Customers can renew the loans indefinitely by periodically settling the interest and resetting the principal to the prevailing gold price. This avoids the risk of a compounding interest piling up over the course of the year.

However, we must acknowledge that the gold loan sector cannot hope to be fully immune to the vagaries of the wider economy.

Non-bank financial companies (NBFCs) specialising in gold loans could see assets under management (AUM) rise 18-20% to Rs 1.3 lakh crore this fiscal, Crisil Ratings said on Tuesday. This would be despite a contraction in the first quarter, when the pandemic-driven lockdown measures hindered branch operations and kept potential borrowers away.

Gold Finance is comparably safe and emotional business too

Business still available at lucrative valuations

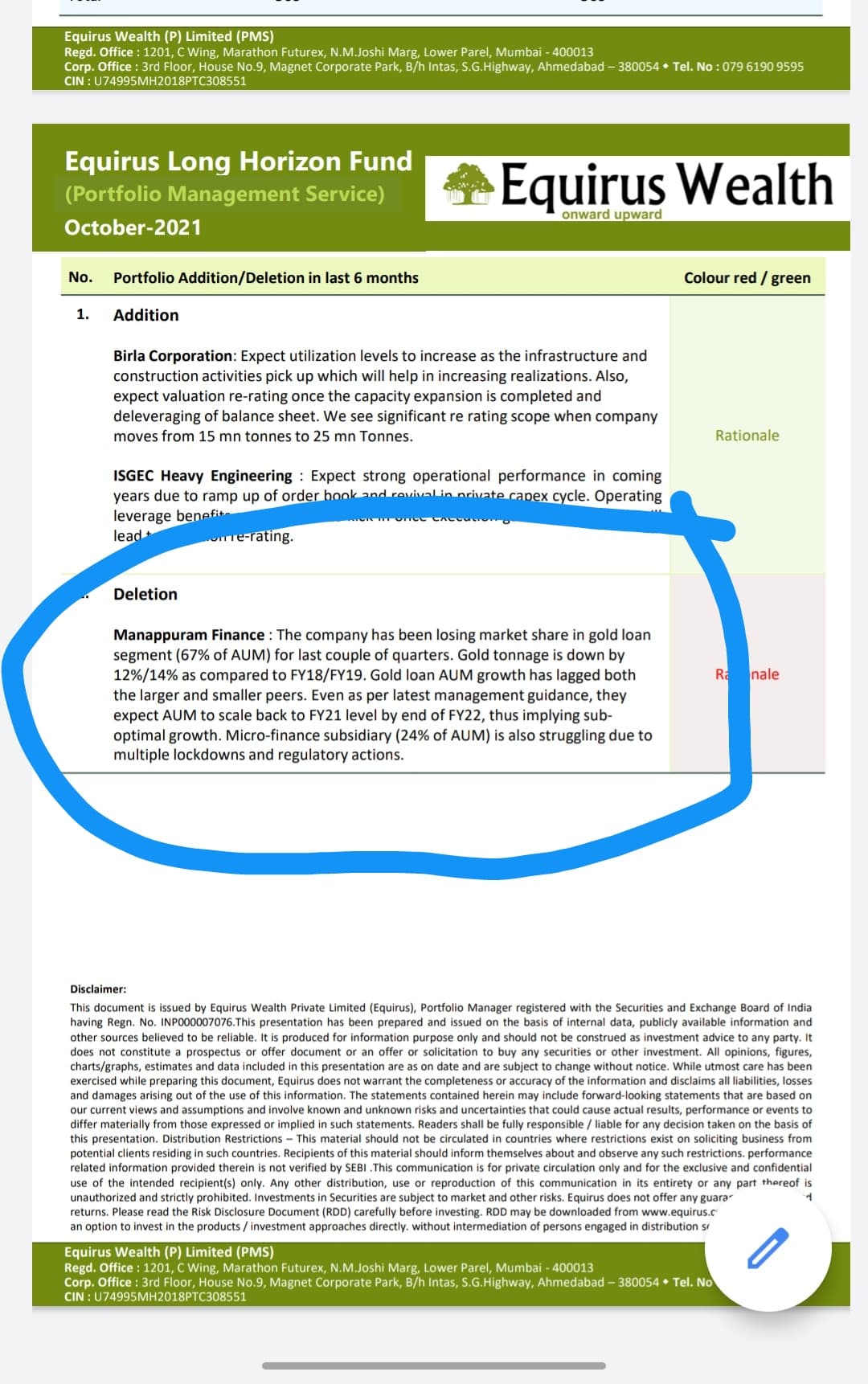

We have seen many coverages & Report on sectors & Co’s specially Manappuram.

