Very good research on the company. This is very encouraging to hear. This tells us why just looking at consistent growth in sales, healthy RoCE in the past might not be enough as the financial ratios do not tell us much about the company turnaround story/future growth prospects.

Added this to my portfolio

1 Like

Cheers. I love turnaround stories(ITC, Kaveri) and companies with growth drivers not yet priced in by the market(Deepak with spec chem, sbi cards with online sales priced at 500) and momentum stories (laurus and granules post results) . Very rare to find these especially in sectors with tailwinds/no headwinds. So when I do I invest a huge amount of my capital straight away. If anyone can direct me to more(already waiting on idfc first bank as my next big buy post moratorium and headwinds) please do let me know. Today is the perfect buying opportunity for kaveri. That being said I am not a sebi advisor so please do your own due diligence first too

Would like to add that research is now easy as pie since I found the VP forums. Most of my info came by just reading all the posts in the kaveri seeds forum and the annual reports for past few years. One of my new golden rules is to buy companies only when they have an active forum on VP lol. Makes everything so much easier.

8 Likes

Just wanted to write about a small change in mindset that’s changed everything for me regards the stock market.

I love starting and running businesses and my main business has been running for the better part of a decade now. However, ive always wanted to start more businesses based on ideas/favorable government rules and sector explosions. The problem with starting a new business is

- You need a huge amount of capital.

- You need to have education certificates and years of study just to start a business in an alien sector.

- It takes years to make a business profitable and there’s no guarantee it will be

- If the business goes through a downturn due to macro issues you are stuck struggling with it until the issues resolve.

Cue the stock market. It literally solves all these problems. If the government gives subsidies to farmers… you don’t need to go and buy land and start a farm to benefit. All you have to do is purchase an agriculture company. If India becomes the next major hub for pharma… you don’t need to get an mpharm and spend crores to start a pharma company… you just need to buy one. Once I realised this the stock market became a lot more than a ticker tape parade. It became a place for me to join businesses in sectors that I wanted to start businesses in.

Instead of getting a diploma in a new field in a sector with tailwinds I just had to study a sector thoroughly enough to get comfortable with my understanding of it.

Instead of starting a new company I just had to search for an undervalued company in that sector and then study its financials, learn about its promoter and ensure that there is sufficient growth runway and triggers for the next decade.

Once I began thinking of companies as my businesses all my earlier issues I had with the stock market disappeared. Right now If I had a chance I’d want to start a pharma company, a chemical company, an FMCG company, a digital payments company and an agriculture company. And hence why my portfolio reflects that. Next year I’d probably want a bank/travel based company but right now they don’t make business sense. I wouldn’t start a bank or travel company now…so why invest in one. Sure they’ll be cheap now but I’d rather look for an undervalued one when the sector has tailwinds rather than buy cheap and hope the management are nimble enough to avoid headwinds. Also I don’t want to overpay for companies so automatically I look for value in lower/mid PE rather than high 30+ PE

The moment I began thinking of companies as businesses with a long term goal of where I’d like to see them in 10 years patience and market downtrends has become a non-issue. All I need to do now is ensure that the businesses are healthy, the management does what’s needed, the financials every quarter (a missed quarter or two is fine as long as the story is intact) play out the long term story, the concalls and management interviews and the annual report shows me the plan for the next few years. So I basically get to own all the businesses I want to start by just clicking on a buy button. If a business stops making sense I can just quit and walk away and join a new one in a new sector(How I wish I could just shut my current classroom education based business right now but I have salaries to pay, students to serve and stakeholders to keep happy so I can’t lol)

I’m now confident enough to ride these stories for as long as a decade and only sell if the story breaks down or book profits if the valuations go up too high ( I think of it as my business did so well that I managed to sell it to a PE investor lol). My plan even in the future is to wait for a sector to have tailwinds… and then study and buy which gives me an MOS far quicker than during a period of headwinds. It takes a LOT of studying and time to build conviction but it gives me a concentrated portfolio of businesses that I feel I’m a part of and I can pay full attention too.

Infact, I currently keep folders with each one of the businesses in my portfolio filled with printouts of financials, quarter reports, concall transcripts etc in my office. So yes… I’m basically roleplaying as the owner of all these businesses… but it’s helping me keep my eyes on long term compounding goals while also giving me a huge entry barrier before buying new stocks and hence preventing knee jerks . Time will tell if the approach works(and now my portfolio is public for all to see if it fails spectacularly) but considering the peace I feel even on days the market crashes it’s honestly helping me already.

