Thanks @naveen062000 !

My concern is if IT dept has also the same data and able to differentiate between taxable vs non taxable distribution. Else there could be unnecessary automated notice and harrassment!

What does AIS portal show you? Is entire amount shown as interest earned?

As I can see in my last year Traces Forms both IRB Invit and Embassy REIT have reflected only the amount where TDS has been deducted and we have tax liability. Tax free return of Capital/Debt amortization being Tax free is not getting reflected and hence there is no concern with IT.I have invested from 2019 onwards and have all IT returns till this year are cleared without any concerns for my NRI/Family Resident IT returns.

Just adding an article which I read today about REIT as a good way to get exposure to commercial real estate.

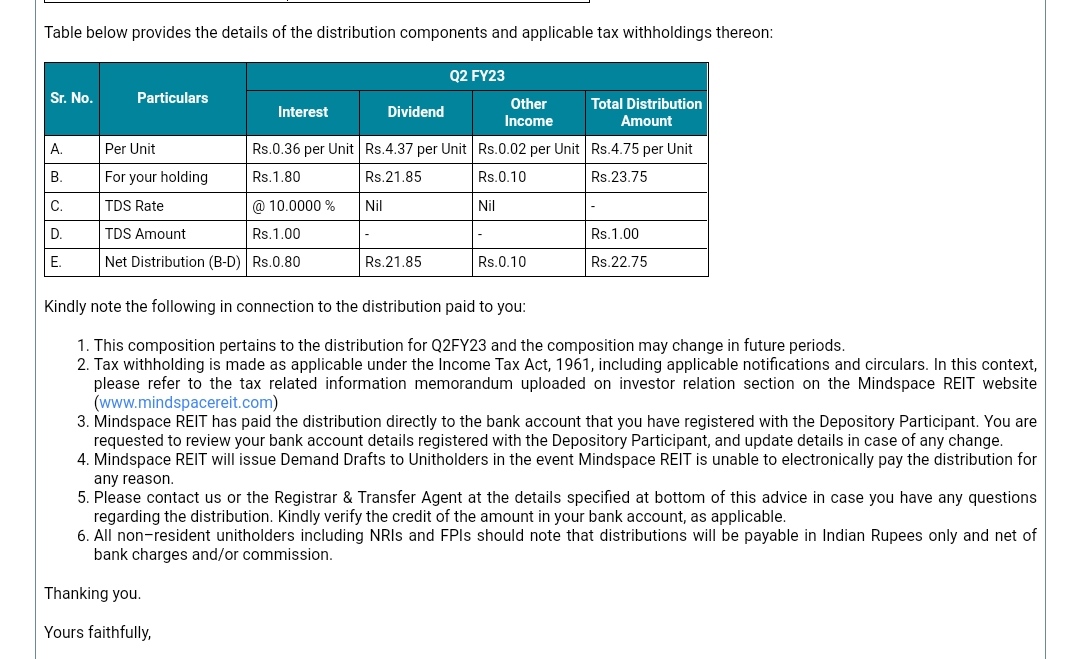

I took a tracking position of 5 units in mindspace REIT last week after going through the thread. I got an email today about the distribution which clearly shows how much is the interest, dividend, other income and total. @Malkd, Is only the interest part taxable for the individual / investor?

Yup. I have no choice but to sell all our holdings. The whole reason behind holding embassy was the tax efficiency. In reality at current prices its just about rs 2.5 being lost per share to tax but the overall reason for investing in reits is now gone for me. Need to look for a new investment to give me quarterly cash flows.

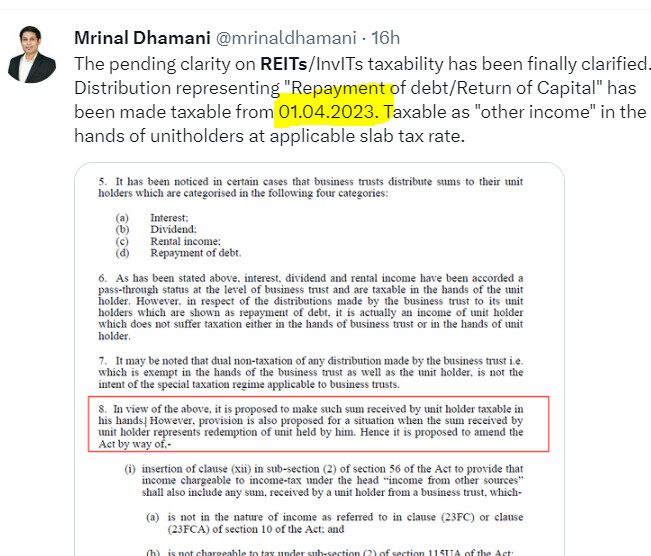

That being said… if this is enforced from FY25 they have a whole year to restructure payout and maybe bring it up to 60 percent tax free from the expected 50 percent. By FY25 payout should be rs. 24.5 or so… which means around rs. 3 to 4 will be lost from tax giving a tax free payout similar to this year so im still considering holding (as long as it isnt a typo and its wrt FY24 and not FY25)

knowing how the govt works and how systematically, they eliminate everything in the form of investment vehicle, I feel that the typo is in the 1/4/24 date and not the assessment year

