This is why I’ve invested in Deepak nitrite. They just posted an entire investors update for the quarter and clearly explained the issues they faced, why revenues fell, future growth plans, what to expect over the year and how management will be tackling and have tackled the issues thrown at them. They did this after an AGM where things were explained clearly too. i have never been so happy with the management of a company and I am shocked to feel such conviction for a small cap and it honestly makes you feel like part of the company. Very investor friendly and that is very rare to find in this day and age. Dint want to spam the Deepak nitrite forum so posted here. Their management really is what makes them so good.

6 Likes

Over the past few days I’ve been intensely following suven pharma and granules. Suven looks like a risk that could pay off handsomely… high operating margins , very profitable crams and specialty chemicals business… stability in formulations business via andas and very interesting rising pharma business has made me take a gamble. Started buying at low rates so even averaging up of late has led to a decent margin of safety. It now makes up 5 percent of my portfolio. I won’t be adding or subtracting more for the foreseeable. My quota is over. Hoping I get a bumper result on Monday so that my margin of safety goes through the roof and I won’t need to worry about it again. Also, been watching interviews and reading concalls of granules and the drop on friday led me to increase my allocation to 5 percent. Very confident management and their vertical integration and high quantity, low cost formulations business gives stability for the long term. Very safe bet with good management guidance and my allocation has increase to 5 percent. Will not be adding any more since I’m very overweight in pharma as it is. To free up the cash for adding to granules and Suven I have cashed in on iolcp and exited completely. Still think they’ll be a good bet but tbh granules feels like a safer version of iolcp with no one product dependance so I’ve made the switch. I’ll be saving whatever cash I make this year and keeping it in hand incase I need to average down my 6 companies if they break supports and crash over the next few months. Cheers

Note: Editing my portfolio in my original post accordingly

7 Likes

Update: Took a position in Kaveri seeds today morning. Had noticed a post by Hitesh sir regards it in the 52 weeks thread. Had the day off so I Did a full day of studying yesterday and built conviction and added some with some of my balance cash today morning. The quickest I’ve ever made a decision regards a company but I’d studied Kaveri years ago so had a good base to begin with(plus after pharma and chem studying an agro company is super easy in comparison  ). Classic turnaround story in a sector with tailwinds ie agriculture and thanks to the genius insights here on VP it looked like the perfect entry point too. Will update the portfolio soon once I’ve finished adding(just checking the finer details before putting more cash in). Hoping it consolidates a little longer. Cheers.

). Classic turnaround story in a sector with tailwinds ie agriculture and thanks to the genius insights here on VP it looked like the perfect entry point too. Will update the portfolio soon once I’ve finished adding(just checking the finer details before putting more cash in). Hoping it consolidates a little longer. Cheers.

Edit: Managed to accumulate nearly 10 percent worth of my portfolio at 606 .

3 Likes

Just wanted to add… my portfolio is the 100 percent stock based one in this thread. For my wife I’ve created a portfolio based on

- NCDs(Currently Shriram finance at 8.40 per annum)

- INVITs(Currently India grid at 12 percent per annum)

- REITs(Currently Mindspace and embassy at approx 7 percent per annum)

- ITC( treat it like a debt instrument around 5 percent per annum)

Every quarter or so I take her savings from her business and put it into whichever of these are at a low/offers the best interest rate. Over the year it ends up being 25 percent spread equally among all 4. So half our money is totally safe. Hence why I can take risks with concentrated allocations in companies in my portfolio and I will continue to do so. Felt I had to mention it so that people know that risks are mitigated and don’t try to replicate the same. If there are any similar instruments that I’m missing(like an invit or REIT) do let me know… Cheers

9 Likes

By REIT, do you mean the listed equity offering 6-7% dividend yield?

