Hello sir…it was really nice reading your whole journey in just one sitting. Its like a movie with different actors coming and going…would be great if you could share your CAGR returns of the portfolio from the time you sold your blue chip portfolio and started in aggressive stocks…Thanks in advance

After a long break on the sidelines i finally managed to invest again. Ive been keeping money aside in an emergency fund as mentioned before to cover for business expenses for 2 years. I had all that money saved in my idfc fixed deposit account. While the returns pretax were acceptable at 7+ percent the 30 percent tax hit would bring that down to a rate im not happy with. So i took all of that money and put it into embassy office… well half of it… was tricky buying a large number of units at sub 325 … will put the other half in over the next few days at hopefully under 320. I already have about 25 percent of my wifes PF in Embassy(in reality its now about 20 percent due to the sharp rises in ITC and RITES) at rs. 308 and now ive added my share too. Its basically now an alternative to owning a second flat for us without the tension of collecting rentals and doing the paperwork and maintenance and overpaying for property ourselves.

Ive been a fan of embassy offices for more than 2 years now and if anything the situation has gotten even better now(paid 308 when there was covid and work from home uncertainty and NAV at 386 and paid 325 now with most of that uncertainttly removed and NAV at 400). The rules of reits are simple… buy at 20 percent discount to nav and yields near 7 percent(with minimal tax hit) and attend concalls and read quarterly reports like a hawk. Promoter selling and unrelated to the reit unit issues + rising interest rates has led to the drawdown in price and the business overall is on a steady footing. All of the money is still very liquid too and i can always sell units closer to nav if needed. So while not a debt instrument by any means… i much prefer having my money tied up here over FDs. As a bonus il be using the quarterly payouts to cover rent of one of my offices while im comfortable with capital protection too at these levels.

@Mudit.Kushalvardhan Majority of my money is still in laurus from under rs. 200 and the rest was mostly in deepak nitrite from rs. 500 to 600 So one can extrapolate my gains from there(deepak money and savings now in embassy though). Taken a few hits with intellect and vaibhav but theyve evened out with idfc. My wifes pf is majority in itc(200), rites(235) and oracle(2900) and embassy(308). So again one can extrapolate from there. Cheers

@Jai_Sipani

I dont follow nazara tech unfortunately

8 Likes

@Malkd, Welcome back.

The income (dividend received) will be taxed at the peak rate anyway like FD right? How could this be a better investment than FD from taxation point of view?

Embassy REIT divided is around 80% tax free. Tax is paid on remaining 20% only.

2 Likes

How to check that NAV are trading at 20% discount? Can you guide us which document is to referred from embassy reit website? It will be very helpful and new learning for us.

There is an entire 5 mb document on the bse website that im not able to upload here for some reason. Youll find it on the embassy office thread too. Buying at 20 percent discount to NAV does the following

- Accounts for any errors in calculations/over calculations. For eg when embassy said their nav was 380 or so a few years ago a seperate study by an independant party showed it at just under 300. So you cant take it at face value.

- At price of NAV yield would be just 5.5 or so percent pre tax. A post tax FD would be a safer investment at that price.

Personally im expecting the payout to reach pre covid levels(24.70) by FY 25 and there should be a jump after as hotels and current investments start kicking in. My current FD at idfc is at 7.05 percent for two years with quarterly payouts… at rs. 325 embassy would be at around 7 percent pre tax assuming payout of around rs. 45 over the next 8 quarters. The good thing is the yield will increase in time + there is a chance of a return to nav allowing me to sell some units at a higher price + only about 15 percent of the yield is taxed at 30 percent. Its a no brainer for me especially since they are so meticulous wjth their presentations and open in their concalls. The other option was storing in the cash in physical real estate(flat and getting a tenant etc or buying one of the offices i currently rent for my business). Both would offer a yield of around 4 to 5 percent with the additional problems of owning a residential/commercial property in the real world and are illiquid. The reit option beat this too. Im not comparing it to direct equity since the gains here would be capped vs direct equity … but there are some benefits to an reit over an fd/direct real estate and a possibility of a double digit overall return when bought at a discount.

