Hey all. So my portfolio is a bit weird. I love long term stories and all of my companies chosen have brilliant stories going for them

FMCG:

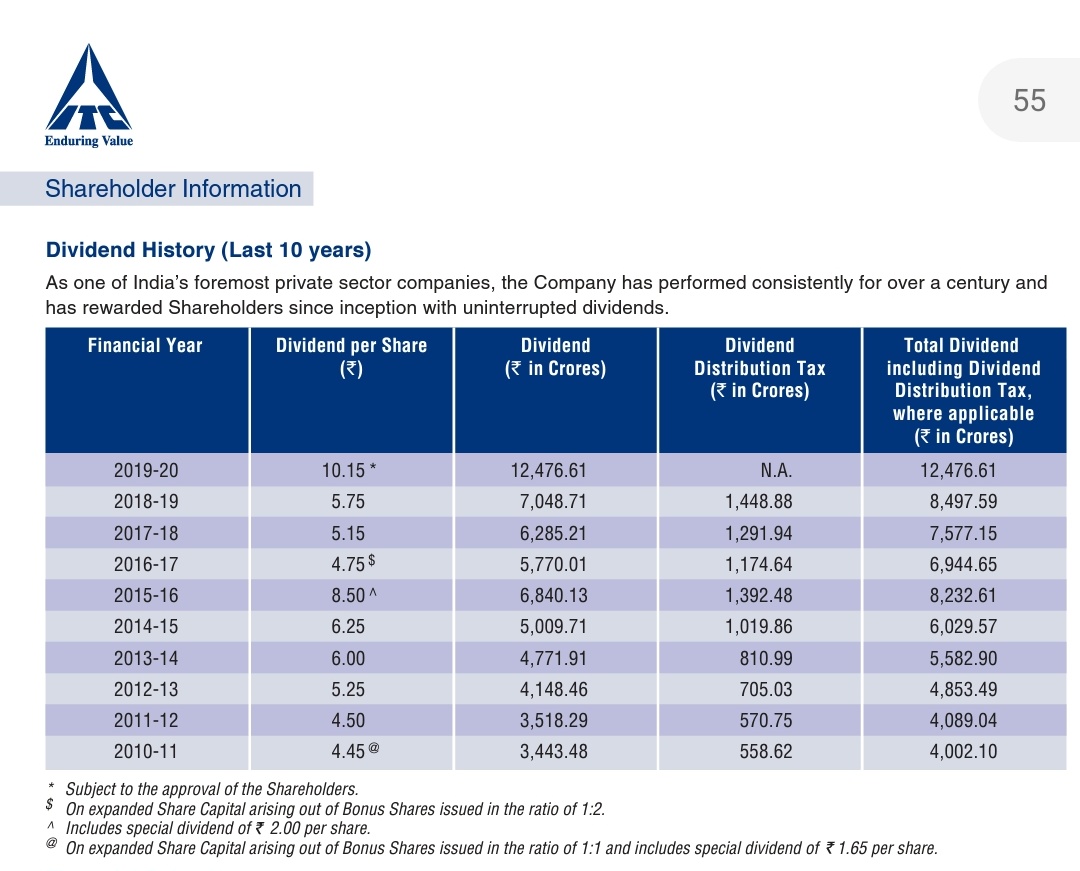

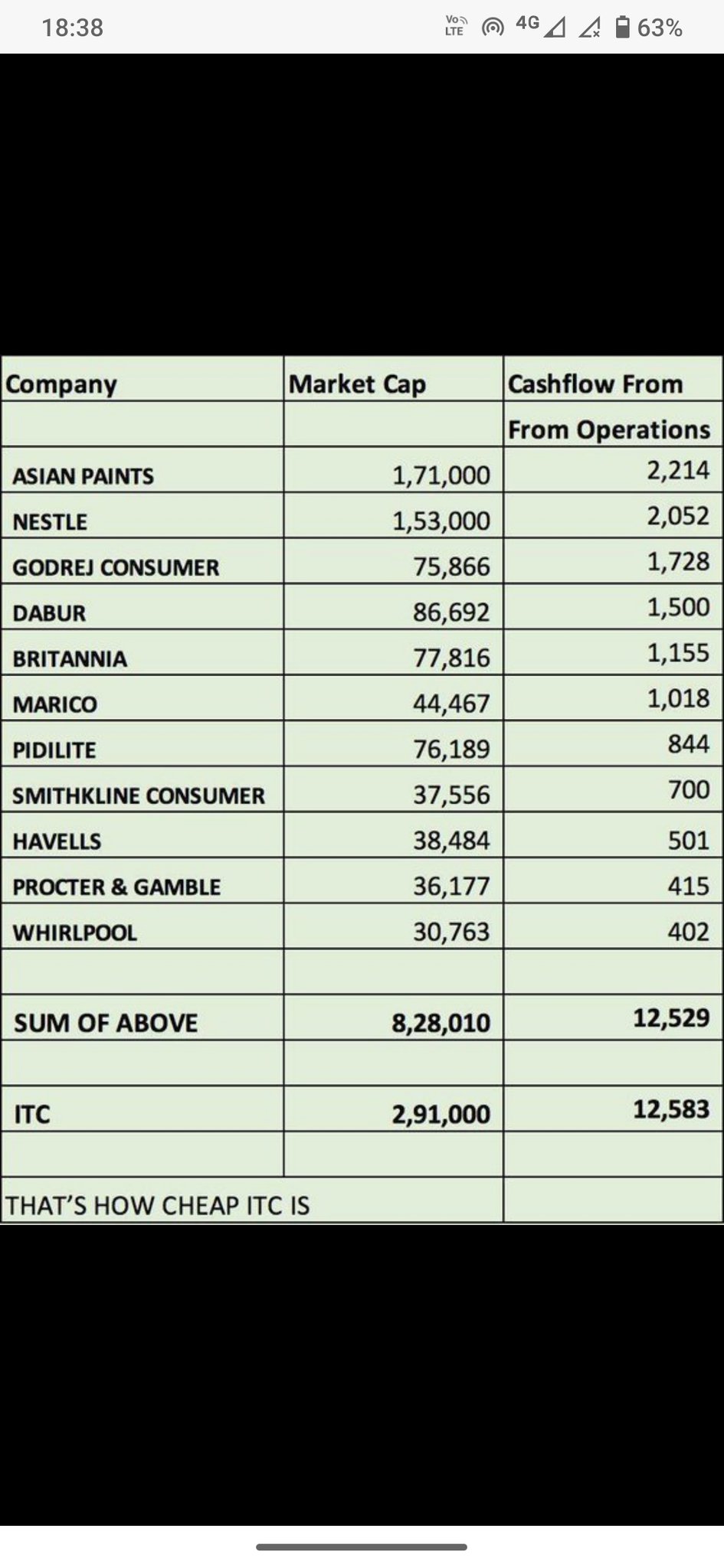

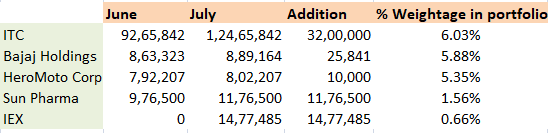

ITC avg 175(17.5 percent): I honestly do believe it will be the biggest FMCG company in India in a decade. Just need to keep a track on FMCG other margins and growth every quarter. Until it gets re rated I have a 5.8 percent dividend yield to enjoy so I have no issues with patience here

Financial services/Tech/consumption:

Sbi cards avg 530(17.5 percent): This is the perfect mix of Finance and Tech and consumption for me…tech because it’s playing on the long term story of Indians accepting online payments as the norm along with increase in consumer spending on Small ticket items(which protects me from Heavy loans and default for auto and homes from other Finance companies). Got it at a huge margin of safety so I’m comfortable even with a moratorium overhand ahead

Pharmaceuticals(API):

Laurus Labs avg 780(17.5 percent):