You can also look for PPF and NPS both of which offer 7% and approx 9-10% respectively along with tax benefits. If salaried then VPF also works fine with approx 7.5% at present if I am not wrong. But yes the capital gets locked for longer terms here…would be nice to know your thoughts on these three instruments for safety…

Agree on ITC…How about a solid PSU like say Coal India or even ONGC/NHPC offering close to 10% yield at present. These resources companies are here to stay and government will ensure dividends as long as these are profitable enough…

Yes. The listed REITs. Part of the thrill in INVITs and Reits is that over a decade+ the capital invested will grow and so could the dividend percent. Plus I’ve spent a lot of time studying both invits and Reits so I feel comfortable investing in them hence removing that risk associated since I can track them quarterly without a lot of trouble. We both have been investing in PPF from a young age but it will be maturing in around 3 years. Post maturity I may shift mine to stocks and hers to the above 4 instruments since while the tax saving benefits are huge the lockin period gets a bit too long .

Considered NPS but again… the lockin is a deal breaker. I like NCDs, reits, INVITs and ITC since the dividends we get help cover expenses every quarter/year hence making it easier to save our capital without breaking our instruments and letting the magic of compounding run its course. So even when our businesses go through a downturn(like right now) we can still cover our expenses without dipping into our savings hence not getting in the way of compounding so that we can be financially independent in 15 years and run our businesses out of passion rather than necessity. I looked at PSUs too but none of them fill me with confidence regards capital protection…the only one I really like is RITES(Railways). Looks like the perfect mix of dividends and long term stability but considering I want 0 risk I’m still studying it(and watching my margin of safety disappear as a result ) . So what I’m looking for is capital protection, chance of slight capital appreciation(not a priority but would be nice) and consistent but high dividend rates. So far reits, INVITs, NCDs(non cumulative), ITC and maybe RiTES fit my criteria.

1 Like

Thanks @Investor_No_1 PSUs are the next logical investment. I’ve managed to filter RITES. Will be studying it judiciously next few weeks…the problem with coal India , IOC and other PSUs are historixally they have been wealth destroyers at higher levels… And since il be investing in a sip format I fear il get stuck somewhere at a high point and won’t be able to retrieve my cash if it crashes. Rites looks a bit immune to that the way it’s set up. And railways look like they have a huge runway. So Im pretty excited about it. Thanks for the tip though. I do also agree that the only option left are PSUs

1 Like

Although I have not studied INVIT and REITs so far, I am wary of debt instruments other than the PPFs, NPS from GOI. Any other debt to me is more risky than carefully chosen equity. Debt from a poor (only known in hindsight) corporate can collapse (and take you completely by surprise as you are not that vigilant like say in equity and also such collapse have been seen overnight in past) but a carefully chosen equity company would grow in long term. Also, I see that you have long term vision of say 15 years which makes instruments like PPF all the more interesting. After maturity, you can continue it in blocks of 5 years with or without contributions. Tax free 7+ % returns and exempt even at maturity would make it ideal retirement instrument where safety is needed. NPS is a bit tricky…even in this crash I see its funds fared decent, however at maturity you have to buy annuity of 40% amount which makes it less attractive than a PPF/VPF. Its returns are although greater at approx 10% CAGR over long term.

Also, it would not be bad idea to explore annuities when interest rates are good and get yourself locked in at higher interest rates for life before the interest rates start falling like in West. There is practically 0% interest rates in US/EU so imagine if you get yourself locked at say 8% today and in next 15 years interest rates in India are 3% or less…Would be good to know your thoughts on annuities.

Pls note I have never invested in annuity and myself also thinking on above aspects…Thanks

Thanks, I agree PSUs have been at times amazing wealth creaters and subsequently destroyers as well…say something like ONGC. Timing matters here a lot. It is better to avoid them completely if we do not understand the complex matters involved along with pure business. I have therefore given them a total pass so far inspite of thy being super attractive with great dividend yields and upside potential as well…wanted to mention above as disclosure. Thanks

I’ve not studied annuities in detail either. Basically her portfolio is a compromise. Once I build conviction in a company I tend to go all in on them(for eg laurus and Deepak) and will continue to do so with my portfolio. I’d initially planned on doing the same with hers but at her request she wanted less risk. FDs and government bonds and annuities etc just seem like too much of a compromise for me though … I like the atleast remote possibility that my capital increases along with interest. In most debt instruments this will never happen. With the hybrid instruments once you really study the different options available they do not seem risky at all.

