please find attached my notes on man

2 Likes

How does having a new product “hydrogen transportation pipes” would change outlook for company ?

It can now deliver such pipes up to 5 lakh MT/Annum, from existing setup.

Unless these new pipes are different technologically, i am sure man may not be alone in “hydrogen pipes”, since plenty of companies already use such pipes for transporting hydrogen & hydrogenation purposes.

D-Not invested

For Hydrogen, new pipes needs to be laid. Existing pipes are technical certified for Oil , gas and Water accordingly.

Man Industries is first Indian companies whose pipes are certified for Hydrogen handling by European labs. Lead time to get this certification is ~18 months. It gives them a short window of 6months - 12 months where they can pitch their products to Indian and European companies without any competition from other Indian companies.

Since, it is new products, their margins (~15-18%) will be a little better wrt current OIL pipes (~12-13%).

Disc: Invested

5 Likes

Quick notes on Man Industries concall:

- Order book → Unexecuted orders of 1300 crs to be completed in the next 6 months, evenly split between oil and gas and water (50-50%). EBITDA margins for oil and gas are 11-13%, while for water, they are 7-8%.

- Guidance → Projected 20-25% growth in topline (approx 3600 crs) with a 30-35% bottom-line increase. EBITDA margin expected at 9-11% (330-350 crs). For 2025-26, a topline growth of 60-70% (approx 5000 crs) with an EBITDA margin at 10-11% is anticipated. EBITDA margin includes other income, excluding which shows a 1.5% difference.

- Capex → FY24 capex was 90 crs, with 25 crs remaining to be spent in the next 2 months. For FY25, capex is estimated at 150 crs.

- ERW Plant → Anticipated revenue of 300-400 crs to commence in 2024-25, reaching 400-500 crs in FY26, with peak revenue potentially at 1000 crs.

- Stainless Steel Pipes → Operations expected from Q4FY25, serving both domestic and export markets for the oil and gas sector. Mother pipes constitute 60-70%, and pilger pipes, with higher margins and smaller sizes, make up the rest. Margins projected at 10-11%. Revenue for FY26 (first year) estimated at 300-400 crs.

- Rational for raising 250crs → Current capex of 550 crs for stainless steel, with more capex pending approval for LSAW and HSAW in different countries; debt to increase to 600-700 crs.

- Hydrogen transportation pipe → Approval from European Research Lab received after 16 months; bidding for orders in Europe started; new sector with exclusive pipes required for hydrogen; expected orders in the next 3 years; margin expectation of 18-20%; in Vibrant Gujarat approx quantity in the next 10-15 years is >5 million tonnes;

- Saudi Plant → Awaiting in-principle approvals; limited disclosure of information.

- Real Estate → Joint Development Agreement with an A+ developer; entire project development by the developer; upfront and ongoing revenue for the next 4-5 years.

- Other Expenses → Rise in expenses due to increased component of freight charges; Q3FY22 freight cost was 22 crs, rising to 70 crs this year due to more export-based orders; no observed price impact from the Red Sea.

- Volume → For this quarter, 85-90k tonnes; compared to 65k tonnes in the same quarter last year.

6 Likes

@vineet_mittal

Man Industries has been heating up lately to the point where the rise is eye-soringly impressive! Do you think it’s still at good valuation to jump in ? What are your thoughts?

D-Tracking and plan to invest.

1 Like

I think, you should start with SIP for this stock.

One of the reason for today’s run-up can be finalizing of Saudi Arabia deal which was hinted in Q3 call.

Lets see when that announcement comes.

Disclaimer: Invested . Not a registered advisor.

1 Like

Recent Developments in Man Industries:

-

Issuance of preferential allotment to big investors like Ashish Kacholia, mutual funds and AIF funds for capex plans for new plant in Jammu. Link.

