Helmets; i am referring to be lighter (not thinner).

Key is mining industry.

1 Like

My bad. I accidentally wrote thinner instead of lighter. ![]()

I have worked in oil and gas and I have friends in the mining industry. We are required to wear helmets on site and these things haven’t really changed much over time. Surely they have gotten lighter over the last decade but nobody is complaining about their weight. They aren’t that heavy. What I am trying to say is that there is no catch 22

1 Like

I think there is an increasing trend of ensuring that the ‘cost of life’ is important - whether it is ensuring safety compliances are in order or workers are thoroughly insured - either through ESI or private general insurers. I see this as a proxy play on manufacturing alongside increasing push of compliances for safety norms.

2 Likes

Recently I attended IREE 2023 , RAILWAY EXHIBITION at pragati maidan , mallcom had thier stall , after talking to that respresentive person, company is expanding thier sales where there is possibility, one interesting things happen one of the railway person might officer level come & asking everything and asking him to meet in office & exchange thier business card , my interaction is mallcolm is third mfg of good leader, in India & UAE they are expanding with thier own brand name, peer competitor is karam & liberty , arvind fashion.

But not any player who provide all things under one roof.

Usually helmet & safety shoes is one year replacement & clothes depends from six months to 8 months.

Another ground work

Talking with some executive person where bullet train ![]()

![]() work is going, they said now govt is so focused on labour safety

work is going, they said now govt is so focused on labour safety ![]()

![]()

![]() , if any worker doing job without safety shoes & helmet,there is penalty of 200 rs /days / labour ,

, if any worker doing job without safety shoes & helmet,there is penalty of 200 rs /days / labour ,

Safety officer is appointed, I asked India me chal nahi jata , ye sab temporary hota hai, jugaad ho jata hai, he tell me that saab ab nahi hota, drone se watch hoti hai hum par . Take this scuttlebutt as pinch of salt. Just sharing what I observed might be wrong ![]()

disc invested in MALLCOLM 2-3 % portfolio.

16 Likes

Meeting with the management of Mallcom within the next week, please share list of questions (if any).

1 Like

- With increased pressure on topline, what initiatives company has planned to protect bottomline ?

- Specifically, what initiatives have been planned to increase working capital’s efficiency ?

- One key large investor “Jaya Kumar Daga” has history of selling at every rise. This has overhang on the stock price & deterrence for new investors. Does company has plans to engage him better?

Regards

9 Likes

Hi Charanjeev,

- With increased pressure on topline, what initiatives company has planned to protect bottomline ?

→ the company is moving into more certified products and more cat-2/3 products where it faces lesser competition from the unorganized markets - Specifically, what initiatives have been planned to increase working capital’s efficiency ?

→ Within India they anyways operate on very minimal credit days (some 7-9 days), as share of Indian business increases with Sanand going live, the working capital situation is expected to improve; apart from this they have Oracle ERP which is being used for production planning and inventory management and salesforce CRM to track dealer and their sales team productivity - One key large investor “Jaya Kumar Daga” has history of selling at every rise. This has overhang on the stock price & deterrence for new investors. Does company has plans to engage him better?

→ The investor Jaya Daga has been invested in the company since atleast 2005, and is now looking to exit, there is nothing specific apart from this as to why he’s exiting,

Do note: the stake in MSPL was given to AB Holdings (which is a family office of Arindam Bose and Mr. Daga), and post the mgmt buying out their stake in MSPL, Mr. Daga has started to exit

Hope this helps

13 Likes

Apart from these responses, any other key take aways from your visit that you can share with this forum.

1 Like

Summarizing the overall discussion:

Mode of discussion: online, not in person

Focus of discussion: To understand more about history and evolution of the company

Attendees from Mallcom: Rohit Mall and their CFO

Points discussed:

About Mallcom:

1. Rohit Mall is part of the second generation of the management, and has been with the company for 2.5 years

2. Over a period of time the company has moved on from mono-line (leather gloves) to multi line products of hand, body and feet protection; head protection is a new business line they are entering into

3. Over the last 7-8 years, the co has changed it objectives towards growing more in the Indian markets as well as going higher margin business and becoming more proactive; the last few expansions have been unlike what Mallcom was used to doing earlier, now they are building capacity in anticipation of demand

About Industry:

1. Globally China dominates the industry with 70% market share

2. With China+1 wave, parallel supply chains are being developed and RM supply for non-leather material increasing

3. Private Equity players are also taking interest in development of this supply chain and enabling connections between clients and manufacturers

4. Indian market is about 12-15,000 cr market with half of it being un-organized

5. Indian market currently don’t have certification standards, BIS is trying to setup something and Mallcom is also pushing for these certifications to get developed