- NCDs: if investing in companies you’ve studied well then there’s no issues here. All it requires is a good initial company study and then it’s all clear. The odds of the company does an ilfs are very low

- REITs: instead of buying a flat and looking for a tenant I’m buying reits. Infact it’s safer then an actual real estate instrument since you are buying with smaller investments and getting a guaranteed tenant

- INVITs: the fact India grid has 25 to 30 year agreements in power transmission makes this a safe bet. I would never buy a road or infra based invit(looking at you irb).

- ITC: my thoughts are well documented here. This company will probably outlive me and will be a continuous wealth generator for my kids(if I have any)

- RITES: asset light model with less government interference. The bonus is it has everything I’m looking for in a company ie high roc/roe , op. Margins etc… I would invest in this in my core portfolio too tbh.

There are small chances that some of these companies could go bankrupt but the chances of more than 1 doing that are very low so at max 20 percent of the portfolio is at risk. Plus I’m sure il see the signs coming before hand so at max there’s a 5 to 10 percent risk of capital loss here. There are high chances that her capital could double over 15 years via these 5 too as well as give dividends equivalent to a salary by then as opposed to parking the money in debt instruments alone. At the end of the day I enjoy investing so tracking 5 more instruments(4 considering I have ITC) makes it even more interesting for me and even though I’d rather pure equity some part of me acknowledges il get better sleep this way tbh. Note: I’m also considering the high dividend payout IT company sonata as an option. That seems a bit risky to do though haha

3 Likes

@Malkd @Investor_No_1 How does Sukanya Samriddhi Yojana fare as long term saving. I am getting Income Tax exemption also in this scheme. Does Reits, INIVIT, NCDs etc have Income Tax saving benefit?

1 Like

The magnitude of how underpriced Kaveri is kept taking over my mind everyday. Today morning I finally decided to stop dilly dallying and add more. Problem was I may need my spare cash for my business over the next few months. So I made the tough decision of selling Suven pharma today at 720(at a nice profit) and bought 5 percent more of Kaveri(602) for my portfolio(my timing was accidentally immaculate! And the urgency justified based on the run up since today morning). Nothing wrong with Suven… however, kaveri is a lot easier to track(vegetables and rice) over suven. I recently listened to the concall for suven and realised how difficult it would be for me to keep track of it especially at such high valuations which have now reached nosebleed levels especially since I’m already fully invested in laurus and I have a lot more stake in it. Plus I’m not happy tracking a company with just 5 percent of my portfolio (Granules is safe and easy ie manufacturing and tracking of 5 products and low PE so don’t mind so much). So I made the change. Will update above.

@Caution_Investor I’ve realised that in trying to save tax over the past few years I’ve actually lost more money due to opportunity cost of misisng out on bigger percentages just to save tax(so I just pay PPF and that’s it. When my lock in is over in a few years I may start ElSS and keep my PPF liquid but let it compound). Once I let go of that tax fear life has become a lot easier. I’m not too well versed in samriddhi yojana so I’m not sure. It looks a good bet at the interest offered+ tax savings though. The likes of nps etc just look like deferred tax instruments with huge lockins so I’ve never bothered.

3 Likes

Sorry for mentioning my views in @Malkd thread but as you asked me also here are my views - It is a good scheme for girl child for the part of your portfolio you need to keep safe. Infact, all EEE instruments offered by Gov. are good for the debt component of your portfolio. I believe debt part is for pure safety, hence dont mind a few percent less returns and what better than a EEE government instrument offering maximum yield. Only flip side is lockin period and specific ways i think in which you can use the corpus later…so if that thing matches your needs, its good…Thanks

2 Likes

I was evaluating few things about some of my stocks and thought to share with you since we discussed on the topic of dividend yield…Some stocks that I hold, specially the ones from FMCG like Britannia, Marico etc. which I had bought 5-7 years back are currently giving me more dividend yield than ITC/debt products on the initial capital. Most important point is that I never bought them for dividend in first place.

