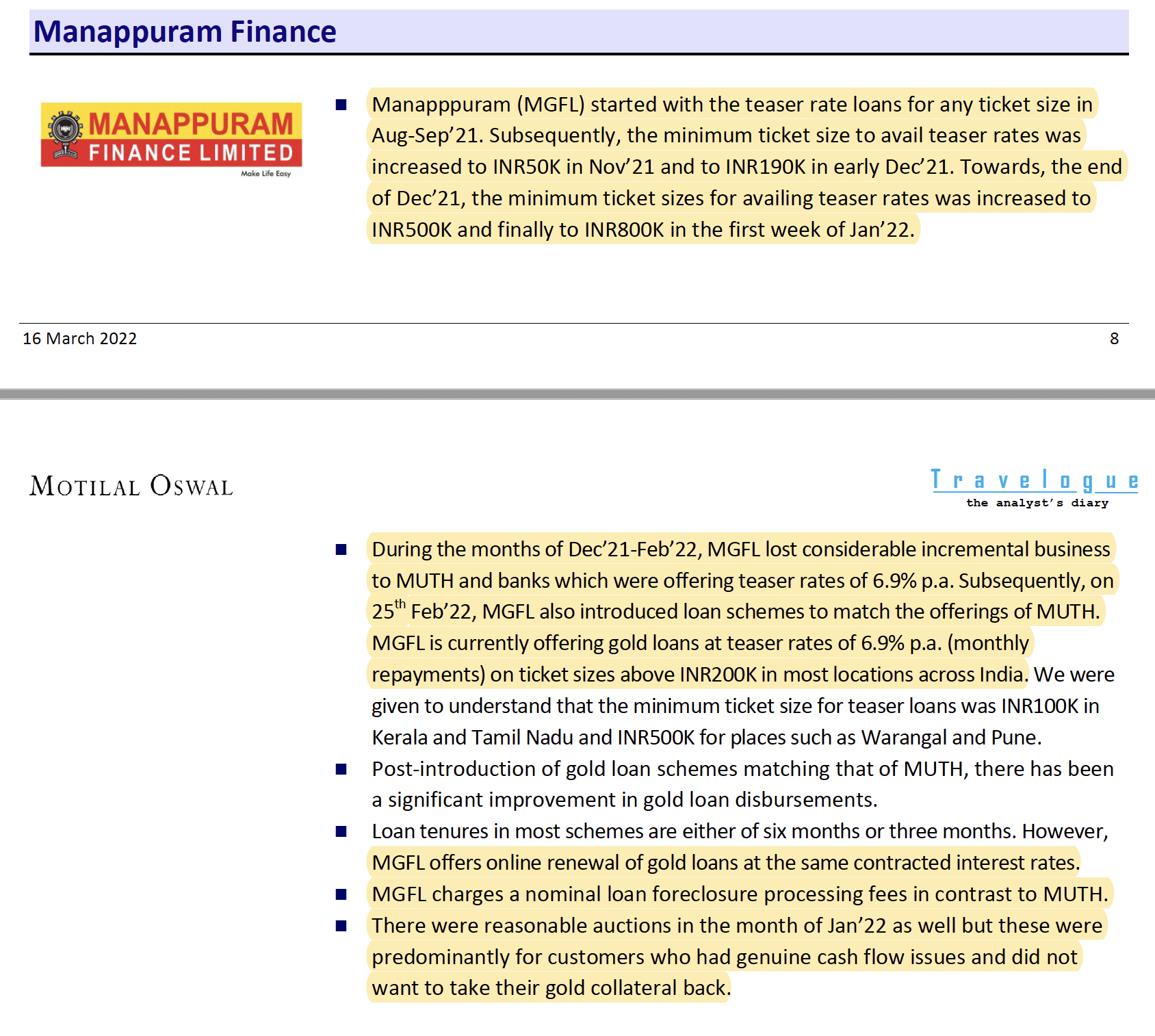

Very interesting field visit report (Hyderabad and Vizag) from Motilal about competition among gold loan NBFCs, I have attached the relevant excerpts at the end.

Summary: Competition is intense between Manappuram, Muthoot and IIFL. Each company is trying to poach high value customers by offering very low teaser rate loans (0.6% monthly interest) which are applicable if one pays monthly EMI. Apparently, 75-80% of customers who take these teaser loans end up not paying monthly interest and are moved to a higher interest rate slab. There is lot of flip flop happening where companies are changing the terms and conditions of these teaser rates abruptly resulting in very high balance transfer for high ticket sizes. Basically, these high ticket customers do not have any stickiness and have a plethora of options to avail loans.

Disclosure: Invested (position size here, no transaction in last 1-month)