Thanks @Lucifer … I’m not going anywhere so I will reply/post here but on a weekly or monthly basis at most and not as often as I have of late. I realised I need to stay away from everything stock market related because even with my own balance sheet in distress I was still trying to work up cash for deepak fertilizers and rpsg a few days ago even though I knew a market downturn combined with a covid 3rd wave would wipe me off totally. And then seeing them rise 30 to 40 percent since those exact days made me feel regret for something I couldn’t really have afforded in the first place… I also took cash I could’ve easily put in a safe spot like mindspace at 275 and threw it at tips industries instead lol. So I’m in a way grounding myself to protect myself because the temptation is just way too large in this bull market. Hopefully I reach my March 31st 2023 target early so I can get back on track with equity investing sooner than I’ve forecasted. I will continue to update this thread along the way as my PF company goals and antifragile goals get hit. Cheers

Good Luck with your plans. And many thanks for this thread overall. Being a newcomer to this entire thing, this thread has been invaluable in realizing how to approach investing in the stock markets in totality.

Very instructive to read your portfolio thread. I noted your investment in ugro which has done well in a short time, kudos on that. Would be nice if you can share your thoughts on home first finance which has similar market cap.

Hey @abhijeetc … Sorry for the late reply. I’m only on the forums/looking at the market today since a company I’m tracking ie Rpsg ventures results just came out and a company I own ie Rites is coming out later today so I just happened to see your question. Regards ugro… Its too early for any sort of celebration. The thesis is that it’s bought under book value, 0.58x leverage and under what the main promoters paid while setting it up giving a rare opportunity to perform in a reverse ipo where I have an advantage over the original PE investors. Il only know if its a company worth investing in 5 years from now when they get all their ducks into play so it’s a huge risk but with a margin for safety.

Regards home first finance… I don’t know much or anything about it. All I know is it was an Ipo this year and I’m a huge non believer in ipo valuations. It’s still trading at 5x book while I only look at finance companies under 2x or preferable 1x book value so I can’t comment. I’d be very wary of overpaying in this current market and even if its a future hdfc paying 5x book to start with and not exit a company looks a bit scary. Il be posting further thoughts regards valuations in general later today when Rites gets its result out

