There is a sharp fall in gold price in last few weks (approx 10 % fall & trending to fall more). This might impact the gold loan growth rates in the near future. Also a fall of another 10% means , they will start loosing interest income on the loans , if they have to liquidate the assets

I think Mannapuram Finance is facing headwinds currently but once Gold gathers pace then we will see it staging a comeback…It is a very good business with NPA challenges lesser than other sectors due to the business model of gold loan…and considering the PE multiples at which it is trading at now, it might see some PE re-rating going forward as the sector will see a re-rating going forward…

1 Like

Latest management interview (link):

- With recent gold prices going down by 15%, tonnage has been stagnant resulting in de-growth in AUM; Will maintain gold loan growth of 15% in FY21

- Disbursements have come back to normal for other business segments

- Margins have improved slightly

- Credit cost for microfinance will settle at 7-8% of portfolio

- Long term growth: 15-20% with ROE of 20%

Disclosure: Invested (position size here)

4 Likes

Paid research

Hello Fellow Investors,

I have been tracking Manappuram finance for a while and being a amateur investor I have a few doubts with the recent news about hiving off it’s micro finance group,

Will the market cap and revenue of Manappuram Finance come down because Asirwad Microfinance has a portfolio of 5360 Crores?

Would existing shareholders in manapuram be given shares in Asirwad Microfinance?

Thank you in Anticipation.

2 Likes

@Sabarikumar89

Yes and No because there are a lot of scenarios in this and they haven’t mentioned on how they are going to do it. In some cases existing share holders will get new stocks if its Split type of demerger otherwise existing shareholders wont get it in case of IPO kind of listing.

I think its very early to discuss this. This kind of decisions and process usually takes a longtime and sometimes it may not happen.

Mr. VP Nandakumar latest interview

")

1 Like

3 Likes

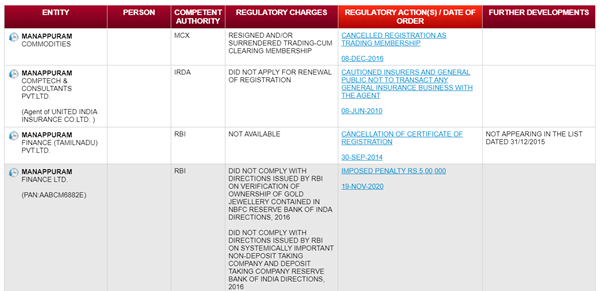

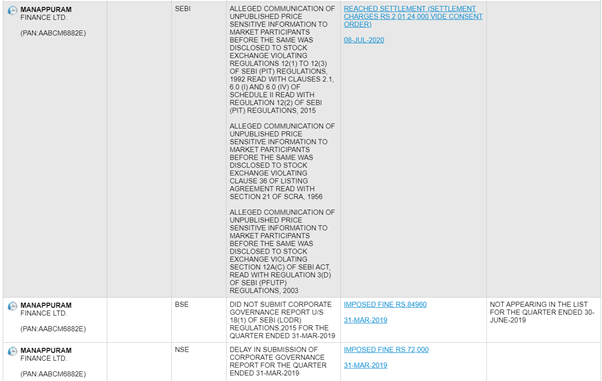

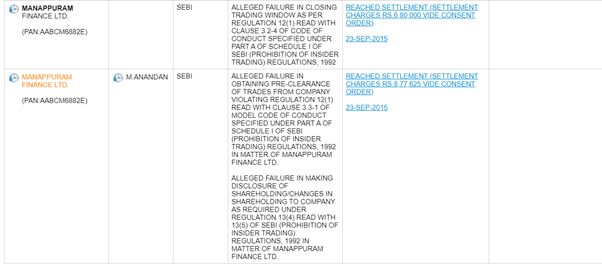

Many regulatory charges and fines/penalties imposed on Manappuram Finanace Ltd in last 2 years.

Hi everyone. I’m new here. Can anyone help me understand that even after posting successful quarterly results over the past few quarters, why is this still stuck at the same place for more than a year? The pe is around 7.5 whereas the eps is growing almost every quarter. My question might look very naive, but it would be great if someone can throw light on it. Is there any red flag that I’m missing?? I’m heavily invested in this stock since 3 years.