-

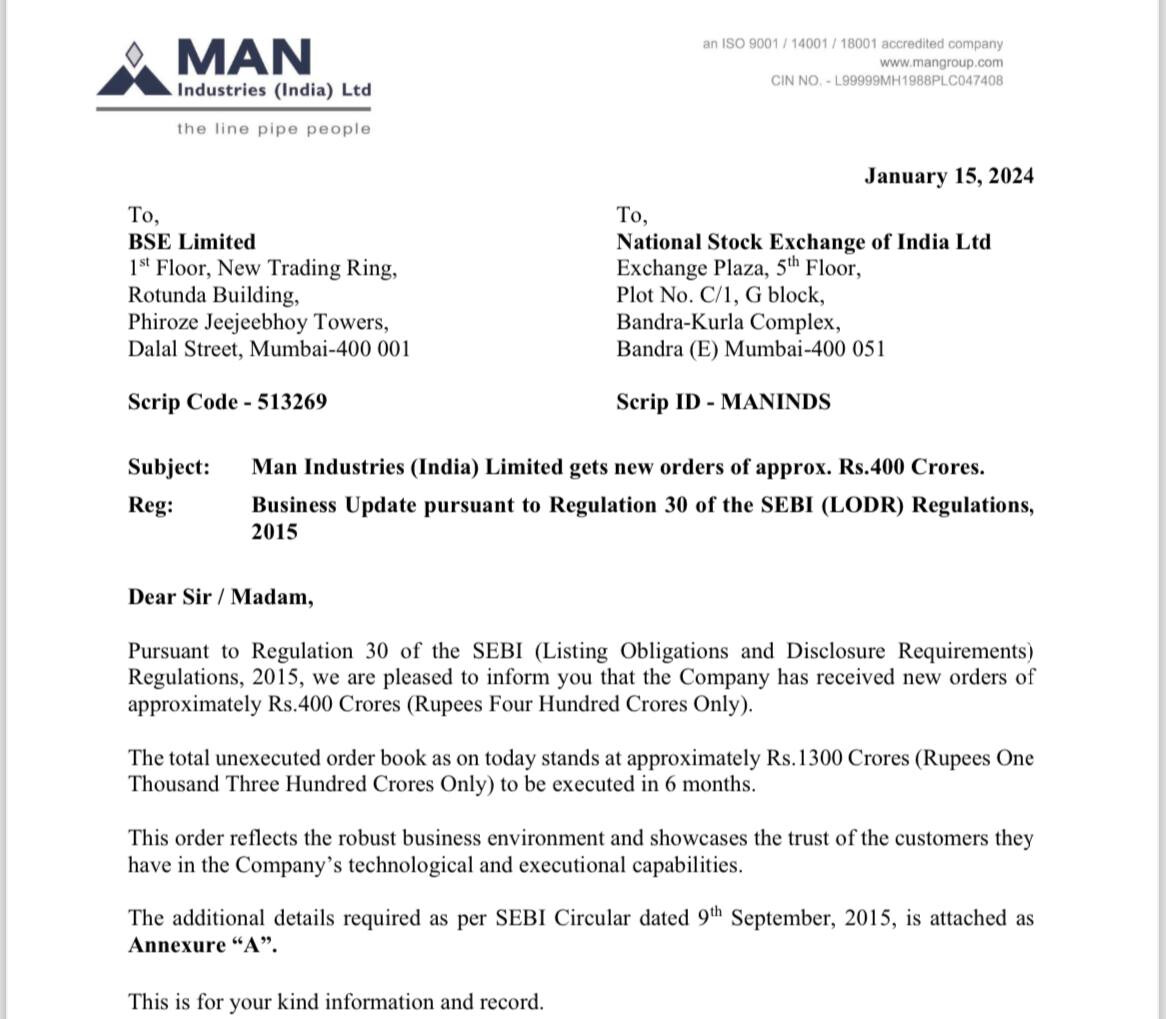

2 new orders of 525 Cr and 555 Cr which are to be executed in the next 6-7 months. The current unexecuted order book for 6-7 months is 2000 Cr. Link for latest order.