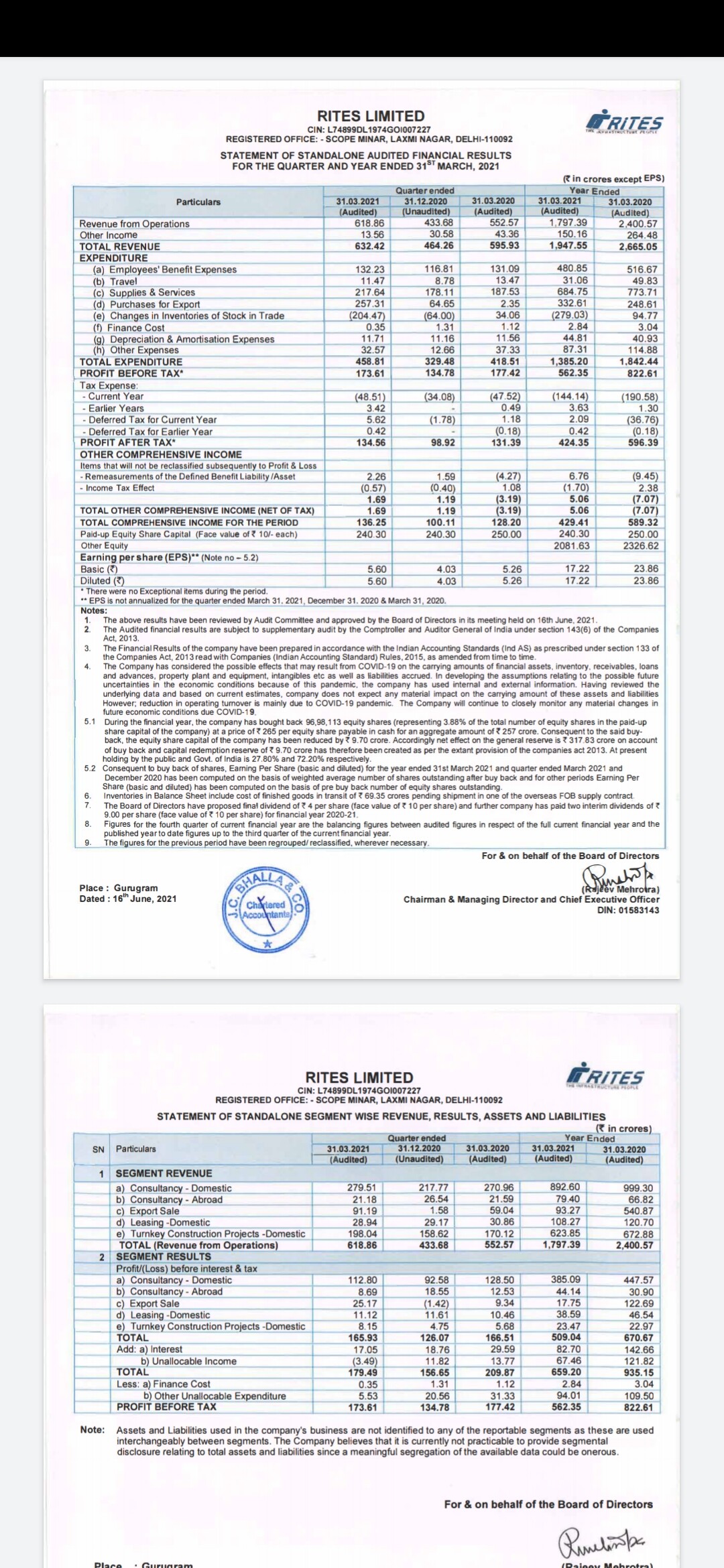

Will elaborate on the comfort of valuations with Rites just announced result as a basis and referring the future of investors by Jeremy siegel(which is imo the best book on understanding valuations) . Back in April Rites reached a low of Rs 235. At that price removing the cash on books(not cash equivalents) and considering management clearly stated in Concall that Fy22 would be back to pre covid levels and the order book could be perused to confirm this Rites was trading at mid single digit forward multiples. Now here is the beauty of buying at that price… All negatives were priced in and you were actually buying the business and not market sentiment at that price. As the business grows the earnings would fully be captured in the investment and as market sentiments turned bullish there was a chance of a re rating too. As a bonus a dividend yield of approx 6.5 percent pre tax was thrown in to make this an even safer investment. This let me put a huge amount of cash knowing my investment was safe(the technically strong base here at thus level helped too). The negatives of it being government owned along with supply chain disruptions were all priced in. Today Rites announced their result…

They are already nearly back at pre covid levels and there is no reason to believe the next year won’t be equal or better than 2020. I’ve now got a margin of safety and a buffer of 20 percent from buying price(the price may consolidate/fall a bit for a few months since its overbought now) and a locked in dividend yield of atleast 6 percent pre tax. Come hell or high water regards the market crashing or not there is no way il need to sell here so I am confident that apart from corporate governance issues my money will compound nicely since I am not at the mercy of market sentiments rather just business performance now. If the market sentiments give it too huge a PE re rating it gives a chance of a little profit booking too. And this is the beauty of buying at low valuations.

On a side note and in continuation of my restructuring process that I started above:

I don’t like predicting the market but I know that some valuations to even the top nifty 50 companies just doesn’t make sense anymore and needs a lot of suspension of disbelief and 10 year runways of 30 percent growth etc to swallow and I’ve heard of all this before ie at peaks of previous bull markets… and that just signals even more that the current market isn’t for me. The risk reward isn’t favorable for me in most companies for additional capital but I’m glad to hold my core PF to see where this goes and book profits if the market goes crazy ie my PF doubles or triples from here.

My restructuring process is now complete(borosil renewables and Idfc are sold… 1/3rd of Vaibhav Global is sold due to high valuations along with the other companies mentioned above) and I have enough cash to survive my business expenses assuming no income uptil end of this year now. Laurus, Deepak and ingrevia which take up nearly 90 percent of my PF now were bought at low double digit valuations(concentration is the only risk I love… Not paying high multiples) and with expectations of 20 to 30 percent growth so even now they are fairly valued but I’ve mentally prepared myself to lose about 30 to 50 percent of my PF if the market turns sour and valuations revert to bear case earnings growth. And I have enough head room to add to Intellect and Vaibhav if they crash due to a de rating and if ugro shows clean growth with low npas in the future to increase these positions.

