@arjunbadola has hit the nail on the head frm the given data. Nd the insight frm this vl help in comparing & interpreting growth rates in other cases as well. Comparative faster growth rates are sometimes signs of :-

Lower initial starting revenue base - this is pretty evident from the AUM figures in the chart - The startin AUM figures for the fast-growers were low compared to the top 2 leaders & also compared to the total industry size as such

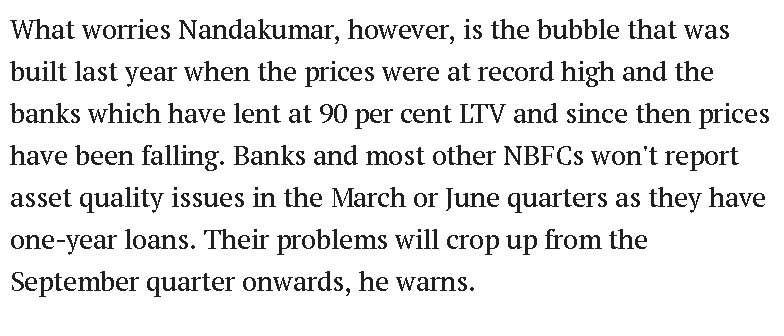

Desperation - Most of this gold loan lending has come in vogue over last yr for reasons well described in this thread above - Gold as immediate line of credit, Higher LTV allowed , rising gold prices etc… Hence, a favorable tailwind for an industry for a short period of time can certainly produce a good picture - How sustainable is it - that’s the question. And in fact, in lending this can be a case of reckless\loose lending standards. Yes, gold loans are comparatively safer bt one never knows.

IMO & analysis in progress so far - if slow growth rate is due to prudent lending practices - thn Manapuram is certainly doin better thn others as of now.

Disclosure : - Not invested. Analysis in progress for both Muthoot & Manapuram.

@arjunbadola

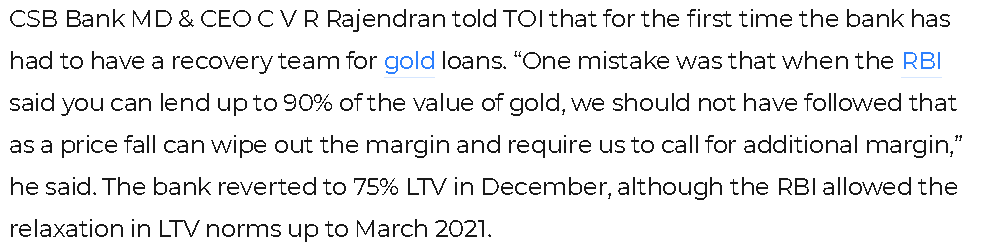

Your Observation is right in uncertain situations where it is difficult for Banks to grow their loan book in such times Banks aggressively expand in Gold Loan Business because loans are backed up by security.

Also to maintain Credit growth in system RBI proposes bank to give 90% LTV loan of gold value which was not given to NBFC which stands at 75% (Ended in March FY21) hence there is sudden growth in gold portfolio of banks but having higher LTV of 90% puts banks at heavy risk to sudden change in gold prices in such situation Gold Finance NBFC are much more suitable to absorb change in gold prices as they have 75% LTV.

I have background from National Institute of Bank Management (RBI Institute) and as per my observation banks only in distress times focus on gold loans otherwise Retail, corporate banking, credit cards are much profitable for banks as their asset light business which can grow in higher upper digits in good macro environment conditions.

To say least it is said in commodity business only lowest cost producer survives same is applicable for banks where institutes with lowest cost of funds added with lowest operation cost will dominate the space and has longer horizon of competitive advantage. Even though NBFC don’t have lowest cost of funds they lowest Operations cost, I believe it should be sustainable advantage for Gold NBFC in long horizon provided they stay focus on core business

One notable thing to see in gold loan AUM table shared by @harsh.beria93 is Federal bank they have able to grow their AUM with high growth rate despite having already big base, I am not sure but i believe it is because they have tied up with Rupeek (Online gold loan platform where customers deposit gold in federal bank) even though it is still not profitable, i believe is more immediate threat to gold loan NBFC then banks. Moats of gold loan NBFC are getting weaken a bit by extensive competition because as per capital returns, Gold loan NBFC has supernormal profits which is bound to attract competition there by reducing profit pool.

