Man has done almost 1000 Cr in H1FY21 and got orders of 1600 Cr out of which the company claims 1200 - 1300 Cr order will be completed by Q4FY21. So that makes the company’s sales about 2200 - 2300 Cr.

Man Industries is virtually debt free in last quarter.

This year FY21 sales will be 2200cr approx and Based on the management commentary, H2FY21 will be much better H1FY21

I just heard the last Con-Call in which the last question was a suggestion to reward shareholders with buybacks as opposed to dividends. It was met with such vehement opposition. Not so sure why. Instead of doing primary infusion into a cash rich company through warrants when there is no need of additional cash, isn’t buyback a better tax efficient structure and a route to increase promoter shareholding ?

The vehement nature of opposition is a red flag for me. Also, there was no indication of a more aggressive dividend policy and the management spoke like “You should be happy because we gave 40% of FV as dividend”. When you have no debt to repay and no capex plans, I do not understand why they should just hoard cash. The tonality of it is not inspiring

I think the rest of the questions on the con call were addressed satisfactorily

I am fairly new to this company. Is there somewhere where I can understand what the demerged balance sheet would look like ? What all assets are going to Man Infra ? Only Marino ?

Would request other members of the group to help as to where I can get this info

They have promoter’s pledged shares, Recently company reduced pledged share from 41.40 to 10.82%, which will be depledge soon, and they they have 760cr as reserve,but other liabilities including trade payables are 769cr, so not much cash in hand now

