That was exactly my concern because of which I was not confident in accumulating Manappuram which was not the case with Muthoot

Gold Loan Specialized NBFC probably had best Tailwinds in Industry (Balance Sheet Side) because of appreciation in Gold Prices which made it easy to grow loan book with control NPA, In such situations I was expecting Gold loan NBFC to perform far better then other competition (Despite Banks having 90% LTV) in such situations Muthoot was able to beat competition but manappuram lagged in it that actually showed me that their competitive advantage is not that strong compared to past. I personally think that focus on niche is most important characteristics gold loan NBFC should have in order to thrive excess competition which is going to come in near term from Rupeek & Banks.

One key characteristics i am very close tracking is “Loan Book and Tonnage per Branch” actually as you might be aware all these supernormal profits are because of Incremental Sales per branch YoY basis as all this incremental loans per branch are directly going in bottom line, Manappuram was lacking in this aspect compared to Muthoot (I dont know why they are not able leverage existing branches like Muthoot despite significant brand awareness, if someone can throw some light on it will be really helpful)

If you look beyond numbers, Muthoot management has given clear indication that they will reducing branches in south and they are consolidating branches (25% of loan book is from south where there are 45% of total branches) consider if branches starts consolidating which is likely to be the case then kind of operating leverage that can play in them.

Manappuram is also really interesting bet even if they find it difficult to grow loan book in near term, all potential downfalls are compensated with attractive valuations, If Manappuram can increase their per branch efficiency (Brand is already available to do it) and micro finance division well it has potential to become well diversified and moated NBFC and even if that doesn’t play out current valuations wont put big dent on principal capital. I will like to observe Manappuram for now and add as business quality becomes better and more competitive in Industry (Returns are made when ugly duckiling turns into a Swan) and @Worldlywiseinvestors congrats on 100K of SOIC keep growing and keep educating Investor.

Disclosure: Please do your own due diligence (Biased & Invested in Muthoot) and I am not SEBI Register Advisor

Manappuram has grown its gold AUM at CAGR 15% over last 4 years and Muthoot by 17%. Muthoot has much better operational efficiency. Manappuram has the better MFI. Both have same cost of borrowing and similar liability mix. Manappuram has less risky assets due to nature of their product (short term). This means that stress is identified on their PnL much before it happens for Muthoot (hence disparity in Q1 metrics). Muthoot gets the chance to average them out over the entire year and has to deal with lesser auction/ unit AUM. But auction as far as I understand has never been a problem for either. And as Manappuram MD said, 80% of customers whose gold is auctioned do come back for more loans due to transparency. From branding point of view, both do extensive branding with expensive stars, both regional and national.

A little scuttlebutt: My town houses both. I’ve talked to a few rice traders who take some loan to buy rice during harvest from farmers. They say they take loan from whoever they feel like. Little difference in experience and taking loan from them is extremely easy. Before they took loan from local lenders (sahukar) at Rs 6000 rupees for every Rs 5000 every 2 months.

These factor according to me does not warrant almost double valuations for Muthoot. Either Manappuram is cheap and Muthoot is fairly price or Muthoot is expensive and Manappuram is fairly priced.

While AUM (tonnage) for Muthoot dropped by ~3% from FY2020 to FY2021, manappuram AUM(tonnage) dropped by ~10% for the same period. Now the questions are:

Is this because of aggressive auctioning by Manappuram

Auctioning can also be due to short term nature of Manappuram lending.

Both are partially true in my opinion. Muthoot auctions after 1 yr of NPA and Manappuram after 3 months. So an maximum non performing tenure for Muthoot is 2 year and Manappuram is 6 month which is 1/4th of Muthoot. This means that in Muthoot customer gets longer time to save her gold. One may think that this is sentimentally more attractive but on the other hand NPA is very less. So for majority of customers , it may be the other way round whereby they do not want to collateralize their gold for long and opt for short tenure loan. I must say these opposing arguments have create not very much growth differential between the two companies and both are doing pretty well without being compelled to change their strategy.

For me, if Muthoot and Manappuram have same valuations, I’ll choose Muthoot because it has operating leverage. Otherwise there’s not much to choose. Manappuram is a little safer from credit quality conservatism point of view plus their MFI business is better.

VP Nandkumar confident of 10-15% growth in gold loan and 20%CAGR on consolidated basis with 20%ROE

MIX REPORTS BY ANALYST POST Q1 RESULT 10 Aug 2021

Motilal - BUY TP 220

Arihant - Hold TP -201

Brokerage firm Motilal Oswal Financial Services has maintained a buy call on the stock after the Q1 numbers, with a target price of Rs 220.It is poised for a decent consolidated AUM CAGR of nearly 13 percent over FY21–24E," Motilal Oswal said.