2 Likes

will you please at least spend 5 min on REITs . Invits Taxation, before posting such basic queries?

@KS16

Everybody is learning. Youd be surprised by the number of people who dont know about reits/invits etc. Everybody around me is overpaying for real estate and they just scoff at me and my wife when we tell them we own an reit instead. I just tell people i own an office in embassy office park now that is professionally managed and given out on rent to an mnc and i get a tax break for the rent i get since that is basically what it is haha. So i dont blame anyone for not knowing how they work.

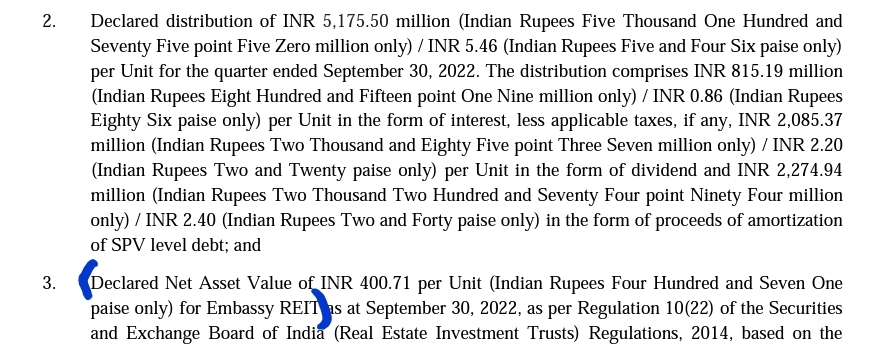

@Sudhakar_Subramanian check the embassy office thread for more details regarding the tax calculation etc. Its a fantastic thread with a lot of information and great posters. In short though … interest component is taxable, dividend and amortization is not. The distribution for this quarter was rs. 5.46 out of which 0.86 is interest… that means 4.6 rs is tax free(around 85 percent!) and youd pay tax of lets say 30 percent only on the 0.86 part.

6 Likes

Main reasons for recent fall are the high debt levels and Rs 82 cr default of construction Finance Loan.

Financial position of Embassy Group will be an overhang on the REIT and I expect near 300 levels in coming month.

Disclosure: Earlier investments already sold 6 months before and now only tracking Embassy/Brookfield/Mindspace Reit for a re-entry.

@amitvohra

This was known about 10 days back thanks to the fantastic work by dd1474 in the embassy thread. We wont know if the fall upto now has already accounted for this or if it will get worse. Ive had 320 to 325 as my comfort range for ages so decided to take half the plunge. In the past ive been waiting for certain prices like rs 75 for manappuram and ignored even rs. 80 and now i live in regret. Decided its better i just start adding on the way down from 325 instead of waiting for a rs. 300 which may never happen. Id say the previous 308/310 may get tested and il gladly add my second half then. 300 and below would lead me to liquidate some of my PF to add even more since that would mean a 7 percent post tax return and a 25 percent discount to nav which would be amazing!

