To me muthoot looks risky with 6-12 month loans as compared to manappuram with 3 months

3 Likes

Someone shared an unconventional way to store gold. They pledge their gold and take online gold loan from Manappuram for minimum Rs 1000/- which they pay back with interest of Rs 5 within a week. They get to keep their gold in safe locker which is insured plus option to take instant loan from the app in the future. They keep renewing it every 3 months in the app and no need to visit the branch except first time.

It seems gold loan companies are ok with it since it increases their AUM.

2 Likes

So you will pay greater 24% (5 per week is 20 per month which is 240 per year) interest per year to keep your gold with gold finance company?

How does that make sense?

@vnktshb Main purpose is to get a cheaper locker and not a loan. They wont pay interest rate for full year. They repay the loan in a week itself and need not to pay interest for further days.

Yup. I can confirm this happens in my town as well.

2 Likes

Rs 5 is paid within a week for a loan whose tenure is 3 months so Rs 20 per year would be my calculation. I am not sure of the fine print of the loan. Even your calculation of Rs 240 per year is cheaper than bank locker annual charges. My point was the AUM figures may not be completely accurate if there are large number of such folks.

AUM will be accurate, whatever they report as Gold in Tonne will be inaccurate

2 Likes

Here are the updated gold AUM and auctions for FY21 and how it has varied over time across gold financiers.

| AUM (in cr.) | FY13 | FY14 | FY15 | FY16 | FY17 | FY18 | FY19 | FY20 | FY21 |

|---|---|---|---|---|---|---|---|---|---|

| Muthoot finance | 26’000.04 | 21’617.90 | 23’349.90 | 24’335.50 | 27’219.90 | 28’848.40 | 33’585.30 | 40’772.40 | 51’926.60 |

| Manappuram finance | 9’945.80 | 8’155.20 | 9’269.30 | 10’080.60 | 11’124.53 | 11’734.98 | 12’961.52 | 16’967.18 | 19’077.00 |

| Bajaj finance | 37.39 | 146.78 | 543.96 | 655.01 | 853.37 | 1’557.49 | 2’239.97 | ||

| SBI | 900.00 | 2’179.00 | 20’987.00 | ||||||

| HDFC Bank | 4’042.00 | 4’057.00 | 4’531.00 | 4’800.00 | 5’500.00 | 5’900.00 | 6’200.00 | 8’300.00 | |

| Shriram City Union | 4’787.00 | 2’453.00 | 2’943.00 | 3’408.00 | 3’427.00 | 3’374.00 | 2’712.00 | 3’119.00 | 3’789.00 |

| IIFL | 3’865.00 | 3’912.00 | 3’790.00 | 2’914.00 | 2’910.00 | 4’037.00 | 6’195.00 | 9’125.00 | 13’149.00 |

| Federal bank | 6’360.00 | 5’962.00 | 6’524.00 | 7’228.00 | 9’301.00 | 15’816.00 | |||

| CSB bank | 2’958.00 | 3’799.00 | 6’131.00 |

| Gold auctions (in cr.) | FY13 | FY14 | FY15 | FY16 | FY17 | FY18 | FY19 | FY20 | FY21 |

|---|---|---|---|---|---|---|---|---|---|

| Muthoot finance | 3’429.31 | 2’787.90 | 3’880.00 | 1’184.70 | 2’517.68 | 1’400.05 | 854.78 | 325.48 | |

| Manappuram finance | 1’301.30 | 2’284.70 | 1’188.00 | 1’932.00 | 929.00 | 1’204.50 | 419.40 | 116.10 | 412.25 |

| Bajaj finance | 6.29 | 18.79 | |||||||

| Shriram City Union | 50.21 | 17.85 | 32.48 | 10.42 | 3.07 | 0.37 | |||

| IIFL | 159.06 | 148.76 | 308.33 |

| Auction % of AUM | FY13 | FY14 | FY15 | FY16 | FY17 | FY18 | FY19 | FY20 | FY21 |

|---|---|---|---|---|---|---|---|---|---|

| Muthoot finance | 15.86% | 11.94% | 15.94% | 4.35% | 8.73% | 4.17% | 2.10% | 0.63% | |

| Manappuram finance | 13.08% | 28.02% | 12.82% | 19.17% | 8.35% | 10.26% | 3.24% | 0.68% | 2.16% |

| Bajaj finance | 0.40% | 0.84% | |||||||

| Shriram City Union | 1.47% | 0.52% | 0.96% | 0.38% | 0.10% | 0.01% | |||

| IIFL | 2.57% | 1.63% | 2.34% |

Auctions went beyond 15% of outstanding AUM in the last cycle, this time it has been much more controlled across NBFCs. Banks are not obliged to share this data in their annual reports.

