I have no words for laurus labs anymore. I have nearly 50 percent of my networth in it and my main job currently is to ensure I stay on this journey of it turning into a 100,000 Mcap blue chip company(a crazy target I set for myself last year and it’s well on the way) and do all I can to protect my investment here and follow every event related to the company in detail.Yet again they have gone above expectations… 292 crores PAT in this year vs 110 YOY and 272 QoQ. That means it’s currently valued at just 25 PE even now! A huge base has definitely been set here and my outlandish target of nearly 38 to 40 EPS in FY24 looks like it’s on track and a re rating looks imminent yet again. Eagerly awaiting the concall… however, I am posting the presentation and result below. What a company… probably the biggest wealth creator il ever see in my lifetime. Since I’ve attached my personal belief and portfolio contribution I’ve posted it here instead of the VP thread.

Can you pls elaborate on the nature of the instrument that why would yield decline every year. Also, if the yield for existing assets would decline every year as per its nature and growth would only depend on acquiring more of such declining yield assets…dont you think that such nature INVIT is not good at all for long term, be it from any sponsor?

@Investor_No_1

It’s the nature of the contracts. Hence why you’ll see the cashflows decreasing every year. In order to support the yield and increase it the only way is to add more assets but its like running on a treadmill. Hence why I prefer REITs over Invits. The only time to buy an invit imo is when you get it at approx 12 to 14 percent yield. They are fantastic lock-in buys at that time due to a high chance of perpetuity of yield at that level. There isn’t a high chance the yield will rise much higher than that over a decade but you’ll be locking in a high yield for decades. With REITs the rental agreements and increase in value of land along with addition of assets can take the yield higher over the long term and hence why I prefer them. The analysts call above briefly talks about this. I’d recommend watching the entire thing if you are still considering investing. It’s the main reason I bought indigrid at rs. 90 and haven’t added since (even during the rights issue). At 8 to 10 percent yield Il always rather an REIT or and NCD over them(NCDs by these invits look like fantastic options since I do agree that the companies are safe as nails overall). I am personally going to ignore Powergrid unless there’s a day in the future where I can lock in a 14 percent yield like I managed with invit. I do not like this management at all so I may ask for a bigger premium. Lol.

Note: I’d rather we carry the powegrid discussion to its thread. I have made up my mind regards not investing in it and am enjoying my laurus moment right now haha

Thanks, I am also giving INVITs and REITs a pass for now. My simple logic is that I see risks everywhere so I am choosing the highest risk albeit direct equity. I would rather invest in equity whose 2% yield today increases at 25% every year. (There are such excellent management companies available).

I would keep revisiting REITs and not ruled them out completely for now.

Btw, congrats on your Laurus results. Its always great to have your maximum allocation and conviction pick to give above estimate results!

Speaking of REITs… I have placed a lot of faith in embassy offices at an average of around rs. 307 and it takes up a huge chunk of my wife’s portfolio. Their results are out too and they have released a huge 360 page document that is too big to attach here and this amount of detail and professionalism is why I love investing here:

I’ve only gone through some of it but the highlights for me are:

They have confirmed the change in tax structure and and announced rs. 5.6 as Q4 distribution which is 78 percent tax free! Thats over and above what I was expecting!

I don’t care about their earnings right now but they’ve been stable. Rental collection at 99.8 percent. Occupancy is down but looks like it’s just short term.

They have given full short term, medium term and long term outlooks for anyone worried about work from home. Rental renewals are as high as pre covid. Rental collections too. There will be a short term impact but by CY2022 they predict things will be back to normal and WFH is overblown.

NAV at rs. 387 which makes the discount almost 20 percent even now.

