I just checked sceener, and looks like the net income / net profit they have is a little wrong. What screener is doing is simply taking the profit before tax and then directly taking consolidated net profit. While this is good enough in most cases, MAHSEAMLES has a Non-Controlling/Minority Interest, we add this in a consolidated statement, but for net profit attributable to shareholders, we need to subtract it.

I just went through the annual reports, and there is almost ~200Cr of minority interest over these years that does not reflect on Screener. The remaining ~90Cr can be explained due to tax rate and a few other line items it seems, what Screener seems to be doing is that they are taking profit before tax and then taking consolidated profit after tax without subtracting minority interest and using the above two created a plug for tax rate, which is why it is negative during some years. The number I have arrived with are in line with the annual reports on BSE.

I just redid the calculation, this time without rounding decimals, Cumulative earnings were 2,965.3Cr, their investments were 2,017.2Cr with which they increased earnings by 833.6Cr, so redeployed 68% @ 41.3% returns, multiply that and again, compounding value at 28.1%, hope this adds context.

Will the increase in exploration and production of crude oil improve the demand prospects for seamless and ERW pipe industry, and Maharashtra Seamless in the given case?

What is the future prospects of this company? In their investor presentation, they state that the following have invested in the company.

Quant Small Cap Fund , Quant Active Fund

• Quant Flexi Cap Fund, Quant Value Fund

• HSBC Small Cap Fund

• Aequitas Equity Scheme

• Vanguard Total International, Vanguard Emerging Markets

• Vanguard Fiduciary Trust, Vanguard FTSE All-World

• Abakkus Diversified Alpha Fund

• Morgan Stanley Asia (Singapore)

The first reason is the fall in sales realization, which has been on account of increased competition, lower raw material prices, and some dumping from Chinese manufacturers in certain segments.

We are in discussion with relevant authorities to address the issue of Chinese dumping, but that is a long-drawn process.

Due to the preventive maintenance shutdown of the mill manufacturing high value orders thereby impacting the earnings profile for the quarter. This mill has since resumed production at the start of Q2

FY25 and normalization of dispatches is expected in the second quarter.

The third reason was the dispatch of high value orders which were in limited quantity. As fewer high value orders were dispatched in Q1, the entire high value inventory which was purchased against

the remaining high value orders had to be marked down when raw material prices fell during the quarter.

Quarter numbers are lower because of:

a. account of increased competition,

b. lower raw material prices, and

c. some dumping from Chinese manufacturers in certain segments. <did not elaborate which segment specifically it is impacting. This anyways is a time-consuming process, and no quick turnaround is possible. Roughly above 3 were equally weighted impact wise per management.>

d. Preventative maintenance shut down, led to not executing on some high value orders.

Lower RM cost, led to inventory devaluation, which will be nullified once we fulfill the orders that were supposed to be dispatched in the Qtr gone by.

Telangana Unit:

a. The Telangana finishing line was expected to be completed by March 2025. But, I don’t think that will happen, in all probability it will be deferred by at least 9 months, because we have recently placed order for some equipment, those orders have been finalized, purchase order has been issued. However, the gestation period for that order is 12 months. So, reasonably speaking, the Telangana unit expansion should get completed by December 2025.

Hot mill upgrade will only happen once the Telangana finishing line is in place because we will have a loss of production whenever we take the hot mill upgrade. So, in order to compensate that loss, we need the Telangana unit to be active in full capacity. The sense which I am getting from your question is, when will volume growth come in? So, I don’t think there will be any volume growth in FY25. And in FY26, volume growth will only happen once the Telangana finishing line has been completed and is open for commercial production.

We don’t export to the Middle East, exports have not revived, exports have been slow for more than a year. Market size in US and Canada is very big, but they have not revived for us.

EBITDA per tonne fell from Rs.22,000 a tonne to Rs.9,000 per tonne!!