One of the reasons is their micro finance book. They are not a pure play gold loan business like muthoot.

Market is expecting a hit on their micro-finance book due to second lockdown.

I too am waiting for their results to see the hit.

1 Like

But, their micro-finance will have spin off , right. It will be listed separately & that should instill confidence in the investors… I don’t understand … Looks like , I am missing something here

Interesting innovation, cashback on paying interest. Horrible video though!

5 Likes

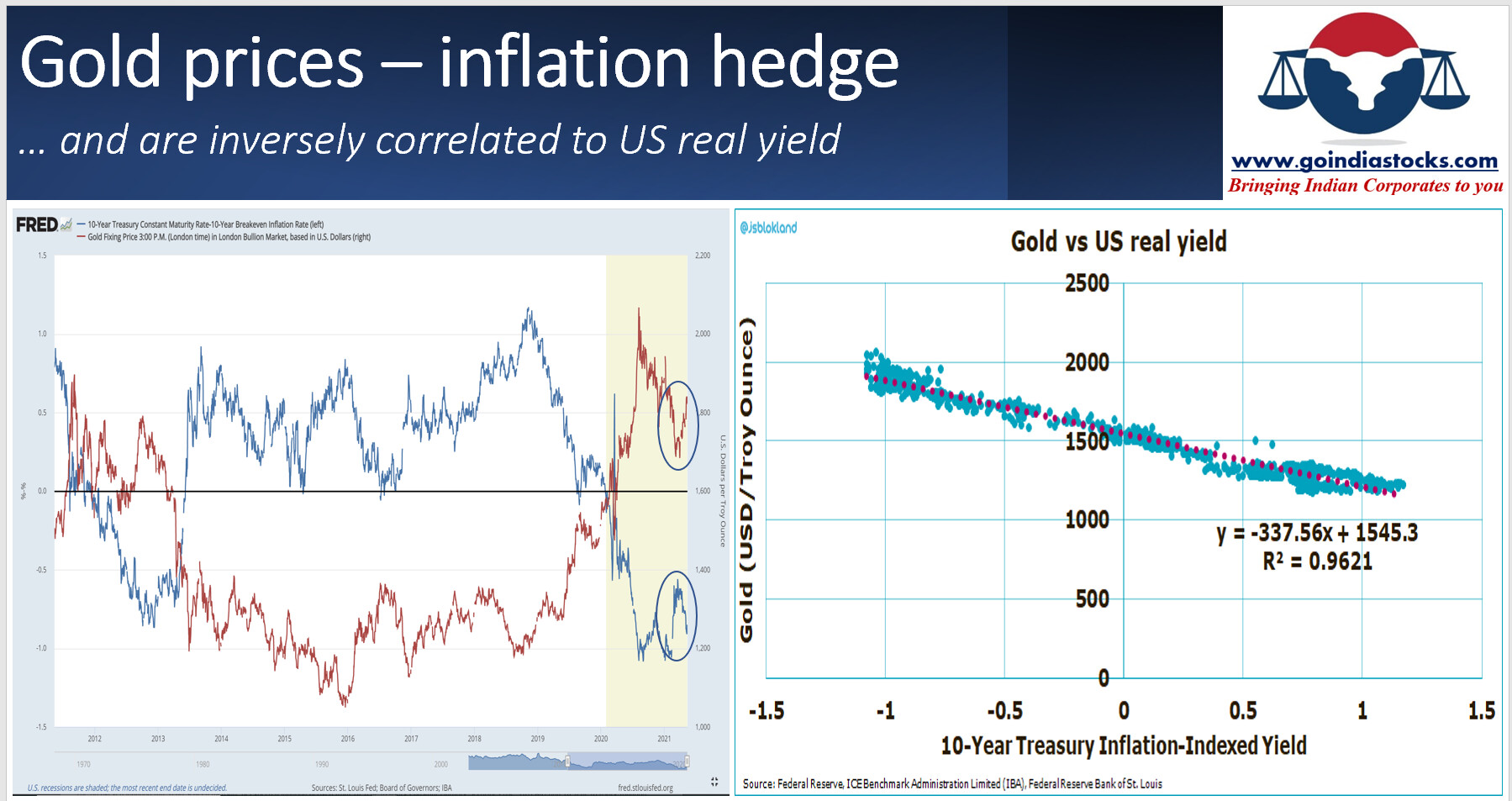

Inflation is threatening to go up. US Fed is looking to keep interest rates low till 2023. Real yields will