6. Purchase of the items is being influenced by plant heads and sub-heads with safety/functionality and aesthetics being considered into making these decisions; PSUs are buying through the GeM portal

USP:

1. Head to Toe → One stop manufacturing

2. European standard products

3. Certified products only, Mallcom hasn’t taken a price cut till now, but has actually raised prices for its products

4. Mallcom doesn’t bypasses its distributors even if it wins the deals

Mgmt team and structure:

1. Continuous investments being done towards plant and products

2. HR talent pool is being developed with a focus on building 2nd line of mgmt

3. The teams have dedicated KRAs

4. In the next 10 years they expect totally new set of people to take up the business

Sales and Production:

1. Sales team structure:

a. White Label: Geography followed by sales RM structure; for big clients there are dedicated sales team/RM

b. Branded: Area Sales Manager approach which are then bifurcated into geography and product line

c. The teams use Salesforce CRM to track the performance of the dealers and teams

2. Production Planning:

a. White Label: Almost back to back order based

b. Branded: Depending on the product category and past trends, the production happens through a mix of inventory stocking (eg. Shoes 60-70% are stocked) and customer back to back

c. Co uses Oracle ERP for production planning and inventory management

3. The mgmt focus is on the top-line and bottom-line growth (i.e. not necessarily RoCE or working capital)

4. New Product Development: New product development is more led by the teams developing the products internally and then trying out in the market; however inputs to developing these products is driven by

a. Based on the number of enquiries received for a particular product

b. Competition catalogue whats getting more presence

c. Tracking of Imports

d. Company’s capability wrt infra and RM and being able to manufacture the product

e. Co is open to outsource the product development initially and giving samples to get feedback before committing resources

f. Is the product going to be margin accretive

FY28 targets:

1. Co has taken up a target of 1000 cr, internally they also know it’s a stretch target, but wants to hit a number closer to it

2. FY28 sales mix is expected to be equally divided across categories of head, hand, body and foot protection

3. Given head is 2% of sales i.e. ~8cr and FY28 target would be 250cr, the company is investing in making injection mould capabilities to develop helmets

4. This helmet product portfolio to also enable the co to start catering to construction industry which it was not able to do earlier; fall protection and harness are other products required by the industry, but Mallcom not looking at those lines

5. Mining industry is expected to drive demand for products

AB Holding:

1. MSPL stake was provided at around 30 rs and bought back at 24 rs (at book value)

2. The idea was for AB Holdings to help connect with customers in Europe and ME

3. It didn’t materialize as per plans and AB Holdings offered their shares to be bought back and Mallcom did the same at book value

Plant specific discussions:

1. Ahmd Plant: Max util level is going to be 65-70%; currently at 50%, challenge is to find trained manpower

2. Sanand Plant:

a. 108 cr capex provides optionality of launching other product lines and therefore the asset turnover expectation is lower (100 cr on 108 cr capex)

b. The product of nitrile gloves is not the same as the medical gloves that top-gloves is manufacturing, but is industrial nitrile gloves

