company is also able to manage the fluctuations in gold price with below startegy

gold loan tenure is short (3 months) . So the percentage wise fluctuations will be minimized

changing the LTV for gold loan based on gold cycles. when gold price was at its peak last august, management was talking about 60%sh LTV . But now after the fall in gold price , their LTV increased to 70%.

company looks very conservative on gold loan business & able to grow secularly.

i’m only worried about their aggressive growth in vehicle loan & MFI business

I would suggest looking at the earnings growth and stay put if you believe that they can double their bottom line in 3-4 years. Even if PE rating doesn’t happen stock will most likely double. If rating happens then it’s a bumper return.

Gold fin and housing fin are out of market favour since 2018. Nobody knows when the tide would change but a reversal is possible within the next 3 year as the valuations are reasonable.

This is my personal thought and reason for holding Manappuram. I too think of moving it to momentum sectors but then resist myself as I’m getting good dividend and the company is doing better even in this worst time.

Good observations.

Also this is 70-80 year old time tested business. Management is conservative. And there is a trigger when they list their micro finance arm. As long as business keep performing at some point price will catch up.

When one see the trailing ROA & ROE numbers of this financial institution and compare the P/B or even P/E with other peers. This is a no brainer buy.

My reasons for not buying:

Tide can turn around pretty fast:

Gold loan is a high disbursement low AUM business. Since the tenure is 3-6Months, they should disburse 4× their AUM evey year just to maintain the current AUM numbers.

imagine this, if Manappuram stops disbursement for 6 months, their AUM will be 0 .

This also opens up chances for customers loss.

Competition heating up:

Competitive intensity is heating up a lot. Look at AU, IIFL Fin, Manappuram, SBI, karnataka bank,Canara Bank, federal bank,IDFC F etc no one wants to go slow in this these days.

Reason:

This is almost 0 credit loss product

RWA for Banks on gold loan is 0 - so, no capital block+ growth.

In addition to this, everyone is equipped with unlimited capital access- thanks to co-lending & onward lending tie-ups.

Banks are building capability:

GL focussed NBFCs used to have capability, focus and they managed to take some 28% of the market till date. Now, even banks are getting this capability by partnering with NBFCs and reduced timelines - Banks are evolving.

Personal experience: SBI disbursed GL in 4 hours after application @ 7.5% interest rate. Very clean & quick process. It used to be fussy some time back with too many docs required.

Reducing Gold Tonnage :

True metric & lifeline for GL companies like Muthoot, Manappuram are going down since last year. It’s almost 10% down for Manappuram.

This Trend had been positive for past many years and turned around during this year. Banks managed to gain some market share during this period.

This is not reflecting in AUM because of the massive gold price increase. This will start reflecting once the party is over i.e stable prices or price crash for 1+ year.

Diversification for growth:

This business is a high returns low growth model . So, Manappuram managed to venture into other lending areas. The problem here is, Gold loan procurement, storage, disbursement, collection is a complete Operations game. Even if the customer is new on this earth it doesn’t matter for the lender & recovery is instant.

Same with Microfinance vertical- very high customer interaction & affordable tickets.

Other lending required underwriting expertise- underwriting scorecards, behavioural scorecards, collection scorecards, Offus repayments, fraud identification & many more. It’s a tough analytical skill to build for any lending institution & it’s a continuous process.

I honestly don’t think Manappuram has this DNA atleast they haven’t proved it as yet.

Final take:

I honestly think that this is a great cash machine but unable to see massive upside & value it’s equity by factoring in the upcoming degrowth/ instability.

A banking license can change a lot of things though.

Fully agree on this “I honestly don’t think Manappuram has this DNA atleast they haven’t proved it as yet”

But the rest of the concerns are there for a decade and the business is resilient to these. Banks aren’t able to crack into the gold line of business, it’s just a different game. Growth is where the concern is, we need to watch how management leverages their branches and brand to expand into other verticals.

New here. Trying to understand the business. Why is gold tonnage a metric to be tracked? Rather, it should be just the value of gold w.r.t the loan book or LTV. I would think that having less gold tonnage is better due to operational reasons (storage, safekeeping and all). So, if loan book/gold tonnage goes up with stable LTV, it would rather lead to more branch efficiency, no?

Rather, Gold tonnage is THE metric to be tracked, isn’t it? LTV can’t go beyond 75%. Gold price is highly volatile and can’t be taken at face value and more importantly cannot be controlled by gold loan players.