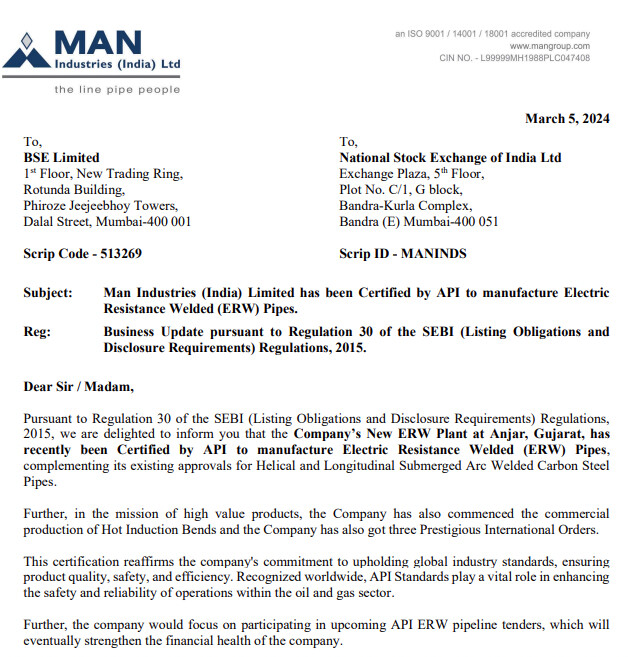

Man Industries’ ERW plant in Gujarat receives API certification to manufacture electric resistance welded pipes

The plant will commence its commercial production of hot induction bends

The company has also bagged three international orders

1 Like

The CMP~370 is getting closer to rights issue price of 367.

I, myself with limited understanding of overall picture,think its in my hypothetical range and is good to hook up for H2 & growth guidence.

The logic of comparing with rights issue is in right direction, yes ?

D-Invested. Not registered adviser etc.

1 Like

Manind promoters bought few shares from market during march-24.

Following is info including other insider aquisitions.

1 Like

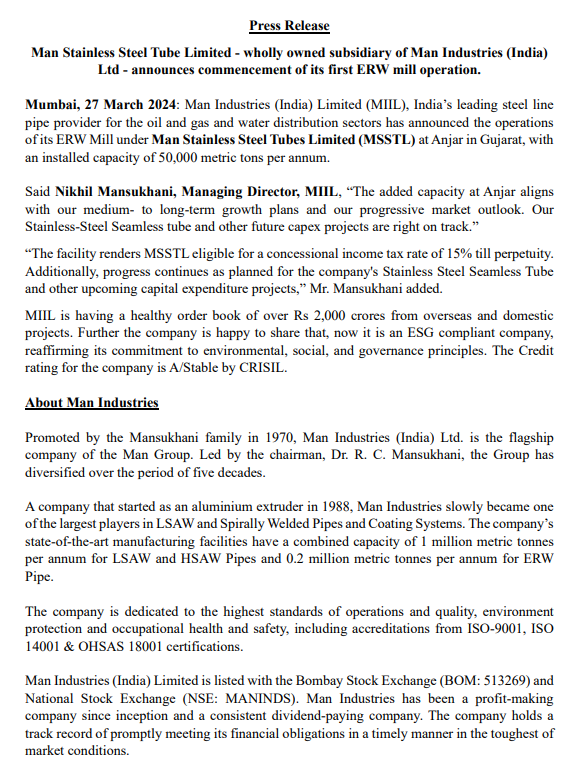

Man Industries announces the commencement of its 50,000 MT ERW Mill plant.

With this facility, they’ll be eligible for a concessional income tax of 15 % till perpetuity.

Does anyone know the reason for this concession? Does this mean going forward the tax rate will be reduced to 15% from the current 25%?

