About:

Mahindra & Mahindra Ltd., a mobility products and farm solutions provider, is the flagship Company of the Mahindra Group. They offer a wide range of products and solutions ranging from SUVs to electric vehicles, pickups, commercial vehicles, tractors, two-wheelers, construction equipment.

BUSINESS PRESENCE IN 100+ COUNTRIES WITH 49% REVENUE FROM OUTSIDE INDIA

“It is tempting to see the “group” as a conglomerate, but Mahindra prefers to call it a “federation” where each company is ring-fenced from the damage failure elsewhere can do, even while being free to finance its own growth and make its own mistakes.” Federation outlook of Mr. Mahindra.

Ford JV seems to be a win-win deal though we need to see if it succeeds. Previous automobile JV didn’t work out well for M&M as well as Renault.

Roxor can help M&M gain a foothold and establish the brand in the US auto space. But again, we need to track further product launches of the company in the US w.r.t automobiles.

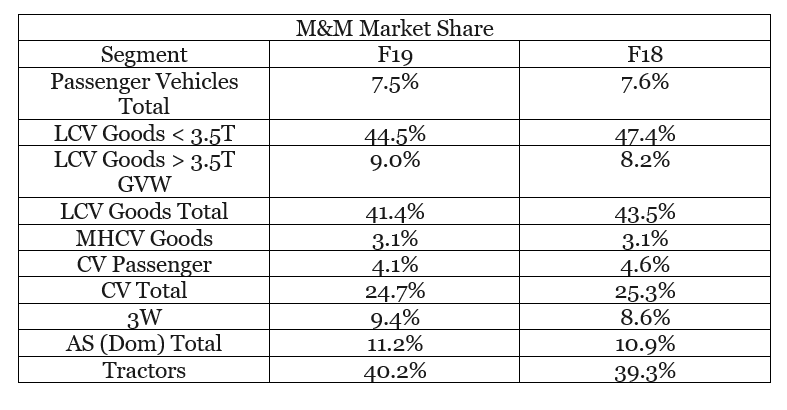

Scorpio & XUV500 were quite successful models. Marazzo seems to be struggling as it competes with Maruti Ertiga. M&M needs to come up with a few competitive models and gain market share. I have lately observed Creta & Venue being preferred by SUV buyers.

With the present government having the intent to increase farmer income, a policy aimed at achieving the same can be a big boost to tractors and farm industry.

Corporate governance is top-notch in my opinion.

Meru acquisition and shared mobility are also part of M&M strategy.

Though sometimes I feel they have spread themselves quite a lot, it can be an issue or not, I am unsure.

Jawa has grabbed customer attention, current waiting time is a problem, going forward this can be reduced with proper mfg operation in place. Two-wheeler space with Jawa models can give a thrust to not so good numbers of M&M 2W.

Specifically on TREO, apparently it is very hard for organized players to get market share it seems. The unorganized players are selling at ~40% price e-rickshaw’s which are unsafe and hence have 85% market share

Overall M&M seems to be in a downward trend and is a good value buy imo

Hey thanks for your inputs! Your point is spot on w.r.t unorganized players, I recently found a company which came into existence in 2015 and is being run by young engineers and entrepreneurs - https://www.croyanceauto.com/about-us.php ; If it’s that easy to make an electric vehicle, makes me wonder what’s the moat (apart from safety)?

With all these doubts, I still feel Auto space is going through temporary rough patch because of BSVI, Trade War & liquidity crunch. M&M is almost debt free, with great management & has appropriate resources. Thus with right strategy and execution, M&M can move up i.e its market price will start catching up with its profits sooner or later.

Comparing with the September 2019 figures, Mahindra sold 4,127 more units of passenger vehicles in October 2019 (September 2019: 14,333), registering a growth of 28.7 percent. Similarly, the SUV sales increased by 3,927 units in October 2019 as compared to September 2019 (13,858 units), registering a growth of 28.3 percent.

I’m using Valuepickr to discover companies with quality management and using DCF to check if a company is undervalued before I use charting to picky my entry points.

I discovered an issue with M&M while I was checking their valuation. Isn’t negative operating cash flow a sign to worry about?

That’s a very valid question, thanks for bringing it forward. From my limited knowledge of financial fundamentals, I’ll try to answer this question. If anyone has better clue about the answer to the given question or any related queries, pls do contribute, it will help everyone.