Note: I’ve read and watched everything written and said by Benjamin Graham, Warren Buffet, Charlie Munger and even Mohnish Prabhai. And tbh this roleplaying business method feels like a less technical combination of everything they had to say so I’m not going in blindly. I’ve also studied the technical aspects ie charts of the stocks I own so I always keep upto date on all the major supports/resistances of the stocks I buy and I try to buy on days the markets crash rather than when everyone is bullish. so I’m not a total idiot who just buys businesses and ignores the technicalities and realities of the stock market

16 Likes

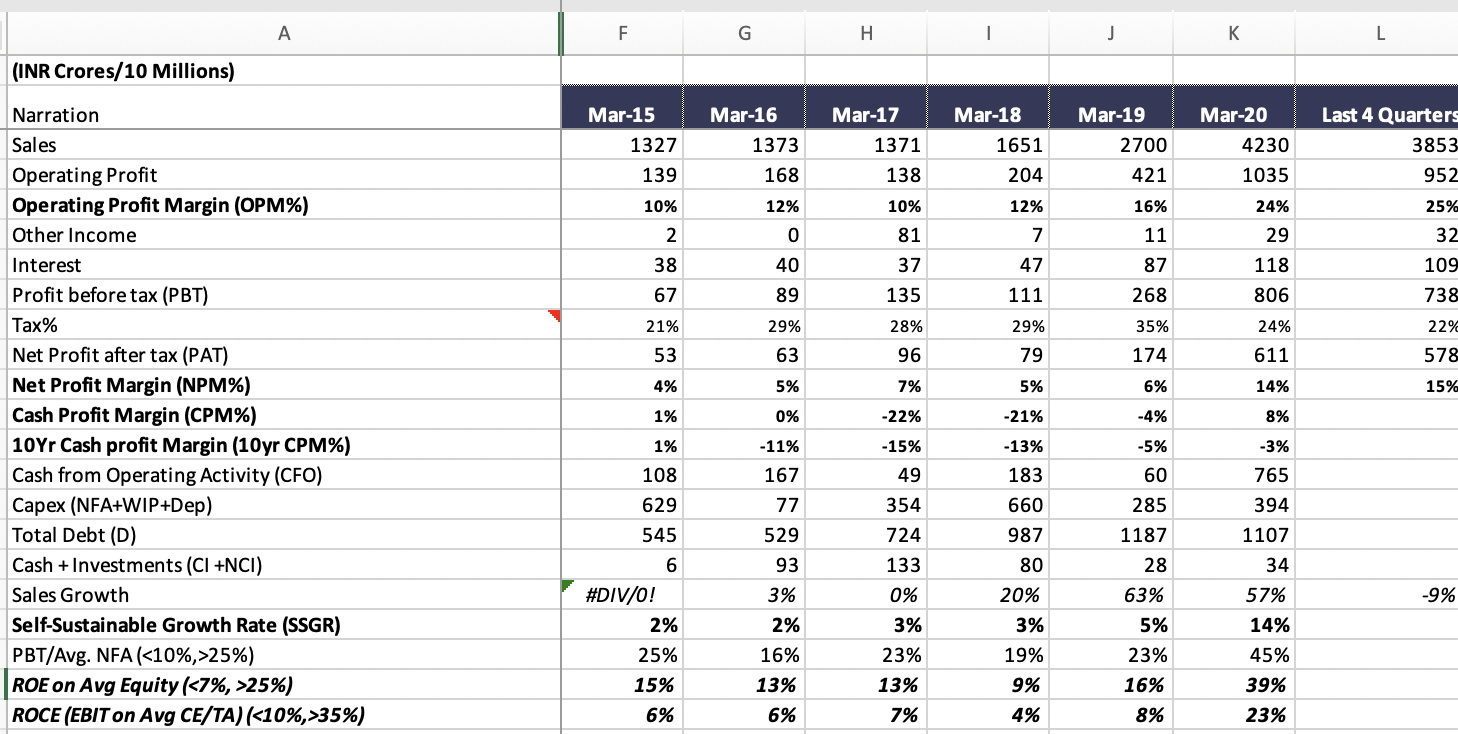

Here is analysis of Deepak Nitrite and some questions for Mr Malkd

Growth Company Checks are ok

- 5 year CAGR of Sales → 24%

- RoCE and RoE steadily increasing. From 15%, 6% to 39%, 23%.