Arihant Capital has downgraded the stock to ‘hold’ from ‘buy’ with a revised target price of Rs 201 from Rs 197 earlier, based on 1.6 times FY23E P/ABV.

Positive things are : clean management ,demand picking up ,risk management good ,good ROE ,good dividend yield ,management identified gaps and working on them,slow and steady approach, valuation not expensive

Negative things are : growth slowing ,competition ,gold price fluctuations ,covid

I believe the best days for Manappuram are behind. The fact that non-gold book is now ~30% of its AUM shows that gorwht in its core business is slowing, and that was vindicated by a sharp fall in the gold tonnage. The competition in gold lending is heating up, and many SFBs and small Banks (like CUB, Federal) are pursuing it. Given their cheap cost, it would pressurize the NIMs.

Moreover, I have some doubts in their MFI and Affordable Housing book. The entire industry has seen sharp growth in NPAs, barring Manappura. There could be some element of evergreening. That’s just my opinion, and I could be wrong. But one thing is clear Manappuram is steering from gold loans and venturing into segments where it was absent hitherto… So, if I want to play those segments I would bet on compaines who are expert in the domain, and if I wnt to play gold I would turn to Muthoot. So, I believe Manappuram is at a point of no where at the moment.

Alternative is as we go near main event of when US rates rises then Gold prices will fall. So this reduced goal loan portfolio can act as blessing in disguise. Gold prices are already under pressure. Management has good experience in gold loan and still they are not aggressive and not defending their gold loan turf.

With almost 30 trillion in debt. How will US service the debt in a high interest scenario. Also inflation is very high (5%)which should aid gold prices. Most real assets including gold are cheap. Ofcourse with yields touching 1.2℅ gold should be at 2000$ . I think its a matter of time and price should catch up after 1 yr underperformance.

There is huge unorganised gold loan market in India .Market is worried that other NBFCs and banks will take Manappuram’s share .Or may be everyone will take some share from unorganised sector and all will grow. I feel there is enough pie for everyone with focussed approach .So all those with focused approach will grow.But can everyone maintain the focussed approach .History tells us no .Why ? I think the main reason is huge operational issue .Not a easy business to grow steadily .Only few like manappuram and muthoot have succeeded.Other players come during boom and disappear during bear phase .But many feel this is a different time and things will change .Probably not ,but I may be wrong .

Both are growing in almost some rate with few small differences over long timeframe.

Coming to valuations ,current valuations with PE <8 and P/BV < 2 means market is assuming more bad is coming .Some are even saying that manappuram thesis/business has collapsed .But will it happen? Thats where we have two groups ,one assuming muthoot will keep growing and manappuram keep degrowing/slow growing .Hard to digest this as both businesses have almost same model of convenience ,i.e u get loan instantaneously with trust and reliability .One group is happy to pay double premium to Muthoot and other sticking to comfortable manappuram valuations.I belong to later group .Lets see …

Anyhow such polarised views keep market interesting and keep creating opportunities on both sides

Does anybody have any insights on the threat of online gold lenders like Rupeek to the Manappuram and Muthoot? Doorstep distribution and minimal turn around time are both part of Manappuram.

Thanks @ChaitanyaC for posting the Finshots article, I was about to post the same when I read few days back but got some other work

So IMO, the reason why its trading at double premium is :

Muthoot is trading double the premium of Manappuram is because Muthoot is rather taking a conservative approach and consistently delivering it. Whereas Manappuram is aggressive and their plans are often disrupted by the external factors like in 2013 and 2020 covid crisis as mentioned in the above article especially refer the Manappuram profits hugely came because of auction. But they constantly agile and trying to stay competitive is really good.

Obviously both are good companies for long term. But for myself, I can be aggressive on any other sector but particularly when it comes to Banking and NBFC space I am slightly conservative. So When NBFC sector already have an issue of loans being not repaid, conservative investors happy to pay double premium to Muthoot.

So Manappuram fanboys don’t come and post 100 articles and PPTs to bash me saying that its the best. I am not saying or talking about which is best or worst.

Muthoot (for conservative investors) , Manappuram is for aggressive Investors. Period.

The document posted by @Vinay_T_M was really helpful.

Page No: 6 last question have the answer for you.

Finally for the above Business Standard article,

UBS tells to “get out” but in the last para of the article “Others are more optimistic and Goldman Sachs Increased the Target”

But this newspaper guys wants to panic you with the negative title.

So “News” and “Noise” are 2 different things where an Investor need to understand which needs to ignored and which needs attention. – Said by “Who knows”

So for long term investors of Muthoot or Manappuram, we can classify as “Noise”

Just read this how much gold delivered since Independence. Though I prefer Equity over Gold, I have 5-10% for hedging purpose.

In my view, Rupeek will garner some market share for sure. However, for Mutooth/Manapurram, it will not be a rocket science to aggressively compete with Rupeek on door delivery model.

