The ongoing dispute amongst the promoters is hurting the investors & the company. It is time that some sense prevail

1 Like

I’m researching about Man Industries for the first time as it came up on my value screen. I am confused about the pledge scenario. In some interview promoter said that the pledge was created for a loan for project from SBI and the pledge shall be removed. But on screener.in the pledge percentage is shown as 33.4%. I even confirmed the same on the BSE website.

Can someone clarify this pledge scenario for me?

Strange case of Man Industries

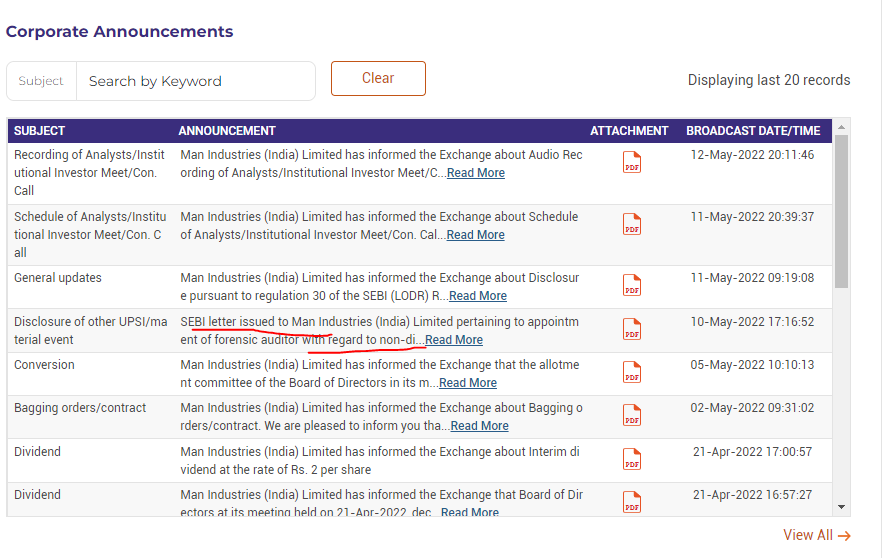

SEBI letter dated 22nd Nov’ 21 requesting a Forensic Audit for Man Ind being informed to the exchanges yesterday ie 10th May ‘22.

Although a mediocre business, the outlook has been improving apparently and has garnered interest from investors lately.

Also, poor corp. governance isnt a new thing for the company as it has been fined and reprimanded by SEBI previously (hence the valuation)

Overall,

Management sounds enthused since last few quarters, macros (crude oil prices 75$ and above) augur well for Oil and Gas sector which gives 80% of the current topline, doing a sizeable capex which should be more value accretive (better asset turns), gave an interim dividend recently, next genereration joining in, working on both topline and bottomline improvements, divesting non core assets.

Has seen promotor buying.

Is this priced in already?

1 Like

When I bought Man Indus at 90+ price, I had already factored poor corp governance into the price anyways. I do it to almost all small caps, mid caps and even PSUs.

So today’s additional fall is merely a buying opportunity for me.

Over the long battle between the brothers many skeletons have come out even though market is aware of the forensic audit the language by sebi letter is now including for the scope of siphoning of funds and doubt on the provisions now we all know some diversion happen in merino but if found guilty of manipulating then it’s a disaster for retail investors over 10 yrs always smoking some sort of corporate issues should we catch the falling knife based on the perception of value or to assume the old adage IF THEY CAN STEAL FOR YOU THEY WILL STEAL FROM YOU ONEDAY

DISCL came out of the holding after long time

Unfortunately, everyone is just acting quick bytes. The disclosure was made way back in Feb’22. The news was double discounted.

1 Like

Call discussing the SEBI letter might help throw some light on issues. Man Industries India Limited Q4 FY22 Earnings Concall - YouTube

I had a lot of respect for moneylife articles. Although in this one they totally take Man to task (Man Industries: Shocking Lapse by SEBI and Some Questionable Details in 2020-21 Annual Accounts) but 9 months back the same team talks about an impending turnaround Man Industries: A Turnaround Story? ? Didn’t they see issues highligted (in the recent article) way back in Sept 21?

Price changes narratives for everyone

2 Likes

Hi anybody following this company closely? The book value is more than double the CMP and they have significantly reduced debt and have strong free cash flow, results have been muted in the last two quarters.

What is the reason of such less valuation?

If you dig deeper into companies’ history, you will find a lot of irregularities in financials, especially in their Real Estate division. The company has invested huge sums in Real Estate Projects and I doubt they are able to realize any money out of it.

Also, we can see contingent liabilities are huge and if any of it realizes, could easily burn one go, all the cash company has. Management on the other hand is not so predictable with their targets, guidance, and so on.

So, factoring all this in, don’t think valuations can be fair till the execution takes place.

Disc: Tracking Position Only.

3 Likes

Man Industries (India) LImited

Positive outlook -

-

In the recent Concall, it was informed that the company has order of 700 cr in pipeline.