- SSGR is 14% and lower than the sales growth. Company needs debt to fund growth and no wonder D/E is 0.7 which is manageable with a very good interest coverage ratio of 8.8

- NPM of 16% and Sales/Capital of 1.6 drive the RoCE

Accounting Shenanigan checks are okay.

- Accounting shenanigan checks are coming out okay. cCFO ~ cPAT. Other income/Other expense in lower limits. CWIP/Gross Block is low. Inventory turnover is improving and so are receivables improving.

Questions to Malkd to understand his thoughts:

-

Why is there so much variation in NPM% and the higher NPM in recent years. Does this mean that if the NPM go back to old levels (all chemical companies are benefitting from increased demand and lower raw material prices). Could this be a big risk?

-

Something sems to have turned on starting 2019. Is this sustainable?

-

Sudden increase in CFO from last year that has made it FCF positive. It was negative in prior years

-

Valuation parameters: CAPE is 26, EV/FCF is 15.26 and EV/PAT is 9.25

We can get 15-20% CAGR over 5 years, as long as the copany grows profits between 15-20% and P/E is at-least 15. My only worry is if the earnings can sustain as FY19 onwards it has been a bonanza of growth in sales and NPM.

3 Likes

Deepak Nitrites management is as blue chip as they come. For years I’ve underestimated them and they’ve always surprised me. They’ve spent almost 75 years becoming market leaders in their basic chem field but the problem with that was the margins were low. So they added performance based products to increase their margins. Problem with this is dsda etc are commodity based and hence cyclical. So you see spurts of huge margins like last year and then falls like this quarter. so the management added phenol… huge margins and huge upcoming demand as seen by government commentary and policies. So they took some care of the problems with the previous products with this already. And now comes the nimble management… seeing demand for ipa they ve increased capacity. Seeing demand for specialty chem they’ve done capex for the same and future capex will be for the same too according to the concalls. So while the margins would not be possible to maintain from last year on performance , phenol and basic chem alone they now have specialty chem growth to add to the mix and imo has taken deepak to a different stratosphere. They have steady income from basic, cyclical huge income from phenol and performance and now have growth drivers in ipa and especially specialty chem. Hence why I’ve invested. Expecting huge profits over the next few years and a spec chem re rating

11 Likes

Excellent explanation. Migrating up the value chain is the way to increase profit margins and they seem to be doing just that.

I will do some research on phenol - the anti-dumping duty is going to definitely benefit them. Usually when there is huge demand, in a year’s time, multiple suppliers get in and there is a price crash. Rememer arecanut boom in 90s, Vanilla plantation boom, rubber boom etc. Farmers in Karnataka/Kerala grew vanilla around trees, then there was rubber everywhere etc.

In any case, this is a good company for investment. Already bought KSCL and will be adding Deepak Nitrite this week, based on this thread. Excellent top notch research by Malkd

1 Like

Cheers. Yet again please do your due diligence too since I’m just a business lover and not a sebi advisor. Conviction can only be built Individually. Without it a 10 percent crash can lead to jittery exits. Also, I valuate based purely on business prospects. I haven’t done any DCF calculations etc. I prefer keeping things simple but you may feel differently. The prices I’ve bought at gives me a margin of safety now but I honestly dunno what MOS you currently have at the current price. That being said you only know your real margin of safety after you’ve bought a stock and have skin in the game… until then it’s all theoretical. There’s nothing like having a support about 10 percent above buying price and I’m not sure deepak can offer that pre Q2 so the decision is yours. Good luck to both of us

3 Likes

I will share my portfolio details soon. I have a similar picking style but I diversify into close to 40 plus stocks. That gives me leverage to buy several good ones and I treat that as margin of safety. Even if a few are wrong, I treat it as fees given for learning to stock market.