Hope this post helps in you some insight over gold loan industry.

Disc: Invested in Muthoot Finance currently tracking Manappuram on potential of rerating(as their microfinance has bottomed out it might see rebound from this low base) but staying away as i felt it lack focus towards Gold loan business, Please do your research wisely this is not recommendation and I am not a SEBI Register Advisor.

Yes this is exactly i was mentioning in my previous post, I was expecting many smaller banks to have this problem since last year as they might not be well versed with nuisances of gold loan industry also interesting fact to know is in Gold loan business NBFC do not have deposits or CASA as their sources of funds most of the NBFC fund comes from Bond markets and Commercial Papers But in banks sudden change in gold prices and nature of gold business is generally short term(<12 months) this can cause potential Asset liability mismatch for Banks in short horizon of time span as banks have Deposits and CASA Account which gold loan NBFC do not have as they don’t have public deposits. Hence Banks need to be more careful then NBFC when distributing loan at 90% LTV especially when there is significant increase in gold prices in shorter span of time as price reversion happens.

Any idea how is the future valuations of the company if the Asirvad Microfinance is listed in public. What will be the impact on existing shareholders?

Manappuram Finance went up 7% today on news that it acquired 2.72% stake in Asirvad Microfinance for ~40Cr. This values Asirvad at ~1,500Cr which is about 10% of current Market cap. How is this a positive news? How is the valuation of Asirvad going to affect Manappuram Finance valuation.

Given that company has increased its ownership in Microfinance subsidiary, it shows the management has high faith in this business. That may have led to sharp market reaction from quarters which were discounting Microfinance business heavily until now.