Loan book/gold tonnage with stable LTV alone won’t indiciate branch efficiency. You need to control for 1 more variable gold price which is the overwhelming factor. LTV is seldom stable too as it’s again decided by gold prices.

@DIPAN_BISWAS

Even without tonnage you can get same with LTV, loan book, current price on gold. Being gold is always tracked in weights, they are providing it.

Your second point I couldn’t understand, how if loan book/gold tonnage goes up, LTV remains stable. Both are directly proportional

As Aravind said, the collateral is the price of gold and not gold itself. I can give gold ETFs and that would probably serve the same purpose (although it doesn’t carry emotional value, but lets leave that for now).

LTV may remain stable for Manappuram because their loans are 3 of months. Plus both the big players keep quite a big LTV headroom for price fluctuations. But lets even leave that aside. Say gold price goes up by 10%, that means I need that much less gold per rupee of loan availed for a given LTV, right? Say, in 10 years gold price doubles but the AUM stays same. Meaning, the gold in vaults has reduced by half (again assuming LTV stays same). But does that mean they have insufficient collateral? No, right?

So, a customer needs Rs x loan and keeps y grams gold with Manappuram. Next quarter, gold price goes up but he still needs Rs x. But now he keeps less than y grams for same amount. Vice-versa for fall in gold price. Would you characterize this event as loss of customer? Continuing same example, gold price doubles. So, two customers take Rs 2x loan with same gold deposit. Is this not growth? Yes, it is. Is this loan book more risky than the previous one? No, right? (I know they have this gold locker facility, but that’s besides the point). Plus, at 65% LTV its highly improbable they won’t recover money through auctions. Because, 35% price crash in 3 months is a rare event.

So, my question is then how is gold tonnage an appropriate metric for either growth or risk?

Also, difference between loan book/gold tonnage at a given LTV at 2 points in time is just the returns on gold, no?

Yes, Gold tonnage is not a important metric to look, as it will give misleading data. Moreover, this metric is not even needed, as you can get all necessary data with LTV, Current gold price and loan book size.

They are providing this information to tell they got this much collateral and being gold is measured in weights, they are having it in tonne