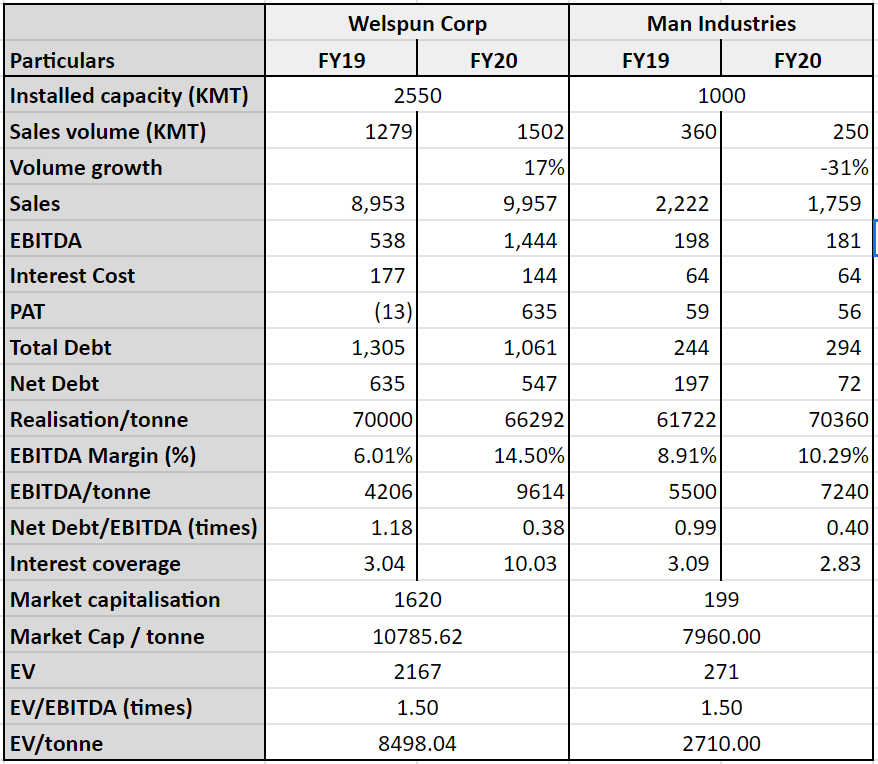

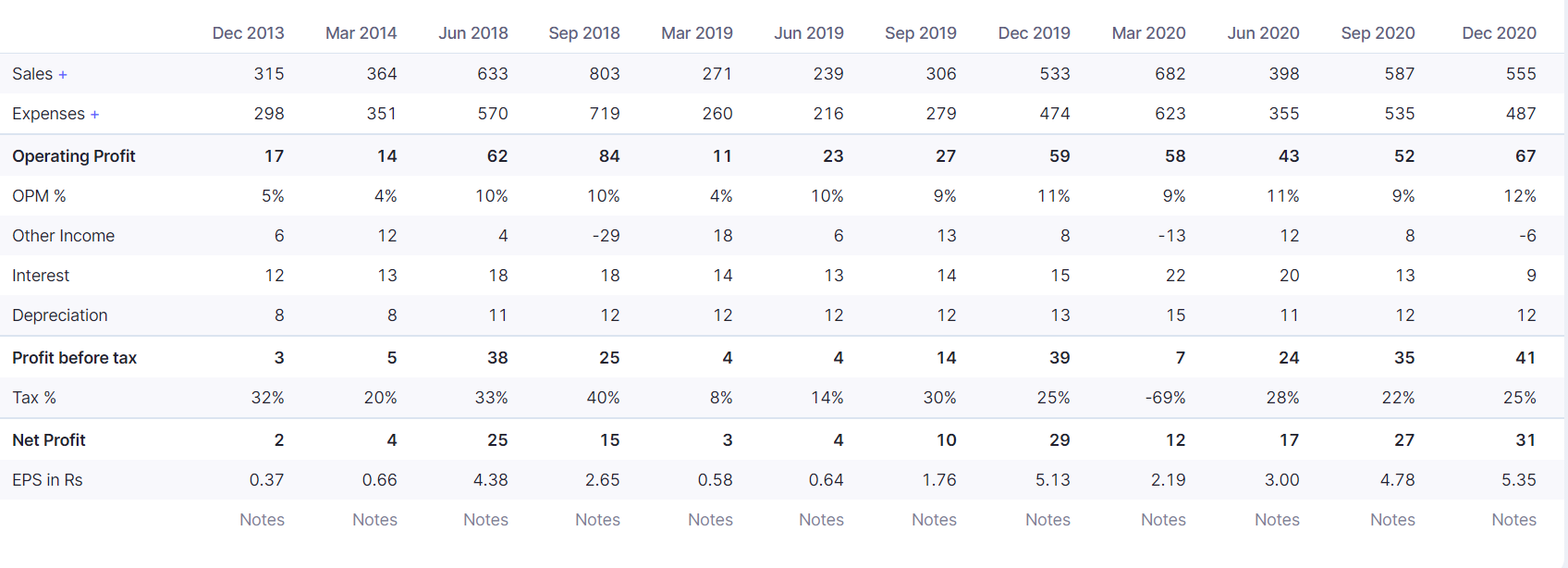

Man Industries come up with good set of numbers. Two quarters with good revenues, margin and PAT no. is commendable.

My estimate is margin will be in range of 10-12% as guided by management.

Order book is robust, with recent order of 250 Cr.

I work in middle east in petrochemical sector, can see visible traction in new projects for oil and gas, petrochemicals.

As management commented business have tail winds from oil & gas, govt of India is keen to develop gas pipe lines and water infrastructure.

Company have consistent dividend history, so earning will be distributed as there is no CAPEX plan.

All in all, Business have tailwinds, let us see when re rate company.

As said in book Dhando: Heads I win; Tails I do not loose much.

Concall is cancelled due to mother of CMD pass away (RIP).

Overhang will be of Man Infrastructure shares allotment, anyhow it is not too much important.

Going forward steady quarters with protected margin will make company more cheaper.

Good article on steel pipe manufacture company.

Before these companies ( Maharashtra Seamless, Man Industries, Ratnamani Metals and Welspun Corp) have one way for orders that is oil and gas.

Now they have in addition to oil and gas, they have water segment, natural gas and City Gas Distribution orders to bid for.

Nice article from Finshots.

Was deliberating whether to invest here.

