I think midSize bank will be under much duress in the next 2 quarters , but as u mentioned if IDFCB and BB comes upto 1X or 2X there book, i will jump on to it.

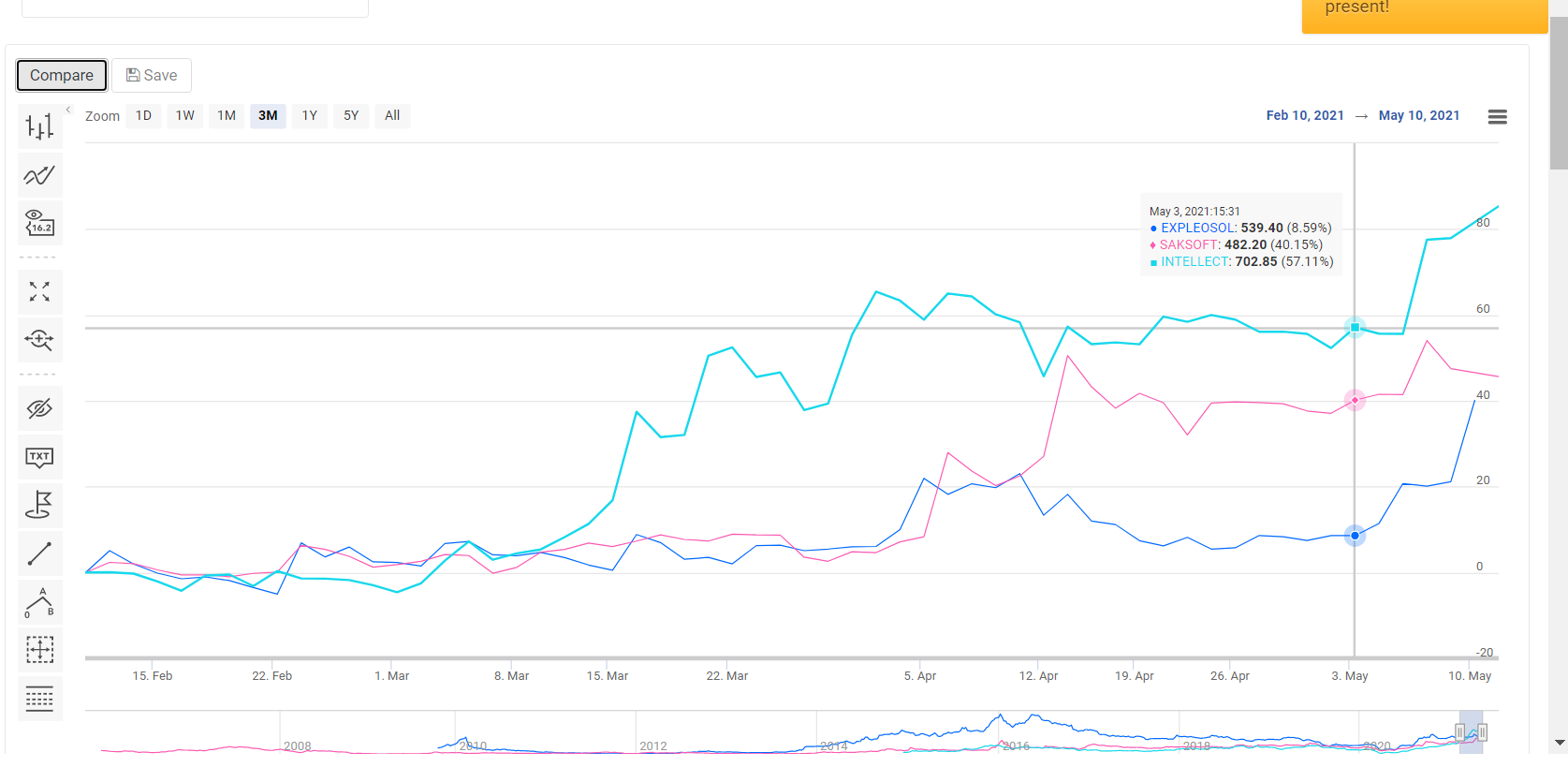

We Studied Saksfoft, Expleo and IDA during mid Feb , and looks like we took the right call

I had a graveyard of good ideas ie expleo at 466, saksoft at 330, Kpit at 60 etc which I acted on and then sold too early… lol. anyway when I sold them I used that profit in the likes of laurus/deepak/intellect etc so I have no regrets. Made similar in less risky companies and have less things to track post concentrating my portfolio into a few names so I can’t complain.

