Cheers. I ended up skipping Acrysil. The upper circuits made me paranoid. Had a chance around 250 but since I missed it I might as well wait a few quarters/years instead of risking it now. Had a choice between Apollo tricoat and Acrysil as my construction Proxy bet and I’m well chuffed I went with Apollo tricoat. Few days later the merger with apl Apollo was announced and now I have inadvertently got an arbitration bet and will soon have shares in the much safer and bigger Apl Apollo with tricoat as a growth driver …

IDA my conviction grows Day by Day. Currently takes up 3 percent of my portfolio but I’m tempted to go ahead and double my holding soon. Next few years are going to be fantastic

That’s a non event based on latest concall and was one of the reasons I waited. Indiamart has no basis for any claims and hence why JDmart could launch. They have launched a counter suit against indiamart for certain infringements etc. Non event for both parties by the looks of it. Settlement date is mid April. It’s just a formality waiting for that though.

Do you track indiamart too ? Did any analyst ask them about this case, what was their response.

Also, sorry if I am asking too many questions asI don’t track both of them.

Disc: Had bought JD at 360 and got out at 650. (interested due to no B2B competitor and this could be a good opportunity since market has room for more.

Don’t track indiamart. I had a look at it and ignored it around 2000. The value of low capex , high free cash platform companies hit me too late unfortunately. I have tried the product and spoken to customers as part of my competition research for just dial and I must say most I’ve spoken to(in total 7 friends who have their own businesses) prefer the UI of just dial and would have no issues switching when JD has the right number of customers. They are currently with indiamart just cause there hasn’t been a better option(i personally too have used indiamart once for my business and found the UI cheap and I dint really get the products I wanted)

Regards the case, analysts did ask about the case in the recent just dial concall. They said indiamart have no grounds for their infringement case. Could sense that there’s no love lost between the two companies… Infact just dial filed a counter suit against them. Mid April should be the verdict of this non event.

The very fact indiamart had to resort to this means they are worried… but that’s just me speculating. JD also said that the b2b space is big enough for a few competitors. Nothing against indiamart… but the fact JD have managed to compete ably with the monolith that is Google In what should have been a dead end business shows makes me not worried at all about the competition in the b2b space considering there is a huge runway for growth.

The only threat i see is If someone like Google or Amazon does destroy this space in the future… though I’d be more comfortable having paid for valuations in teens rather than in the 90s in this scenario.

In short, I am more excited about the possibility of just dial eating and gaining market share in this space (which even now isn’t being priced in) over the next few years than hope that indiamart holds on to and grows at 30+ percent every years and doesn’t lose market share at current valuations.

Also just dial already has a core business that can act as a cash cow and has 1500 crore in cash so they can make inorganic acquisitions too(management said they are looking) so they are in a similar boat regards indiamart regards a cash cow plus potential acquisitions. Market seems to have not considered this too at current valuations. Can see lots of triggers here over the next few years.

Disc: had entered JD at 360 and sold at 650( 5-6 month period holding) . currently watching.( I am not a fan of B2B businesses but if they start taking market share, hopefully will be able to ride a ship similar to indiamart)

IndiaMart alleging that the hyperlocal search engine was infringing on its intellectual property rights (IPR) with its yet-to-be-launched service .

The temporary restrictions was put till enquiry commissioners conduct an investigation and submit their findings,”

If anything wrong was found they would have put Perpetual/Permanent Injunction on JD mart launch, which didn’t happened.

So as a lawyer with my limited knowledge in IPR , I feel nothing much to think of it . Even JD has filed a counter case on IndiaMart indulging in illegal activities , such as copying data cyber theft and cybersquatting.

The only trigger which none of us could see and which came is the Tata’s dialing JD Seems you got a Midas touch.

I knew that with right investments behind JD can take the fight on with Indiamart…but never expected the Tatas to pitch in.