Admire your conviction in a concentrated portfolio. That is what I am trying to get to

1 Like

After a lot of deliberating I finally decided to enter the micro cap space today. Racl gear tech. Reached a throwaway price of 96 from a high of 116 a few days ago. Dint put a large amount(enough for it to be more than a tracking position but not enough for me to worry about it everyday) in it so I won’t be updating my portfolio above but it’s a huge step from me away from the safety of the 1000 crore+ companies. As an ex mechanical engineer I wanted an auto company and this covers that theme perfectly. The other option was kpit but chose racl since the members in the vp forum for racl are of the highest quality so tracking it becomes an easy process. Caters to 2 wheelers and tractors so is somewhat covid proof compared to the rest of the auto industry. My next micro target is cupid. Though I’m waiting for a throwaway price there too since there are quite a lot of issues(succession issue, us FDA wait, global tendors falling due to covid)

Edit: Also, took advantage of the negative vodafone verdict to add 1/10th of my planned amount to idfc first bank at rs. 29.9. don’t want to be exposed too much to banks right now so just did one tranch. Couldn’t resist and I want it to by a major part of my portfolio next year anyway. Will do my full investment in more tranches over the next 1.5 years as the macro news for banks improve so that I end up avoiding the headwinds and keep capital safe.

2 Likes

RACL is a good buy. But these kind of stocks crash like anything during market fall. There will surely be a ~10% correction at some point during which you can expect RACL to correct by 30-40%. I would buy it then.

1 Like

Haha wish I’d waited for this post first … anyway I’ve taken a very small position. If it does fall 30 to 40 percent I will average and let it take up approx 2 to 3 percent of my portfolio if so. My first foray into micro cap. I want to see if I can stomach it. Looking at the volumes to reach 90 though I can’t see it falling by much espexially considering their low covid impact, high OPM, huge clients and capex last 2 years. Delivery was near 90 percent earlier today too. I think for now 95 is a safe base. Unless the sensex crashes like you said though. Still see it doing well short term too however

2 Likes

Alembic Pharma has been on my watchlist for a long time thanks to the amazing thread and posterd on VP. However, it had run up too high before results and I wanted to see Q1 before buying. Post Q1 it went above 1000 and even reached 1100. I had given up. They held a QIP at 932 and it was oversubscribed by bigwigs like Tata, hdfc , bajaj etc. When the QIP came out I’d given up on ever seeing a good price again similar to when reliance had a rights issue at 1200 or so. Now it’s fallen below 932 due to the parent holding company’s schools division selling (they run classroom based schools… in the current environment they need cash for payments etc since schools are shut and income is low… so there’s no nefarious reason here) .So imagine this… how often do you get a chance to buy a quality stock at under the price given to institutional investors who have met the management , researched a stocks long term prospects and bought in bulk at a discounted price… and then you as a retail investor get an even bigger discount! That takes care of the margin of safety right there. They also deal in generics which helps me diversify within pharma(laurus is an api play, granules is a low cost high volume manufacturing play). They all overlap a bit but considering the tailwinds and business outlooks of each i don’t mind. Long story short I deployed all my balance cash in waiting and have added alembic pharma and it’s now a new core member of my portfolio taking 10 percent at and average price of 917. I had kept the cash to average down my companies if needed but I’d rather bet on them doing well then bet on needing money for averaging. I’ve also realised that I’ve slept really well for months but last night i barely slept due to my small bets on idfc and racl. They may be small bets but the business outlook for both sectors make me uncomfortable even though I trust both businesses. It’s made me realise Im not built for buying beaten down stocks in bad times but rather somewhat undervalued stocks in good times/sectors with tailwinds. If I can’t sleep tnite either il be doing a btst on both of them tmrw (racl will have to wait for delivery due to no btsts for it). Small amounts but capital protection is always key for me no matter how small especially since I may need to liquidate a bit in a year or so if the headwinds continue in my own business. Planned expenses for around 8 months for the worst case scenario for my business but if covid doesn’t allow normal resumption even by then I may need to book a few profits so would rather stick to tailwind sectors just out of paranoia for the worst

7 Likes

Considering your concentration in Pharma and since Granules and Laurus are part of my portfolio too, how do you think about geopolitical risks at play here?

Any kind of trade issues with China would effect these two badly since they rely on China for raw materials and intermediates. Also I have been thinking about the risk of regulations in countries like US for ex - deciding to manufacture their own FDs, APIs or regulating drug prices which Trump has already stated. Personally I don’t think that would play out as cost advantages will eventually win out over short term patriotic sentiment but it is still a concern.