My entire watchlist currently is filled with financial names including idfc first, bandhan bank and even Edelweiss etc + some realty names like sunteck and nesco etc (post studying realty for embassy I was hooked). I have the cash available too. Hopefully some good opportunities pop up next few quarters.

Btw @rshankv I’m still quietly building a position in just dial and will continue to do so. Next few quarters should be mute so should give a nice opportunity to add for a while. Added more today sub 800. I almost feel like I’m an idiot for accumulating it but it ticks all of the boxes for me. It has no existential threat considering the cash in reserves and post the last concall and some scuttlebutt ive done regards jdmart I’m convinced it will aid them in growing 10 to 20 percent a year from next year. Their core business which I always hated is actually pretty steady and gives them a nice cash cow to work with. I expect it to be the butt of most jokes investing wise this year but I won’t be surprised if it completes a full turnaround perception wise a year from now. Difficulty to hold with the volatility but it looks like another midcap disguised as a small cap. Let’s see if it works out. Q4 should provide a good buying opportunity since I’m not expecting it to be great but at current valuations it just needs to be average for it to catch the markets eye. Of late delivery is increasing to nearly 50 percent too so it’s finally left the hands of intraday traders too. Did you take a position/study it too? Would love your thoughts on JD if you have any regards the company

for some reason i didn’t believe the story of JustDial nor Indiamart, I dont have that conviction , probably bcos i have not used it , I will anyway study abt JD tonight and will keep you posted …

Go through both apps and the balance sheets of India Mart and just dial along with the latest concall of just dial and I promise you you’ll be surprised.

Minus cash in hand just dial is at about 5 times sales and IndiaMART is at nearly 30 times sales(btw both are currently near similar sales too so it’s a good starting point) and while some may say IndiaMART deserves a premium… if the space is so profitable then just dial with its existing customers + Salesforce deserves to be trading at atleast 2 times where it is now. They also have similar goals ie grow in b2b and then move into spawner businesses via acquisitions. Story seems to be playing out technically too since JD has taken a support above its 5 years resistance between 780 to 800 after a break out a few months ago. Definitely an interesting story and imo a safe one to bet on considering brand/cash reserves and with a huge upside. Let me know your thoughts post studying.

Note: I absolutely hated just dial as a service. The concalls, annual reports and presentations were a pleasant surprise when I saw how well their core business has performed over the past decade against all adversity ie Google.

While most of the stocks have run up there is still some margin of safety left with Justdial and Indiamart taking legal action to stop Justdial makes it look like they are on to something. Justdial’s website also seems to be much more interesting as compared to Indiamart’s, still evaluating as I do not under stand the economics of this business.Another similar platform that looks interesting is Sastasundar ventures do look into it.

Thanks @d.investor … I stayed away from sastasundar because I’m already overweight on pharma even though it looks like a good indirect play. With netmeds etc in the picture I just ended up overlooking it.

Regards the economics of just dial… for someone starting off a brand new b2b business it would be a long way to profitability. For just dial it’s a lot easier since they already have a huge database. The simplest way to think of it is:

Imagine you owned just dial and for years you had a B2C platform. While the platform is b2c you have a database of B2B customers since they are the ones who signup for your service. Now imagine you had customers who have successfully used your service for years… You can now upsell them this new b2b app (approx 20 percent of their revenues were from b2b as per latest concall). These customers have had success with you so would adopt if given a 3 month trial(they’ve been given an upto 6 month trial from the concall). While you onboard these low hanging fruit and create product catalogues you can leverage your entire rest of the b2c database to try out the app. You also have 1500 crores in cash and investments so you can spend cash on advertising this new app(IPL for eg. Plus in the last concall they said they’ll be doubling ad spend this year). As your app downloads cross an inflection point (currently 1 lakh+ on playstore) the already onboarded free clients get business and see the potential. Few months down the line you have happy clients and customers. You then subscribe the already existing clients to paid packages and before your know It you can set up silver/gold/platinum etc levels where higher paying clients get more views etc just like any other platform. You can leverage your already existing Salesforce to do all of the above (they’ve also hired a lot of sales last year to add to this) since they are already trained in a similar domain earlier. Once all of this is set up you just continue advertising and leveraging your sales force to ensure that clients are getting results and that customers have a nice catalogue to pick from. Keep doing this and slowly a network effect seeps in and as number of clients and users rise your costs go down(sales/advertising etc). This would obviously take a long time to play out. As per JD it will take 2 quarters for the low hanging fruit to be converted and customer base will increase by then too due to agressive ad spending and margins wont start of negative due to database/Salesforce leveraging.

