Hi Harshitt

Yes got the reply yesterday only, reproducing below:

Dear Mr. Kohli,

With reference to your earlier mail regarding queries which you raised, please find below**(Highlighted points)** the clarifications for the same.Hope this will resolve all your queries.

1. Employee Remuneration :

Basic data from Annual Report 2021-22 :

a) Total expenses on Salaries, Wages & Bonus : 1323.43 Lakhs INR (src page 78)

b) Remuneration paid to KMPs : 87.71 Lakhs INR (src page 81)

c) Means remuneration paid to non KMP employees : 1235.71 (a-b)

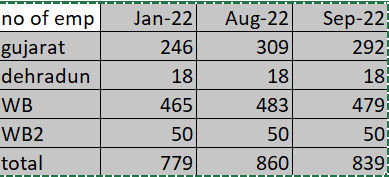

d) Total employees (permanent + contractual) : 2890 (src page 22) - 4 KMPs = 2886

f) Employees under Gratuity : 328 v/s 372 last FY (src page 80)

g) Average basic salary for employees in gratuity : 8844

Concerns:

- Company is paying too low salaries to its employees. Based on the above data annual payout per employee is Rs. 42,817 (c/d).

Mallcom: Please appreciate the company do employ on direct and contract basis and the total no. of people engaged is in the range of 2890, whereas the total employees on payroll as reported on page 29 of Annual Report is 570. For a total employee cost of Rs.1175.70 Lac, average salaries per employee comes to Rs.2.06 Lac / Annum.

- Number of employees under the gratuity scheme is too low

compared to total employees.

Mallcom: As mentioned above the total no. of permanent employees are 570 and no. of employees 328 is comparable with the total no. of permanent employees.

- Number of employees under the gratuity scheme has reduced by 12% in 1 year , which is too high for a growing company.

Mallcom: A total no. of 44 employees moved out of the gratuity coverage out of total 372

nos. i.e. 12%. We would like to see that employee’s continuity improves over the period.

- Average salary of employees under Gratuity is close to minimum

wages.

Mallcom: Average salary under gratuity is referred to Basic Salary for the purpose of gratuity calculation, which is almost 40% of the total salary as per Industy standards.

- Data of employees under Gratuity is same under Consolidated &

Standalone report, indicating lack of experience & expertise in

subsidiaries.

Mallcom: There is a proper integration in Managerial work for the company and its subsidiaries [Mallcom, MVSFT & BEST SAFETY] all units within FSEZ and is managed therefore by common team with long experience in overlooking SEZ operations. These employees continue to remain at the payroll of the MIL.

Also, One of the subsidiary i.e. MSPL has started its operations during the second half of FY 21-22 and therefore will not have any gratuity liability.

Questions:

- Is the company ensuring compliance to minimum wages to its employees as defined by Office of Labor commissioner, Govt of West Bengal wide Memo No. 108/Stat /2RW /9/2022 /LCS /JLC

Mallcom: Yes All employees under Mallcom in West Bengal has minimum wages compliance as per its latest circular.

- Is the company verifying compliance of its labor provider to its contractual employees w.r.t. above referred requirements ?

Mallcom: Yes, all of our labor contractors are govt. registered and duly authorized by the local authorities to operate and are under contractual obligation to comply with all the labour laws including payment of minimum wages to contractual employees and the compliance thereof is verified by us.

- What is the break up of Permanent & Contractual employees out of 2890 ?

Mallcom : We have 570 permanent employees and rest are under contractual basis as on year ending March 2022.

- What is the average monthly salary of a permanent blue collar employee ?

Mallcom :Average Monthly Salary of a Permanent Blue Collar employee is Rs.13K/ Month.

- Have you booked workmen compensation under some other head as well under expense statements ?

Mallcom : Yes, the employees benefit expenses refers to payment to permanent employees only. The total wages payment to both permanent & contractor employees will be around Rs.60 Cr. [Including fabrication/Processing& Labor charges booked under Manufacturing & other operational expenses] and average cost per employee therefore will be about Rs.2.07 Lac per annum.

- Why has experience & expertise been consolidated in a Standalone entity, with no employee >5 years experience in subsidies ?

Mallcom : Please appreciate that Mallcom is a flagship company engaged in business for last 40 yeras. All business growth and expansion therefore originates from the parent company. Both 100%subsidiaries having units in Falta SEZ had been acquired for capacity expansion within the same zone, where Mallcom already had existing operational units. Being at same place, these units are being managed by same team with significant experience in PPE gained working in Mallcom.

2. Largest Individual Investor:

Basic data (src. available annual reports)

- One individual NRI investor Mr. Jay Kumar Daga is holding 18.42% equity under public shareholding.

- Mr. Daga has done gradual dilution in his ownership from 22.44 % in 2015

Questions:

-

Is Mr Daga related to Mallcom’s Promoter family ? please cover both friends & family part here.

-

Is Mallcom’s management aware about any relationship of Mr. Daga with M/S AB Holdings ?

Mallcom: No, Mr. Jay Daga is not the part of Mallcom’s Promoter family. Mr. Daga,

acquired the stake in company almost 11 years back from our outgoing foreign

collaborators and is known to us as an investor in PPE domain .

Yes, we are aware that Mr. Jay Daga is associated with M/s AB Holdings and the

association with AB Holding as stake holder in Mallcom safety is purely on brining

business on board for Mallcom Safety .

3. Availability of Annual reports : Since the company was listed on Calcutta & Delhi stock exchanges prior to 2016, earlier annual reports are not available on public forum. Hence request you to please share annual reports from 2006-07 to 2013-14.

Mallcom: Noted the requirement. Do let us know your mailing address, where hard copies of Annual Report can be sent as per your requirement.

We really appreciate your interest in the company and look forward to your association with a fast growing & professionally managed entity engaged in a unique product category i.e. PPE from India. Thanks for your patience and co-operation.

Regards,

Anushree Biswas

Company Secretary

P: +91 33 4016 1050

E: anushree.biswas@mallcom.in | W:www.mallcom.in

Mallcom (India) Limited

EN-12, Sector 5, Salt Lake, Kolkata 700091, WB, India