Risk reward highly favourable from here

Good report .Eventually market will recognise Manappuram as well diversified business with better safety profile .And one day it will get better valuations and will get rerated .Till that time expecting 15-20% price gains per year which also is not bad .

It’s amazing how good all analysts are in copying each other’s reports .All brokerages will have almost similar projections .Genuine research is very limited .Also most of the times research report mirrors the price trend .

Good reports start coming after good price action

I guess reverse should happen .

Standard and Poor’s (S&P) has upgraded Manappuram Finance Ltd’s long term issuer rating from “B+” to “BB-” on the expectation that it will continue to perform better than its NBFC peers over the next 12 months.

The company’s core earnings are likely to remain at more than 5% of its average managed assets during this period. This ratio is one of the highest among its rated peer

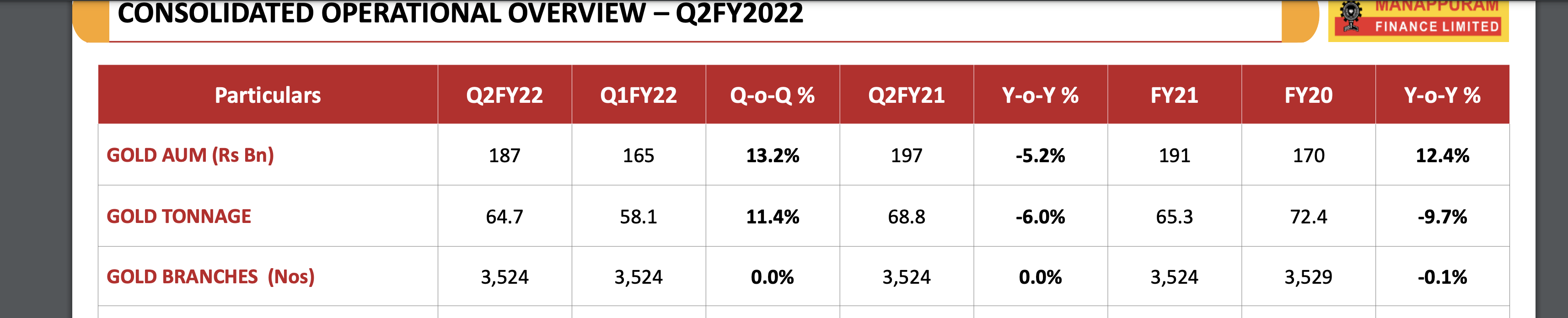

This was expected as there was 15% AUM reduction in last quarter. And analyst’s expectations were that it would take almost whole year to reach FY21 AUM (Refer to screen shot below).

But surprisingly, they have came back to FY21 AUM, within a quarter which shows that management is walking the talk, This will boost the stock price on monday.

Thank you for the report post, i read the investor presentation post that, happy to see AUM growth coming back. MFI has also bottomed out,

They hired employees for marketing which resulted higher employee benefit expenses.