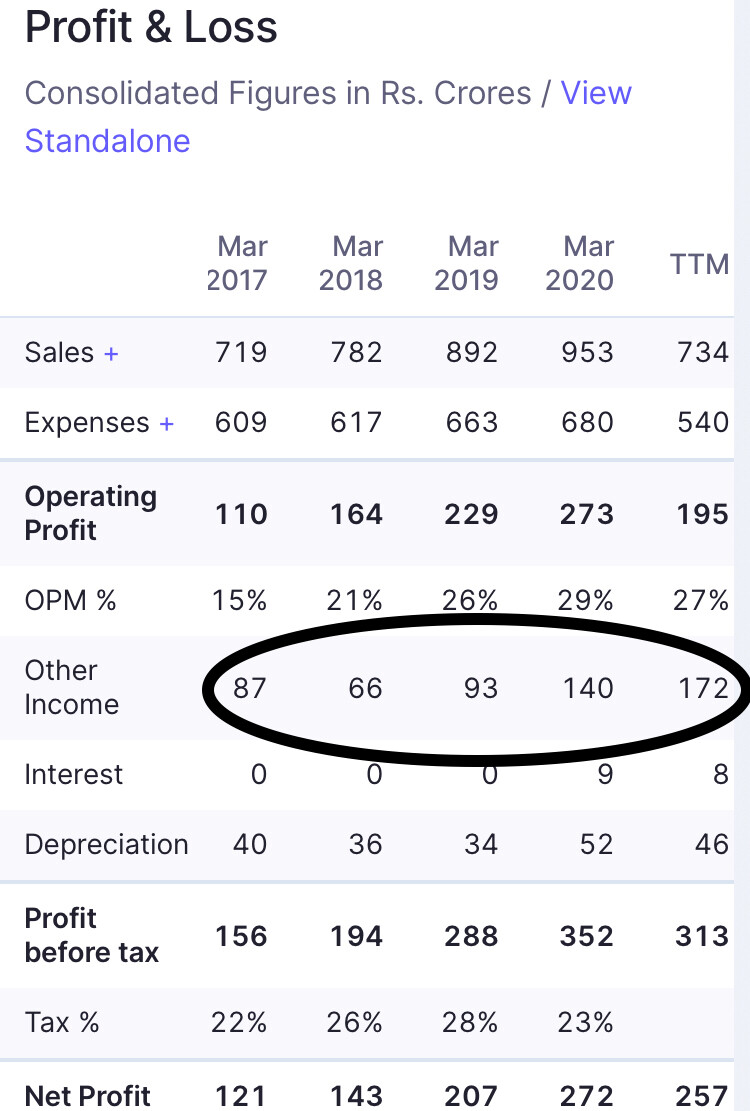

Just dial did about 273 crores operating profit pre covid and as per concall should continue growing at 10 percent per year post covid. Their investment income covers interest/depreciation costs and then some so even if their growth in core is stagnant there is a stable base. From that stable base is where JDMart (and soon JD xperts) will launch. Imo currently company is cheap at just 3500 crores for the core business (minusing cash and investments) and the entire b2b business is literally available for free. If it’s a success then there’ll be a whole new income stream to be valued. If it fails the core business is still sold at 12 to 13 times which should be the growth rate for some time anyway. Hence why I’m bullish.

