Maithan Alloys FY22 Q2 result is out.

Q2 Sales at 673cr vs 413cr last year

Q2 Profit at 165cr vs 54cr last year

This is the best quarter in Maithan’s history. Its greatly benefiting from current commodity cycle and may be at the peak.

Maithan Alloys FY22 Q2 result is out.

Q2 Sales at 673cr vs 413cr last year

Q2 Profit at 165cr vs 54cr last year

This is the best quarter in Maithan’s history. Its greatly benefiting from current commodity cycle and may be at the peak.

Inspite of record profits, why has the cash flow from operations fallen YoY ?

Primarily driven by receivables increased. Given that steel is doing extremely well – why will receivables increase so much! This is the key question @akash_1cr and I have…

Loans worth 127 cr shown under current asset (which is shown as increase in receivables) + 32 cr addn in inventories… Am I missing anything?

Yes… The increase is due to current asset (loan) of ~Rs. 100 cr due to which cash flow is negative

2 do anyone has any idea whom this loan is to. Was there something planned?? Hope it’s not related party loan.

Thanks

Had posed the same question to the management.

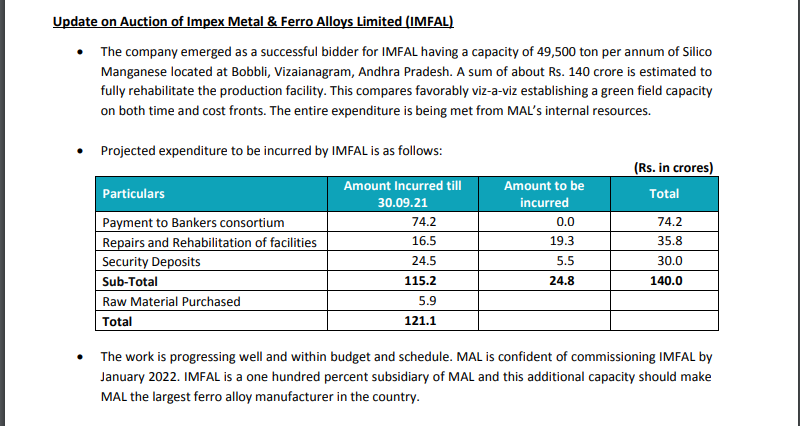

They replied that this amount has been infused into Impex Alloys

Hopefully this clarifies the increase in Loan amount

On a side note, really appreciate the management in answering questions of a common shareholder.

IMO presently maithan is operating in full capacity, no volume increase expected in next 5 months…revenue increase will depend on the market price of product… How much added revenue do you expect from Impex operations?

From the only concall that the company has conducted, they mentioned the total capacity to be around 240000, with ~50k added, ~20% added revenue could be expected, Interesting to see and note would be how promoters would be utilising the cash that the company is generating each year,

Feel there is not much to loose at the current valuation

Please correct me if I am wrong,

20% added revenue along with strong realizations should boost the operating profit, expecting it to close at 600+ cr. EBITDA for FY22. Good strategy by the company opting for brownfield expansion over greenfield which will result in faster commissioning to tap the strong tailwinds in the current market. Further acquisitions are possible considering it is sitting on a pile of cash.

Any Idea why receivable and Inventory days shot up in 2021? Looking at the past trend the company is degrading in working capital Management.

The company has started the IMFAL operations earlier than planned.

AP govt. imposing power cuts from April, can extend in May as well (50% power cuts across all days impacting ~60% of Maithan’s capacity that will hence operate at 50% for one month at-least

This could dent Maithan Q1FY23 revenue to the tune of at least 20% if not more, but with impex facility coming onboard, expecting not much difference in Q3FY22 and Q1FY23 numbers.

Thoughts ?

Apologies for the typo, meant Q3FY22!

IMPEX should add around 20 to 25% of its revenue/capacity. So agree with your analysis (but the dent in Q1FY23 could be as low as 10% - multiple 60% x 0.5 x (1/3))

The issue would be regarding margin. Is there a hike in power price and how much reduction in realisation is going to be there when steel market stablizies? Not able to guess/answer this question. Awaiting quarterly result/annual report.

Any idea, what is the status of green field expansion in West Bengal which they announced couple of years back?

That project is shelved long back due to various reasons ,mainly red tape. That is why they went for inorganic growth with Impex Metal.

where did you decipher the reason from ?

Thanks

What is the future growth plans for Maithan? If they don’t come up with organic/inorganic growth in next 2-3 years, again it would start building up huge cash reserves. I couldn’t find any management commentary about future plans after IMPEX acquisition.

Disc : I have position on this stock. Decided to hold,recent power cut by Andhra Electricity board is not a trigger for sell decision for me.