From the article, how did you deduce that the project got cancelled? Won’t they start when the approval goes through - which might have gotten delayed.

Disc - I’m also holding sizable position in Maithan Alloys and the power cut in no way affects it’s long term performance of the company.

Does someone have an idea on the impact of export duty on steel products on Maithan? Its not clear to me if export duty is applicable to Ferro-alloys as well? From the news, it doesn’t seem so but any expert comments?

Disc : Invested and closely watching. Views my be biased.

Can anyone please explain their rationale of acquiring Ramagiri Renewable Energy Limited? I did not find any mentions in their Annual Report’21. They have uploaded a scanned copy for Annual Report’22 so its very difficult to look for anything there. They recently switched off one of the furnaces at Impex Metal & Fero Alloys Limited owing to steep rise in power cost. So is there any relationship between these two events. I understand RREL has wind and solar power generators. Would they be able to offset the rise in the power cost in long run. Are they trying to move towards renewable energy as backward integration or entirely different business line?

Hi pranav, in general this is the problem with these small caps. When They are doing great, they will come with all the rosy investor presentations, but when not doing so good, no investor presentation. And Forget the concalls altogether.

So the options available for us retail investors are

Call the Investor Relations / company secretary and find the information.

Go through the credit report by rating agencies and find the answers

Last and best is to follow some industry expert on social media / do on ground scuttlebutt if possible.

I have burnt my hands (lost 40%) in such a small cap pharma company. Nice investor presentations in 2021 and then just nothing. Didn’t get any proper answers from company secretary and dont have the connection / time to do the ground scuttlebut.

So maybe avoid altogether or give small allocation in your portfolio.

Even I agree with you on the aspect that in many such small caps there would be developments we are not aware of .Even I have seen this happen in a couple of my investments,. The only reason I still try to add one or two in my portfolio is the greed/ hope that the returns of a success is outsized in these investments.

considering power cost is one of the major expenses, the rationale for the investment must be to curb that. Albeit not much information has been provided but that is the only thing that makes sense

IMFA is to be closed down completely due to rising power costs. Does anyone have any insights into the trend of power tariffs in AP?

Although this rise in power costs could be a blessing in disguise I believe, considering the fact that if there are leveraged players in the sector, they will have a hard time and finally the cash can be put to some use

Maithan Alloys Ltd (MAITHANALL) manufacture and export value-added Manganese alloys namely - Silico manganese, Ferro manganese, and Ferro Silicon alloys. MAITHANALL is a key supplier to reputable steel companies such as JSW, SAIL, JSL domestically and POSCO, Hyundai Steel overseas to name a few. For context, ~1.5% of Manganese alloy is required to produce one ton of steel. As MAITHANALL depends on the steel industry, we can expect cyclic behavior due to volatility in raw material and finished goods prices. MAITHANALL strives to differentiate itself from its competitors by being the lowest-cost supplier to steel companies.

Positives:

The company has received a CRISIL AA/Stable and CRISIL A1+ ratings for its long term and short-term ratings respectively

The company is witnessing steady sales growth with healthy net profit margins (though dependent on steel cycles which impact the raw material prices)

The stock is trading at an attractive price (P/E as on 11th May is 3.85) with the debt-to-equity ratio almost zero. The PEG ratio is also low (0.11), indicating that the company is undervalued currently. The price-to-sales ratio is 0.87 increasing the stock’s attractiveness. The current ratio is a healthy 5.70.

The management is focused on a single business segment – “Ferroalloys”. If we look at “Cash from Investing activity” section, it is evident that the company does some commodity trading. But since it is a common practice by all commodity companies, I am ready to give the benefit of the doubt to MAITHANALL as they must be knowing the industry cycles and are planning to utilize that.

The Joel Greenblatt metrics – ROCE and the earnings yield – have been healthy – 54.9% and 41.9% respectively. MAITHANALL has efficiently allocated capital over the years as can be seen from their healthy ROCE numbers.

The company’s net cash flow turned positive in Mar 2022 (70 crores) after a negative cash flow the previous year. Since the company has zero debt and significant cash reserves, the company is able to sustain crises well on its own. The retained earnings

The succession plan is clearly sorted in this company and there seem to be no red flags against the promoter family.

The management is able to execute projects (CAPEX expansions) as per their previously committed timelines.

The business model of MAITHANALL is relatively asset-light. The company has a CAPEX of 2888 crores and has generated sales of 17039 crores in the same period of March 2011 to March 2022. This is also highlighted in one of their annual reports saying that MAITHANALL doesn’t want to backward integrate, meaning they don’t want to invest in mining rights. They would rather buy Manganese ore instead of mining it.

The promoter shareholding has been almost constant over the past two years.

Out of their three manufacturing plants, their two big plants at Kalyaneshwari & Visakhapatnam import 65% and 90% of their raw materials. This is a huge risk for a commodity company. (Source: Investor presentations)

Their cumulative cash flow from the operations is much less than their cumulative PAT over the last 10 years. This indicates that MAITHANALL is finding it difficult to convert its profits to cash. Maybe the cash is struck in inventory and with debtors. So, I checked the data, and it aligns with this hypothesis. The cash conversion cycle and the working capital days are increasing. Established and powerful buyers will obviously have more power during negotiations, which is shown in these numbers. I still think it has not reached a panicky situation but as an investor, we have to be cautious and always keep a check on the inventories as well as the cash flow from the upcoming quarters.