Assuming payout of rs 23 in fy 24 that means 19.55 will be post tax vs the expected 22. At current price that would still give an approx 6 percent return post tax(vs nearly 7). Considering i am bullish about the payout increasing post FY25 it would still beat FDs but its a kick in the gut. Atleast this whole tax things is now clarified. May just hold on for a couple years and accept it as an fd and take the hit when it comes to zero/-ve capital appreciation since i only recently added more and dont want to take an actual loss since i would probably just transfer the cash to FDs only if i were to remove (since its part of my so called debt side lol) it AND take a loss too which doesnt make sense even if it gets painful to hold for the next few years. Maybe theyll figure out a way to give us a higher divend and less roc by then so all may not be lost… though i certainly wish i wasnt so heavily invested right now since along wiith this you have FD rates at above 7 + the issue with embassy group + higher interest rates can see a huge fall here over the next year and this was mwant to be capital protection

I have a very small stake in zydus since the beginning and have not added to it since since back then i preferred ITC as my FMCG bet. If the fall is even deeper i may have a look at adding some more. I have a lot of cash saved up waiting to deploy from my embassy sale so I’m actively looking at companies again. Will be going through zydus properly again over the next few days and will then decide what to do with it.

Tbh I’m Currently looking for companies to invest in and apart from adding more to laurus plus a punt on everest kanto(i am not sure about the long term thinking regards cng here and the capability of management to be nimble to survive) and maybe Zomato/jubilant foods (both still about 10 to 20 percent above my risk appetite) i honestly have no idea what to do atm. Been out of the markets so long and spent so long trying out faux debt ie embassy type instruments that I’m in a bit of a rut now lol

I’ve owned laurus since early 2020. It’s already a huge part of my PF and i haven’t sold a share since(post selling Deepak nitrite and embassy it’s at 70 percent of my PF even now). It’s one of those few businesses i know very well and am comfortable with. As far as I’m concerned nothing has changed in the long term story… it’s just that ARV/API getting hit has happened earlier than expected. It’s still on track regards everything else until 2027 and as a bonus we may finally have a humble Dr chava now who doesn’t go overboard and ends up over performing instead of the cavalier chava from 2020 with his over the top targets. Im not too bothered about paxlovid contribution etc in the short term either. There will be a replacement over the next few years. That’s how their business works. A year of consolidation with upward surprises is what can be expected for the next year or so… but fully expecting things to kick in to full gear in FY25/26. My investment horizon is atleast until FY28 end so I’m just going to keep enjoying(and surviving) the ride. These downturns happen with every company at some point and I’m just getting it for cheap again(note that a lot can go wrong until FY28 with fires/usfda/de rating due to margins decreasing and cdmo not working out etc… that’s the risk one takes with Pharma so hence why buying at lower valuations ie under 20 PE etc when NOT in the good times makes sense). Remember that they jumped from 200 odd crores profit to 800 odd crores just 2 years ago. 1 more year of consolidation at 800 crores is fine by me since there’ll be another huge jump again hopefully by FY25 when op leverage and higher margins and contributions from ex api kick in

Yup. As mentioned above. The whole thesis broke down with the government taxing repayment of debt. I got out at between 310 to 316 which meant about a 4 percent loss which i was willing to take(which works out well this FY since I’m loss harvesting from my huge Deepak nitrite sale mid 2022) considering this isn’t a laurus labs type equity instrument where there ll be an amazing upside if held for years. It’s supposed to be slow and steady and give monthly tax efficient returns. I won’t be surprised if the government ends up taxing the dividend part in the future too. I’ve learnt a harsh lesson here though… debt is debt… equity is equity. Never try to mix the two up. I have sold my entire stake but I’ve kept my wife’s stake. She was fine holding with the FD like returns for the next few years(and the upside post FY25 when leverage kicks in) but I wasn’t. I will be moving back fully into equity and ignoring any sort of faux debt type instruments introduced into the market(and yes… i am more than a little annoyed that i lost money due to the government taxing something I never even knew could be taxed ie repayment of my own capital)

Over the past year I’ve gotten too conservative. I’ve been watching and let go of too many opportunities ie irfc at sub 20, ptc at 70 rs, manappuram at rs. 80, zensar at rs. 201 among others. All of which i was sure were undervalued but I decided to not take any chances but decided to chase conservative bets like embassy and debt(grrr). Today I’ve finally decided to dip my toes in again with Everest kanto. results are expected tmrw and I’m expecting horrid results ie margins and pat compressed to a point where they’ll just hit single or low double digits pat. However, I’m not going to wait on the sidelines for further drops. I’ve divided my investment up into 5 tranches and bought one tranche today fully expecting the price to crash tmrw to supports around low to mid 70s… at which point il be adding my second tranche. infact I’m fully expecting the next 2 quarters to be a whitewash too so won’t be surprised if the prices fall further(at which point il add my last 3 tranches). Is the company cheap now? At book price… definitely. Is there potential here? Just a year ago predictions were for a 40 eps year and that year will still happen though it will be delayed to FY25/26. I was interested early last year and nearly twice the price so I’ve got a discount here by waiting. The management isn’t nimble enough, the sector has question marks around it… all in all its a horrible investment. But at current pricing I’m willing to begin loading up in anticipating for a huge opportunity over the next 2 to 3 years. I’ve realised my main strength is patience . So I’m willing to use it to chase bigger than normal returns in companies like this.