However, while I sound bearish… I’m not lol. I can now sit back and enjoy a bull run that could potentially double or triple my networth without any worry of being forced to exit too early now ![]() . Cheers. Again, sorry in advance for late replies since I may not be here for another week or so.

. Cheers. Again, sorry in advance for late replies since I may not be here for another week or so.

Since I’m on the forums due to ugro capital I thought I might as well post an update here. The only addition to my portfolio was a small under 2 percent bet on rpsg ventures when it crashed to Rs 480 post its result since I couldn’t resist the chance and had been saving cash at a faster rate than I’d imagined. I’ve added it to the ugro capital bucket ie a long term project that il be adding to every few quarters or years based on how the business grows for my own education(understanding the ups and downs of creating an nbfc and Fmcg company from the ground up with skin in the game which is in itself worth the price of admission) with a huge upside and low capital at play.

Been saving all excess cash in an Fd as planned which will be transferred to ITC at the opportune moment(Currently hoping for 50 dma levels to close below 200 dma ie a death cross. Will gladly add on the way down below Rs. 190 if that does happen. If it doesn’t then il add near 200 dma over the next few quarters).

The way things are going I should be able to finish stage 1 which is money in FD/ITC equal to business expenses by this time next year instead of 2023 as my planned safety buffer since my cost cutting measures looks like they will be a bit more long term than I’d imagined at first and My state seems to be doing a good job vaccination wise.

Currently my entire portfolio seems to be running on Laurus labs. Recently, I felt a bit horrible that I’d booked my profits in just dial, tips, Racl, expleo, Idfc, kaveri, kpit, pix transmissions etc and when I had gotten them so cheap but I then remind myself that all of that money is in Laurus and in an emergency fund which is a lot easier to track then 10+ companies. At the end of the day it doesn’t matter how the capital appreciation comes… Its that it comes… And I’m reasonably confident Laurus will continue to do me proud for the next few years at the least.

The Last 6 months alone my own portfolio has gone up 81.61 % vs the composite index at 21.43% and sensex at 9.91 percent(as per markets mojo) so I can’t complain. In that period my wife’s capital protection PF too has gone up 23% including dividends… so again… My responsibility is to ensure no disturbance to these PFs over the foreseeable and reinforces the fact I need to set myself up properly with emergency funds before adding more to it so that the temptation to liquidate never arises. Cheers.

Small update on my current path to building a safety buffer of business expenses = debt like instruments to protect my core PF.

Added my first of 5 planned equal tranches in ITC today. As mentioned I’d been saving money in an FD waiting for the right time to do it and today seemed like as good a time as any since at 201.9 and an expected 11 Rs dividend for FY22 it just about beats the FD for returns. Technically ITC is oversold and near 200 dma and the delivery percent today is a whopping 70+ percent which is no mean feat for a stock with such huge float. This level of 200 to 202 has held up quite well before and with the agm meeting a month away and with the q4 results not being half bad which dint justify such a fall in the first place(and with the news of Dr harsh vardhan retiring) there are some short term triggers here which makes me feel we ll see 210 before we see 190. That being said Il be collecting money in my FD over the next quarter for the next tranche too and will gladly add then if ITC breaks this support and creates a support at a lower level(near 170 hopefully).

Idfc first at current levels was another low risk temptation for me for this safety buffer purpose but even though I don’t see too much downside from here there is a possibility of vodafone and the third wave leaving some prospect of further downside here which il evaluate next quarter. Also, while everyone expects Idfc to go 40 percent above Idfc first I don’t really understand the situation too well to bet on either since I don’t want to play an arbitrage game here and I can’t discount the possibility of a reverse arbitrage too ie Idfc first falling while Idfc stays the same… Once there’s more clarity on voda, arbitrage and 3rd wave il consider a position here since I need to be very careful about downside protection with this business expense buffer asset.