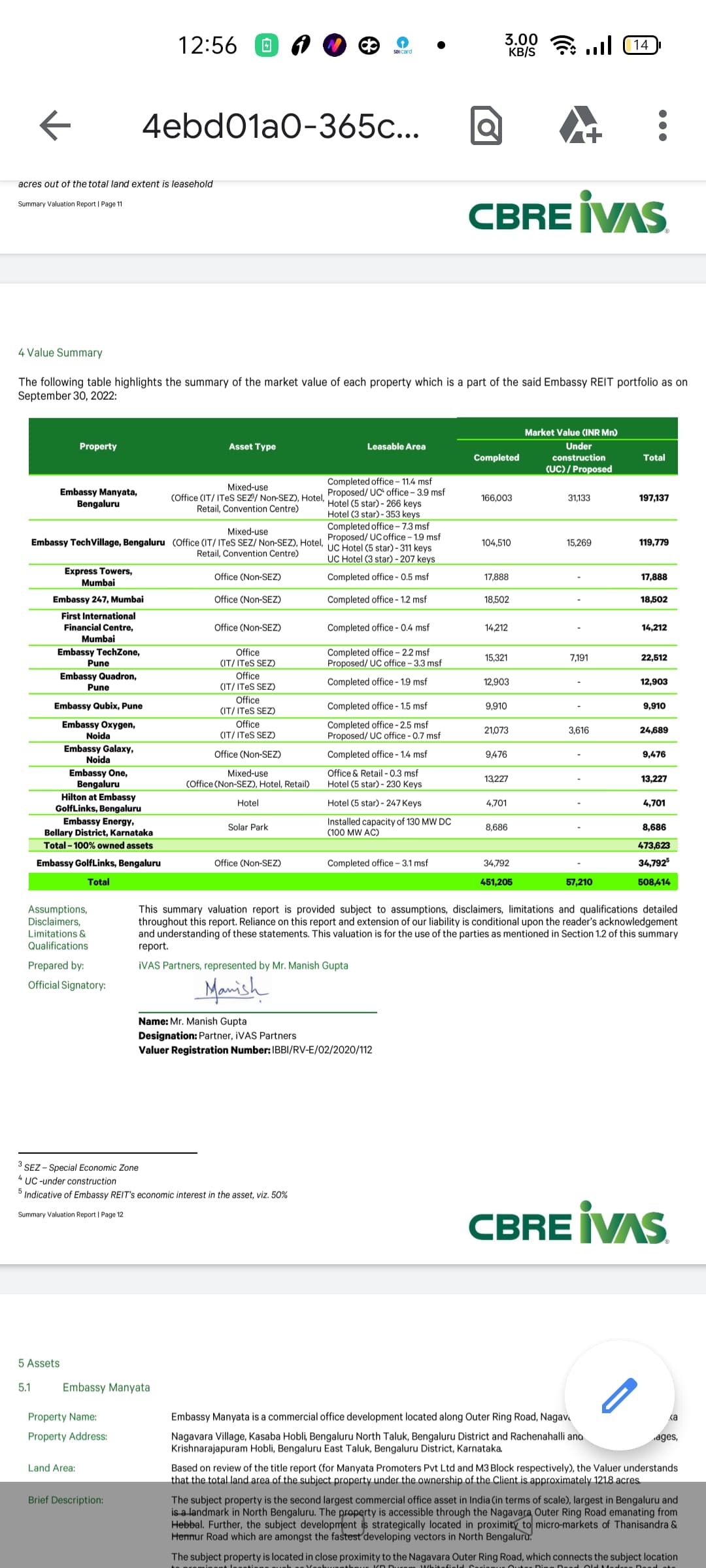

Submission Of Valuation Report Of Embassy Office Parks REIT For The Half Year Ended September 30, 2022 Under Regulation 21 Of The Securities And Exchange Board Of India (Real Estate Investment Trusts) Regulations, 2014.

Page 12 of valuation report tells us that total assets of REIT is INR Mn 508414. Is this are you talking about sir.

@thakurvi

They disclose the nav directly alongside the valuation report (which you are looking at). Attaching screenshot below

So assuming an error/ over valuation of 20 percent then 320+/- 5 and below is where the time to pounce begins. These reits rarely stay in this range for long ie near 20 percent unless something drastic happens ie covid/ a combination of high interest rates+ promoter selling + promoter issues (all of which is happening right now providing this opportunity)

4 Likes

Thanks @Malkd. You’re kinder and forgiving than many others in VP. I’ll go through the embassy thread. I was looking for a post tax investment opportunity that can beat FD and savings account. I’m fairly invested in equity so don’t want to get into it more than that. Liquid and ultra short term funds are no good either. REIT sounds like the one I was looking for.

3 Likes

Hi @Sudhakar_Subramanian ; you can also check IRB invit which is in toll collection business & it’s also trading below NAV of 100. At the current price of 63 & management guidance of 8.5 RS payout per year, the yield will be around 13.5 %. In that also some of the payout is tax free. In addition management will add additional assets going forward & current debt ratio is also still at comfortable level. You can look at that thread for more details.

