Hi all,

I was doing basic accounting work on Mahindra Logistics. Here are my short notes from FY15-FY19:

- cumulative PAT ~ 270 cr., cumulative CFO ~ 52 cr., cumulative EBITDA ~ 457 cr.

- CFO only matches PAT in FY19, in all other years CFO has been negative or lower compared to reported PAT

This generally means money is getting stuck in working capital and the earnings are overstated. On closer inspection, I realized that cumulative accrual taxes from FY15-19 ~ 146 cr. whereas the company paid cash taxes ~ 218 cr. (~71 cr. extra tax paid). I did not find any tax asset of this amount in the annual reports. Does anyone know why company is paying extra taxes?

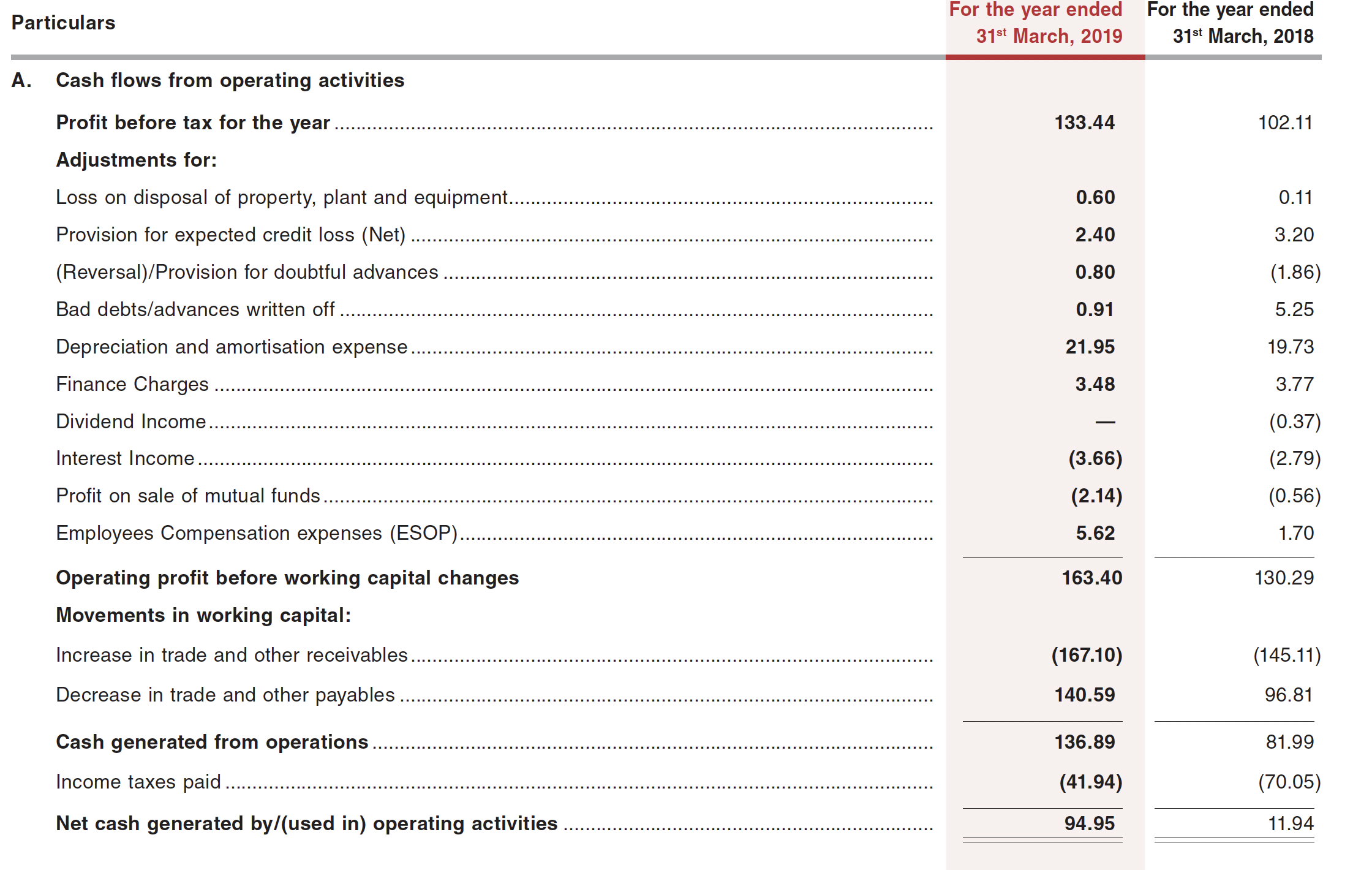

If we add the extra taxes back to CFO (52 + 71 ~ 123 cr.), this is still lower than cumulative profits of 270 cr. Cash flow statements from annual reports of FY18 and FY19 say that the main difference in CFO and PAT comes because of increase in working capital (receivables increased more than payables).

FY18

FY19

This is understandable as its a very low margin business and small changes in receivables will have a bigger impact on CFO. But why is the company paying higher cash taxes? Any feedback will be very useful.

@1.5cr