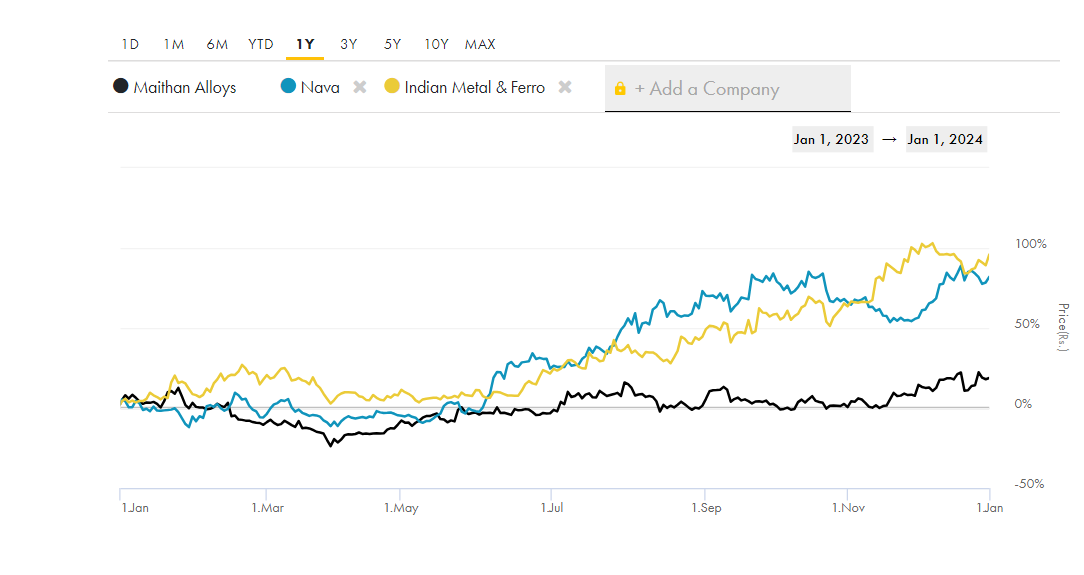

I am trying to infer why market is not valuing Maithan Alloys, but its peers are appropriately valued. Am I missing something?

1 Like

projected numbers are on weaker side

IMFA is Ferro chrome business which has completely different demand supply dynamics than Maithan alloys which is in Silico manganese ferro alloys. Currently, ferro chrome alloy prices are at a good level since last 2 quarters and sustaining now also… whereas silico manganese alloy prices have been soft for quite a while now.

Nava’s main business is power generation with them also recieving their long term receivables from Zambia govenment (Stock specific trigger)

5 Likes

Buying NSE in pre-IPO can still be understood as parking short term funds, since NSE is soon coming with an IPO and surely given its monopolistic nature, the listing would be at a premium.