5 Likes

I went through the embassy thread and not able to dissect the tax related info for the investor straight away. So did a Google search and found a live mint article. But it says interest, dividend ( SPVs have paid concessional rates of tax on their profits) and rental income are all taxed in the hands of the investor. But @Malkd , @naveen062000 and @KS16 said it is not. I’m a little confused.

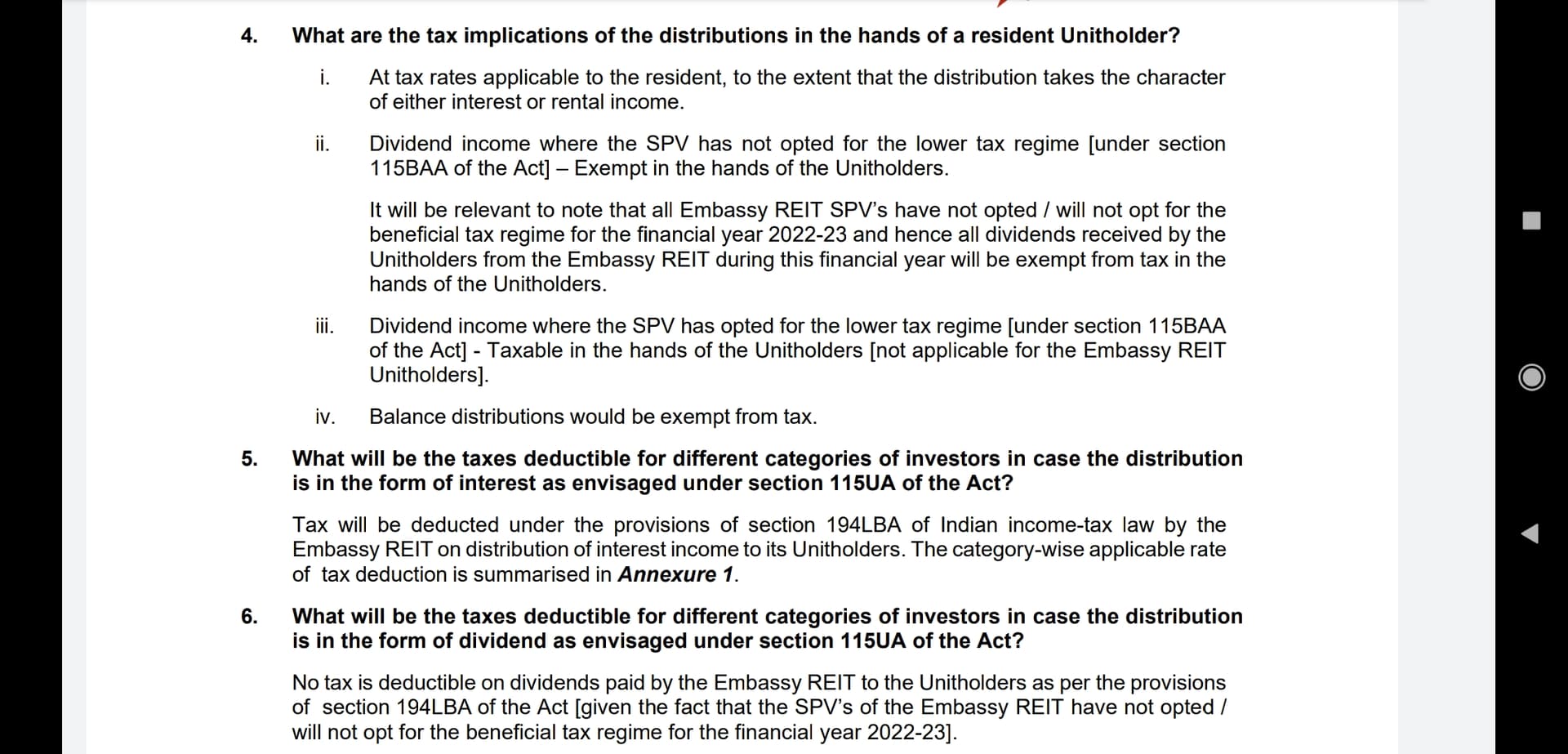

- If one examines the various streams of income, interest paid by the SPVs is an allowable tax deduction for the SPV, not taxable in the hands of the Reit/InvIT but taxable in the hands of the investor.