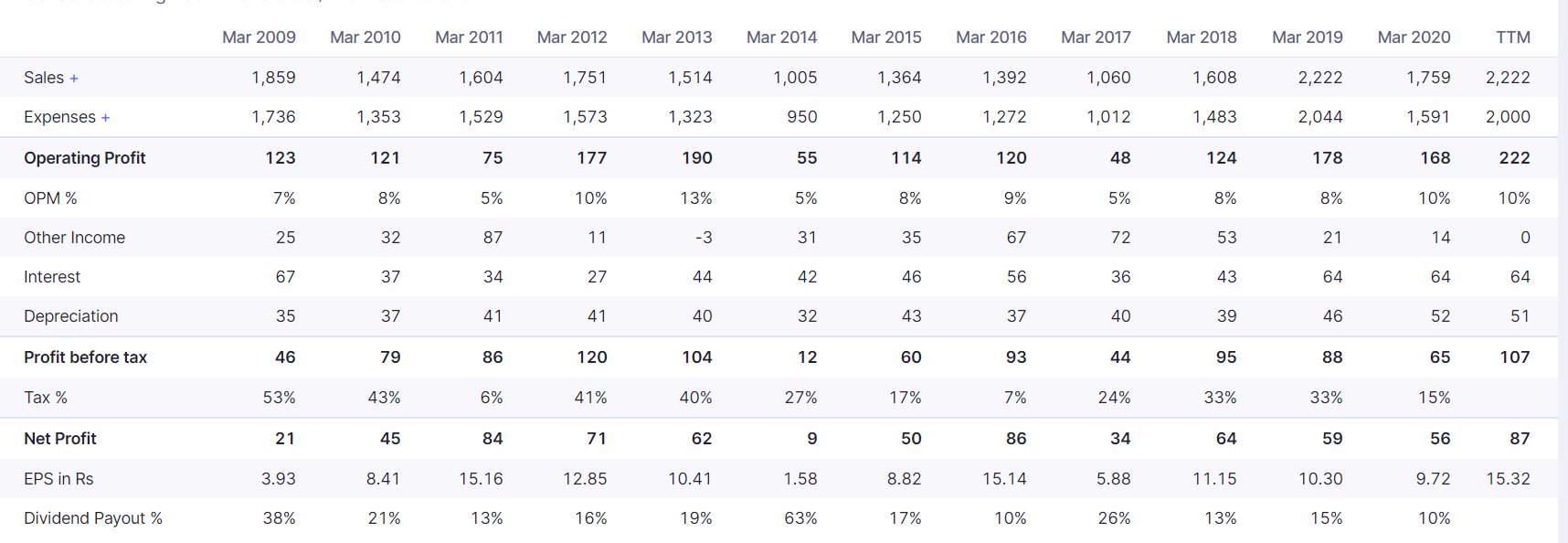

The future seems promising (based on probable tail winds) but the past seems abysmal.

The revenue growth the past decade is poor, profit growth is poor.

I understand one should not drive a car seeing the rear view mirror, but the company does not induce much confidence, except the fact that they have consistently reduced their debt.

I guess there are better sectors/companies to invest than this one.

Proposal to divest up to 100% in Marino Shelter. How much it valued will remain puzzle. however in 2018 my advisor tell, land parcel is worth 1000cr. In one of the concall management said they have line up with mall developer to develop this land. Let us see what come out from this.

One overhang will be over on company, as I do not see any other hurdle as it is in their control.

For Man Infra share allotment, still we are waiting.

Disclosure: Invested

Current capacity is enough to grow without CAPEX for current business.

New line to cater city gas distribution plant in Gujarat, which is having a higher margin. April 2022 will be online.

Cash flow reduced due to export order and receivable got stuck up in march, released in april and may.

Rising steel prices: back-to-back tie up. the impact will be minimal on us.

Share holder value creation: Review in few months, money invested in City Gas Distribution.

Margins in ERW/CGD: For ERW topline 800 to 1100 addional reveneue. capacity 125000 Tons. Existing player, welspun, maharastra seamless, surya roshni, ratnamani. Focus on seamless pipes used in defence. EBIDTA 10-12%.

Other income: 17 cr. is on foreign exchange. export incentive is part of bussiness. Write off of 33 cr. Annual write-off 70 cr. Still, 15-20 cr left to write off. which are pending for receivable since long, some may be recovered.

MIS: New scheme by the government for export incentive, rate not decided. loss is 17-18 cr.

Average cost of debt 9 to 10%. 1.5 to 2.0% for raw material bank credits.

Marion is the top priority, discussion ongoing. 110 cr. investments.

Only 3 to 4 % is pledge, will be released in few months.

Outlook: hit of covid in April. capacity utilization at 60 to 70%.

Dividend distribution policy approved and uploaded on the website.