continue to stay negative. Gold prices can move up as investors look to hedge inflation risk. Already this seems to be playing out. Gold Prices strongly correlate with negative real yields. Manappuram does look to be making a bottom.

Source:Everyone is missing this commodity play...

8 Likes

Q4 Results and dividend declaration of .75 paisa

1 Like

Good set of results from Manappuram (FY21 PAT growth of 16.5%, ROE ~ 26.2%, Book value growth of 27% and standalone capital adequacy of 29%).

-

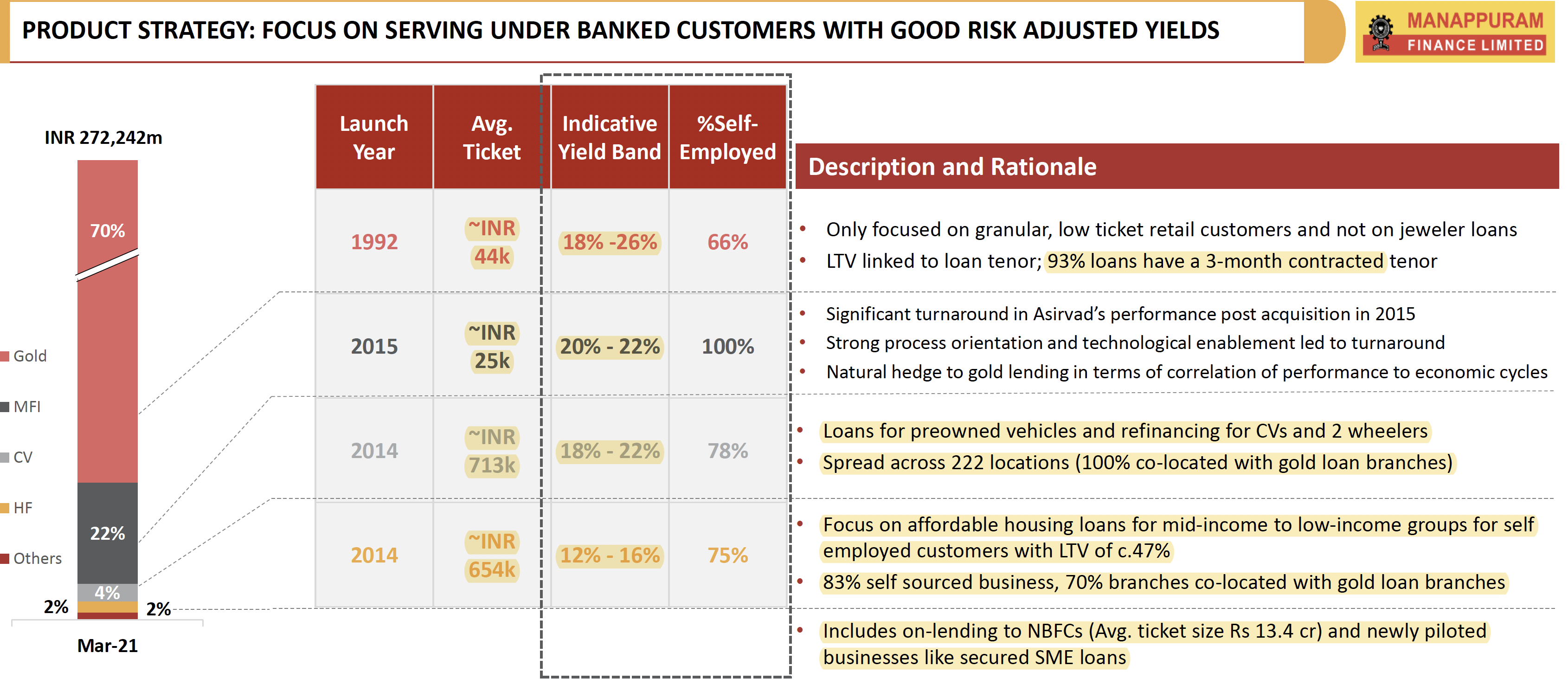

Company is experimenting with a new business of on-lending to NBFCs (current average ticket size is 13.4 cr.) and secured SME loans.