I was a bit concerned on the day trump signed those orders. Upon further digging I began to realise it’s just election noise. Looking at his pattern of behaviour for 4 years him actually going against big pharma did not fit… him making a short publicity stunt about it did. So I am playing the odds with the US and have dismissed trump. China is a worry I have to admit. Ever since countries began shunning China regards trade I began worrying about china. When a country is already going through economic turmoil and bad name via covid … threatening them with trade puts them In a nothing to lose situation especially when they’ve already spent so much on BRI. The basic priniciple of NATO and the UN post world war 2 was prevent World wars by facilitating trade. So in the worst case scenarios I do have brief moments of panic regards china. But it’s in no countries interest to start a war yet so I just ignore it as noise. In the end trade always has won over the past 75 years and I can see it winning now too. Again, I’m just playing the odds. If things worsen it would mean leaving the stock markets altogether and not just pharma anyway… and pharma has more than enough tailwinds in the mean time. From what I’ve seen this has now become the main long term concern for most pharma companies and good management… and they are already working on backward integration and using capex to lower their dependance on china. So in a few years this won’t be an issue anyway. Plus I have full faith in businesses over goverment. The most cost efficient method will always win in a business environment so I try not to mix politics and business unless really necessary. Sometimes you just have to ignore the noise and focus on the information in front of you at present and not speculate on macro affairs until they play out. So that’s what I’m doing now

3 Likes

Agree that pharma and chemicals are the plays currently. The bull market for these has started just 4-5 months ago and is likely to last at-least 1 year. As long as we have quality picks from the portfolio of pharma and chemicals, nothing to worry. I think it makes sense to be in sectors with tailwinds and ride the wave. That is the right strategy

If we see the US stock market, every 4 years or so, there is a bull run towards election time as the Presidents do everything possible to pump up the markets and have a ‘feel good’ factor. Tightening if any is only possible Jan/Feb 2021 onwards and by then pharma/chemicals will be 1.5-2X from here. If you just sell in Jan/Feb 2021 you have made your CAGR

4 Likes

Yup. There’s a video in the granules thread where the granules ceo mentioned that Q1 is just the base and the other quarters will be better this year when questioned about the pharma bull run. That convinced me more than anything else. Expecting laurus, alembic and granules to have an eps of around 70, 60 and 20 by Q4 this year. If they pull it off(and all signs show they will) then expecting them to trade at PEs of around 25 to 30 by then. If this does play out theres a high chance they’ll be trading at double my buying price. Calculated bets for the medium term if Indo-China doesn’t get worse. The odds are in our favor though so I’d rather take a chance and bet big then watch from the sidelines. When the stock market throws you a bone you have to accept. Gives a chance to profit book a bit if corona continues to disrupt my business etc too next year. Regards chemicals it looks like deepak re rating is already in progress was at 10 to 11 or so PE when I bought it. Read and article by dr. Vijay Mallik that mentioned that once a company crosses 10000 cr MCAP they get an automatic higher PE by the market due to perception of stable/strong businesses and that looks like it’s happening with all these stocks specifically. So overall I’m pretty comfortable holding pharma and chem at present and ignore the noise(for now).

6 Likes

I am staying away from Cupid due to possible governance issues, in the latest concall one of the analysts asked about some writeoffs of loans given to companies run by relatives and it wasn’t answered properly. You may want to check that out.

Yup. Decided to stay away too. One reason was the issue regards the real estate write offs, the other was the succession issue. Also, I’d rather wait for demand to come back since I’m sure developing countries have other priorities right now and hence tendors may go down. Also, would rather wait for us FDA to get confirmed. Will only consider around 150 or if the problems all go away. Wouldn’t mind buying higher too if that happens.

2 Likes

As you mentioned cupid - which is a small cap consumer oriented company and can be considered an OTC healthcare subsegment…what are your thoughts on a more than 100 year old OTC leader in pain management Amrutanjan Healthcare? Their new generation has been trying to change things since last 4-5 years or so not much results in numbers though yet…their fruit juice segment not sure what they are doing and sanitary napkins also not much info I could find in public domain. Marcellus invested in it but thats a no event to me , just thought to mention as many track Marcellus. I have been tracking Amrutanjan since few years now but havent invested yet as I do not get sufficient info about the company and its progress in public domain and I am not an accounting expert and cannot read from numbers alone. Any inputs would be great to have from you. Thanks

3 Likes

Adding to your points,

I have been tracking Cupid from last few months, even I didn’t find consistency in the business model. If I just talk about the business then they are now trying their hands on Medical devices, which I found absolutely disconnected from the kind of business model they have.They are not even thinking of expanding in the case of heavy orders, on the other hand they will outsource it from somewhere .This gives an indication that the management is not confident about the business sustainability.

1 Like