-

New PLant will be functional soon with ERW segment and Stainless Steel segment

-

Positive cash flow from Operations.

-

Pipeline industry to grow in India at CAGR of 5% for the next 4 to 5 years.

POssible Risks -

-

Promoter holding - 45.69% (29.61% pledged)

-

Ebitda Margin (6% approx ) - LOwer than the industry Median of LSaw Pipes which is 20-25%

-

Trade receivables in the balance sheet are not totally realisable

-

Trade payable are 736.60 cr as against Trade receivables of Rs 552 cr (as per BAlance Sheet H1-FY23)

-

Trade receivables are not totally realisable, the amount is under dispute due to late delivery.

Disc : Tracking Position, Not Invested.

The results (poor show QoQ basis. YoY maintain) were just out by 6:25 PM today. (Board meeting commenced at 3:45 PM after market hours). But the stock was 8% down in the 1st two trading hours… Is this just speculation or absence of controls by the company on confidential financial matters?

1 Like

Summary of the Q1 FY24 earnings call Man Industries (India) Ltd:

Strengths:

- Diverse Product Portfolio: With products like LSAW, HSAW pipes, and the addition of ERW, the company has a diverse range of offerings catering to various sectors.

- Certifications and Compliance: The ERW plant’s recent certifications (BIS and upcoming API) demonstrate a commitment to quality and adherence to industry standards.

- Strong Order Book: With an unexecuted order book of around 1900 crores and bids for more than 13,000 crores, the company has a robust pipeline of business.

- Improved Financial Performance: The growth in EBITDA and net profit, along with improved margins, indicates financial strength.

- Strategic Expansion Plans: The company’s plans for expansion and diversification into new areas like ERW and stainless steel show a forward-thinking approach.

Weaknesses:

- Operational Challenges: The impact of natural disasters like cyclones and heavy rains has shown vulnerability in operations, leading to production losses and delays.

- Dependence on Certain Markets: If the company relies heavily on specific sectors like oil and gas, changes in those industries could affect its performance.

- Capacity Utilization: The current capacity utilization of 60-70% in certain segments may indicate underutilization of resources.

Opportunities:

- Growing Infrastructure Needs: With increasing demand for infrastructure development in India and abroad, there are opportunities for growth in the pipe manufacturing sector.

- New Product Lines: The introduction of ERW and stainless steel products opens new markets and customer segments.

- Strategic Acquisitions or Partnerships: Collaborating or merging with other players in the industry could enhance the company’s market reach and capabilities.

- Sustainability Initiatives: Emphasizing environmentally friendly practices and products could align with global sustainability trends and attract eco-conscious customers.

Threats:

- Market Competition: The industry is competitive, and new entrants or aggressive strategies by existing competitors could challenge the company’s market position.

- Global Economic Fluctuations: Changes in global economic conditions, particularly in the oil and gas sector, could affect demand for the company’s products.

- Regulatory Changes: Any significant changes in regulations or standards could impact the company’s operations and compliance requirements.

- Supply Chain Disruptions: Global events like pandemics or geopolitical tensions could disrupt the supply chain, affecting production and delivery timelines.

Management Guidance:

- Financial Guidance:

- Revenue guidance for the year ending FY24 is around 3000 crores.

- For FY24-25, with the addition of ERW and other new products, the estimated revenues are between 3500 to 4000 crores.

- Operational Guidance:

- The unexecuted order book stands at approximately 1900 crores, expected to be executed in the next six months.

- The ERW plant has received BIS certification and is awaiting API certification, which will strengthen the company’s position in the market.

- The company is actively participating in tendering processes and expects good order book inflow in the near future.

- Expansion Plans:

- The management has plans for further expansion, including the introduction of new products like ERW and stainless steel.

- Proceeds from land sales may be used for debt repayment or further expansion.