-

Gold auctions during the quarter was 404 cr. vs 8 cr. during the previous 9MFY21. This was because of increased defaults. Also, there was a lot of foreclosure of loans. The strategy of short term lending with 3-M loans accounting for 93% of outstanding gold loans have produced very good results (ROA: 6.9%, ROE: 27.7%) despite de-growth in gold tonnage (65.3 vs 72.4 in Q4FY20). Also the strategy of keeping LTV at 60% has paid rich dividends, because with gold prices decreasing LTV only increased to 71% which is below RBI’s benchmark of 75%. Current LTV is 63%. Increased competition hasn’t brought down net yields much (FY21 yields: 24.9%)

-

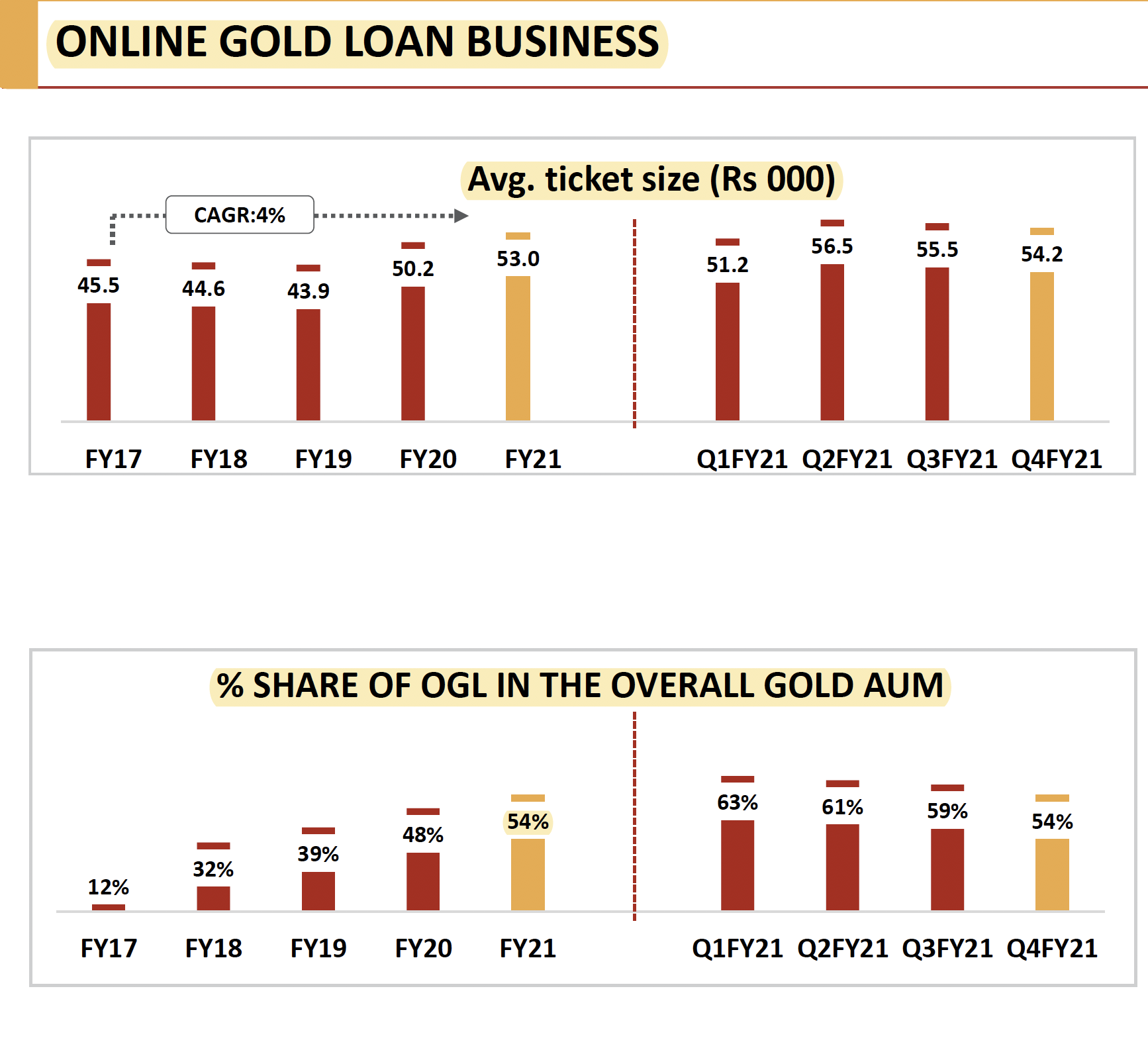

Online gold loan now accounts for 54% of outstanding gold loans (down from 59% in Q3FY21). The sharp decrease from 63% in Q1FY21 suggests online gold lending is more volatile compared to physical lending. Also, the average ticket size is higher in online gold lending (53’000 vs company average of 44’600).

-

The company has a very stable borrowing mix with bonds + ECBs accounting for 51.8% of outstanding borrowings. Cost of borrowings have also come down to 8.8%