Note: of course everything above has to be tracked every quarter to ensure its playing out. Main thing is knowing what to track. Il be adding more as the story plays out above every quarter or when I get it at higher margins of safety. This is almost like buying a startup with a safety net of an already existing income stream and is no way something I’d just blindly put my entire allocation in.

You’ve perfectly captured the market’s thoughts in your previous posts. I noticed that all the brokerage reports that are currently available on JustDial are quite old, and only evaluate the search engine business. This makes you wonder why brokerages that include JD in their coverage universes have missed such a large business offering, or have chosen not to write about them. There is also a lack of ratings reports over the years.

From Anand Rathi’s report on IndiaMart:

Competition hotting up, but IndiaMart has first-mover advantage. We

believe that B2B businesses are difficult to build, but easy to scale up once

network effects are in play.

We know how good Just Dial’s network has been with their legacy business, but to me it looks like the policy on subcriptions is key to understand which of the two looks more attractive to businesses.

From their concall, the most interesting bits were their goals for the platform over the next twelve months, and the really smart staggered subscription costs between small and large businesses:

As far as pricing is concerned, so there will be multiple packages on offer for our customers. These particular packages will vary depending on the type of category, will vary depending on the type of geography. The core essence shall be that if you take up a subscription on JD Mart, there are certain items that you will get. For example, our comprehensive digital catalog for your business, a JD verified or a JV trusted stamp for your business, depending on whether you qualify. And apart from that, obviously, you will get a certain assured number of inquiries for the amount that you pay us. And in order to give comfort to SMEs, we are planning that whatever amount that SMEs will pay, that will be deducted only against the inquiries that we shall be delivering to them.

They’re being really fair with their trial plans, and are confident that the numbers will come as a consequence of these green shoots.

This said, I was wondering how often JD updates its database of business details. There are a lot more reviews of the app now since the launch, and a lot of the reviews mention how the numbers for various businesses are the wrong phone numbers. Some of the reviews are spurious, and clearly spam. I don’t trust reviews in general, but some are recurring with various details. People also post negative reviews more often than positive experiences in general. I’m following the various changes they implement on the app with every iteration (Last update April 19th).

All in all, I think they need time, and a lot of visibility before the market properly evaluates JDMart. As I’ve written on my portfolio thread, my family and I tries to diversify holdings between us, and we’ve been slowly building a position in JD over the last quarter.

@Chins … I was with the market tbh. Until I delved deeper. There’s a gem here. However, a lot of patience and volatility lies between it’s cmp and the day it challenges it’s all time high price. I think the market has grown numb to just dials new offerings ie omni pay etc. They’ve tried and failed multiple times. JD mart is right up their alley though and I’m just surprised they dint delve into this earlier. I honestly can’t believe I’m getting a platform business with such potential at these valuations. Very contrarian bet in a hot sector but with a not so hot stock. Would I buy just dial outright as a pure Business if I had 5000 crores? As a pure business bet yes i would.

Anyway, I read your post after I posted my thoughts regards their business model btw. That post above concurs with your thoughts regards their approach to the b2b app and business model. Good luck to us both. Expecting a very volatile 6 months until we see jdmart affecting the P&L positively. Until then it’s all about trusting the managers during the concalls.

Regards the reviews… I’ve gone through a lot of them and most of the negative reviews are duplicates. It bodes well that someone thinks they need to spam them with negative reviews. However, I’d just look at app installs and not the reviews for now(a lot of the positive ones are clearly spam too to cover for the negative ones lol). There are a few well written reviews that look legitimate and based on my experience with the app so for I’m leaning towards those. I’ve personally spoken to a couple of suppliers regards buying education institute benches and supplies etc through jdmart and all of them have been legit. Though I dint place the order yet due to lockdowns. A couple of my industry related friends have already shifted to it for their factory needs. The verified suppliers atleast are legit and the UI is fantastic vs IndiaMART (which I still find looks cheap). My wife is an architect and she has here own suppliers… but I showed her jdmart and she now has an even bigger list of suppliers and all of them have been legitimate. She too loves JDmart now and she told me that almost all of the major and minor suppliers in goa are on it already for furniture and interiors. Fantastic app and it’s just in a nascent stage currently

thanks a lot for this information, i will study this company let you know aboout my findings soon.