Seems another opportunity lost for me as I missed it…nevermind…good news is the market is so full of opportunities you never know from where they come…and go

Haha @Investor_No_1 . That’s fantastic news. The good thing about a company that noone expects much off and is at throwaway valuations is that the triggers just keep on coming and the downside is capped. Especially when it’s a company in this space without capex etc.

Another trigger is JD sponsoring the IPL. Shows how serious they are and proves they are walking the talk after the recent concall.

Did not see Tatas coming… but considering the low valuations , high cash in hand and high prospects for their B2B business I did hope that some PE investors would get on board(infact my initial thesis in the JD thread was about how we ourselves should look at it as if we are PE investors looking at a tech company with loads of potential).

This Tata news though is out of this world. I wouldn’t say it’s too late to get in even now.

Il be averaging up for a couple months/years now though I’m glad I have a throwaway anchor price since I wouldn’t be surprised if it makes up 5 percent of my portfolio in 2-3 years even without me adding more to my initial 1+ percent (already at around 2 percent now)

@Patrioticindian I’m slowly coming around to your thoughts on Borosil renewables. Fantastic company. Fantastic management. Huge scope for growth…

but there is one fatal flaw: Solar glass prices. China looks like they may kill the entire solar glass market with their increase in supply. So while Bororenew looks fantastic on paper… they may be making 950 TPD of something with no margins in FY23. I’ve gotten a bit wary about it now and i fear I maybe caught in a commodity at the peak of its cycle. I’ve only done 2 tranches so far and usually in a drop like today I would have aimed to add another one. However, Considering the risks involved and that current valuations are factoring some sort of ADD / china not increasing supply(which they certainly are doing) I’ve put it in the don’t buy more don’t sell category for now.

Edit: looks like those fears don’t need to be worried about now regards Bororenew https://m.timesofindia.com/business/india-business/india-to-levy-import-tax-on-solar-modules-cells-from-april-2022-report/amp_articleshow/81435511.cms

@Malkd in my view ie. in the shorterm Borosil might do well with the news flow like import duty but in the long the entire renewable value chain is so far not economically viable without govt.subsidies.Which is visible in their return ratios.I don’t want to take chance again (as it happened to me in Suzlon many years back). Unlike api/speciality there is no stickiness in the business with their clients ,as they are squezed a lot in their tenders.More over If the import duty is high enough it will invite competition as there are no entry barriers unlike in api where they have some sort of process chemistry expertise. As I am maintaining a highly concentrated pf Borosil renew doesnt offer wide mos with the present valuation and wild margins. I would also advice caution in many co’s , not to extrapolate the last quarter margins which may be due to supply chain issues or pent up demand due to covid. Also I notice a sharp drop in the promoter shp of 9% in the last qtr.

The drop in the promoters holdings could be due to the QIP that the company undertook some time back. Don’t think the promoters have sold any stake in the last few quarters.

@Malkd Hi, I got interested in OFSS after reading your thread and did a preliminary study. I have observed a few things and I would like to get your views on the same.

What will be the impact on OFSS customer base when many companies switch to cloud.

2 The Cashflow is growing at about 6%. With such low growth rate, the intrinsic value using DCF is working out much lower. Have I missed the bus when it was available at lower prices?

What is your investment rationale ? Is it pure Dividend play? i.e. you do not mind if the growth rate is low.

Disclosure: Not invested. Not a SEBI registed Advisor.

@Ramanathan_Narasimha

Since OFSS don’t conduct concalls information is scarce. However, based on reports elsewhere they are moving into the cloud already so switching shouldn’t be an issue.

Personally I added in bulk when it was below rs. 3000 since the risk reward seems favorable in that range since dividend of 6+ provides a good cushion. The tailwinds in BFSI digitisation sector should allow for some good growth here however my primary aim with ofss is capital protection and dividend yield. Over the long run considering cash in hand and cash generated yield should stay at 6+ levels(there will be poor yield years and huge bonus years too) and I’m hoping that growth is high single digits atleast(with a chance of a re rating considering low valuations and tailwinds). It’s a safe dividend play for me with potential for growth and re rating alongside ITC and Rites.