-

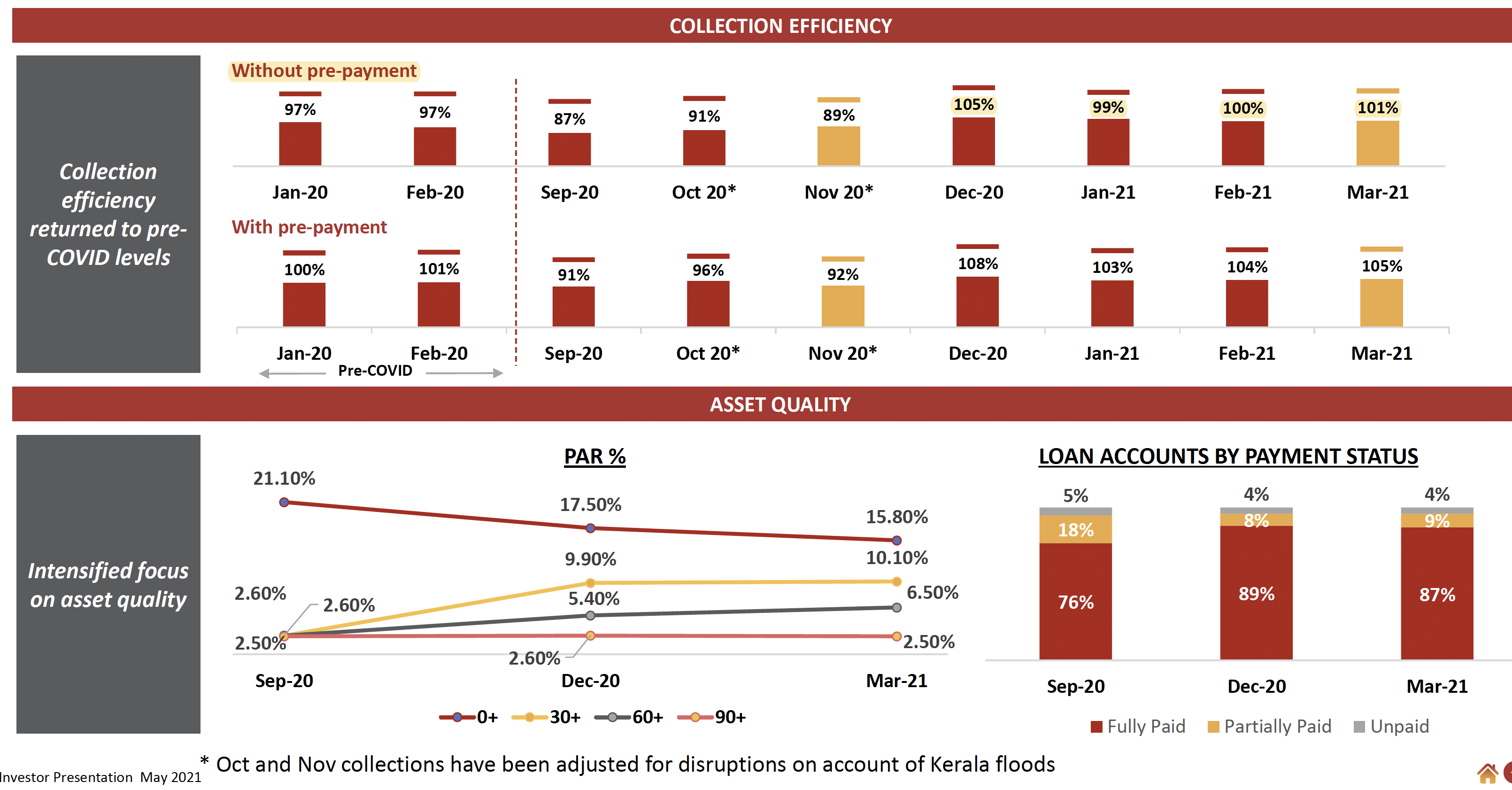

MFI book is very well provisioned (net NPA ~ 0; provision ~ 5% of book). Collection efficiency improved to 100% (without pre-payment) since December 2020 which suggests their MFI business sprung back very quickly. This is in-line (or slightly better) compared to leaders like Credit Access Grameen. AUM/borrower is below industry standards (at 25’400). Cost of funds have come down to 10.5%. Also they were able to garner 26% of borrowings from NCDs (more stable funding) which is even better than Credit Access.