One more issue I see with Rupeek is, it has to again depend on banks for the last mile connectivity with the customer. How practical/fast it is?

I think valuations will fluctuate and some years muthoot gets premium and few years Manappuram will get premium .This is because of fluctuations in their growth in short term but it will even out over long term .Thats how i see and I may be wrong .

And most likely eventually both will get rerated for established well run NBFCs

I will wait another year to see change in valuation premium

Housing Finance: Average loan size of Rs.1.5 million

Forex and money transfer

No bank account needed for amount up to ₹ 50,000

• Send cash anywhere in India within seconds

• Send money abroad

• Authorised Dealer Category – II Licence from the RBI

Our consolidated AUM grew by 7.92% to ₹ 272.24 billion, and net profit improved by 16.53% to ₹ 17,249.5 million, the highest ever.

Non-gold verticals now account for 30% of our consolidated AUM and contribute 21% of consolidated net profit.

We have delivered attractive returns to our investors with ROA of 5.61% and ROE of 26.17%. Our standalone capital adequacy ratio is at a healthy 29.02%.

From the peak of US$ 2,000 per troy ounce in August 2020, the price has fallen to levels of US$1,700.

Learning from previous episodes of gold price volatility, we realised that a short-term gold loan product is the best way to manage the gold price risk. Accordingly, we shifted

almost the entire gold loan portfolio to a tenure of 3 months, a departure from the industry practice of granting gold loans for a tenure of 12 months…

The short-term product offers benefits both to the customer and to the company.

The company can manage the price risk and asset quality prudently, without taking away flexibility from the customer in terms of his credit requirements.

The periodic renewal of the loan and the regular servicing of interest by the customer enforces credit discipline and it also lowers the interest burden on the customer.

The customer can also renew the loan indefinitely by periodically settling the interest and resetting the principal to the prevailing gold price.

The share of digital collections in gold loans has increased steadily over time, standing

at 54% in FY 2021, compared to 35% in FY 2020

We are working towards establishing an automated solution to verifying the purity of the gold assets.

I have seen videos online where there are machines which can do this. But it might come at increased cost.

We made the transition from classroom trainings to virtual classes and eLearning courses, thereby saving time and money. We prepared over 400 e-learning courses of over 220 hours duration and now our Learning Management System is the main platform for learning and development at our Company.

We are implementing augmented reality (AR) framework in our training programs to create near real, yet fully virtual classroom environment. AR infused training programmes will impart role critical training and get employees ready for future challenges. AR has the potential to

revolutionise the learning industry completely.

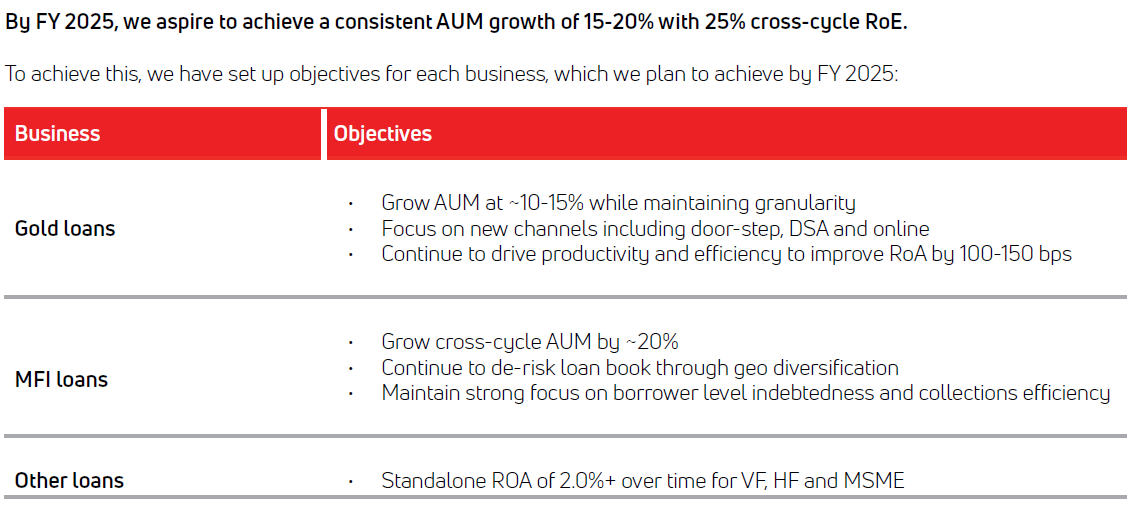

Supported by our resilient performance, we are marching tenaciously towards our FY 2025 goal of consistent AUM growth of 15-20% with 25% cross-cycle RoE.