I have been buying pharma and chemical companies since June. Wanted to go all in on API since even when demand slows down API companies can increase the companies they supply too hence protecting them a little from demand slowdown. Laurus ticks all the right boxes for me. Also, as a bonus when the likes of Hitesh sir and Donald sir get interested in a company following it becomes a joy since you can see red flags and growth triggers miles in advance

Pharmaceuticals (Generics)

Alembic Pharma AVG 917 (11 percent)

Always considered this as a blue chip pharma company with good management. Had given up on buying it post the run up in price just before and after the Q1 result especially when a QIP was done at 932 rs with the likes of Tata, bajaj etc. Was a pleasant surprise seeing it at under the QIP price and bought straight away at a relatively low PE of under 20. I’m currently very heavy in pharma with almost 1/3rd of my portfolio in it but I honestly feel this is just the start of a multi year bull run.

Pharmaceuticals (Manufacturing):

Granules avg 240 (4 percent)

Slow and steady performer. Good margins of above 20 percent… vertical integration leading to a moat of low cost high volume production this is a pharma manufacturing company that will slowly but steadily become a large cap by virtue of expertly run management and via sustained growth using internal accruals. Good guidance by management every quarter. Seems like a safe bet. Only problem is everything post 2023 seems murky but I trust the management enough to give guidance for that too closer to the date

Chemicals:

Deepak Nitrite avg 520(17.5 percent):

Specialty chemical companies are over priced imo. Deepak Nitrite is a company that will have specialty chemicals contributing a lot more to its overall revenue soon and is not priced even close to a speciality chemcjals company. They have classy managemen, are investor friendly and have been growing consistently and have huge potential in phenolics and specialty chemicals which imo will lead to a re rating soon.

Agriculture:

Kaveri Seeds AVG 605(14 percent)

Always was a fantastic company but got beaten down by cotton prices, an audit scandal and a court room saga a few years ago. Went through a couple years of pain but the management managed to get the company back on track by reducing their dependence on cotton and spreading the dependence across all their field crops. Rice could be the main growth driver now. Has always been Q1 heavy due to the sowing periods of field crops but they’ve managed to create profit in all their remaining quarters too as of last year via vegetables. Management looks like they walk the talk (backed by Mohnesh Prabhai) and they’ve guided 10 to 15 percent revenue and 20 to 25 percent PAT for 7 years(2 already completed). Managed to do this even with cotton and maize prices beaten down in Q1 FY 21. They have a huge corpus of cash which they’ll be using partly for buybacks and dividends. Severely underpriced and very easy to track.

Auto:

Racl geartech avg price 96 (1 percent)

Not a fan of the auto industry or cyclicals. Also, I usually do not delve into companies under 1000 crores MCAP. However, there’s RACL just blew my mind. With its industry leading operating margins , amazing clientele both abroad and locally, good father and son management team with skin in the game, exposure to two wheelers and tractors ie less hit covid products and constantly improving financials I couldn’t ignore it at its price (revenues are twice the MCAP!). However I have a very limited exposure to this ie just 1 percent due to the headwinds for auto, my dislike for cyclicals in general and my lack of experience with sub 1000 cr MCAP companies.

Overall I think of these companies as my businesses more than my stocks. also, i’m currently tracking the following with small amounts and I don’t consider them part of my portfolio yet:

Idfc first bank, Cupid, Rain, VIP , Sirca Paints, Kpr Mills, India mart, Rites, Polycab, Tci express. Not fully convinced in any of these as of now. Will be waiting until next year post covid and until I gather the required funds and then one of these will be added to my core portfolio changing the overall allocation. I’m also interested in adding a IT/tech company soon and il probably wait for an IPO for the same since there’ll be an explosion of them soon and the ones currently in the market look overpriced.

So overall the allocation of my portfolio will normalise across sectors in a few years with the aim of getting an even spread across sectors in time.

Open to criticism and reviews in the comments… cheers

We need to keep a close eye on profit margins and the measures they bring to improve efficiency.

We need to keep a close eye on profit margins and the measures they bring to improve efficiency. So I fully concur with your view on having a super concentrated portfolio.

So I fully concur with your view on having a super concentrated portfolio.