For Consolidated nos. of ops cash flow, 3 factors i.e Financial Service Receivables, Inventories and Cash used in operations majorly resulted in drawdown which eventually resulted in negative operating cash flow. I’ve tried to relate March’19 nos with the current scenario (news) to make sense of this negative operating number.

a. Financial Services receivables

Customers have become more sticky since competition has reduced after the liquidity crisis. With less competition, the number of customers repaying loans early has reduced. Maybe this could be the reason for increased receivables in cash flow. Why M&m Financial Services’ Steady Performance Didn’t Impress Investors | Mint

b. Inventories

I guess an increase in inventories can be due to quite a few factors right from BSVI transition, increased insurance cost, agricultural distress, liquidity crunch, etc.

Hi @Ryuzaki,

Thank you very much for your input. I’m trying to break into the investment banking industry (I bought two courses on udemy about investment banking and financial analysis) and your post clarifies with more detail about what I thought was going on with M&M.

M&M have been having a wobbly operating cash flow for the past 5 years so while I’m convinced about the dedication of the team of M&M; I’m not sure that they’re in the best of businesses (auto industry may remain shaky until players come up with worthwhile EVs).

Edit:

While it is next to impossible to do a DCF of M&M, I have done a DCF analysis of Ashok Leyland and it shows that Ashok Leyland is slightly over valued at P/E 15 considering its cash flows. M&M and Ashok Leyland may both be worth entering into at a P/E of 12 or less.

SsangYong’s net loss widened in the first quarter of this financial year, making it the 13th consecutive quarter where the company continues to post hefty losses.

Technical analysis:

M&M has recovered quite well from the lows. Though now stock may consolidate going ahead.

On weekly chart looks like bearish harami pattern, 509 is acting as good resistance. Downside, 460 as S1 & 435 S2.

However, if closes above 509, 570 can be seen!

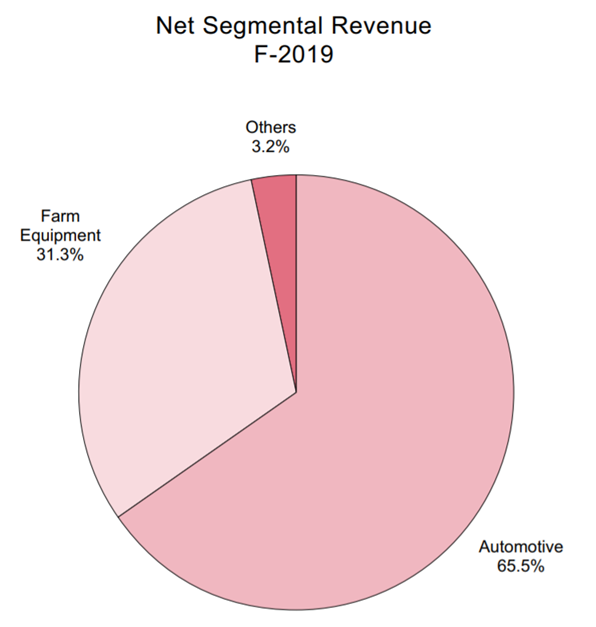

Tractor business is doing well (Management stated that most of its plants are functioning at ~80% utilizations and nearly all its key outlets are operational). Market share grew by 1%. The company is also working with Mitsubishi to launch four new platforms in next one year.

Auto division seems struggling (auto town slowdown) with ~30% utilization levels and ~80% of its retail outlets are now operational, also demand drifting towards gasoline in SUVs. Demand in compact SUVs is drifting towards gasoline SUVs and it also stated that ~50% of its bookings for the XUV300 is for gasoline based vehicles. While for larger SUVs, diesel continues to be a preferred choice.

Liquidity position is decent. The company is at a comfortable Net cash position of ~Rs34bn. It further said that its liquidity position is healthy with cash reserves of Rs103bn and credit lines of Rs22.5bn.

On Capex plans, management said that FY21 capex will likely remain at 15% lower of FY20 levels. It plans to incur Rs30bn/year from FY22e vs capex of Rs 40bn/year over FY19-21.