-

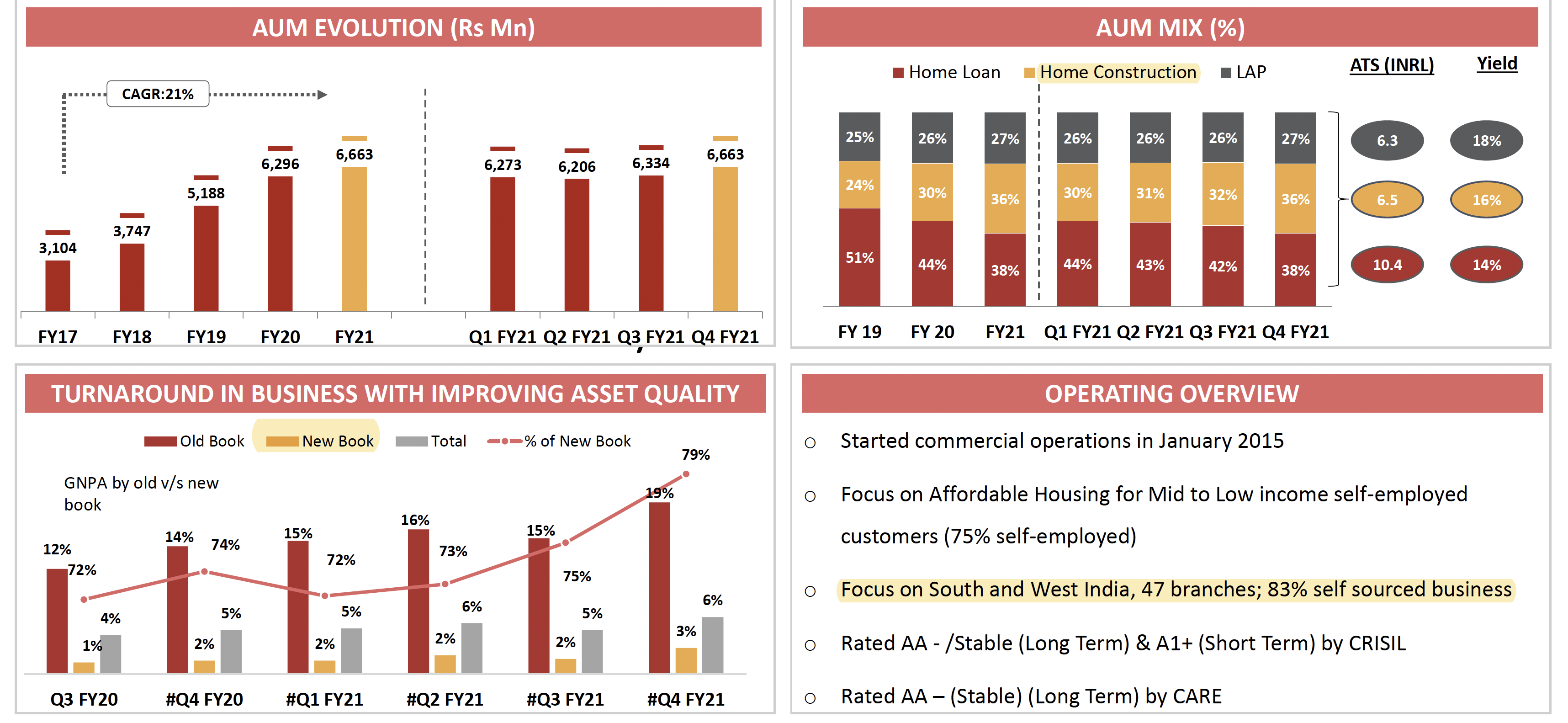

Housing loan business is doing okay with NPAs on the new book at 3% and 6% (including old book). There has been growth in self construction book, LAP has been kept constant.