Disc: not a sebi advisor (and most probably an idiot too)

Hi Malkd sir…In my opinion Manappuram is still at lower valuation to buy for. I have buyed at 2 tranches one at 89 rupees and another at 112 rupees. Planning to buy third tranche at current price. Imo Manappuram still a good bet as compare to Everest kanto. Nobody knows when there be again difference in petrol and cng price will occur? Any why government will give any price cut in cng and vanishes its own income source?

Even if it takes 2 years for the price differential to occur(it doesn’t need to go to the lows of feb21 ie sub 50) when demand falls and supply increases it will fall. I don’t trust the government one bit regards their 2030 cng infra plan but cng infra but even assuming half their plan plays out and supply comes back to normal Everest kanto should do well in the long run. They don’t have much debt and they have cash… so even if their profit is in low single digits(or negative) for a few quarters that just means a slowdown with expansion and no dividend(already paltry) and they won’t go bankrupt(and even if they do they can sell some of their assets etc. That’s the beauty of buying around book value. The above is the worst case scenario though. Ideally they can move towards increasing production in other products ie hydrogen/price differential comes back/infra story plays out and this turns into a 40 eps per year and rerated company 2 to 3 years. I like the risk vs reward here especially since I’m putting a very small amount on the line that i can live without(since i have only 1 tranche invested with one more this quarter and the rest when things look a bit better next/the quarter after) and I’m already expecting the price to fall to low 70s and stay stagnant for some time.

Edit(post results): As expected(and hoped so that price stays low) standalone profit down to low double digits ie 10 crores and consolidated down to negative(due to an exceptional loss of 19 crores due to non fulfillment of a contract with a customer… need to check what this is in the concall). Expecting the price to now go to the low 70s. We are right at the bottom business wise atm and already cng prices are cooling a bit as of last week. Expecting q4 to be a washout too… will wait until the concall before adding the 2nd tranche. If they were struggling with debt and with no cash in hand i would be worried if this went on for a few quarters but they can easily handle this downswing now. My main worry is that the derating will be permanent now that the price differential for cng has proven it can disappear. Will be an exciting few months here.

I am quite hooked up with reading your views and in fact these have influenced mine investments in Invit/REITs, ITC,IRFC, UGRO and made me even track Laurus. I know that you have started sipping in Everest Kanto and may be thinking on your second tranche. What are your views on this quarter results and also on Corporate Governance concerns of their China subsidiary a few years ago.

Also share your views on Glenmark Life Sciences if you have track as its at tempting levels.

@amitvohra

Regards Glenmark… i don’t track it. But currently there seem to be a lot of opportunities in Pharma.

With Everest kanto the logic is simple. A black swan event has led to them struggling last few quarters. Had the company been in huge debt and with pledged shares etc i would be worried. However, they have cash in hand… minimal debt due to reduction last few years… and even in this darkest of circumstances they are able to churn out single digit profits. How i see it playing out is simple… A few more quarters of pain but with profits steadily rising to double digits by mid FY24 as cng prices drop. We all saw what they could do with cng prices at their normal levels ie hitting nearly 6 eps per quarter . Minus covid revenue and add their 40 percent brownfield expansion and they should hit 6 to 8 eps per quarter by FY25(or FY26 to be safe). At approx 30 eps even at a PE of 6 it would be a doubler from here(could be a 3 year wait but i have nothing if not patience and the company won’t go bankrupt until then even if the bad times continue for longer than expected). Add a few optionalities ie repayment of debt/turnaround or selling of loss making subsidiaries/increase of dividend payout to 10 percent instead of 3 /cng infra increases/shift to hydrogen etc over a 3 to 5 year period and there could be chances of a rerating too. Regards CG i went through the few allegations online + the everest thread and I’m comfortable. The reemergence of concalls(though not too great ones) and the fact they still own 67 percent of the company gives some comfort and shows that they are trying to get things back on track. Barring another black swan event we are currently at business bottom at near book value and it seems the ideal time to buy. I would never buy a business like this when things are going well and when the share price is rising and only good news ahead since there isn’t much of a moat and there are a lot of factors on the outside that affect it. But at present scenario the opportunity just looks very ripe to me. Im fully expecting the price to fall further(low 70s seems all but guaranteed… if it breaks below 60 and the overall situation is similar to today maybe there’ll something under the hood we don’t know and then id be a bit worried and i won’t add below that price) considering results + poor expected q4 but that will only increase the MOS with my future tranches(1 done… 1 near low 70s… none below 60… add remaining 3 as things improve and price near book value)