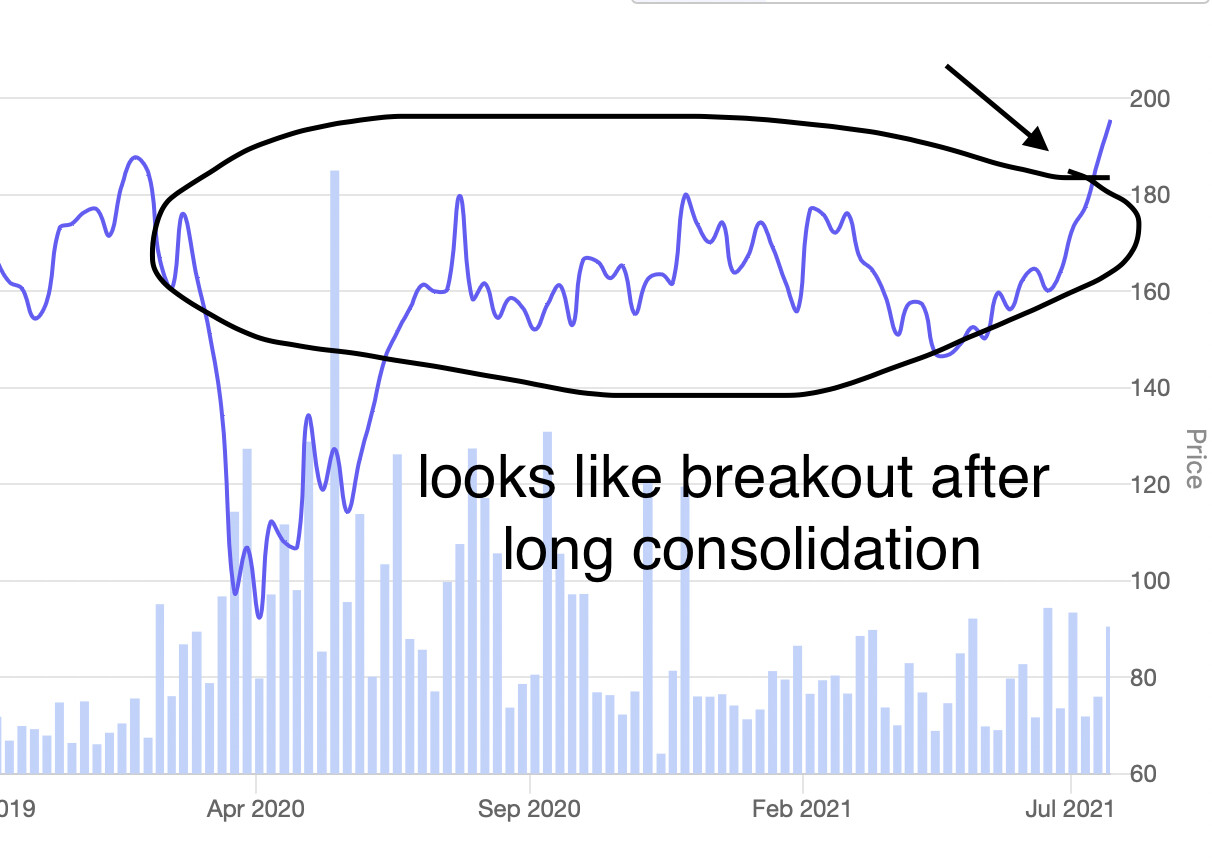

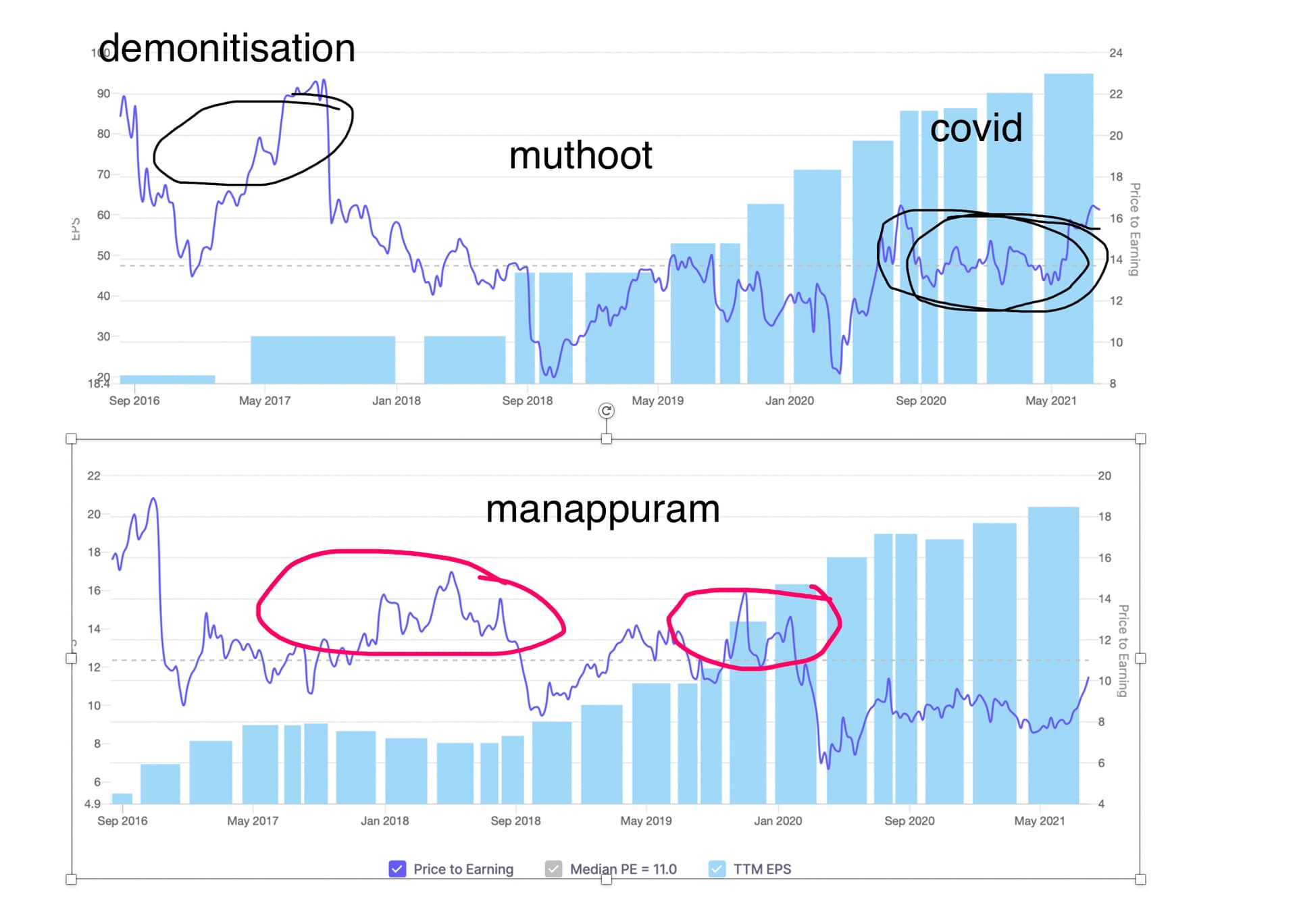

Rare to find such graph in roaring bull market.Usually in cyclical companies PE goes down with earning growth.

But Is Manappuram cyclical?Most people consider it cyclical due to fluctuating gold prices.But if we look closely gold price is not that closely related in case of manappuram. With rising gold price people pledge less gold but with decreasing price people just pledge more gold.So it compensates.So can’t classify as cyclical according to me .

In bull run most of the companies trade at PE 2X of growth .But here its available at half .Growth 20% and PE less than 10%. But controversy is how to price such companies PE or Book Value .Most research analyst will price it as per BV ( except few like prof Bakshi).So its very cheap as per PE but not super cheap as per BV.

Any how good recipe for a breakout .

But with manappuram something always go wrong ,demonetisation,covid ,gold to loan ratio, political issues ,geographical issues .But management has shown great strength and it is coming out strongly every time .

Good cash flow,excellent management ,great dividend ,high credit rating .

Post covid recovery will improve gold loans .

Nongold portfolio is showing turnaround .

Manappuram acquired shares of Asirvad through a call option they purchased 5 years before. Hence it was obligation for the seller.

Asirvad had around 1000 crore of equity in books. And earned 240crore profit in 2019-20 with a growth rate more than 35%. No seller will sell it this cheap unless he is obligated to do.

Because of this analysis, Manappuram stock showed positive sentiment.