2 Likes

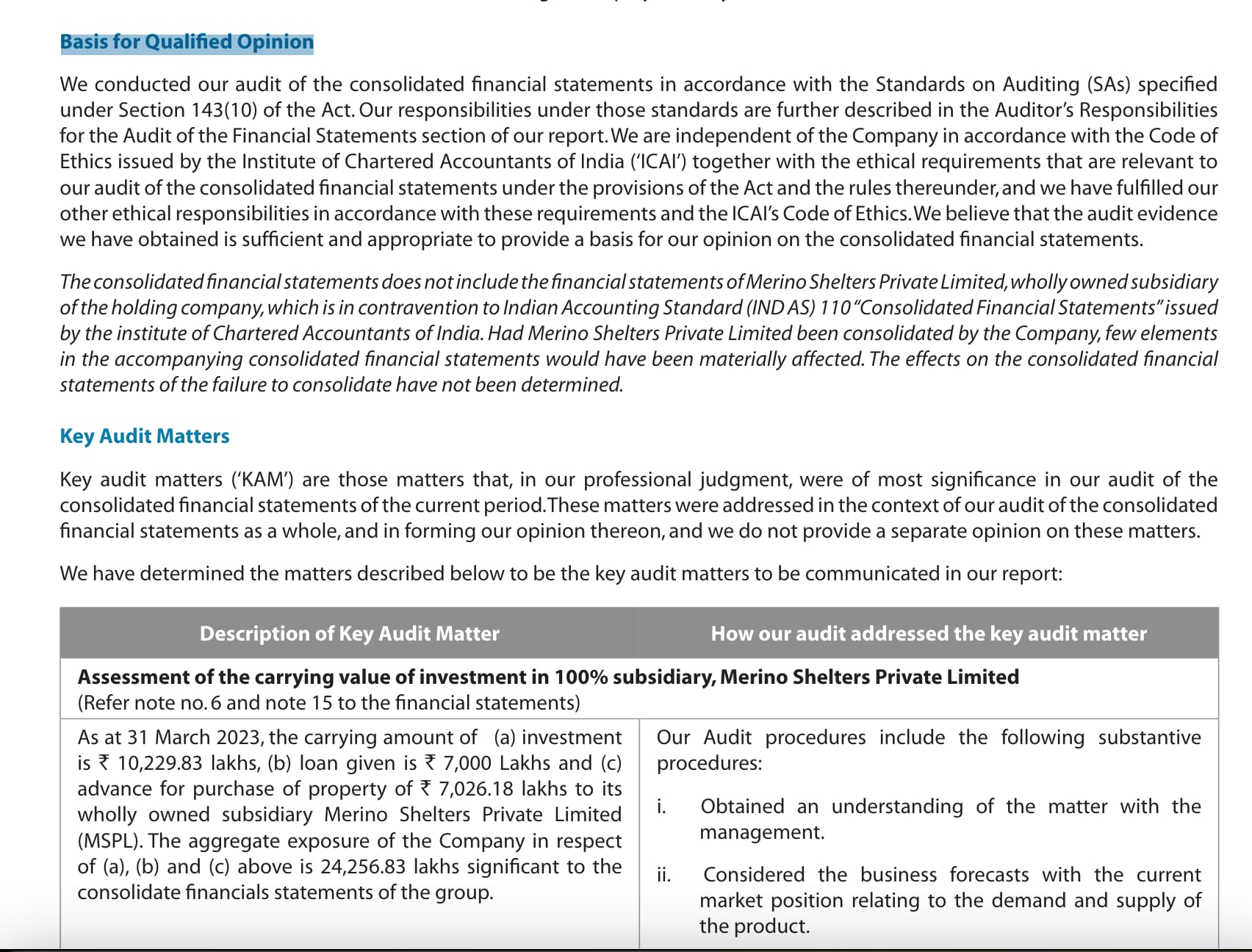

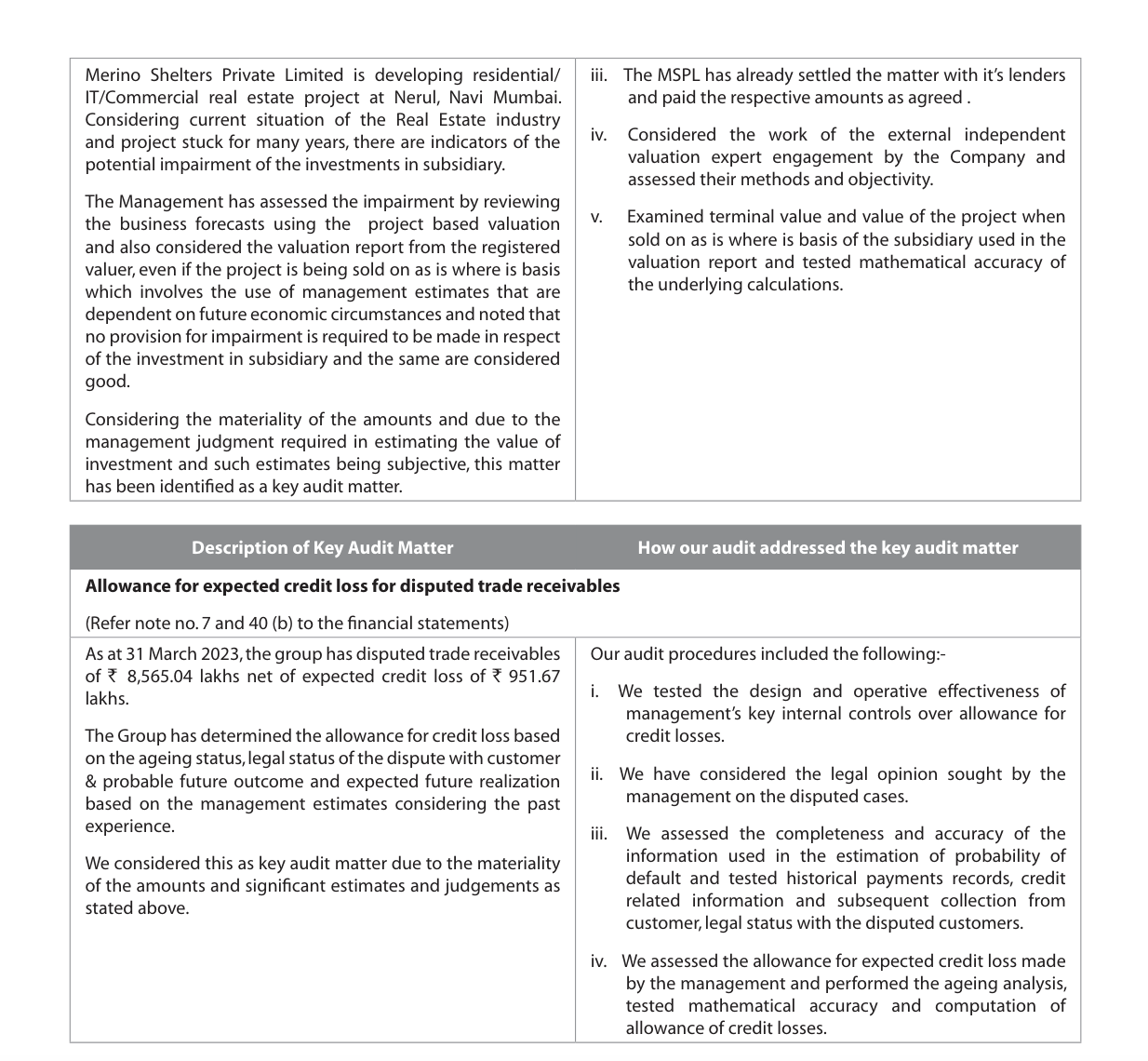

I started reading this company’s annual report for the fiscal year 2023 (FY24 is unavailable). I came across a related party transaction where they have given 70 crores (Rs. 700 million) to Marina Shelter (page 134). Let me know how big of a concern this is. The auditor has objected to this transaction and given a ‘Qualified’ status for the same reason.

2 Likes