Asirvad Micro Finance Limited now among the lowest cost providers of microfinance loans in India. Asirvad proactively provided ₹ 75 crore provision during Q1 to alleviate COVID-19 and provided ₹ 130 crore provision cumulatively so far.

Given the 3-month average contracted loan duration for Manappuram Finance, a significant proportion of loans disbursed at the time of peak gold price in Q2 were due for repayment during Q4.

Despite significant volatility in gold prices, we were able to arrest gross non-performing assets (GNPA) in the gold loan portfolio to less than 2%. Auctions during the quarter were ₹ 404 crore compared to ₹ 8 crore during the nine-month period ended December 20.

Added significantly to the gold loan marketing team.

Gold Loan Segment Performance:

Average loan ticket size increased to ₹ 44,600 in FY 2021 compared to ₹ 38,500 in FY 2020

Share of Online Gold Loans (OGL) in gold loan AUM up to 54% from 48% a year back

Loan-to-value (LTV) is 71% compared to 59% in FY 2020

Undertook various cost rationalisation initiatives, such as introduction of cellular vaults, which has resulted in ₹ 521 million average opex saving annually

Asirvad

One of the lowest cost microfinance lenders in India

Had added ~900 loan officers last year which helped enhance collection efficiency and increase borrower retention.

Vehicle and equipment

Covering 3,000+ co-located gold loan branches for collection and marketing distribution.

Digital loan agreement signing with e-stamping to save cost

Brand tie-ups with manufacturers for better reach

Cost of borrowing at 8.8%, ROE 26%, Capital Adequacy Ratio 29%, ROA 6%, Net Yield 24.9%

Gross NPA at 1.9% vs 2.01 in FY17

Net NPA at 1.53% vs 1.73% in FY17

Lending industry data

Bank credit growth hit a new low for the second year in a row in FY 2021 at 5.56%, the lowest in 59 years.

Credit offtake in FY 2021 at ₹ 109.51 trillion was lower than FY 2020’s when it had clocked a growth of 6.14%, which was the lowest in as many as 58 years.

It was way back in FY 1962 when credit growth was lower than this at 5.38%.

The agriculture and allied segment were the only bright spot with growth rising to 12.1% in FY 2021 from 4.1% in FY 2020.

The banking system’s credit growth is expected to almost double to 10% in FY 2022 riding on the economic recovery and policy interventions, according to rating agency CRISIL.

The quantum of gross non-performing assets (NPAs) could rise to 10.5-11% by the end of FY 2022.

According to RBI data, the consolidated balance sheet of NBFCs registered a y-o-y growth of 13% and 11.6% in Q2 and Q3 of FY 2021 respectively.

The overall assets under management (AUM) of NBFCs are estimated to grow at a slower rate of 5% in FY 2022 and are yet to touch the pre-pandemic levels, according to rating agency CRISIL. The biggest constricting factor for the NBFC industry will be funding sources to take care of the liabilities side, it said.

According to RBI data, outstanding loans against gold jewellery among banks grew by 131% in FY 2021 to ₹ 600 billion from ₹ 260 billion in FY 2020.

For FY 2021 and FY 2022, the gold loan market expected to grow at a rate of 15-16%, reaching a maximum of ₹ 2.69 trillion by the end of FY 2022

Edge over banks in Gold loan

Turnaround time

Geographically wider reach especially in the southern regions with high coverage in non-metro, semi-urban and rural areas.

employee transfers are less frequent in NBFC branches, which ensures staff are around for much longer and become familiar with the customers in a town or village. Generally, the employees are local and can communicate with the borrowers in the local language

which ensures familiarity and comfort particularly while understanding the financial terms and conditions.

As the gold loan is only a part of the whole portfolio of a bank, they do not have full-time employees specialised for appraisal and advancing a gold loan. An appraisal is done by a professional appraiser therefore, loans can be extended only when he is available. On the other hand, specialised NBFCs have several trained and specialised employees to appraise collateral and quickly disburse loans. Therefore, a customer can reach out to NBFCs anytime to avail of a gold loan.

The life insurance industry in India is expected to grow by 14-15% annually for the next three to five years.

I was doing some competitive analysis, and frankly very impressed with “Rupeek” business model. Rupeek Business Model: Essentially, they are similar to cloud-gold-lenders for banks; like third party customer acquisition, at-home gold transaction, 30 minute loan disbursal time, and safe deposits of gold (at local banks) are some of their +ve. They operates on asset-light model which means banks will carry liability on their balance sheets and Rupeek will do all the leg work for a small % cut (still its not known that what is % of their cut - however, after they achieve economies of scale, it looks easy for them to be profitable).

Only question I had was how accurate their at-home gold valuation method/process is? If it has any flaws or can be easily tricked than that might be their -ve point.

I have added some references for everyone’s review above. Staying on my toes for Manappuram.