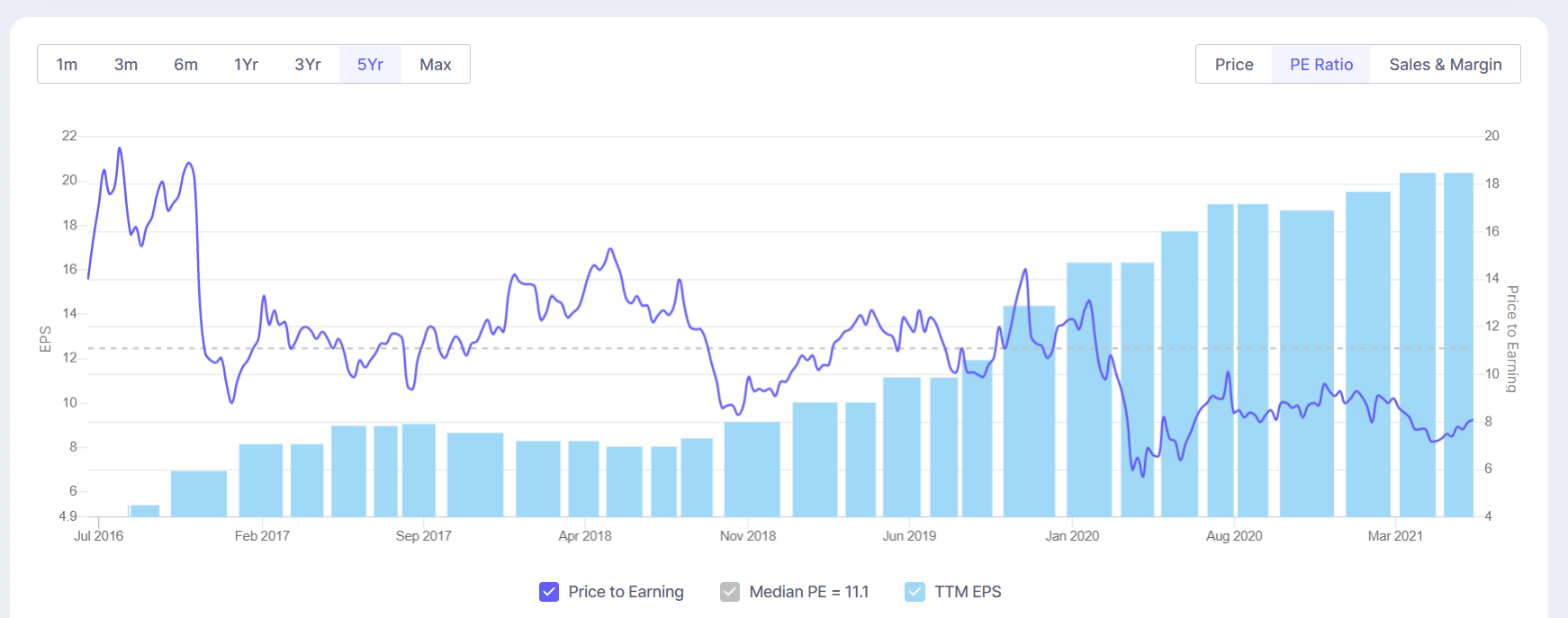

Over the years we find the EPS for Manappuram regularly increasing. The gradient is a gradual one. However despite the increase in EPS, the PE has reduced since Jan 2020. It seems like the market has rerated the stock downward.

Has the general market seen something that is not been revealed? Thoughts welcome.

Much hype has been created on Gold auction in last quarter. Media also made this as key highlight while reporting quarterly numbers. Clearly Manappuram needs to do better job there.

On the contrary Muthoot gave bullish guidance in there call. Market has taken that very positively.

Above 2 points have widened the gap between Muthoot & Manappuram. But this shall be short lived. Markets act as voting machine in short term. Manappurum offers deep value in current market, just compare it’s PE v/s Index’s PE.

Am a strong believer that with protection of capital through Gold, Manappurum must be valued as per PE & not basis PBV. Although not named, am sure Dr. Sanjay Bakhshi is talking about Manappuram in the following video.

Manappuram will always trade cheaper, no matter how much PAT growth happens

Their loan book has some riskier assets apart from gold loans

When you take standalone gold business of both companies and compare metrics, manappuram have poor metrics.

Why they can’t retain as much as gold(customers) per branch as muthoot do. Since we talk about customers, let’s see this business from customer view. If I take a loan in manappuram, I have to roll over it in every 3 months and in muthoot every 12 months. I remember muthoot says usually on average customers close their loans by 6 months itself and they will not keep it open for 12 months.

There are two sets of customers one who will repay and another will not repay. Let’s keep non paying customers aside and look into repaying customers. Since manappuram has 3 months timeline, they will ask customers to cover LTV shortfall, most people can do but some can’t do at that point of time(but may be in another 6 months they can be able to pay). But manappuram will auction these loans. Incase of muthoot, since loan tenure is high this problem will arise less. Due to this practice, muthoot has more retained customer base than manappuram.

Now let’s see why manappuram auctioned more on this quarter than muthoot. Answer: again 3 month tenure. If you see gold price chart, gold price peaked at 8th month of 2020. Loans disbursed at 8th should do renewal at 11th month, since there is price drop and customer cannot cover shortfall, they are in non paying bucket. Again if you see in Feb and March gold price still falling, manappuram is forced to auction those assets. But muthoot can only auction these loans only by November of this year as they follow 12+3 months for auction. For muthoot luck, gold price again raised after march.

Doing all this manappuram can safeguard their loan book but manappuram is not convenient for customer. Even keeping 1 year loan tenure, muthoot does not have NPA in their history, then why do manappuram keep 3 months, atleast they have to increase to 6 months

Whatever they derisk in gold loan portfolio, they add back those risks in MFI, vehicle.

Disc: Invested in manappuram, no position in muthoot

The rapid pace at which almost everyone but Manappuram has grown, is this busting the notion all of us have held that there is a pseudo moat that Manappuram and Muthoot have in the gold loan business? SBI has a higher AUM than Manappuram, and even Federal Bank and IIFL are close on its heels. Two qustions that need some pondering as far as I am concerned:

How sustainable are these high growth rates for banks and NBFCs?

What has changed so much in the last year that everone is jumping into gold financing in such a big way?

In my opinion, these numbers have less probability of sustaining.

Think about it like this, during the time of crisis when people were losing job how can a lender protect their balance sheet? By offering the safest loan possible: Gold Loan. (not stating the reasons here)

We say that the banks are not focused and inefficient, that would still remain true but these times seems an exception, because it was necessary for them to focus as it could help in their survival (or improving balance sheet when other segments were dead).

I would personally wait for things to get normal and then look at the numbers again.

Since Manappuram does lower tenure gold loans than most, just wonder if part of the lower growth was because of quicker run down of the old book and inability to do new lending during the first lockdown?