c. Expected Plant payback period of 4-5 years

3. Kolkatta:

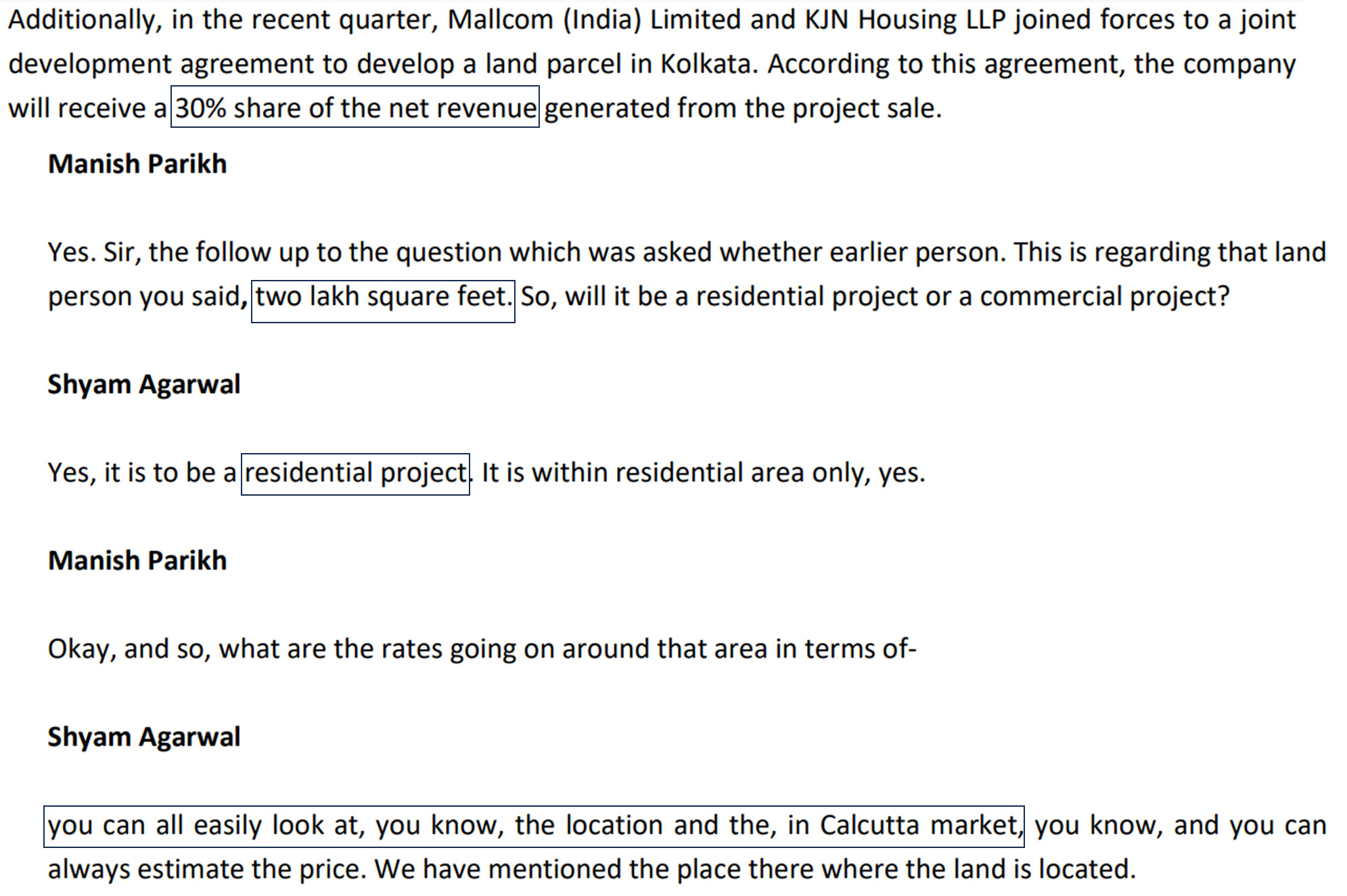

a. Consolidation of plants is underway

b. Revenue from sale of land through housing project atleast 2-3 years away

What keeps management up at night:

1. Capex utilization

2. People availability and costs

27 Likes

by any chance, does anyone knows which companies are their OEM clients ? is there any conversation of manufacturing for 3M as well?

They do OEM’s for Honeywell and Bansal etc. This was stated in the Q2 call. There is a good probability they do some work for 3M as well.

1 Like

I visited the store which sell safety shoes and helmets. The dealer strongly recommended Torp Shoes. He said if you are price bound you take Mallcom (The company gives 6 months warranty)

He kept very less varieties of shoes from Mallcom (when I asked about any discount on the bulk purchases he denied saying there is very less margin in selling this but we can give discounts in Karam and Torp)

I wore all three brands of shoes and tried almost 6-7 shoesMallcom shoes have a very thin sole and the metal part which is kept near the toe for prevention of injury in the case where a heavy object falls on the ankle so there wasn’t enough cushion in Mallcom shoes so it gave pain in my toe.

Karam had a cushion but it was thin. Torp had a super good cusion.

Mallcom seems to Target a low-price market while Karam is a premium market product.

All are certified shoes.

He said there is not much price difference. He said whats different in any helmet. It’s all same just that brands like Mallcom Karam give 6 month warranty and local players don’t but workers buy local products. No certification here.

20 Likes

Mallcom is mainly into the red and yellow category and the torp is in green category. Karam is in yellow and some products in green.

13 Likes

Best analysis sir, good questions

1 Like

Would appreciate if anyone knows and can share the ballpark range for the below puzzle:

Source: https://www.bseindia.com/xml-data/corpfiling/AttachHis/a9fa0331-7336-4e86-ae91-45ee708665c2.pdf (Page 4 & 18)

Recently went for some scuttlebutt to some of the local dealer of safety shoes. These were stores which had multiple brands.