For growth in the IT Bfsi space I also own Intellect Design Arena and Expleo where I’m expecting my growth plays in this space to play out. I don’t own and trust leveraged institutes like banks(I trust them near book value and not higher so this is difficult to get) so owning these 3 in the bfsi space is my indirect play at banking too.

@Patrioticindian I think Harshad is right. You are referring to the QIP. Regarding margins, I don’t mind them falling as long as they don’t crash to Suzlon esque levels… and the recent government announcements give me some comfort. Solar energy is here to stay too… while wind energy is iffy(I believe at Suzlons peak valuations they needed a windmill everywhere on planet earth to justify it… atleast I think I read that somewhere). Imo borosil Renewables is actually cheap. Even if margins get hit they should clock 100 crores over the next year(25 per quarter) and about 200+ crores in FY 23 when expansion and operating leverage comes into play. And after that the sky is the limit if government continues to be favourable since the demand will allow even a few competitors to come in without causing too much market share issue(as long as china is kept out)… and this while solar is in a nascent cycle. It is currently valuated considering the past 4 quarters where they had one furnace running, contingent expenses etc.

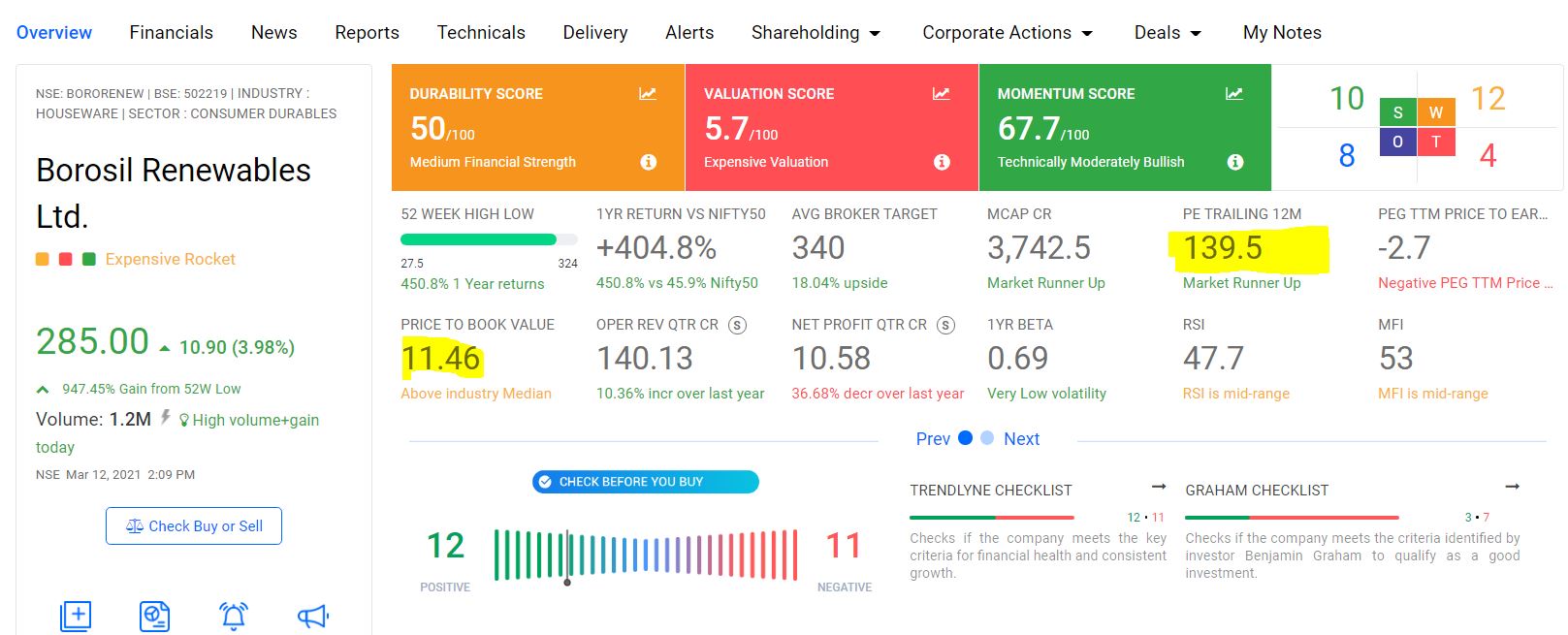

Wondering how is BorosilRen cheap with a PE of 139?, even if they double their business by expanding capacity and the margins are intact , still I believe it is way to expensive, please correct me if i have missed anything here.

@rshankv. They did 27 crores over last 4 quarters combined. They should hit 27+ crores every quarter from now on in if nothing crazy regards solar glass margins happens.

So the valuations will drop to 30’s in 4 quarters(if margins intact) which while not cheap isn’t as crazy as the current valuations when looked at with context. and post that double capacity in FY 23 means the valuations will drop to teens.

As things stand this looks very possible today since with the latest government policy the main risk looks nullified for the medium term. The ball is now in bororenews court and I have faith in the management delivering in the absence of external factors. Recent stock options were offered to their new directors at 274 too so we are probably around fair value even though valuations look crazy at present due to the previous 4 quarters.

That being said I have a margin of safety here and only have 2 out of my planned 5 tranches invested so far and will probably consider adding to my position only if the above plays out upto FY 23.