- The dividend paid by the SPVs out of tax paid profits are not taxed in the hands of the Reit/InvIT, but are taxed in the hands of the investor only if the SPV has opted to pay the concessional rate of tax on its profits.

- Rental income of the Reit is exempt in its hands, but taxable in the hands of the investors.

- Effectively, there is only a single level of taxation for most streams of income, except cases where the SPVs have paid concessional rates of tax on their profits, in which case the dividend is taxed again in the hands of investors, though the SPV has paid tax on its profits.

Source:

And with respect to capital gains, the articles are even more confusing.

- LTCG if held for 1 year and LTCG tax is 20% (not 10% and no mention about indexation) according to an ET article.

- But another mint article says 3 years for LTCG. But there too confusion saying a) 10% (no indexation) and b) 20% (with indexation).

Source:

1 Like

From the above link, the document for “Income-tax treatment for distributions…”

-

Interest and rental income are taxable in the hands of investors. Dividend and balance distributions are exempted for investors.

-

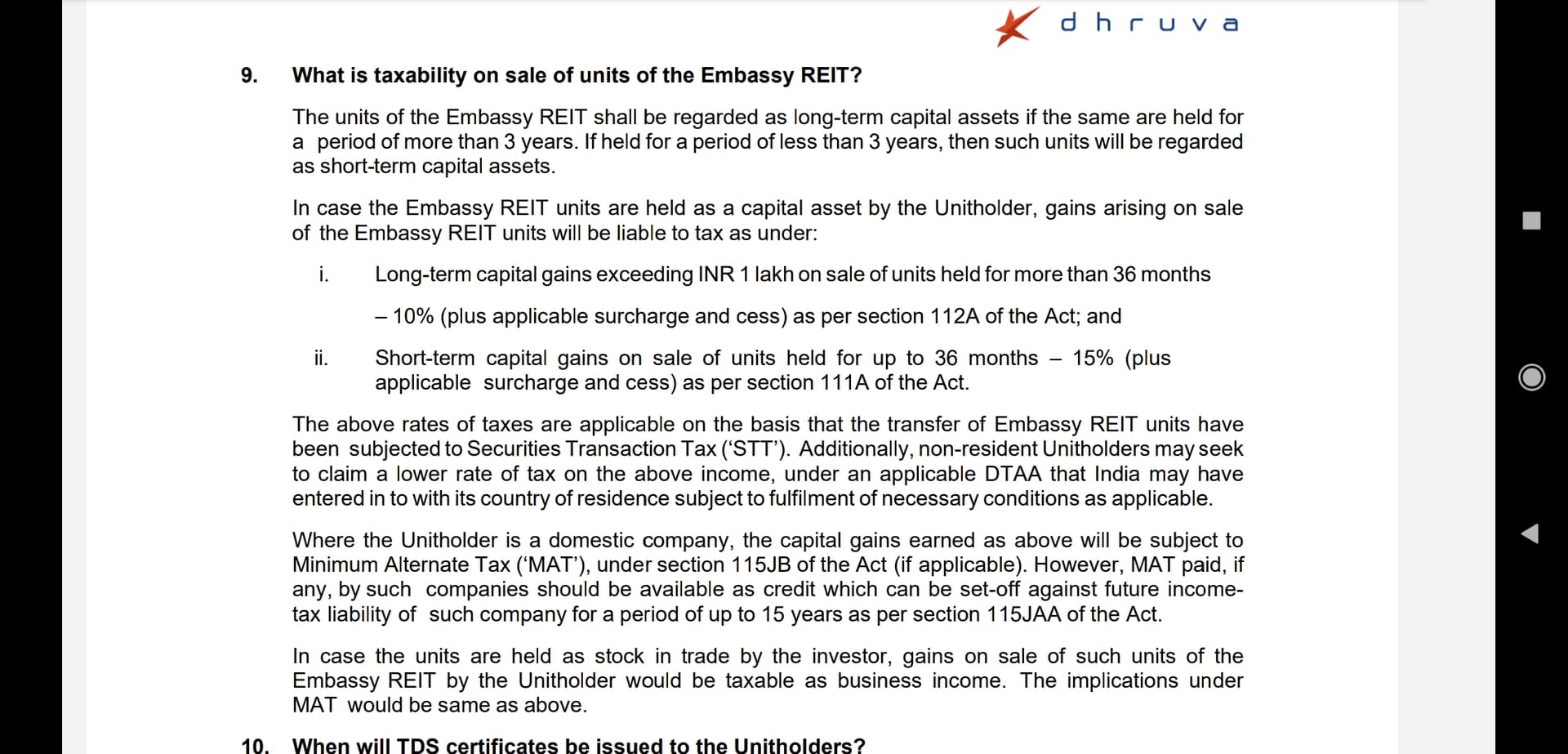

LTCG is 3 years, tax is 10% no indexation.

1 Like

@Sudhakar_Subramanian

In short:

There is a new reduced tax regime(under section 115BAA) and if SPVs opt for it the dividend income would infact be taxed. But embassy office(and mindspace) have not opted for it and stayed under the old regime. So basically, The Dividend income where the SPV has not opted for the lower tax regime [under section 115BAA of the Act] is Exempt in the hands of the Unitholders.