M&M looking to give up its majority stake in the struggling company Ssangyong. The company has written-off its investments in Ssangyong in Korea and has shutdown GenZe EV business in USA. It further acknowledged that further investments will be monitored regularly and it is working on categorizing subsidiaries into

Entities with a visible path to 18%+ ROE,

Lack of clarity on profitability strategic impact which is quantifiable,

Unclear path to profitability. M&M will exit the investments in third category gradually over next 10 months.

Mahindra-Ford JV’ focus will be on joint product development, supply of engines from M&M and tapping Ford’s distribution network in global markets.

M&M is on a roll, price moves with volume, closed at 570.6 today! Some more triggers that may turn out to be positive for the company (scrappage policy):

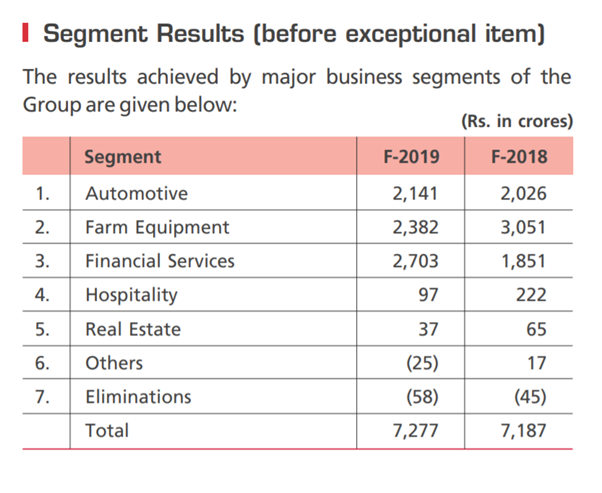

Tried Valuation for M&M through SOTP:

Current MCAP: 90,000 cr

Conservative Valuation

Particulars Valuation Remarks

M&M+MVML 45000 4500 cr normal annualised PAT at 10x PE

TechM 18000 60% of current Market Value

M&M Finance 6000 60% of current Market Value

Mahindra Holidays 960 60% of current Market Value

Mahindra Lifespace 800 60% of current Market Value

Mahindra EPC 120 60% of current Market Value

Mahindra CIE 480 60% of current Market Value (11% Stake)

Mahindra Logistics 960 60% of current Market Value

Total 72,320

Current Market Cap 90,000

Upside / Downside -19%

Thoughts on business:

Expected recovery in Auto post Mahindra Thar

CV recovery to take time

Exit of Syyangong to improve Conso ROE

trying to assess Valuation model considering current market Cap:

Current Market Cap 90000

(-) Investments 27320 60% discount

Auto + Farm 62680 Derived PE of 14x

Considering PE of 20x for Farm + Auto business: there seems further upside of 30%

Target CMP on aggresive valuation of 945

Healthy YOY growth in sales of all models (latest BSE update yesterday)

A very good start for the new Thar, it has already sold 25% of the quantities of high sellers like XUV 300 and Scorpio (sales in June 2021)

Yesterday the company announced the launch of the Bolero Neo (though a renamed TUV facelift) - Bolero is a high seller, top selling car for them in June 2021

new XUV 700 and Scorpio slated for launches in 2021 and 2022 respectively

Additionally, the article above talk about uplift in tractor demand, and sales trends look healthy for the CV business as well as per the latest update.

Additionally, large structurally tough areas could be towards the fag end, from the Ssangyong issues, to the BS6 transition, RM costs and the brutal CV cycle.

Would be interesting to see if the company now starts increasing sales at good margins moving ahead - and could this be a start of a new positive period with a good refreshed range of products as well as growth over historically low base.

Based on valuation of Tata Motors EV, what would be valuation of Mahindra Electric. It should be something similar based on investments they have made in the past. They are on verge of electrification of most of the new models.

A year of two down the the line current valuation of M&M can be justified just based on Mahindra EV and Tech M.

Looks like market has seen through this undervaluation this week.

CAPEX Plans of the Company

The company and its wholly owned subsidiary (Mahindra Vehicle Manufacturers Ltd) incurred a capex of around 3,300 crores in FY21. It has also provided capex guidance of approx 12,000 crores for FY22-24 and guidance for investments in subsidiaries and group companies of approx 5,000 crores for FY22-24

Please correct me if wrong, as per my understanding the listed M&M is only the Automobile part of the Mahindra business…Automobiles, Farm equipment & tractors only…