Comparing it to some companies that I did buy for dividend (and thankfully sold at right times) are like ONGC, Oil India, HCL Info, Bajaj consumer etc. all of which have not only eroded capital but also dividend reduced drastically with lower profits (except maybe PSUs who still py dividend although capital maybe lost).

ITC is not of same league as other wealth destroyers that I agree and as disclosure I also hold ITC in core portfolio. The point I wanted to make and think is that am I doing a mistake of being attracted to the high dividend yield of ITC and instead could have brought more of other pure excellent FMCG/consumer play which would in due course give good dividends as their profits increase.

There are no shortcuts. If I am getting excellent dividends today in say an ITC - there will be a cost attached to it. Am I better off in a Marico at 2.5% div yield today which in next 5 years translate to at least a 5% yield if not more at today’s buy price is what I am confused. Thanks

2 Likes

Agreed. If I could find a cheap FMCG stock I would buy it. The problem is all of them are above 30 PE and more and to buy them cheap you have to sit through a long incubation phase while they build their brands. Tata consumer was the only other one I was interested in… however, with ITC I think of it as safe and high dividend yield as a temporary 10 year bonus until it gets rerated into an FMCG other company. And then it will also offers the growth that they offer and more. So I’m thinking of this as the incubation period in a new FMCG company but without risks of debt rising/brands failing. I wanted to lock it in early because I honestly have full faith that they will be trading at the same valuations as other FMCG companies in a decade+ and in the mean time my money will be safe as possible. It’s basically the safest value investment possible and I can’t think of any large cap that I can do similar with. For my wife’s portfolio itc is a cheat code that I snuck in. Will sneak rites in too which looks good long term as a growing company. The rest I have to keep them as defensive plays(invits etc) as that’s the only way I can take so called “risks” with my stock allocations. May add a company like reliance to hers too though, however we are trying to save and invest a HUGE percent of our business profits and the dividends/quarterly payments right now are what I’ve promised her to cover any expenses she comes across for her business. So a good yield now AS WELL AS later makes sense so the temptation to break her nvestment for expenses doesn’t come up. Hence why the ones I picked for her. Totally agree with you though… Growing companies will lead to better dividend yields later. My own portfolio will always follow this principle. Also, your post and discussion with caution-investor helps me too so please go ahead

3 Likes

I’m just writing my long term views on these companies here so I know why I have the conviction I have so I can stick with my investments for a decade if possible (or look like an amateur fool in 10 years). Plus all one can do after getting a nice margin of safety is to dream big and then make a thesis at present and then check news, quarter results and commentary to ensure the dream plays out and exit if doesn’t. So here goes

In the long term:

- ITC: Fmcg Margins will be around 15 to 20 percent in a decade+. Contribution from FMCG others in revenue and profits will be the main business of ITC and cigarettes, hotels , packaging and agro will offer enough cash for them to re invest and continue paying 80 percent dividend payouts. PE multiple will be 3 times what it is today due to its switch to an Fmcg other company and less reliance on cigarettes and no esg worries and profits will have nearly tripled overall. All this just for checking Fmcg other margins and profits 4 times a year. If margins fall and contribution doesn’t increase substantially over the next few years it LL be time to exit.