-

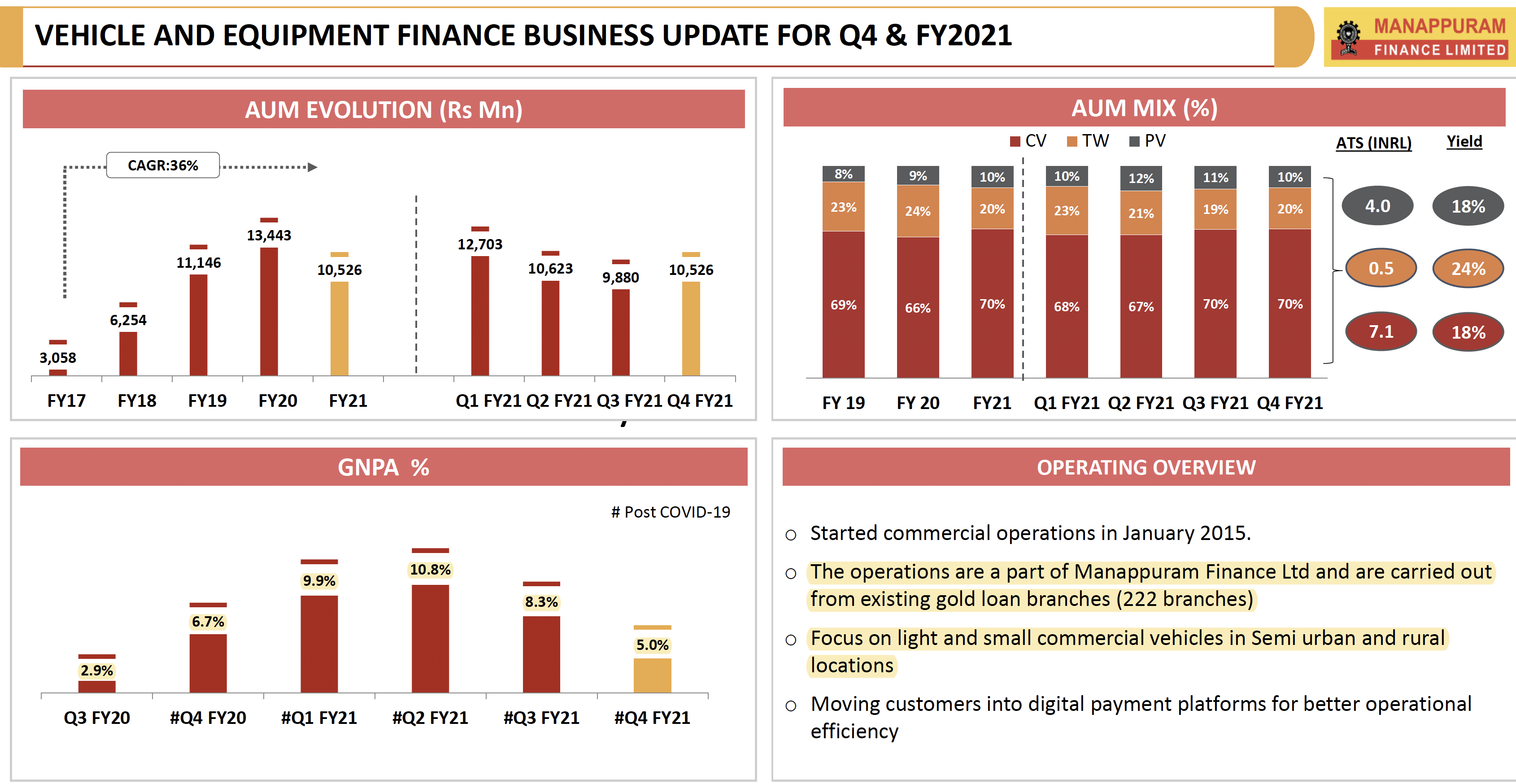

There has been a big improvement in vehicle financing book with GNPAs coming down to 5% from the peak of 10.8%. Is this because of a structural improvement in this business or due to Manappuram’s strategy on focusing on small vehicle owners or due to de-growth in book?

Disclosure: Invested (position size here)

10 Likes

“The sharp fall in gold prices and the higher auctions this year have caused a contraction in the gold loan portfolio. During the last six months we have had to auction gold at the lowest prices,” VP Nandakumar, chief executive officer, Manappuram Finance told analysts over a conference call on Wednesday.”

Disc: Invested

2 Likes

Motilal Oswal target price 205

Prabhudas liladhar target price 187

Arihant capital 197 target price

Not sure why everyone value it by book value which we know will keep on changing with gold price. Anyhow manappuram is out of flavour since long time .And this time the huge gold auction will further dent the negative views.Looks like it will give 10% valuation upside every year with huge risk .I was hoping for rerating since long time but dosent look like it will happen anytime soon .Also the risk associated with holding such business for 10% gain every year ,is it worth !!!Thought of exiting it since last few months but was holding with hope of rerating ,but every quarter something bad happens .Looks like market is very smart in valuing stocks and combined consensus is right most of the times