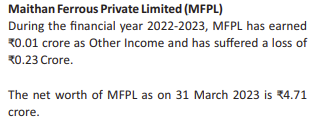

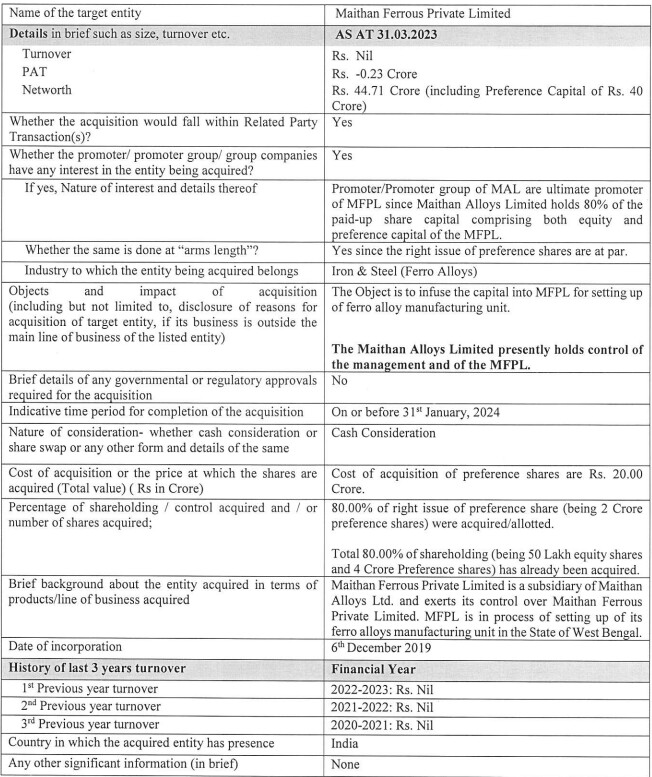

But why put 40Cr in a firm which you already hold 80% of and has not produced any revenue for the last 3 years, and has a networth of only 4.71Cr!!

Mining is still not a straight forward and easy business to understand it seems…

From Last year’s Annual Report

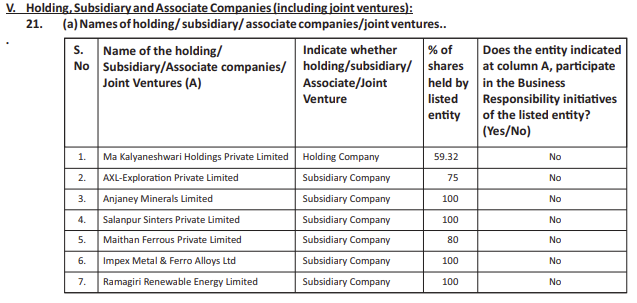

I believe this is the ferro chrome plant subsidiary - since they are setting up a new plant - ofc they will need to infuse capital into it

Sure you are right. I guess i am not clear why do these firms need to have so many subsidiaries…

Is it due to tax incentives offered for the govt for SMEs? but since the promotor is a listed firm. ideally these incentives should not apply, and benefits should flow to the real SME players.

Btw how do you view Maithan parking excess cash directly into stocks; https://x.com/itsTarH/status/1737862856467734950?s=20

wont it be better if they held in liquid funds to be invested in any distress asset sale related to the primary business itself!

See in my view that cash or at least a majority of it, should have been given out to the shareholders way back in the form of buyback or dividend but it would seem that the promoter intent is not there to share cash with the shareholders - I see that as them not being aligned with the minority shareholders but ofc it is upto you how you want to judge the same.

Disc. - Used to be invested, not anymore

1 Like

Thanks but dont you think by returning excess cash to shareholders in cyclical industries where one can get bargain buys at times is you miss those big buy opportunities.

I am all for Maithan to retain the excess cash but just not comfortable with equity purchase specially when markets are elevated as currently…

First, I dont believe, you will ever need 2,000cr for stress buys - second, I wouldn’t want my company to do so many acquisitions at once and make a fool of themselves when they can’t integrate most of those stress buys into their model

1 Like

Maithan is planning to buy shares of National Stock Exchange of lndia Limited for 105cr.

I just feel management wants to do their own investments with company’s cash. Good management ideally distribute the cash instead of this kind of irrelevant investments (though it may not be a bad investment).

Disclaimer: Just tracking now… Exited few years back

1 Like

The company is holding Rs. 660/- worth of investment, bank balance and cash. The stock price is Rs. 1111/-. Nil Debt, Good earning, good margin, good management, in short all good parameters Why isnt the stock moving. Something amiss.

1 Like

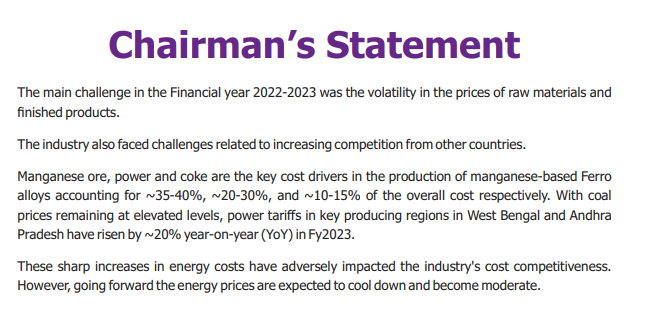

As per my understanding, the margins, earnings are cyclical, linked to steel industry. Currently, steel prices are depressed due to imported steel being cheaper, so while India is producing lots of steel, prices are dictated by imported steel which is lower than Indian prices.