Disclosure: Invested in Manappuram (position size here)

19 Likes

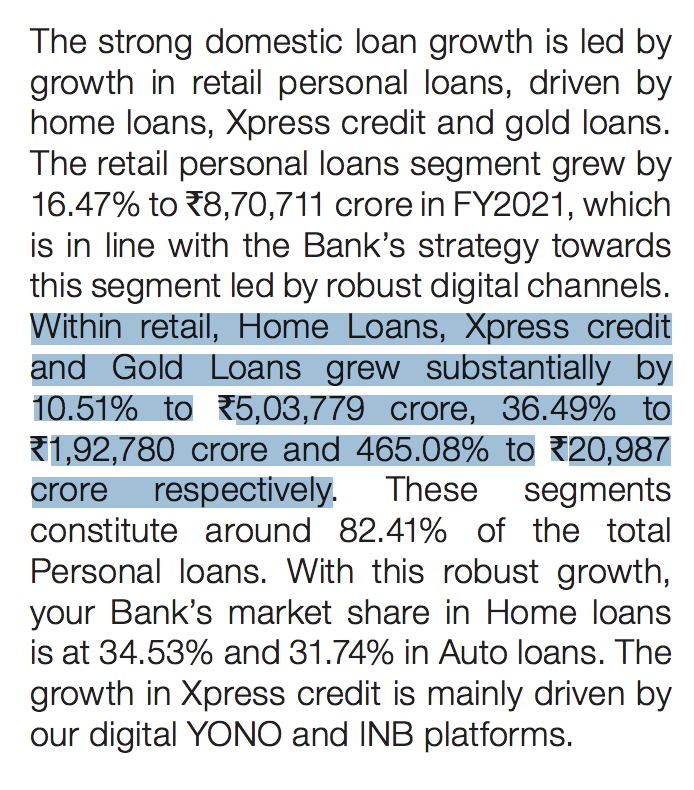

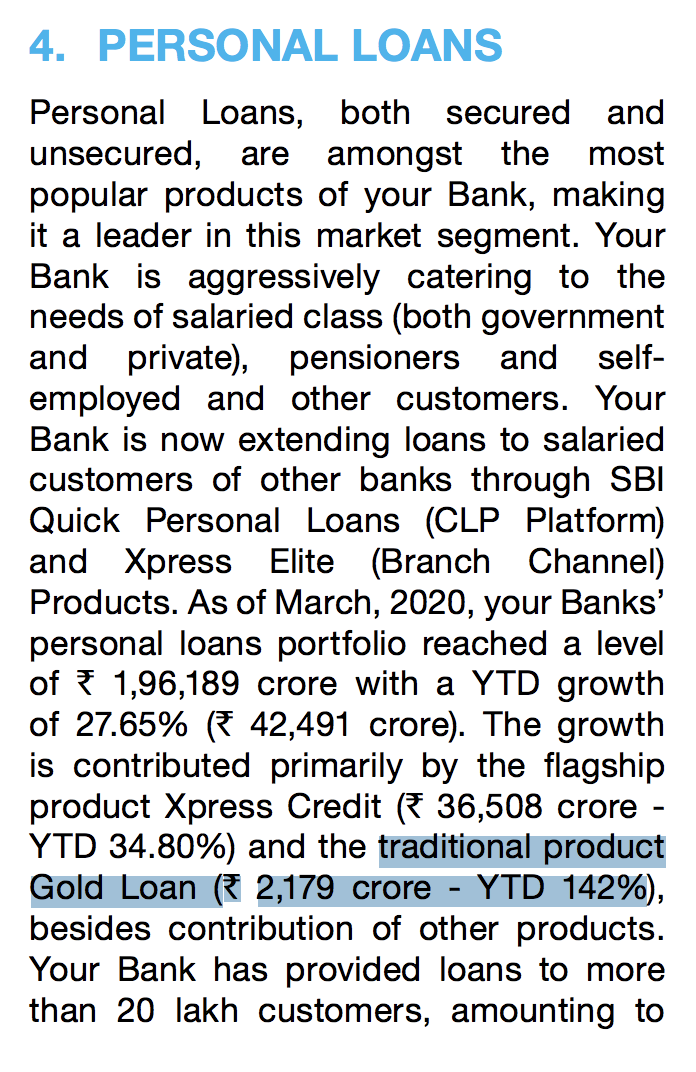

Hi Harsh,

Thank you for sharing the data above. Just wanted to confirm if the data for SBI gold AUM is correct. Unbelievably aggressive growth.

SBI provides many types of gold loan - personal gold loan, agri gold loans, SME gold loans, gold loans to jewellers, etc. I have shared numbers reported in their personal (or retail) loan division.

FY21

FY20

1 Like

1 Like

https://www.fitchratings.com/research/non-bank-financial-institutions/fitch-affirms-manappuram-finance-at-bb-outlook-stable-14-09-2021

On the qualitative aspects, we believe MFIN carries greater key-person risk due to the significant involvement of the founder. This, along with a history of compliance lapses, suggest greater governance risks relative to higher-rated peers, although MFIN has strengthened its practices in recent years and continues to do so.

MFIN has ESG Relevance Scores of ‘4’ for Customer Welfare and Governance Structure, due to a record of business practices, including customer-related activity, that did not fully comply with regulatory norms in the past - although MFIN has taken steps to improve governance and compliance in recent years. The scores reflect our assessment that governance and customer-related practices appear weaker than rated peers’, raising regulatory and reputational risk for MFIN.

2 Likes

Fitch Ratings - Singapore/Mumbai - 14 Sep 2021: Fitch Ratings has affirmed India-based Muthoot Finance Limited’s (MFL) Long-Term Foreign- and Local-Currency Issuer Default Ratings (IDRs) at ‘BB’. The Outlook is Stable.

MFL’s high exposure in loans against gold collateral - 90% of consolidated loans at end-June 2021 - supports its asset quality,

perational risks are high in gold-backed financing due to the branch-led business model and physical handling of gold collateral. Such risks may arise from decentralised cash handling, collateral safe keeping, and lending against stolen or spurious gold. Constraints due to Covid-19 pandemic containment measures had a temporary effect on MFL’s operations. Various checks and balances and the company’s decentralised branch operations mitigate the operational risk.