Note: I have a huge fear of high valuations as demonstrated in my posts throughout this thread. Borosil is the only exception I’ve made because it just makes sense considering what is expected over FY 22 . The latest quarter confirmed the thesis (they had to set aside nearly 19 crores PAT for contingent liabilities which was a one off) that 30 crore run rate per quarter is achievable and the news from the government removed my fears regards margins.

If they do not hit this run rate and margins fall next few quarters then I will consider trimming

i looked at borosil and found it expensive as well atleast compared to other shares ,i picked astec lifescience over it plus at a pe of 30 at FY23 earnings considering everything goes well why not pick alembic with a pe of 10 on FY23 earnings .

@raku FY 22 forward PE would be in 30s. FY 23 would be in teens. Again these are forward looking so who knows what actually happens. Also invested in astec and alembic though all 3 companies over something totally different so I don’t compare their valuations to each other.

Also I dont mind paying up for Borosil due to the ease of tracking. Check solar glass prices, make sure government keeps china and it’s allied producers out, check management commentary for expansion plans, cross check to make sure it’s one product is selling at expected levels. Also, as the benefit of being in a sector which has a long runway of growth in the future and is still in the nascent phase so there could be market frenzy allowing higher multiples here too.

…

… many years back). Unlike api/speciality there is no stickiness in the business with their clients ,as they are squezed a lot in their tenders.More over If the import duty is high enough it will invite competition as there are no entry barriers unlike in api where they have some sort of process chemistry expertise. As I am maintaining a highly concentrated pf Borosil renew doesnt offer wide mos with the present valuation and wild margins. I would also advice caution in many co’s , not to extrapolate the last quarter margins which may be due to supply chain issues or pent up demand due to covid. Also I notice a sharp drop in the promoter shp of 9% in the last qtr.

many years back). Unlike api/speciality there is no stickiness in the business with their clients ,as they are squezed a lot in their tenders.More over If the import duty is high enough it will invite competition as there are no entry barriers unlike in api where they have some sort of process chemistry expertise. As I am maintaining a highly concentrated pf Borosil renew doesnt offer wide mos with the present valuation and wild margins. I would also advice caution in many co’s , not to extrapolate the last quarter margins which may be due to supply chain issues or pent up demand due to covid. Also I notice a sharp drop in the promoter shp of 9% in the last qtr.