I also wanted to pick on mind on your exit strategy. I have been in the market for 4 years now but the first 3 were fruitless and the last year somewhat of a luck factor was involved. There is too much noise in the market at present which can cloud one’s judgement specially if someone is new to the market. With so many stocks hitting UC and so many sectors outperforming the others; its hard to focus on the core portfolio and I keep on thinking about whether I should book profits and move my money to other stocks but I want to play the long game so I wanted someone like you who has been in the market for a long time to help me get my exit strategy straight. Thank you

@d.investor

Honestly, my trick was to invest in businesses outside the stock market to get the temparement to invest in the stock market itself.

When I started my own business I understood how ticking off short and medium term goals so that I reach my long term goal was the main purpose and that a bad month or quarter meant nothing in the long run. I understood how setting up long term contracts (in my instance with certain schools and colleges) gave safe predictable income alongside the variable day to day income.

I understood how once a certain base is set via brand/network effect etc it gets sticky and each year with minimum effort that base can then be hit but breaking through a ceiling needs time and effort and skills in that domain.

So when I invest I apply the same mindset. So instead of starting a business in the education domain which is where I have my main skills I for eg start a business in the chemical sector. I go through the same steps I do with my business ie I try to understand the sector/competitors/products and the only difference is i outsource it to someone in that domain who is an expert at that field for eg deepak nitrite in chemicals. My only job then becomes timing my point of entry(ie buying it at a cheap enough price and valuation to allow the managements hard work to bear tangible fruit) and to check up on the company every quarter to ensure they are performing according to plan and to realign goals etc. As mentioned before, Till date I have a physical folders of all the companies I invest in and I print every quarter result and write notes every quarter to make it tangible(though I am planning to moving to a SAAS soon lol) . This makes me feel like a part owner and hence why I prefer concentrated bets with big holdings. Then the only job becomes setting a long term goal and trusting the management to handle the day to day and any pitfalls along the way(hence why management is key for me). So exiting is always far off in the horizon unless I question management(kaveri), I made a mistake at the point of entry(borosil, xelpmoc etc) or if something like covid comes and makes everything look cloudy and impossible to track (lenders). In time I finalize a set of companies and once they are in my folder(usually a few months after I take the plunge and get a comfortable MOS/feel confident about owning them) I don’t let go apart from minor booking for emergency needs/tax free capital gains under 1 lakh etc(deepak, laurus, intellect, vaibhav, itc, jubilant Ingrevia, rites, oracle, embassy, idfc and now just dial are in this folder )

This helps me ignore all the noise and just concentrate on the business and nothing else. Days of crashes become buying opportunities and is when I get active. When companies reach certain milestones like mid to large cap, 1000 crore revenue etc it’s a small milestone to celebrate(though off late I’ve got a bad habit of watching their stock prices which I’m trying to break again… the last 3 months have been unreal returns wise though so I’ve been hooked watching prices! Lol). Until i am confident to add them to the folder I know I’m not sure about them so I experiment till then and it gives nice entry barriers too. Of course reading every possible book and watching every video related to investing and business also helps… and technicals helps with entry points.

Hey, Just dial is a business which has interested me as well recently. I have only a tracking position yet. I initiated that position when there were rumours about the Tatas interested of a stake/strategic alliance with JD. Never heard back on rumour but I have held on to my tracking position, currently at minor loss.

Before I increase my position here, I would be interested to know more about the Tata group findings and reasons for no alliance so far. Interestingly, it didnt materialize with Indiamart as well. It would take guts from either of these companies to say no to Tata group, if at all they did…and if Tata group took the back step, was it just the valuations or something else.

I tried to dig deeper on this, but coudn’t get any meaningful detail.

@MHS They have 1500 crores invested. Thats the profit from that every year and atleast shows the cash is real(though the buybacks also prove this… which is one of the red flags I have though. A buyback at nearly double the price last year was a bit desperate). In the future management has said this cash + equity (when they reach a sufficient market cap) will be used for spawner business like acquisitions so I’m happy it’s real and exists.