Note that I’ve sold my position in ugro to help build my ITC asset alongside my business profits. I’ve been gradually decreasing my exposure to ugro after the run up to 160 and exited totally a few days ago since I need to see some clarity regards Q1 and npas along with the 3rd wave fallout. I will be investing back in here once my business is more settled though since I love the management and company… But I cannot justify parking capital here when my business may need it so I’ve moved it to ITC ie the safety buffer instead.

Anyway that’s my small update. I won’t be actively investing in anything for atleast a quarter since I need to make cash to invest which will take some time AND I can’t liquidate anything from my core holdings AND any money I make just goes into ITC lol… so I’m just staying away from looking at the market or anything related to the market overall apart from my short trips here … Cheers

Hello @malkd. I have been enjoying reading your posts. This in turn gave me a good idea of your picks useful to make my investments. I know you have made some changes along the way. Would it be possible to give snapshot of how your PF looks currently?

Hey @sbuy210. Post churn of the smaller positions and booking of profits I have a very concentrated portfolio with names that have been left basically untouched since i invested in them:

My Core portfolio as a snapshot of today’s value is:

Laurus labs - 58.2 percent

Deepak Nitrite - 23.1 percent

Jubilant ingrevia - 8.2 percent

Intellect Design arena - 5 percent

Vaibhav Global - 3.6 percent

Rpsg ventures - 2 percent

Faux debt portfolio:

ITC - Currently equals 4 percent of my total Core PF value. Will be upping this to approx what will be 20 percent vs my core PF as per current core PF value over the next year or two(hopefully… Dependant on cash flows since its a huge amount). I don’t consider this part of my PF so ive classified it seperately so I don’t get frustrated with ITC. This is supposed to be as boring and slow as an Fd for a few years so I don’t want to look at it post buying.

Wife’s dividend and capital protection portfolio Has remained untouched with a split between the following in order of decreasing weightage(Total is approx 50 percent of my PF value):

ITC, Embassy Office, Oracle financial services, Rites, Indigrid, Mindspace(plan to build this position here in Mindspace at current discount to NAV over the next few months)

There will be no churn to any of the names mentioned above unless valuations double from here in a crazy short time frame (Vaibhav Global is the only one I feel is currently stretched valuation wise but for good reason) or if corporate governance issues come up.

I Will also be increasing the number of companies in my core PF to atleast 10 over the next few years(financials like idfc/ugro will be priority 1 post ITC) and increasing allocation in the lesser contributing companies too. So while it looks concentrated now with 90 percent in 3 companies it will slowly look “safer” a few years from now

just a thought, as you manage your wife’s portfolio as well and in essence overall outcome depend on that part also, so it maybe a good idea if you maintain an overall total portfolio values from perspective of current allocation of each share as per total family portfolio…returns are the last part…they would come…allocation is something important to understand the overall opportunity & risk as well that we are into…you may ignore if it doesnt work for you but it will be an interesting exercise to know the overall picture from allocation perspective and not in parts!

btw, I remember you had asked me about my portfolio, I started a thread recently and my portfolio is in there after some learning related posts…would be good to know your thoughts as well…Cheers!

@Malkd Did not see JustDial on your PF. Is the position too small?

@manoopatil

Unfortunately I had to do a culling of my smaller bets a few weeks ago due to reasons outside the market ie with a covid 3rd wave possibility and no cash flow from my main education business and a later than expected restart. I didn’t want to risk being forced to sell anything from laurus/deepak etc so I booked profits not only in just dial but also racl/Tips/ugro etc even though I really didn’t want to. Nothing wrong with just dial or any of the ones I sold. When I have stable cash flows again next year il be able to hold on to these kind of bets with no issue since I have no issues with patience… so this past 1.3 years have been a lot more churning than I’d like. That’s led to my decision to create an emergency fund so that I can let my capital run undisturbed in the future. The thought of ruining the compounding in laurus and deepak particularly due to outside factors is something I never want to face again. Those 2 are my main priority at 80 percent of my PF. Next to my own business those 2 are mine now and I’ve never been more bullish about anything else in my life long term as I am about those two lol.