Mallcom is a brand that has been in the market and is selling under the brand Tiger for more than 15-20 years so every worker thinks that’s a good product. The brand recall is super strong but that is slowly fading as majorly they are doing hand-stitched shoes and players like Karam and T- Torp is changing the game by launching more and more machine-stitched shoes. Mallcom shoes get torn and the sole of the shoe also comes off (Surprisingly this was told by 2-3 suppliers which are multi-brand suppliers. So this should be a big question on their quality)

Karam shoes come in the range of 1300-1600 (Very high and good quality)

T Torp shoes are 1000-1200 (Mid price range and good quality)

Mallcom shoes are for 800-1000 (Lower price okayish quality)

There are players like Allen, and Tata (Tagra) but they are very premium and very expensive so if you give bulk orders the dealer can tell them.

Mallcom shoes are taken by workers who can’t afford higher quality products. They don’t understand that it will give them ankle pain in the long run as Karam shoes have a comfort cushion.

There are few spaces where certificates do matter (The distributor indirectly said to me we can give you whatever certificates you need which means there can be fake certifications by unorganized but not sure about this if this is a general market phenomenon as sample size is small)

16 Likes

#MALLCOM

QOQ 20 % growth in revenue

QOQ super margin expansion

Yoy flat growth

YOY FLAT MARGIN.

Disc as before 2-3% of my portfolio, not sebi registered

2 Likes

What’s the reason for today’s upper circuit? Can someone help me understand this please?

1 Like

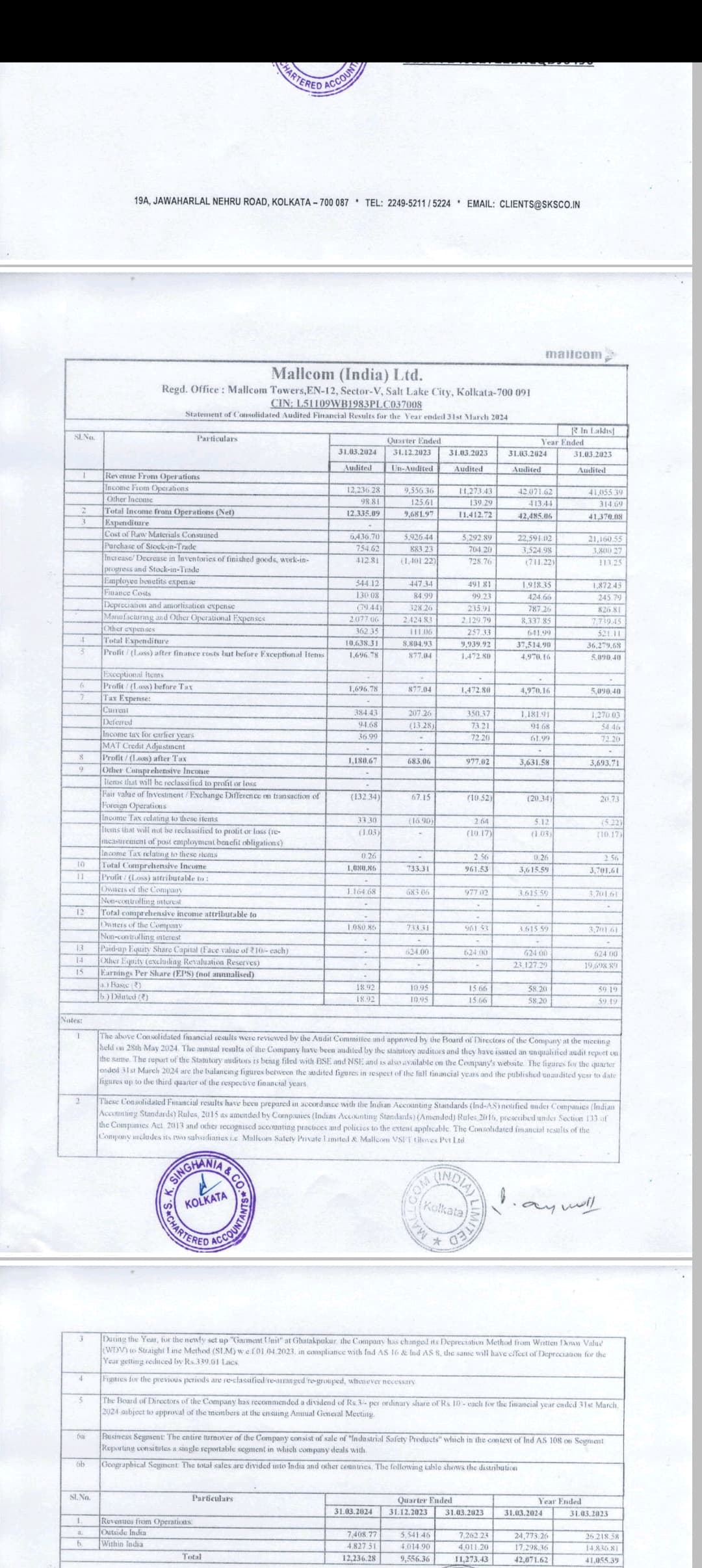

Mallcom Q2 FY25 Results, Earnings Quality/Conference Call highlights

Overall, while Mallcom has delivered fair (yoy) top-line growth in Q2 FY25, the decline in EBITDA margin has to be closely watched in coming quarters, although management tried to justify it as aggressive investments in branding, promotion, and expansions. Got to see how these translate into sustained revenue and margin improvements in next few quarters.