- SBI cards: Credit cards will be in the hands of 20+ out of 100 people in India. Currently in just 3 out of 20. Kazakhstan has 20 out of 100 so it’s not too unrealistic. SBI cards will grow with the increasing market and won’t show any sign of slowing down. It plays perfectly on the tech, digital, consumption and finance theme in India. Upi and digital payment companies will never be able to offer credit since they’ll need to rely on a bank for this and the risk of npas is too high. The only other competitors are banks and nbfcs who have credit cards who demerge and get listed… but they already exist in non listed form and SBI cards still has no issues enjoying it’s bit of this huge pie. Can honestly see this being a ten bagger IF the quarters/Each year proves growth isn’t slowing down. Will need to run away as quickly as possible if growth does slow down due to high PE multiples

- Deepak Nitrite: will be 35+ PE specialty chem player with specialty chem being the main growth driver and offering secularity in growth via phenolics and a cash cow for internal accruals via basic chem and performance products. Just need to check this in their balance sheets every quarter/year. Probably one of the few companies I have full faith in tbh since their management has always been fantastic at finding growth triggers

- Kaveri seeds: Will have managed secularity of growth due to diversifying from cotton to rice/maize as growth drivers for Q1 and will have safety in the other quarters via vegetables. Will continue to have huge amounts of cash to give to investors as dividend and buybacks. Will be rerated for its secular growth and profits to 25+ PE. Need to keep an eye on new growth drivers(for now rice) and the contribution of vegetables. Also, need to make sure management walks the talk via buybacks and dividends and growth next few years.

- Granules: Conservative management will guide for slow but steady growth via internal accruals for the next decade. They will have diversified to more products from their main 5 and this secularity in growth will cause a re rating to 30+ . Again, the management gives me confidence here. Very conservative and have walked the talk.

- Laurus: IF the remaining quarters this year prove that Q1 is the new base then it’s EPS will shoot to 70+. That may lead to a huge run up and cause me to book of profits at some point. If growth can still be guaranteed without any more debt and pledging post this year then will continue holding. This is a 1 to 2 year and then reassess again play for me. This is easily the most explosive medium term option for the next year or two that I’ve seen in the stock market for a while though.

My next target is a private bank(Idfc first bank) post Corona and something related to Tech/IT(Indiamart, KPIT etc) and if I feel I can stomach cyclicals maybe auto(Racl geartech) and metals (rain). Unless another option like Kaveri screams at me of course.

3 Likes

Been ressearching stocks sub 1000 Cr cap last few days. Found 2 that just bowled me over… Racl geartech and Cupid. They are currently providing buying opportunities. May invest a small amount in both and test the micro cap market. Cupid especially looks fantastic. Won’t be a major part of my portfolio but considering the upside I’m hoping that they end up automatically being big parts of it in a few years. May make the small investment in Cupid sooner rather than later.