The costs (i.e raw materials, power costs, etc.) cannot be passed on to the customers, because the customers dont get the prices (for steel) they want. Also there is overcapacity in ferro alloys segment. So no pricing power.

The company bought IMPEX as a distressed sale, but soon shut down the plant as it was unviable to continue the operations. The company is also planning a greenfield capacity, which I believe is going slow, and they have decided to halve the capacity from what was originally planned.

The company has lots of cash/investments on its books, and they refuse to give that to the shareholders citing needs for acquisition. sometime ago they said they will take a decision in 12 months, but I guess those 12 months are long gone.

In the 3 quarters of this FY, their other income is more than the core operating profit. With nil debt and such a low depreciation, it looks like a steal with the Other Income and the investment/cash on books.

I also got interested in the company and was very keen to invest, but havent.

Disc: invested very small amount.

3 Likes

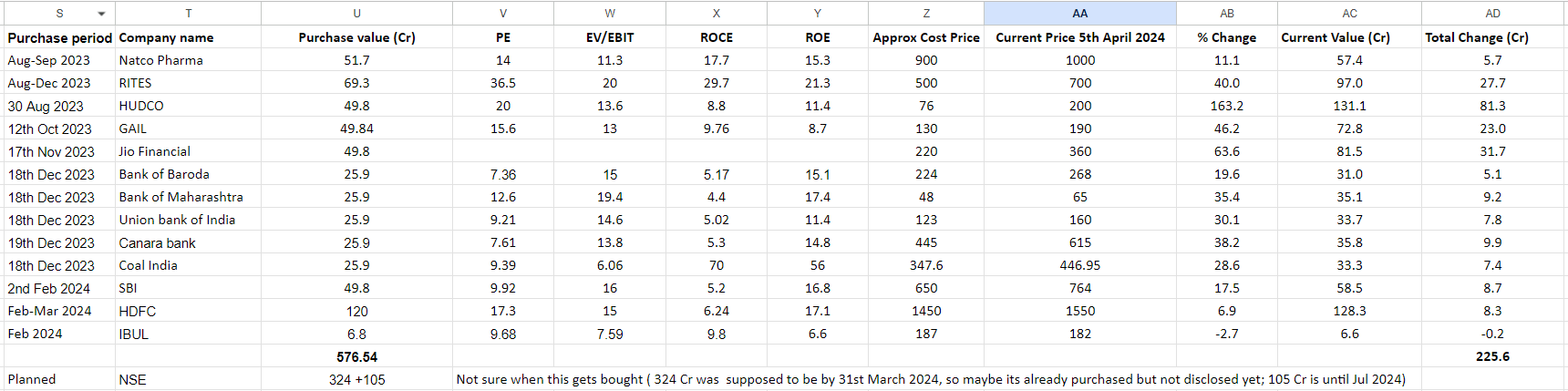

These guys are really killing it with their equity investments. They have invested abour 564 Cr over the last 8 months or so (Excluding the investment into NSE) and they have had about 50% absolute returns so far, excluding dividends.

I think the last quarterly report only showed the income statement. I wonder if the equity investments is really getting priced in. Does anyone know if the book value on screener etc would be adjusting for the equity investment gains? If not, I expect a nice pop when the balance sheet does get disclosed.