Overall I cannot wait for management commentary to learn about everything in more detail and maybe get a peak into FY22 distributions

There is too much to cover here. I’d recommend anyone interest in the commercial office space to have a read on the embassy website. Probably my favorite capital protection + yield bet in the market (not considering ITC) currently. Will invest even more if I get a chance below rs. 310 next few days which I highly doubt. @Investor_No_1 I’d recommend you have a look too. This was the answer I was looking for regards a good mix of low risk+ tax friendly yield

When the second wave looked serious a few weeks ago I let go of all my speculative/expensive valuations/middle conviction/micro cap bets and consolidated all of that money into my high conviction, low valuation bets already in my portfolio ie

Added more into:

Jubilant Ingrevia(rs. 260 average) and

IDFC first(rs. 50 average)

Sold all of the below at profit(approx 40 percent profit all combined) for reasons mentioned above ie speculation/high valuations/micro cap low liquidity and since I had to increase weightage in Ingrevia and IDFC first at what I considered were throwaway prices:

Expleo and Xelpmoc(il always look back and wonder why I even went here), Borosil(I’ve been defending the valuations too long and sahils brilliant commodity posts pushed me over the edge), Astec(couldn’t hold and track 3 chemical companies unfortunately), Racl Geartech (the position got too big ie 3X for my comfort and the illiquidity was a huge worry).

Also, Tracking all of the above relatively small positions in my portfolio just didn’t fit into my concentrated style of investing.

Portfolio is now Concentrated into my main bets that u have no intention of selling even a single share of ie:

75 percent: Laurus Labs and Deepak Nitrite

24 percent: Ingrevia, Idfc first, Vaibhav Global, Intellect Design arena

1 percent: Just Dial (will increase here after a few quarters)

Wife’s capital protection + Dividend yield portfolio consolidated into:

30 percent: ITC

30 percent: Embassy Offices

20 percent: Oracle financial services + Rites

10 percent: Indigrid Invit (Including equity + NCD)

10 percent: Laurus Labs, Deepak nitrite, Praj(took a small speculative bet on Praj last year at rs. 50 and there is no way I’m selling now after nearly 5x) to maintain some alpha

Will be sitting on cash next few months to get through any potential lockdowns that could affect our businesses.

Cheers.

Even though it’s very basic question, pls update if possible.

Any app which can show percentage of each stock allocation in portfolio as per market price so that no need to calculate it manually.

Thanks

I personally use marketsmojo app for tracking my portfolio it shows portfolio allocation, short term/long term stocks, valuations and other very useful parameters. I would recommend using this app to track your stock portfolio.