Also no tax on amortization. So only interest portion is taxed. Regards rental income, embassy gets charged tax on it and it then goes through an spv and comes to us as dividend(under the old scheme… hence not taxed).

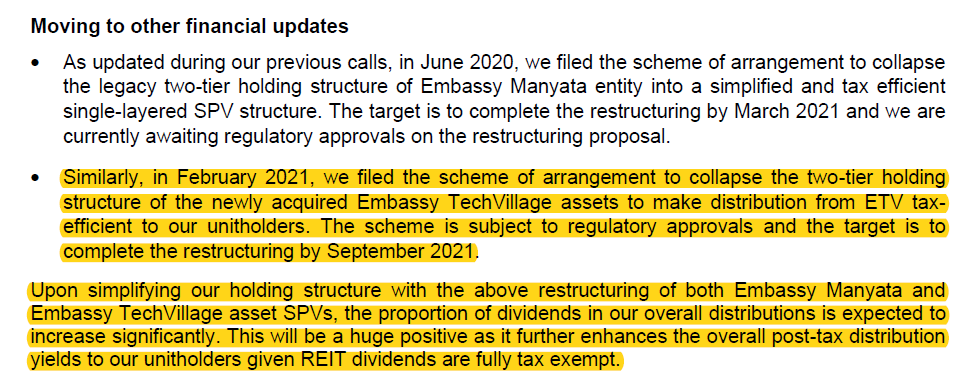

Last year embassy simplified their structure further too to increase this non taxed dividend income. Youll find this in the q3 concall from last year. Attaching a pic from it which is already present in the embassy thread:

There’s a faq released by embassy which i think youve found that explains the way tax is handled that should clear your doubts. The non taxed amount being almost 85 percent was a huge surprise since post simplification 70 to 75 is what was expected. Regards ltcg… yes… its a 3 year hold. But ive found selling a few units near nav/above nav to be worthwhile

3 Likes

Hi Malcolm,

One more question regarding taxation. How does the total distribution amount appear in AIS portal? Does the entire amount (dividend + interest + amortization) appear as dividend?

Thank you,

Anirban

2 Likes

Il know this next quarter when it starts coming to my account since my wifes CA handles her account. But for now i believe the interest amount comes with tds pre removed. And i send him the calculation seperately ie interest x 0.30 and tell him to ignore the dividend income altogether.