Disc: Invested

4 Likes

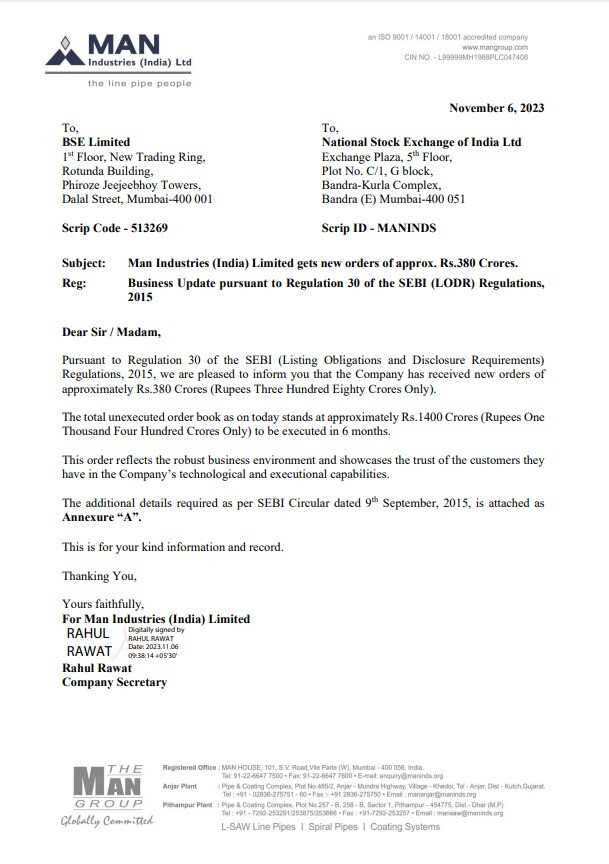

Man Industries (India) Limited has received new orders worth approximately Rs. 380 Crores and now has an unexecuted order book of around Rs. 1,400 Crores to be completed within the next six months.

These new orders reflect a strong business environment and the trust customers have in the company’s technological and execution capabilities.

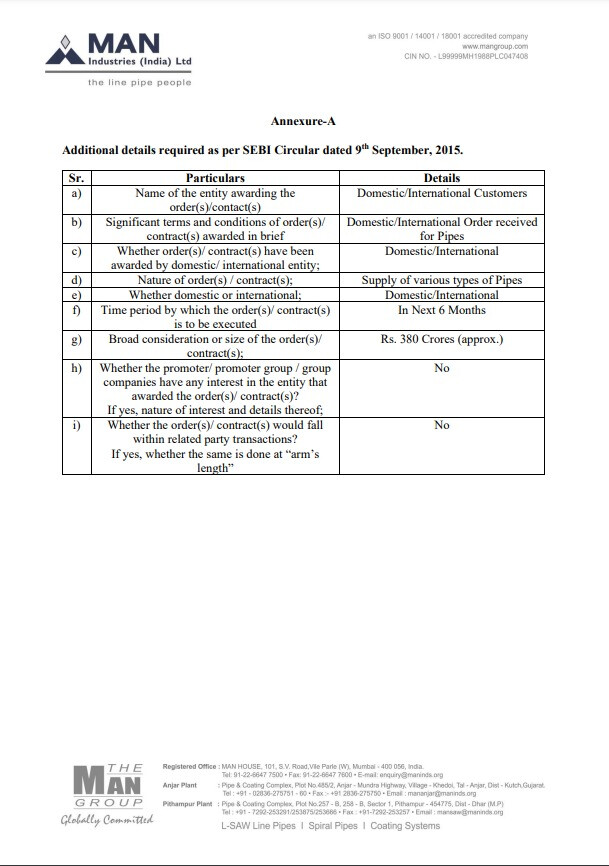

Here are additional details as per regulatory requirements:

- The orders have been awarded by both domestic and international customers.

- The orders pertain to the supply of various types of pipes.

- The execution timeline for these orders is within the next six months.

- The size of the order is approximately Rs. 380 Crores.

1 Like

Anybody have q2fy24 concall notes ? It will be very helpful if you share.

I have exited Man Ind post-Q2 call. Sharing the summary here but take a bit of negative bias:

- This Q2 Revenue Breakup: 75% O&G, 25% Water and 80% Exports. Have OB of 1400 Cr. as of “Today” of which 60% is export. This OB you can say will be delivered within FY24. On top, we can do some sales from the ERW plant as well in Q4.

- Margins were lower due to Forex Gain of Rs. 19 Cr. which is shown in other income. If you adjust this, margins have not fallen much. (Not sure what management is thinking, or it was an escape to justify this margin fall)

- Interest cost belonging to loan taken for the ERW plant, will remain till the time ERW revenue does not come. Hence, till that time expect to remain at this level.

- Inventory is high because of back-to-back RM booking and pending export orders. Once Export orders get delivered, you can see a drop in inventory in Q3.

- SS Seamless Plant is on track.

- Guidance for EBITDA in H2 will be at 10%.

- Merino Shelter, you can assume money will be received in one month.

My assessment after the call: I was expecting pretty good revenue but margins as well. O&G as well as Exports have better margins v/s Domestic and Water. Almost 75-80% of revenue in Q2 belonged to export/O&G. Despite this margins fell too much. In the call, was particularly disappointed with management giving and escape of Forex Gain. I have been following this stock for a long and I knew management guidance and integrity have always been an issue, and at this price, I felt the margin of safety is reducing. Alternatively, I have other opportunities at better valuations.

Hence, decided to exit the stock and book in profit with my average cost being 140-around.

Regards,

Mukul Jain

4 Likes

Strong guidance in ET Now interview

• Looking at 2900-3000 cr revenue by end of year. 50% growth.

• SS seamless plant (to be operational by Dec 2024) – will contribute to better margins in future

• EBITDA margin likely to be 12 – 15% in next 3 years

• Robust India outlook in Oil & gas sector + good demand in Middle east

• Targeting topline of around 5500 to 6000 cr in the next 3 years.

4 Likes

MAN Industries case: NFRA imposes 5-year ban on auditor for lapses

6 Likes

1 Like