@Investor_No_1

Maybe in 3 to 4 years when we consider kids and a house loan il consider combining the two portfolios. For now we both run seperate businesses and those are our main expenses so I keep them seperate. Hence why even though there’s itc in her portfolio I have to build a seperate position in it to cover my business expenses long term lol

Malkd,

Do you see margin of comfort in Deepak Nitrite at current valuation?

@Shankar … I honestly don’t know. I bought everything I could at an average of Rs. 600 and haven’t added since and I doubt il be adding any more since I have other priorities for the next few years ie building ITC, then financials, then increasing my stake in the lesser contributing companies… So if I ever add more into deepak it will be a solid 3 to 4 years from now. Right now at current valuations a lot is priced in… The move from basic chemicals to specialty chemicals looks captured in valuations. So does the fact that Phenol and dasda explode to great effect every few quarters. At current price point the downsides of the cycle of Phenol and dasda seem overlooked and there’s a very rosy picture of specialty chemicals which could end up being a slow process. That being said i am very bullish not just for the next few years… But for a period I can’t even fathom… And that’s because of the management. The way they can mix and match their offerings and jump into related ventures with such ease and success and handle what should be a cyclical business so smoothly is unbelievable. It’s the same reason I love Laurus. You just know that they’ll find new ways to grow (almost like a spawner business as defined by pabrai lately) and this makes the runway ahead a really long one. So regards your question, is there a margin of safety? On the face of it, I wouldn’t think so. However, the fact I have 20+ percent of my networth in it and I haven’t had an issue with sleep due to it for even a second speaks volumes since having capital at play and deploying fresh capital both require a margin of safety and I feel there is a loooong way to go here. That being said there could be a correction if the overall market falls and if Phenol prices fall and if specialty Chem slows down… On the other hand They may just continue posting bumper results for the next few years and reach a different orbit too. But timing the market isn’t something I know how to do so if and when that happens I don’t know. At the least, I can’t see money being lost here over a long time frame ie 5+ years though who knows what will happen in the short to medium term. Personally, both deepak and Laurus management and capital allocation remind me of the best blue chips in the nifty 50. Infact that’s my slightly unrealistic target… Hold on until both of them enter the 100000 mcap list and if they do maybe only then book some profits

Thank you for the update @Malkd.

Thanks a lot for your response.

There were a couple of stocks ( Deepak & Laurus) where I did the analysis and before I could load up, the stock raced away.

I load up on a monthly basis. Laurus was one that I loaded up for a few months and then post last quarter results it has raced away reducing comfort significantly.

Cheers @Shankar … I’d say deepak would be overvalued when 2 things happen. Currently performance products have been underperforming and so has basic Chem. As per the comments in the annual report and overall commentary both of those are slowly but surely coming back up and its just a matter of time when they start firing. Phenol may stay elevated for a bit and specialty Chem should continue growing. IF all segments fire in the same year we could see an eps of between 70 to 80. If the market goes crazy and also values the company alongside its pureplay specialty Chem peers at 70+ PE from that elevated level that is when I’d say it would be overpriced since at some point either dasda/opa and Phenol will underperform crashing the eps. That being said I think the eps they have set for FY 21 as a base looks sustainable and the market hasn’t valued it at crazy valuations yet ie still in the 30s… So while not a margin of safety it looks like it isn’t frothy either.

Anyway, I was lucky I had a lumpsum to invest when i did. Made me realise the importance of keeping cash in hand for opportunities like that. From now on in the future instead of siping every month, which would have been my plan when cash flow becomes predictable, il be storing cash and waiting for similar opportunities so that I can buy in bulk in one go similar to Laurus and deepak… Or alternatively spending the majority of a year building a position in one or two companies whenever the chance comes my way instead of getting distracted with small 1 to 2 percent bets every few months. Currently doing that with ITC and its almost acting as practice so I can replicate the same later with other companies.

Hi malkd,

So, i ask you this question since you are bullish and buying Both : ITC as well as REIT.

i consider myself in the same boat and a bit confused on this issue…

So, with the REIT currently at quite a discount to NAV and a dividend yield or about 6.8 to 7%, i am quite interested to shift my funds from ITC to REIT. ITC’s dividend yield is anyways lower to the REITs and i believe the probablity of REITs doing better and hence getting capital appreciation is more than ITC going up.