2 Likes

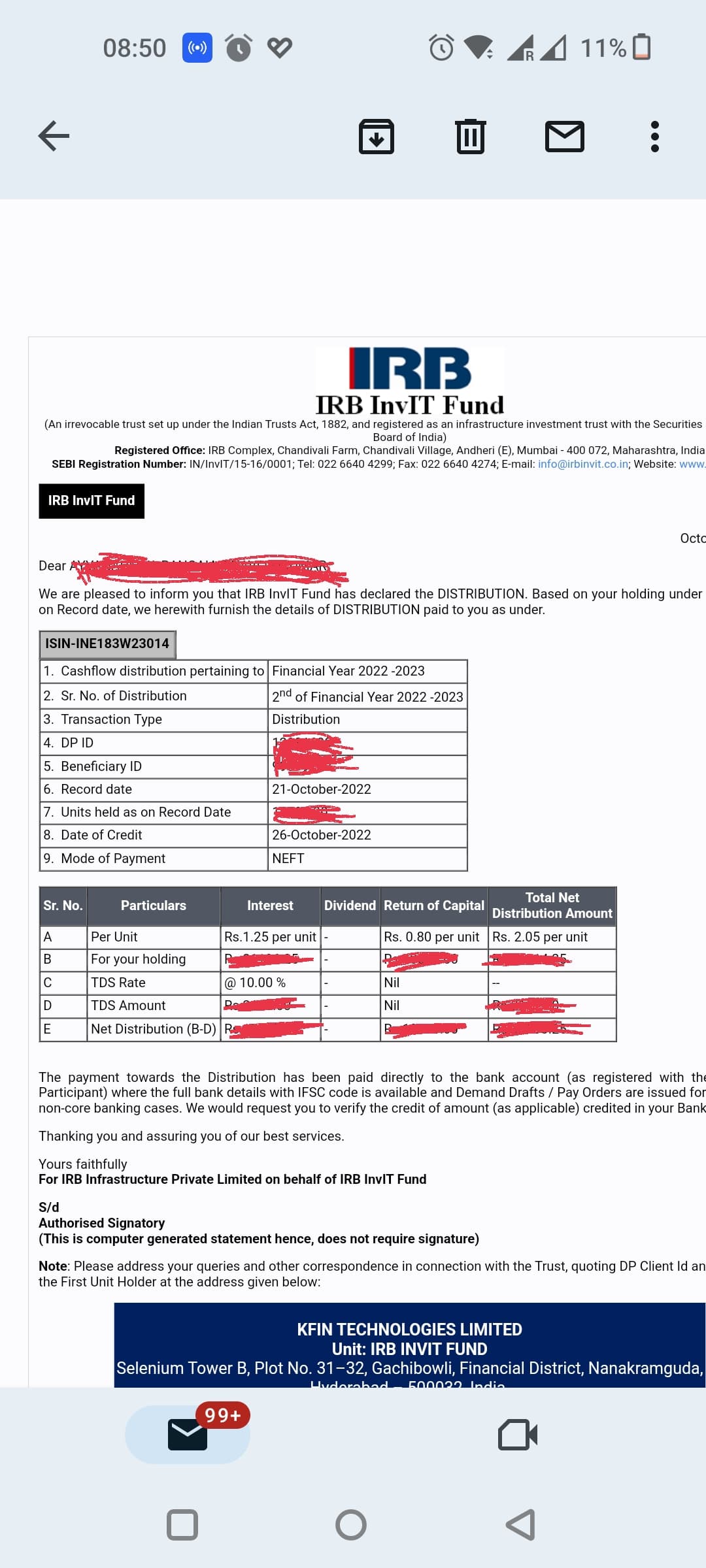

Hi @anirband87 : This is the last distribution statement received from IRB invit. They paid 2.05 in last quarter. In that 0.80 RS is tax free as it is capital returned which you can clearly in the table at the end. I hope this helps.

3 Likes