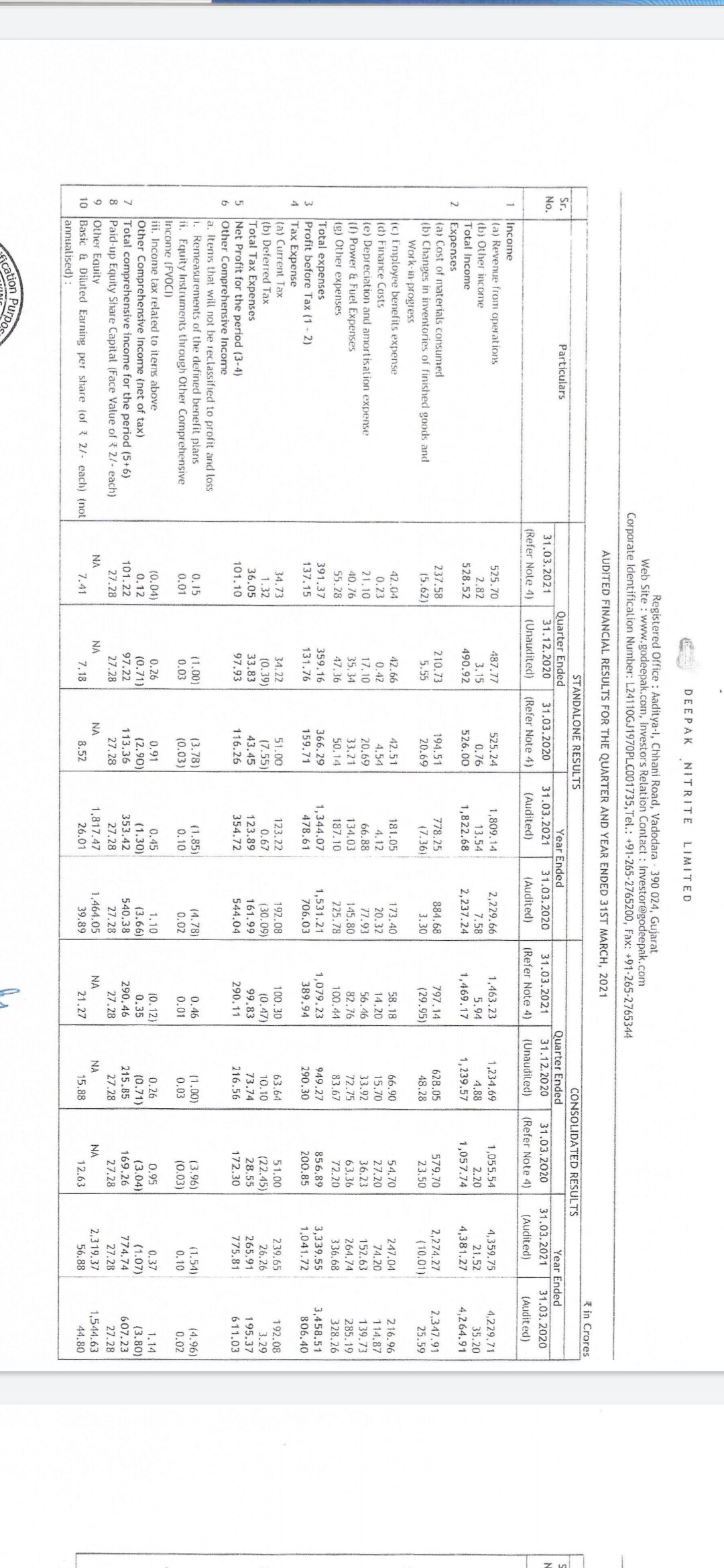

Consolidated Profit for the quarter at 290 crores Vs 216 crores QoQ and 172 crores YoY and margins have stayed above 25 percent. EPS is nearly 57 for FY21 and now it’s still reasonably cheap at approx 33 PE. It takes up 25 percent of my portfolio and has been nearly a 4X bagger for me since I began buying(Bought heavily in the 500 to 700 range and let it run).

Back then it was just a theory that it would turn into a specialty chem company from a commodity company with phenol adding explosiveness and Basic+Performance products offering a stable base and the thesis has played out perfectly since then… Though I must admit its happened a lot faster than I could have expected.

Even if phenol prices cool off over the next few quarters Performance products will slowly come back(still underperforming) and specialty chem has set a good base at approx 35 percent higher than last year. Fantastic company… it’s honestly a race between Deepak and laurus for who touched 50000 mcap first. Both are similarly valued and have set a similar PAT base. Cannot wait for the concall so a clear picture is set regards the future… I had set 70 EPS as my target for FY23 but if phenol stays elevated, performance products comes back to pre covid levels, spec chem continues growing at 20/30 percent and base chem just stays constant they could cross that in FY 22 itself! Cheers…

We can see the prices of phenol have had the expected effects on margins over the year. But the biggest monitorable going forward looks to be the performance segment. Do we know why the margins have contracted this much since March 2020?

Also these figures will be different from the operating profit margins which should appear on Screener once it updates.

The performance products segment has been a write off since Covid hit. They deal in optical brighteners and whitening agents and the entire industry ie paper, textile has been hit since Covid Began and dasda prices weren’t sustainable. Was expected to be a wash out until covid goes away so don’t expect anything here until end of this year. The amazing thing is just a few years ago performance products and basic chem was all Deepak could depend on and their quarters were defined by the busts and booms in those 2 segments prices of dasda etc. Now it barely moves the ticker when it underperforms since they have phenol and spec chem and are basically a new company.