@Investor_No_1 … I remember that rumour. There was just the one article that said it could happen. I have no idea if it will or not. It happened post concall so there was no mention of it by management. Maybe we ll get clarity this time post results.

i had sold my koparn and astec holdings so got some cash and the recent discussion and you praising just dial got me interested in it,I don’t understand how in the times of amazon and flipkart it has been growing it’s topline but maybe i don’t understand the buisness and that is ok

1)Do you think it will be able to compete with amazon and flipkart and other e commerce giants that keep on gaining traction eyery day and also new startups that keep on coming up every week lol?

2)Here in delhi i see a lot of users using olx for B2B and i have seen a lot of from car dealers,to computer sellers, to furniture sellers ,to real estate agents all going for paid or featured ads do you think it has a advantage over it over olx in the B2B business?

3)Main question what kind of spawner business would it acquire going forward i already have 2 stocks kaveri and expelo in my portfolio that are masters in poor use of capital allocation lol and i dont want a 3rd(They are also cheaper and i feel have runway fro growth if capital is used in a good way)?

i am trying to trim my share allocation and running a concentrated portfolio so i might be net picking ,maybe i am not understanding what you are understanding but i would not make it a part of my core long term holding portfolio. I love both deepak nitrate and jubliant ingrevia but i have not been able to get a good price to enter in both the stocks so patiently waiting on itc and waiting whenever these get in buying range will sell itc and buy one of the above (i know this is not for you as you are speciality chem heavy but why not look for a I.t stock or even hero motocorp or any other field to be diversified that is available at such mouth watering valuation).

By the way i didn’t know you were a teacher ,Luckily in my time teachers were amazing and had a personal motherly touch but right now i just feel like education has become to monetised(at-least in delhi) . It is good to know that there are still teachers like you still out there teaching people like me and others irrespective of anything in return maybe a little bit of social validation like we all do lol.if given a chance i would definetly like you to mentor my kids in the fututre teaching them financial education which is missing in today youth thanks and best of luck with your investing journey.

Hey @raku

I am not praising just dial yet. I’m hoping il be praising them in a year is the point. I was as shocked as you are that their topline kept on growing. I absolutely hated their product last decade and somehow assumed the rest of India hated them too. My position is relatively small but I will be increasing it as the quarters pass IF they get JDmart to perform. So hopefully all your questions will get answered in a year or two. This isn’t for everyone. I am just very impressed by their app and I cannot believe the current valuations and they don’t need to compete with Amazon etc at these valuations and I find that the market is large enough for a small b2b player too. I cant find anything wrong with the company so I’m taking a punt. If it was valued at similar levels to IndiaMART I wouldnt even glance at it.

And yup teaching is my passion… I’ve built a business around it but now I have staff who do most of the heavy lifting teaching wise and I’m concentrating on growing it. I still take classes based on marketing/finance, economics, business case studies origin and history of maths/English etc whenever I can though but now I have the luxury of teaching what I want and when I want which is grand

Hi @Malkd, I have been learning a lot from you and this thread. I would like to understand as to how you decide at which price to get in. What all valuation techniques do you use to arrive at a price to enter. I’m struggling in this area and would like to learn this. For ex - I was researching Praj and when I got the conviction, the price shoot up like anything which has me now confused as to what is the right price.

@Gaurav_Bhandari

It’s a combination of things. With laurus labs it was well documented by VPers regards the EPS was expected to be around 20 by Q1FY22. So back in July last year laurus labs was cheap on forward earnings. Deepak nitrite was valued as a commodity chemicals company and it was diversifying into spec chem mid last year… spec chem companies had a valuation of 40+ time earnings whereas Deepak had a PE of 13 or so and the phenol business too was almost free. Similar story playing out with Ingrevia. If a company has loads of cash in the bank and has a high margin business and has retraced to near 200 DMA levels and 30 to 40 RSI (infact I try for these levels with most companies) for eg oracle/rites they become cheap too. I’d always prefer a valuation in teens over valuations of 50+ when 2 companies are in the same business as long as the lowly valued company doesn’t have any corporate governance issues for eg just dial Vs indiamart. Sometimes it’s a poor result/temporary issue that gets me interested for eg Bandhan bank. Sometimes its just a big large cap that has gone out of favour for years and is price supported by dividend yield for eg ITC. Sometimes it’s just a sector that’s gone out of favour and I have a pretty good understanding regards it coming back long term for eg Embassy offices. So it’s a combination of studying companies and charts and a lot of patience waiting for the right moment basically. The problem is usually there is a LOT of negativity and uncertainty at those levels so actually pulling the trigger with large amounts at those moments is still scary lol. However, I find comfort at low valuations and find uncertainty at high valuations even if a company is fantastic. Also, If something gets too expensive I just let it go too and fomo should never take over… there’s always another fish in the sea and every year a few good companies will always be available for cheap. I have missed out on a lot of good companies especially in IT/Tech due to this… but oh well. I hope that helps.