Honestly, I am quite put off by th recent ITC’s decision to sue some analyst…

Hope to know your thoughts on the same…

Hey @Harsh04 The only things common between ITC and an Reit is they require loooong term horizons for anything meaningful to happen and that at current prices they offer decent capital protection and yield and a good chance to accumulate for the future.

That being said… The pick of the Reits for me is Embassy office. However, I personally would never buy an office based Reit at less than a 20 to 25 percent discount to NAV since at current prices you are risking lower rentals with WFH +Hybrid models etc. At a price point of near Rs. 300 I’d consider moving most of my money into Embassy too. At anything above 310 I wouldn’t want to risk my money there. This is infact what I did. I haven’t added a single rupee since. Mindspace at 280 could be a good bet though since they are 92 percent tax free yield and a big discount to NAV and with some movement towards data centers. I personally prefer the embassy management so I’ve only dipped my toes in mindspace though. You can expect stable yields and maybe a doubling of capital over 15 years(maybe 10 if bought at a discount)

When it comes to ITC it’s a totally different ballgame. In a vs Reit fight ITC would lose in the medium term due to the tax on dividends. However, The capital appreciation over 15 years could be a LOT LOT higher. Think about it this way… ITC is a juggernaut. Its much bigger than a sanjay puri or a few hotels and the company itself will far outlive all of the current management. There have been some questionable actions and decisions over the last few years but we are looking at but a snapshot during the middle of a 200+ year story. All it takes is a few decisions, a little luck, a few changes in legal and management etc and we could be looking at a 80 odd PE multiple company in 2 decades with a stable engine of Fmcg others, agriculture, packaging and whatever form cigarettes ie bad habits take then. This isn’t a lehmann brothers ie a leveraged business, nor is it a Xerox and blackberry who can be wiped out with new tech, nor can i see the money disappearing off the books on the quiet. People talk about the ITC guys being highly paid and crorepatis etc but that’s just how it is in this industry. For eg I help college students get placed and nobody would choose an ITC over HUL with the stigma of a dying business in cigarettes plus the not yet settled Fmcg other department… So if they have to use higher salaries to catch the eye of new recruits and keep who they have happy I have no issues. I’d rather the money be spent over the table than under anyway. These “crorepatis” they hire are from cream of the crop colleges and companies and are more qualified than most of us to fix itc and all it takes is a few of them to steer the ship in the right direction(they really need to fix their supply chain for eg. That can happen without us even noticing on the quiet in just a few decisions from these guys).

Tbh apart from the hotels decision (which barely moves the ticker and they plan to move to an asset light model) I think the managements only problem is their timelines don’t match the majority of investors’ timelines. They are building something big… A company that uses synergies between all its divisions(IT, Agri, Packaging, Fmcg and even hotels for experimentation) and backward integration which can potentially dominate the Fmcg industry in a decade or two. This is one company I know il be leaving for my next of kin. If their stock price wasn’t stagnant nobody would be complaining… I don’t want to comment regards the writer of the article who is being sued… But he just seemed impatient and speculative to me. Instead an investor should consider buying When a great company makes missteps like this and use the period of pain to load up since at some point there’s always a reversion to mean with companies like this.

So in short: Reits at 20 to 25 percent discount to NAV for the thrill of owning an office space in a metro and tax free dividends… ITC for the potential of generational wealth and a steady dividend until that time(though always buy at 200 dma supports to avoid frustration). Imo both have a place in one’s portfolio for capital protection and yield along with upside possibilities in the long term. There’s a reason I consider them FDs for now though and separate them from my core equity portfolio.

Note: This is just my point of view. I’m used to being contrarian so changing my mind based on the opinion of the crowd is very difficult. As far as the facts are concerned all I see is opportunity in a temporary period of turmoil

ITC has turned bullish or mild bullish. Any up move from here is extremely rewarding from capital gain perspective. FD like dividends provide stability. ITC being a mega cap helps in large allocation which mid cap growth stocks wont provide. @Malkd - your story telling approach is worth reading.