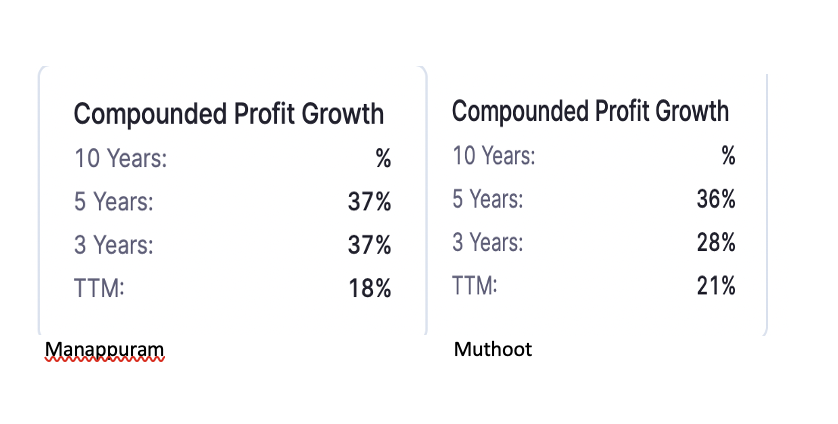

Almost similar profit growth

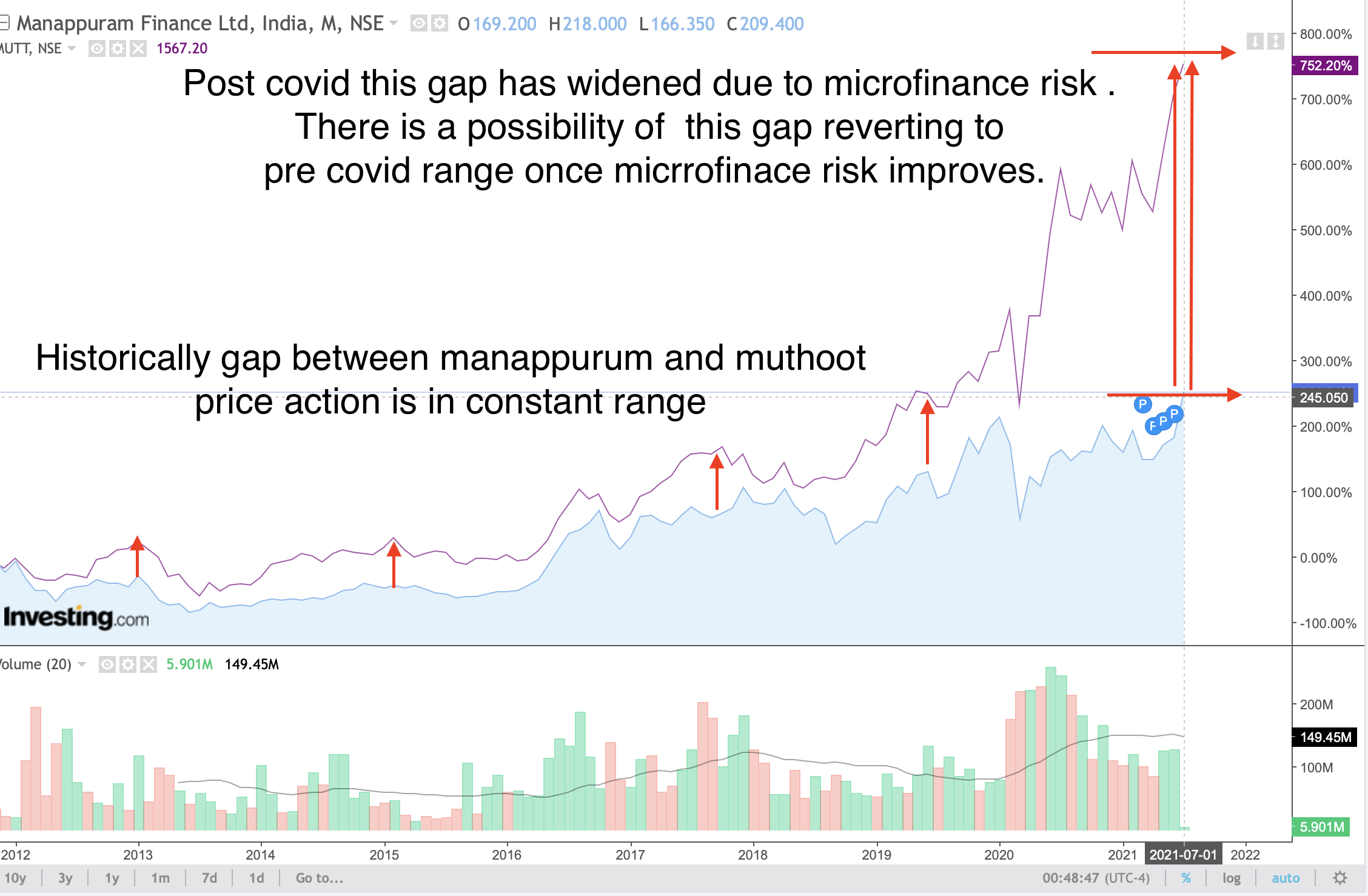

Now with non gold portfolio of Manappuram will bring more risk and may be more profit .Muthoot will get higher premium in difficult times like covid but I guess things might reverse in post covid growth situation .Let’s see how it pans out

during risky periods muthoot gets better PE than muthoot while during post risk growth period manappuram gets better PE …As non gold portfolio brings more risk but in growth period it can bring more growth

But possibly greatest risk is in muthoot with around 1 year loan tenure which can cause NPA if gold price falls steeply

The thesis collapses, due to their inability to hold on to market share which puts long term competitive positioning of the business in doubt. IIFL Finance is likely to be the challenger that competes with Muthoot. Manappuram has an okayish gold loan franchise and a cyclical microfin business. Not an outstanding gold loan franchise and a cyclical microfin business.

Slide 23 also says “However, non-gold focussed NBFCs are unable to sustain cross-cycle growth as demonstrated by historical performance”. The cross-cycle may have begun already with the potential for rising inflation and falling gold prices? Is it too early to write the thesis off? Especially since the microfin business also may be near the bottom of the cycle.

Muthoot, not degrowing QoQ tells you something. Might work out, but whenever competitive positioning is at risk. One of the biggest anti thesis pointers to sell out. Also gives a clue, when there is stress which gold franchise is able to maintain market share and not degrow. Even IIFL Finance was able to grow QoQ. Ordinary gold loan franchise+cyclical microfin business. Likely to get low valuations it gets.