I’m thinking of performance products as just a bonus segment now that will rise when prices of dasda etc rises and give an extra boost to earnings when phenol or spec chem underperforms

@Chins this was my thesis which explained this in the Deepak nitrite thread way back in August when Deepak was trading around 580 rs. After a horrible result and when I bought most of my holdings. It explains everything a lot better and my thesis from that day(it was pure speculation and calculation then) hasn’t changed and infact has come to pass almost exactly lol (I am very proud of this investment thesis and love sharing it since I doubt il ever hit anything so beautifully again lol)

Would I buy more now? No chance. If phenol prices turn specialty chemicals hasn’t reached a big enough level to support the valuations. However, I’m expecting spec chem to become an even bigger contributor over the next 5 years. If markets go mad and value Deepak at 60/70 PE over the next 1 or 2 quarters due to a phenol and dasda price explosion and spec chem hasnt increased at an equal rate to match the valuations then I may sell holdings equal to my original allocation and hold the rest ie majority. If spec chem continues to grow I won’t touch a single share until the journey to spec chem is fully completed and will reassess then when hopefully it will be a 100000 mcap company(which is a target i have fixed in my head for a period of 5 years down to line so that i ignore daily price movements)

Hi

What if i wanted to enter deepak nitrite now? I have been reading your blog and have built a similar conviction towards the company, While I will never have a chance to enter in your ranges. Would you suggest entering LS now or wait for certain points in their revenue mix to enter?

@Voldemort

One risk is already priced in… ie dasda/oba prices and performance in general. From contributing pre tax and interest of 420 crores it’s now only at 22 crores. So it can’t go much lower but has the potential of adding 200+ crores to bottom line as things improve.

The risk of phenol prices falling isn’t priced in but in the medium term they should stay stable and atleast not drop drastically.

Basic chem won’t fall or rise much though some capex has been allocated to this so that downstream can be used for spec chem. But there’s not much downside risk here.

Spec chem is growing well but margins took a small hit in Q4 so I’d recommend waiting until the concall to find out why and what capex plans to speed growth here. However, base looks to be set so not much downside risk here either and by the looks of it an EPS of 70+ for FY22 looks manageable(again, this is pre concall… we LL know more then) which makes this still at ok valuations.

So the main risk at current price is phenol prices falling. If you don’t mind that and would consider averaging down if they do fall then maybe entering now makes sense.

There seems to be a Lollapalooza effect in Deepak right now and if by some chance everything stays as is and dasda/oba prices rise I can see a huge blowout FY22. We LL get a clearer picture into the future tmrw during the concall ie capex plans/debt etc. I’m not comfortable giving a buy/sell decision but I’m hoping the above helps. On a long enough timeline the risks of losing capital here will obviously be a lot lower and overall Deepak looks like it’s stepped into the big leagues very gracefully.

Cheers

Btw technically it’s overbought and high above 50 DMA just incase you look at charts too when entering so keep that in mind.

My understanding was that phenol prices did rise due to global supply chain disruption and will not sustain at the current high prices for long.

The current phenol prices are not sustainable and should not be built into projections to be reasonable. Although the other sections will start firing and should cover the gap.

I may be wrong in my assessment of sustainability of phenol prices.

Yup. This is my working assumption. Phenol could stay elevated in the medium term since the disruption looks like it will last for a bit. But they will cool off. And valuing Deepak with current prices of phenol is asking for trouble. That being said as the disruption cools off and phenol prices fall the likes of dasda/oba etc could start contributing too and cushion the fall since they are at unsustainably low levels and stayed there due to covid and will recover at some point.

Also how quickly they grow specialty chem remains a key monitorable since until it contributes a steady 50 percent to PAT there is always a cyclical risk with the other segments affecting overall bottom line.

Invested since lower levels and haven’t added since myself since I don’t see this cyclicality risk being neutralised until that happens and I will trust high valuations from the market only then… but I am bullish.

However, Deepak nitrites managers are like world class jugglers and I’d never bet against them. They somehow time all of the cyclicality of these different streams to near perfection and somehow manage to find sustainable growth where they really shouldn’t and I won’t be surprised if their mcap doubles even before contribution of specialty chem does.