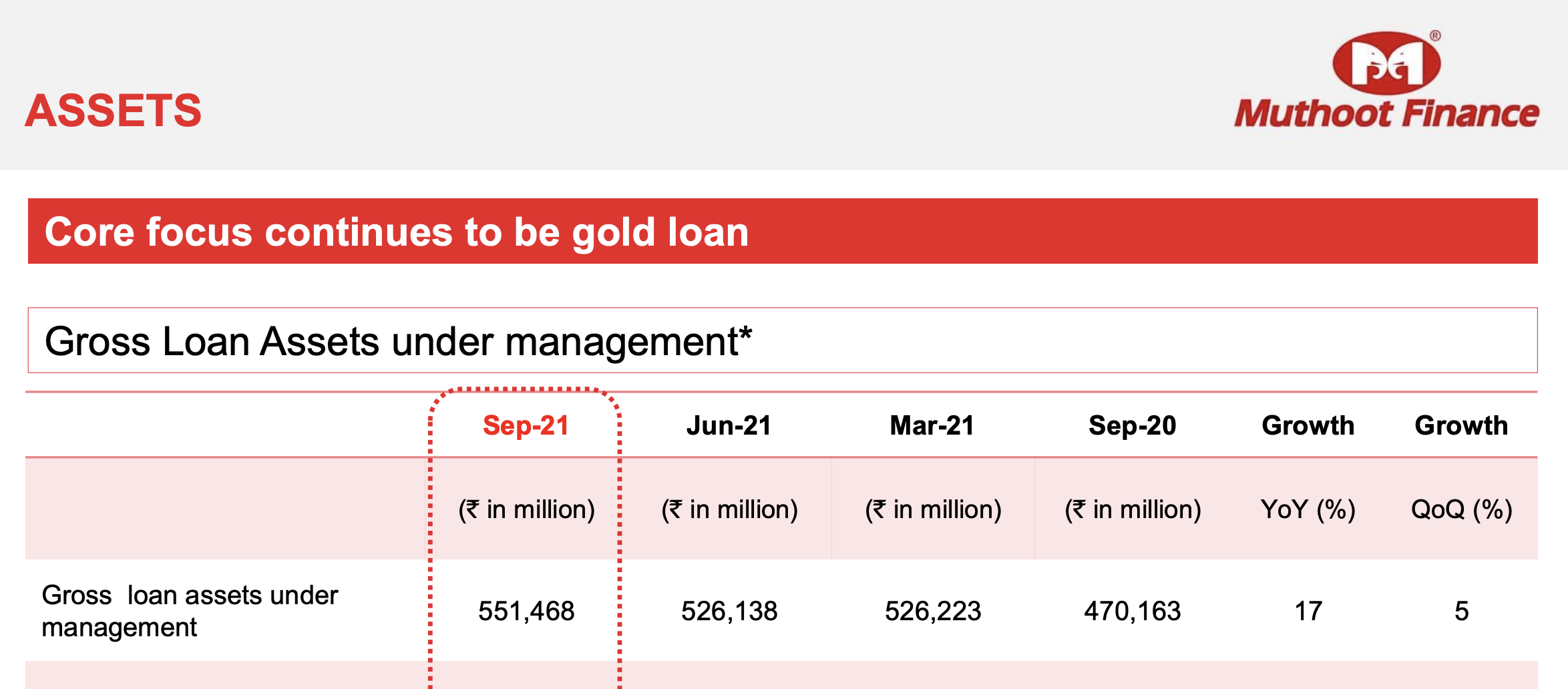

But MFI AUM is bit worry. They increased AUM by more than 1000 Crores in single quater and this lowered the CRAR to below 20%. Not sure how they handle if wave 3 happens And even with such an increase in AUM, asset quality showing higher stress in 0+, 30+, 60+ buckets. If they didnot increased their AUM, this may even look worse

But I think there provisioning is very good as well in case 3rd wave hits. And even in case 3rd wave hits in pockets of India, there geographical diversification is also quite good for them to not worry too much. However, if 3rd wave doesnt hit, I think there is rerating waiting to happen as Asirwad I feel is not currently valued same as other MFIs. I think the potential upside is much than downside.

Disc: Invested. May add if I find current opex in marketing justified .

Manappuram has done the right thing for long term by increasing the Marketing spend and trying to retain or grow the market share. This will lead to short term pressure on profitability. Don’t think it is as strong a franchise as Muthoot and an upcoming IIFL finance seems to be better placed than Mana.

Disc:- Not invested. Sold after they started losing market share and thinking about 2nd&3rd order consequences

i increased my allocation in muthoot after they started losing market share to peers…

i still feel its a very good business to be in…but being focussed in gold loans only is probably more rewarding and maybe thats wut makes muthoot stand apart from all others…

even the management strategy of “not auctioning client’s gold until very necessary” has proven to be the right one…and helped gain customer’s trust…

with manapuram now following suit by increasing period from 3 months to 6 months….actually confirms that muthoot strategy is a good one