Disc:Invested

4 Likes

One more data point about gold auctions, its not an unusual thing. Their strategy of focusing on low duration gold loans is better than industry practise of longer duration gold lending. This is also reflected in the sharp reduction in auctions from 10%+ levels until FY16 to <10% since then. Here is data going back to FY13.

| FY13 | FY14 | FY15 | FY16 | FY17 | FY18 | FY19 | FY20 | FY21 | |

|---|---|---|---|---|---|---|---|---|---|

| Gold AUM | 9’945.80 | 8’155.20 | 9’269.30 | 10’080.60 | 11’124.53 | 11’734.98 | 12’961.52 | 16’967.18 | 19’077.00 |

| Auctions | 1’301.30 | 2’284.70 | 1’188.00 | 1’932.00 | 929.00 | 1’204.50 | 419.40 | 116.10 | 412.00 |

| % AUM | 13.08% | 28.02% | 12.82% | 19.17% | 8.35% | 10.26% | 3.24% | 0.68% | 2.16% |

Here are Muthoot numbers

| FY14 | FY15 | FY16 | FY17 | FY18 | FY19 | FY20 | |

|---|---|---|---|---|---|---|---|

| Gold AUM | 3’429.31 | 2’787.90 | 3’880.00 | 1’184.70 | 2’517.68 | 1’400.05 | 854.78 |

| Auctions | 21’617.90 | 23’349.90 | 24’335.50 | 27’219.90 | 28’848.40 | 33’585.30 | 40’772.40 |

| % AUM | 15.86% | 11.94% | 15.94% | 4.35% | 8.73% | 4.17% | 2.10% |

7 Likes

so it is very bad sign for economy… already auction executed (or) or in place ?