Hey, i just saw results of Tata consumer and its latest dividend announcement of rs 4.05 per share and it reminded me of our above conversation…

Last year it’s dividend was 2.27 per share…so dividend rose 50% in an year…I am aware such a big jump every year may not be possible but see the yield of someone who bought a solid FMCG from house of Tata just couple year back at rs 150 or so would come today at 2.7% and I expect over next decade, such companies are very much capable of dividend cagr of 25% plus…the reason being obviously profit growth and subsequently less need of cash to fund growth when big scale is achieved…

Its not a recommendation for Tata consumer or any stock but the idea to look for solid stable businesses which can compund their dividend at amazing rates and also enable you to let them hold them by virtue of their simple, stable and ethical franchisees…

Cheers @Investor_No_1 . I agree.

However, the reason I’ve gone with high yield options like REITs/ITC etc for my wife’s portfolio especially is that the extra source of income today helps in removing a lot of tension from running our own businesses.

Our aim is to ensure that in 5 to 10 years our portfolio yield will cover all our business expenses and we can then run our businesses for free without worrying about covid type events.

If we had a fixed source of income like a salary then I’d prefer sitting with a good growing company today that would inevitably pay good dividends when they reach SSGR levels with free cash flow to spend on dividends years down the line.

Anyway we get the best of both worlds now since our portfolios our split the way they are and she has the yield strategy and I have the growth + yield later strategy in place.

The IDFC first bank result has divided a lot of investors. For me it’s one of my favorite results of result season as an investor in the bank and here’s why:

It’s pretty obvious now that growth isn’t going to kick in for a few quarters or may be even a year. The current situation across India means they are going to spend more time provisioning and trying to decrease costs due to their recent expansion and growth and profits will just be a token amount for the foreseeable.

So why do I like the result? It means I have a lot more time than I initially thought to build a position here and i don’t need to rush to get my entire position in one go. There is a very high chance I may get to accumulate it closer to book value than 2X book value too.

As far as the bank is concerned they are in a nice position with casa and adequacy at optimal rates so there isn’t an existential fear here anymore. Personally I’m expecting it to trade between 1 to 1.5 X or atleast stay under 2x book value for the next few quarters. I don’t think il ever see it under rs. 30 again and I don’t think it will cross 2X book value until they stop fire fighting (provisions, npas, covid 2nd wave) so I’m expecting a long consolidation period now especially since it has its IPO resistance between 70 to 80 and I don’t mind paying upto that amount for when it’s cleared it’s balance sheet and can start growing again and once the second wave goes away.

I had aggressively bought a lot of shares when it fell to rs. 50 recently. Today I booked a nice profit from 75 percent of my holdings and will slowly add them back in(and more) over the next few quarters at hopefully a price closer to book value or atleast below my earlier buying price. Its a win win situation for me…

If it runs up in price even in current state then it’s good for my existing holdings

If it falls I won’t lose much since I’ve booked some profits and I get to re-enter at lower prices

If it consolidates then atleast my cash won’t be tied up and the cash freed can be used to survive this covid period for my business(which again looks worrying)

Basically I sleep well in all of the above situations

(now watch the market raise it’s price to rs. 80+ in this next quarter alone lol)

Haha @rshankv . We always seem to be on similar wavelengths. I think there’ll be a lot of financial bargains thrown at us over the next few quarters if the situation doesn’t improve drastically regards covid soon. I wouldn’t be opposed to adding Bandhan Bank at 2 to 2.5X book value if I get a chance either so having cash ready for the chance of something of good value coming up in financials seem a good idea.

I’ve stayed away from them for a year and curtailed my fomo without jumping on so I have the patience to wait a little longer and get clear visibility.

Btw @rshankv some crazy movements of late happening in expleo and saksoft. I have no regrets though since studying them was good practice for the future lol. Expleo in particular continues to overperform. Once I’ve reached a certain target I’ve kept with my current portfolio and Investment strategy for a few years il start investing into riskier bets like those in the future. Right now Il continue sticking to 5000+ mcap companies