1 Like

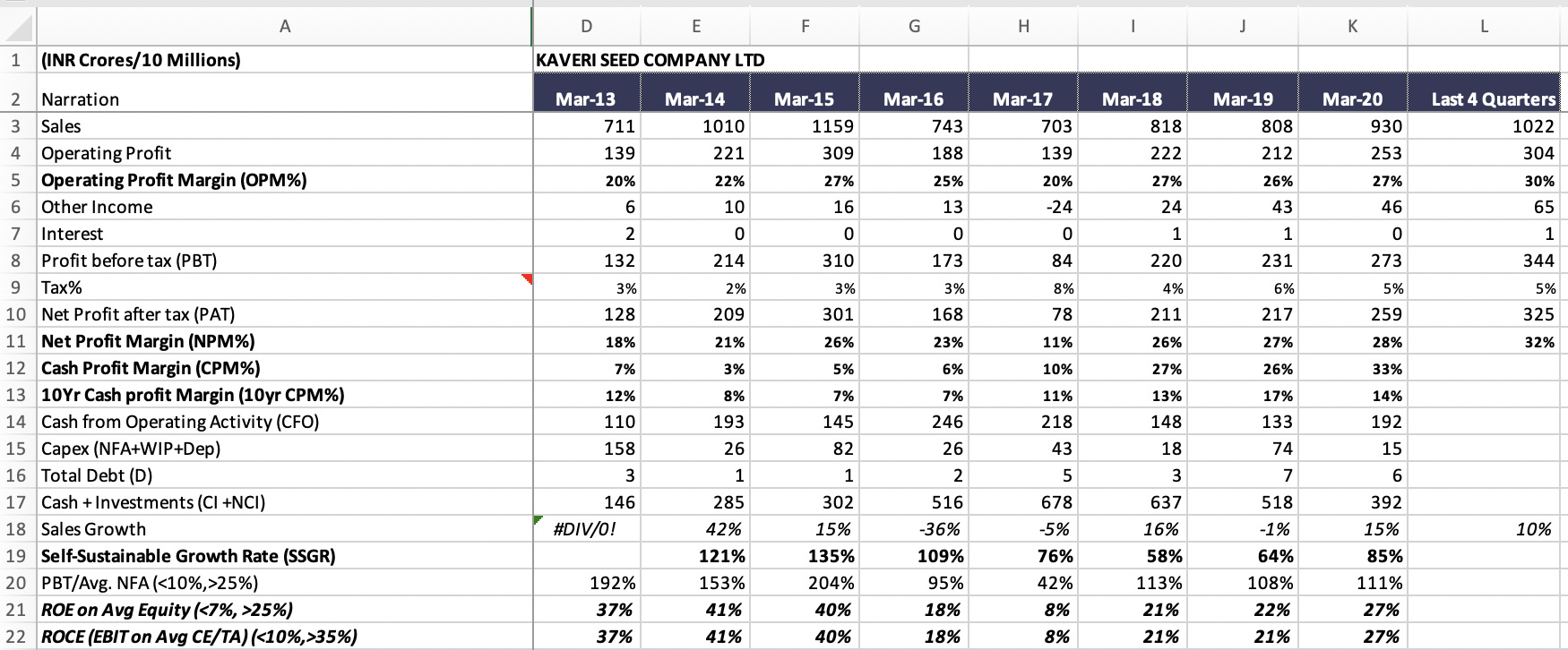

Kaveri Seeds has not shown any growth since 2014. Sales at same level as 6 years ago

I am trying to understand why the sales growth tapered off over the years. Unless growth comes back, it might not get re-rated. Any thoughts/info from the latest earnings call?

Hey @rkirana … so it’s a fantastic story. Back in 2014/15 kaveri was mainly dependant on cotton seeds .Then the government price controlled cotton… so their margins fell and the demand fell. Then they had a legal issue with Monsanto and it led to further decline and there was a triple issue since there was an audit problem which led to the fall in image of the company. Since then the company double downed on changing their product mix and maize, rice ie other field crops began contributing more to the revenue and all of their capex was sent towards these. Now rice is their main growth driver and maize has been increasing too over the past few years. So they are no longer dependant on one product even if future government issues prop up. However, this makes them very Q1 heavy (since field crops only have a limited growing period). The management was so nimble that they increased contribution from vegetable crops and hence why they’ve gone from losses in the other quarters to profits in Q2, Q3 and Q4. All management issues went out the door when they passed Mohnish prabhais checklist in 2018. The management promised growth of 20 to 25 percent in PAT for 7 years back then and theyve done the same already for the past 2 years. They have a lot of cash in hand and promised buybacks and they’ve done the same too(and they still have 200 cr for buybacks and dividends and 300 crore for emergencies). So imagine this… you have a company with great nimble management, growing profits at 20 to 25 percent per year, with 3 main products and new growth drivers, and profits in all quarters and not just Q1 who have finished a lot of their capex over the past few years and all cash made now will be distributed among shareholders via buybacks and dividends for the next few years at a PE of 11… Overall this is the definition of a turnaround story and the market has still not realised this and are pricing it based on the issues in 2015. Check the last few years and you’ll get a good reflection of the next 5 years. Considering all of the above AND the low valuations it’s probably my favourite stock in the market atm with limited downside. I plan on holding for 5 years minimjm though. In the short term the market may need to see more before giving it a re rating but I’m comfortable waiting since at this price I have capital protection(huge consolidation here+ the future planned buyback will keep this level safe) and the agricultural sector has no headwinds due to covid. If the management do what they say they’ll do(and they’ve done it with low cotton and maize prices too!) I can see a re rating of atleast 2x + a 20 percent growth per year over 5 years with low risk.

8 Likes