Hope you got the point, I as an end user, know were i need to go to get the best and JD is my last option.

Earlier around 8-10 years back i remember calling JD if i needed service, then they used to send me bunch of SMS matching me with a vendor and vendor used to call me, I dont recall calling JD from the past 5 years and i am afraid of giving my number to JD and Indiamart , as i don’t want to be bombarded with calls and other promotions, I am just paranoid

I had used Indiamart services too as a B2B customer and it will make sense for the B2B players , but for repeated orders i would establish my contacts and probably not refer to Indiamart again and again if i am purchaser. Only seller needs to obtain this service at a cost and always the case just using this as paid classified, period.

In the near future, most of the business will start using Google search offering much efficiently and ensure that their services comes in the top of search for a particular location.

what abt amazon b2b business, if amazon has smelt a business idea (which it has) it will kill the competition in no time ,of course likes of flipkart and JD/Indiamart in b2bi will play second fiddle

I have not looked into their financials , as i don’t believe the story

I am totally aligned with the below notes from raku

@rshankv

I don’t understand indiamarts valuations. Even today after this 2 week long crash I looked at it and I’m still not understanding how the market can value it so highly and how they managed a QIP at rs. 9000 which just looks like highway robbery. They literally remind me of just dial back in 2014 ie the market was going insane regards their cash generation potential, platform, tech etc and how they’ll diversify into new products and bla bla bla. And look what happened to just dial since then… so I totally agree with you.

Why am I still invested in just dial though is they have now gone through the entire cycle above ie market frenzy/using cash on new products etc and even after optically failing badly(I personally always hated them and their Salesforce) they have still managed to increase their operating profits from 30 crores in 2010 to 273 crores in 2020 and have learnt some nice lessons along the way!

Whether we like it or not they still have customers out there that have stuck with them because they have seen results and I have met some of them too.

It honestly doesn’t make sense that could co exist with Google but they have done admirably well and will continue to do so.

I won’t be surprised if they manage to do the same with B2B. Slowly but surely harass their way into profits like leeches off of indiamart/udaan etc.

I am in no way expecting miracles here… I’m expecting a slow 5 to 10 percent growth in operating income from their core product and 5 to 10 percent growth from their B2B product. While doing this I’m expecting them to generate a lot of cash. I’m expecting them to use market fervour to do QiPS at higher levels and get institutions to give them even more cash(again indiamart qip at 9000 just shows how much investors love this space lol). I’m expecting them to remain in the headspace of people by using this cash for advertising and maybe undertake a few synergistic acquisitions. Hopefully after JDMart and Xperts they stop making new platforms and just concentrate on these(no more Omni’s etc please). Maybe there’ll be another Tata type bid in the future… who knows. I’m expecting a crazy market frenzy in a few years giving me an exit at high valuations. The management is gritty enough to do the above over the next decade and while it is a “dirty” investment I can’t see myself losing much at current valuations and can actually see huge upsides in the future. If it was priced any higher I wouldn’t be interested. The fact I can be exposed to atleast some of the above situations playing out(even if just 1 or 2 of those happen I’m set) at just 5 times sales means I just cannot ignore it since nothing positive is priced in and understandably so .

Note: I was as sceptical about you about their businesses but after binge listening to all their Concalls and binge reading their annual reports of the past few years i am inclined to bet on the jockey here. They have eaten humble pie over the past decade and they themselves know this and imo are on track to correct their mistakes and considering their Goliath competitors have done a fantastic job churning profits over the past decade. Also note that after all my talks I’ve only bet approx 2 percent of my portfolio on it lol. Will increase only if some of the situations above actually play out.

)

)