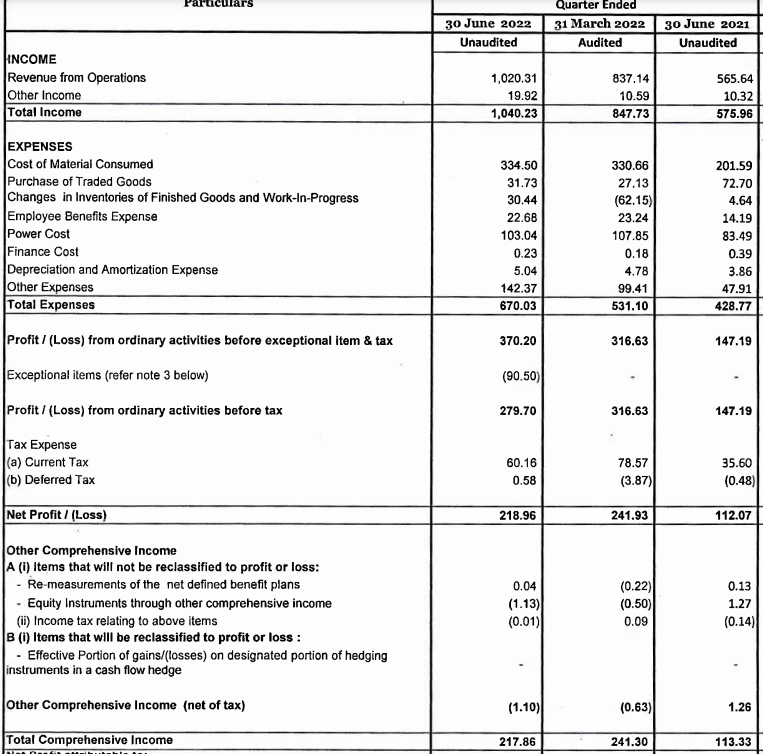

The cost of materials consumed and purchase of traded goods amount to 40% of sales in FY21-22 (This was 51% in FY20-21). Another important aspect is the power cost which was 12.4% of sales in FY21-22 (This was 20% in FY20-21). The company’s operating margin depends on the power cost significantly. That’s why in 2017 and 2018, when there was a power subsidy, it benefited the company as mentioned in those year’s annual reports. Power costs and issues associated with this is a concerning topic for the investor (Sometimes on the good side and sometime on the bad side). The Oct-Dec Q3, 2022 report mentions that the company has gone for an appeal of 90.5 crore which represents the arrear electricity charges pertaining to earlier years on account of increase in power tariff notified by concerned authorities. For further details about the power cost, one can refer to Note 36 (Pg 197) of annual report, FY 21-22. In other words, power costs are an important external factor that significantly impacts the profitability of MAITHANALL.

Same is the case with the price of raw material costs. This is one more external factor that will significantly impact on the OPM of MAITHANALL.

If the big steel companies become too fixated on keeping their input costs as low as possible, their vendors like MAITHANALL would have to shrink their margins. This has happened in the past and this is an inherent risk that an investor should be aware of.

During FY21-22, inventories increased by 74.5% more than FY20-21. Raw material inventories amount to 502.11 crores and finished good inventories amount to 87.05 crores. This is the place where the company can improve a lot.

There is an item called “Others” under Note 29 – “Other current liabilities” section of the annual report which has around 61.6 crores. There are no details provided anywhere. This item is a constant in all the company’s annual reports.

Overall Verdict:

MAITHANALL, a fundamentally strong company, and a clean management is available at attractive valuations now. Since it heavily depends on the steel industry, if we are able to time the entry and exit, we are looking at a multi-bagger (Holding time frame: 2-3 years from now) in my opinion.

Good overall analysis. A few things I would point out

Yes their ROCE is high but they have a lot of cash lying around with no plan to disburse it to the shareholders, so essentially this metric is skewed. Gives a good representation of the business’s ability to give returns but overall, without much reinvestment possible right now, it would be better to look at this metric after adding cash cause essentially it is employed in the business if not given to shareholders

Connected to the above only, and your point on Investing activity and trading. I believe they do not trade. The investments purchased and sold are Arbitrage funds where the huge amount of cash is invested. I believe (and hope) they are not trading. Albeit they do trade a little (below 10% of the revenue I believe) hence they provide a metric termed Manufacturing EBITDA etc. and also have some expenses coming from traded goods. If you’ll go through the reports, you are sure to see a few lines on how they do not keep open positions and do not speculate

Also the valuation metrics are skewed too due to the upcycle by steel and greater realisations by the company. The market knows that this is a one time thing and prices it accordingly. If you will check, the steel prices have actually started to come down and ore prices have started to increase, one of the reasons why 2023 will be degrowth.

One more equity investment. Now its National stock exchange… NSE

I have written to them about why they are doing direct equity investments and why they think its a better capital allocation strategy wrt to Dividends or Buybacks. Yet to hear from them!!!

The one positive I can see is that the companies they are investing in are good and the valuations are relatively reasonable.

But at the same time it seems like they are investing due to fomo. As if they wake up and realised that this 1000 cr of cash would have grown 1.5x in last 1-1.5 year (counting from time when the financial health of company was good after 2 years from COVID). Bad times come after good times in stock market. I hope they don’t overdo the investments.