I want to put my observations on rupeek as under

Does anyone trust and give their gold to a sales representative visiting their home??

@Vikky9995 In my point of view, I can trust the person when I get message/notification from loan provider that so and so representative will reach me for gold collection and I get update in loan provider portal that representative collected my gold before he is moving out of my house with my gold.

I am not sure how rupeek works, but if gold collection works in similar manner, i can trust him

2 Likes

Then the risk is on rupeek, if delivery person cheats rupeek has to compensate the loss.

But most of the Indian people won’t like it, they want to see their gold safe and secure in a bank/nbfc locker…

Yes, They have to bear theft loss while transit either by employee or a thief. This is common, even when you look at microfinance companies they have this risk. But they can manage this, they wont let a single employee to do large gold collection. There is a risk, but a manageable one.

When it comes to people trust on this model, On seeing how our country is changing last 5 years, People can adapt this model. I think Rupeek has high chance of success

Rupeek does not store gold, Gold will ended up in a nearby bank locker.

Customers can renew the loans indefinitely by periodically settling the interest and resetting the principal to the prevailing gold price. This avoids the risk of a compounding interest piling up over the course of the year.

However, we must acknowledge that the gold loan sector cannot hope to be fully immune to the vagaries of the wider economy.

2 Likes

Non-bank financial companies (NBFCs) specialising in gold loans could see assets under management (AUM) rise 18-20% to Rs 1.3 lakh crore this fiscal, Crisil Ratings said on Tuesday. This would be despite a contraction in the first quarter, when the pandemic-driven lockdown measures hindered branch operations and kept potential borrowers away.

4 Likes