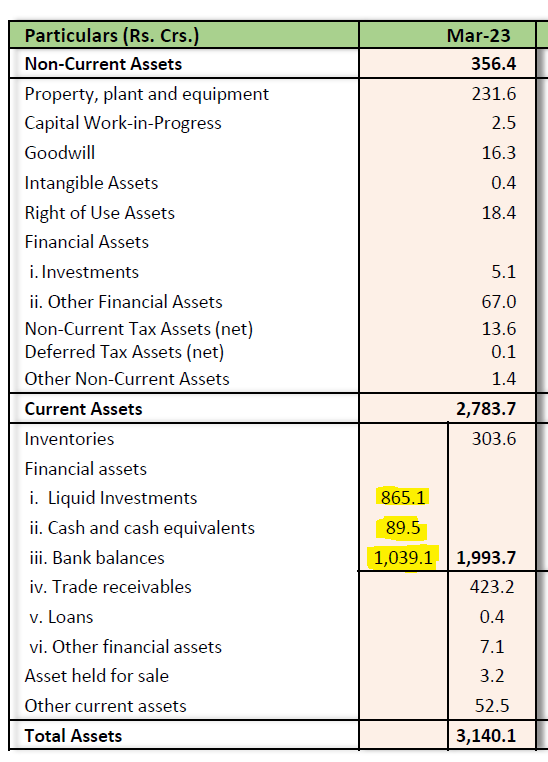

This is the last balance sheet from 31st March 2023:

Add about 250 Cr of earnings over th last 4 quarters to the current assets of 1993 Cr, 225 Cr of equity gains, at least 30-40 Cr in interest on bank deposits, and you get to 2500 Cr of just cash + equity.

3 Likes

Based on the Sept’23 consol B/S, the investments stood at 1389Cr, Bank Bal+Cash was at 748Cr (total 2137Cr). The total equity investments declared between from Dec’23 to Mar’24 were 983Cr (including 429Cr in NSE). There was trade receivables of 288Cr. So I expect that cash+investments should be more than 2500Cr as on Mar’24.

Disc: tracking position

Can you plese point me to where I can get the Sept’23 consol B/S? Its not in there in their disclosures.

Screener.

Below link if you wanna take a look at the detailed info.

https://www.bseindia.com/xml-data/corpfiling/AttachHis/4f6e18b3-64af-4a39-990c-4ed5f8da0e5f.pdf

1 Like

Maithan Alloys bought a total of 17,54,196 shares of MOIL on 23 and 24 April. MOIL is trading at All Time High and all valuation parameters, be it PE. EV/EBITDA and PB is much higher than their respective 5Y mean numbers. Since Maithan understands Manganese, I suppose they know better. I took a tracking position in Maithan Alloys recently betting on their investments but after seeing their investment in MOIL, perhaps we can expect the company’s core business also do well.