Few interesting developments are the launch of website new e-Commerce site that can now cater to both B2C and B2B orders/deliveries, along with revamped e-brochures - domestic and the export brochure (private label). I tried to order few products to my home town in Kerala and the delivery is within in 10 days and has all payment gateway options.

Also, seeing some increased number of expo participations and promotions of product launches in their multiple social media handles, like a recent one on ‘INFERNO’ - flame resistant work wear! Hope these efforts will turn to numbers in medium term. Below are few takeaways from latest Investor presentation and conference calls.

New Product Launches and e-Commerce website launched in Q2 FY25

- A new e-commerce website. This website was launched to cater to both B2B and B2C demand, providing customers with direct access to Mallcom’s range of certified products at list prices.

- A newly designed single-density sole with Docker and Doxle range of shoes having wider toe caps for the Indian market. This launch caters to the evolving demand in the Indian market, where customers are increasingly seeking value-added and user-friendly products.

| Metric | Q2 FY25 (INR Mn) | YoY Growth | Margin (%) |

|---|---|---|---|

| Operating Revenue | 1,291 | 19.2% | N/A |

| Total Expenses | 1,133 | 22.0% | N/A |

| EBITDA | 158 | 3.0% | 12.24% |

| Depreciation | 23 | (23.3)% | N/A |

| Finance Cost | 101 | 10.0% | N/A |

| Other Income | 21 | N/A | N/A |

| Profit Before Tax (PBT) | 145 | 16.9% | N/A |

| Tax | 44 | 37.5% | N/A |

| Profit After Tax (PAT) | 101 | 9.8% | 7.82% |

| Diluted EPS (INR) | 16.19 | 10.4% | N/A |

Insights on Earnings Quality:

- Declining EBITDA Margin: The EBITDA margin declined year-on-year from 14.22% in Q2 FY24 to 12.24% in Q2 FY25. This decline is attributed to higher spending on branding, promotion, and consultancy. While these investments aim to support future growth, their effectiveness and impact on profitability need to be closely monitored.

- Increased Operating Expenses: Total expenses grew at a faster pace (22.0%) compared to operating income (19.2%), contributing to the margin compression. The sustainability of this growth strategy depends on the company’s ability to generate sufficient revenue to offset these higher expenses.

- Inventory Levels: Inventory levels have increased in the first half of FY25. This increase is attributed to supply chain challenges and a strategic decision to maintain buffer stock. While this approach can help mitigate supply disruptions, excessive inventory buildup could tie up working capital and potentially lead to write-downs.

- Reliance on Export Markets: Mallcom generates a significant portion of its revenue from export markets, primarily Europe and Asia. While the company is actively pursuing growth in the domestic market, its exposure to global economic conditions and geopolitical risks should be considered when assessing earnings quality.

- Impact of New Product Launches: Mallcom is launching new products, such as PU gloves and helmets, and expanding into new segments like eye protection. The success of these initiatives will be crucial for driving future revenue growth and maintaining profitability.

Insights from Management Commentary:

-

Management’s commentary suggests a confident outlook for the future, supported by strong demand in both domestic and international markets.

-

The company is actively investing in expansion, new product development, and branding to capture this demand and achieve its ambitious growth targets.

-

Management acknowledges the challenges posed by supply chain disruptions and rising costs, but remains committed to maintaining a healthy margin profile.

As usual Management tried to paint a picture poised for continued growth. The company’s focus on expanding its product portfolio, strengthening its distribution network, and capitalizing on emerging market opportunities positions it well for the future.

Disclaimer: Invested and Biased. Less than 3% of PF, No transactions in last 30 days. Post purely for study purposes. Consult your advisor before any investment decisions.

1 Like

https://x.com/vectorconsultin/status/1901913212297068691?s=48&t=qmmdkDG3G9cyv-MnS0Jnvw

Seems that this consulting company worked with Mallcom ~2-3 years back. Point out some of the inefficiencies that they were able to correct.

Slow but steady.

Disclaimer - Invested for last couple of years. No recommendation.

2 Likes