The unexecuted order book as on date stands at approximately Rupees One Thousand Five Hundred Crores (approx. Rs.1500 Crores) to be executed in the current financial

year.

If we extrapolate this to the entire year, the sales are going to be in the same range as previous year. Unless new orders get added and executed during the rest of year, I do not see significant YoY growth.

Concall highlights

Nikhil is appointed as MD, giving command to new generation. 1. How Nikhil will improve performance: Cut down on OPEX, de bottlenecking, Focus on marketing to get better orders with better bottom line. 10% growth year. EBIDTA margin after 3 years 15%. Minor shareholders are replied on time. Keep improving to change company’s image.

2. Raw material fluctuation: is tackled by back to back arrangement. Once order received, order is put with steel mills. May be 10% kept open ended.

3. Margin: For 1500 cr order book, expect 30 to 32% gross margin for full year. Ebidta 11 to 13%.

Capacity at 40 to 50%, with current capacity we can do 3500cr/4000cr revenue depend on product mix. 4. Debt: No long term debt. Working capital 100cr. 5. Corporate Announcements:

Marino Shelter get few serious inquiry, that will help in capex. Asked Bankers to get NOC. Hope to finish by year end.

Man Infra: record date is given by court. Court suppose to act. 6. Growth:

Bid book of 10000cr. Historical win ration is 5 to 10%, expected to be same.

Growth of 10% in with top line. Can depend on quarterly number. In next 3 years, 3500 cr. Water orders are more, but EBIDTA are less, so we take less water orders. 7. Receivables: Last quarter was 700 cr. This quarter 450 cr. 8. ERW: Expected machinery delivered by March and 3 months to commission. Full swing by Q2-22. 5 to 6 players . Market share will be 10 to 15%. Company will pursue API, not water. 11 to 13% EBIDTA in API pipes for City Gas Distribution. Year 2023-2024 can be 800 cr revenue from ERW. 9. Water: Will not be aggressive. only bid for orders that gives our required EBIDTA.

32a05237-91fa-434b-9592-2146b32d448b (1).pdf (66.2 KB)

The company has received new orders worth approximately Rs. 225 crores (Rupees Two Hundred Twenty Five crores) resulting in the new orders tally reaching approximately Rs. 900 Crores

MIIL is one of the largest SAW pipe players in India with a combined capacity of 10 lakh tonne per annum, distributed equally between HSAW and LSAW.

#Thesis

Revenue should grow by over 20%, with steady operating profitability of over 10% for fiscal 2021

Higher-than-expected cash accrual, moderate capital expenditure (capex) plans, increased focus on working capital and additional working capital lines would aid liquidity profile and support future growth.

Additionally, MIIL expects to divest stake in its wholly owned subsidiary, Merino Shelters Pvt Ltd (MSPL), which could further support liquidity.

MIIL is likely to become term debt free by the first half of fiscal 2022.

Liquidity Adequate

MIIL has adequate liquidity driven by expected cash accrual of more than Rs 120 crore per annum in fiscals 2021 and 2022 and cash and cash equivalents of Rs 238 crore as on September 30, 2020.

Strengths

Established position in SAW pipes industry**

The domestic pipes industry is consolidated, with the top four players accounting for 80% of capacity. Limited competition is due to large capital requirement, and necessity to have critical accreditations and customer approvals. MIIL is amongst the largest SAW pipe players in India, and produces both helically submerged arc welded (HSAW) and longitudinal submerged arc welded (LSAW) pipes. It has been manufacturing SAW pipes, branch pipes, and coatings since 1995.

Weaknesses

Susceptibility to cyclicality in end-user industries and to volatility in raw material prices and forex rates**

The Man group has historically derived over 85% of the revenue from the oil and gas segment and the remaining from the water and irrigation segment.

Moreover, there is a 2-4 month lead time between application for, and the final award of, a tender. Because these contracts are of a fixed-priced nature, the Man group cannot pass on increase in input costs to customers after applying for the tender.

Working capital intensive operations**

Gross current assets have been more than 200 days in the past, driven by inventory of over 100 days. Over the medium term, the working capital requirement is expected to rise with increase in the order book. Also, concentration in receivables renders MIIL susceptible to further increase in working capital cycle, and remains a key monitorable.