3 Likes

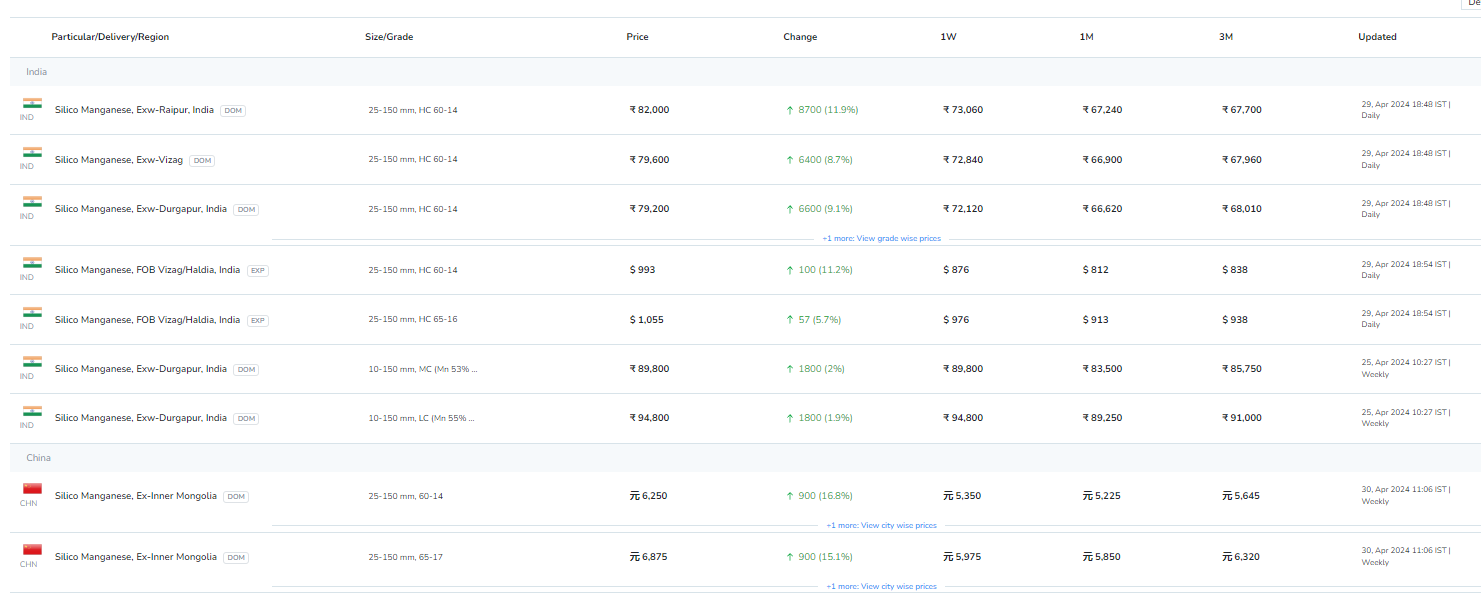

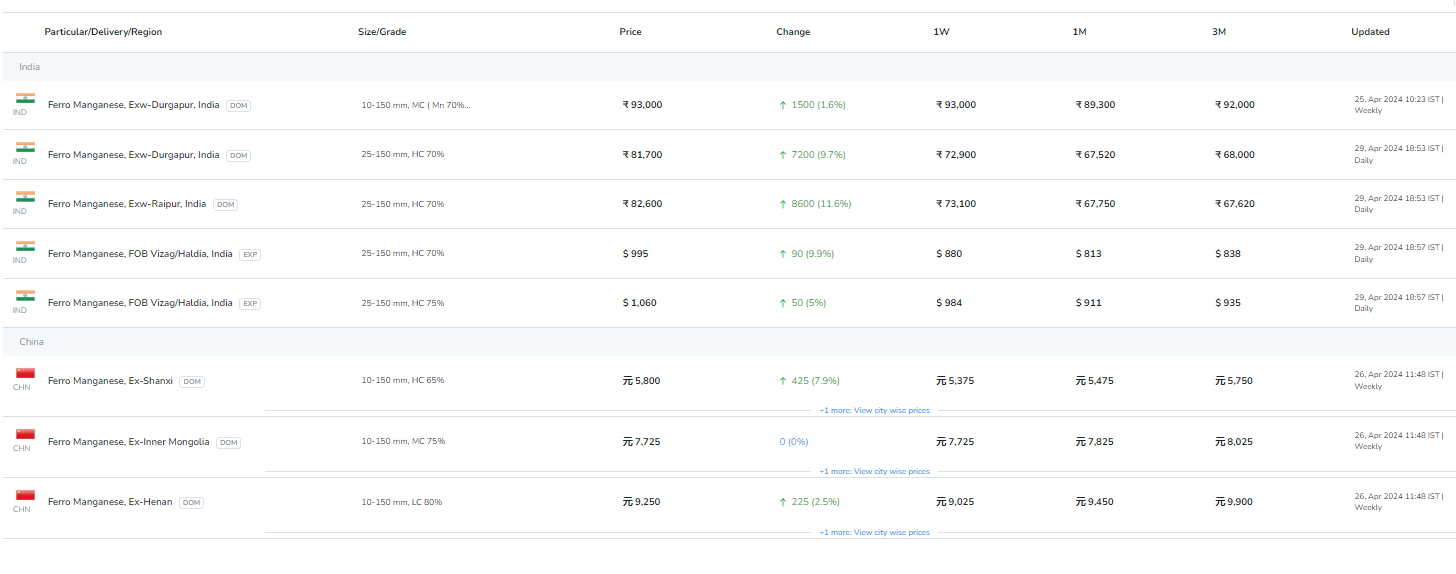

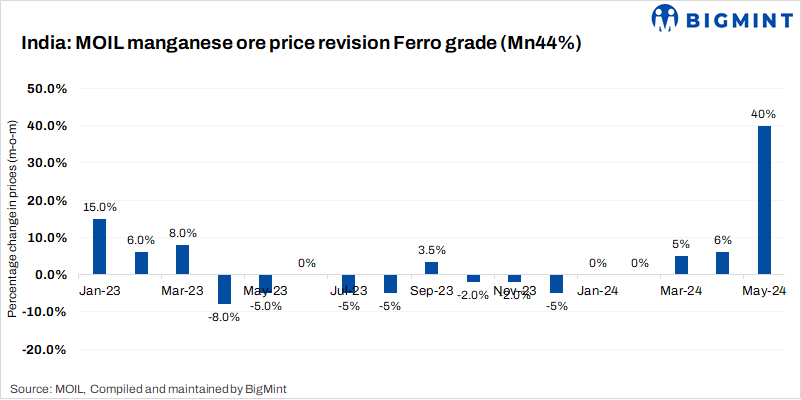

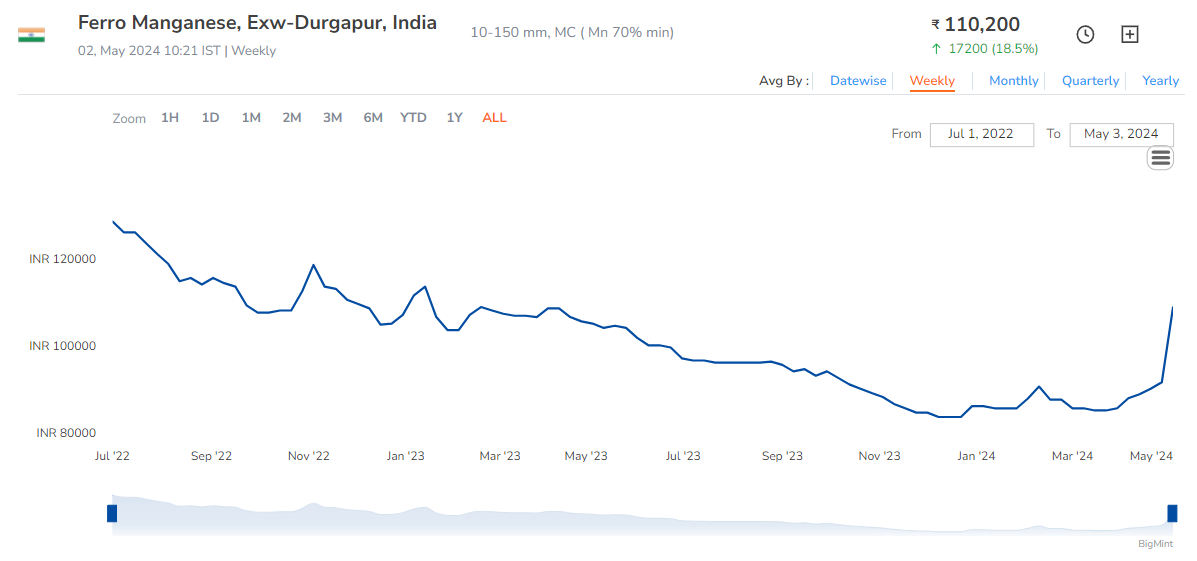

Manganese ore prices have increased dramatically post the news of suspension at South 32’s GEMCO unit. Manganese alloy prices have followed. The ferro alloys industry in India has been facing severe headwinds the past few years - could this help turn it around a little?

Disc: Invested

6 Likes

Maithan had around INR 750 crores of Cash as on 30-Sep-24. One would assume that since Maithan is buying MOIL shares, they would have been bullish on Manganese ore and would have also bought Manganese Ore which is a key raw material- As per their Annual report ores constitute around 40% of RMC. But it is unlikely that they have very high inventory of ores as they have used around INR 600+ crores of cash from September to March to buy Equity shares of NSE, MOIL, HDFC, SBI, Rites etc. In short term it is positive as the inventory gets repriced, however in long term it is not a very big positive as Manganese ore is RM for them.

2 Likes