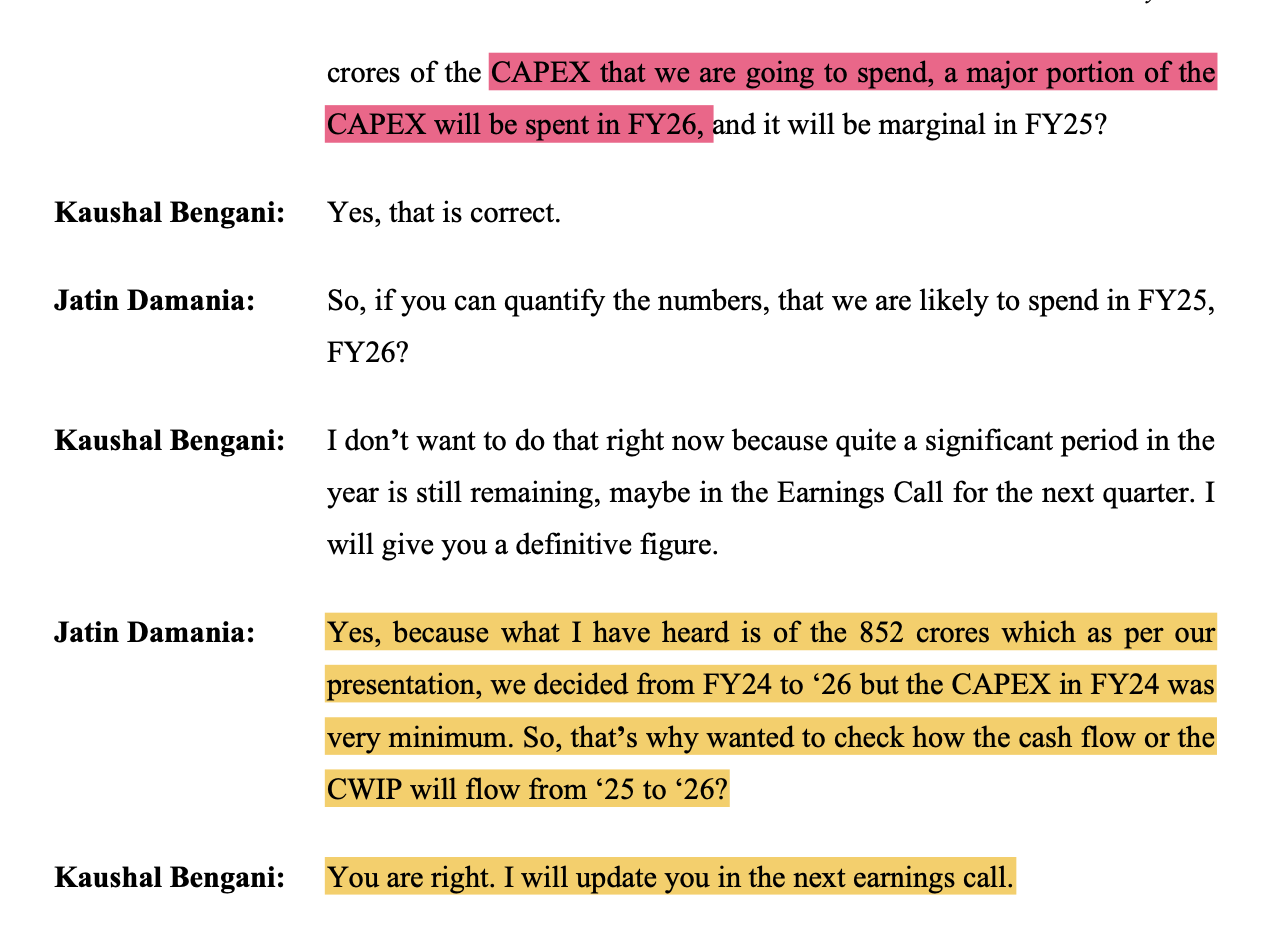

Capex:

The announced ~850 cr would be mostly spent only in FY26.

Although there might be a quick reversal once the high values get shipped and the RM prices adjusted and might show profit and bump in margins, the Capex has been delayed to FY26. So, its wait and watch for me in this counter.

Maharashtra Seamless Limited faces short-term challenges but maintains a positive long-term outlook. The company experienced a significant drop in EBITDA and profitability in Q1 FY25 due to three key factors: falling sales realizations, a preventive maintenance shutdown, and inventory mark-downs. However, management expects these issues to be temporary, with normalization likely in the coming quarters. The order book remains strong at Rs. 1,812 crores, up from Rs. 1,754 crores, indicating healthy demand.

Strategic Initiatives:

Focusing on high-value addition products like cylinder pipes to improve margins

Expanding capacity through the Telangana unit, though completion is now expected by December 2025

Exploring new export markets for sour service subsea seamless pipes

Addressing Chinese dumping through discussions with relevant authorities

Trends and Themes:

Increasing demand for seamless pipes in the oil and gas sector

Growing focus on infrastructure development driving demand for pipes

Shift towards high-value, specialized products

Industry Tailwinds:

Strong demand from the oil and gas sector, particularly ONGC and Oil India

Robust capital expenditure in infrastructure projects

Government initiatives promoting domestic manufacturing

Industry Headwinds:

Increased competition and dumping from Chinese manufacturers

Volatility in raw material prices affecting margins

Slow revival of export markets, particularly in the US and Canada

Analyst Concerns and Management Response:

Concern: Sharp decline in EBITDA per tonne

Response: Management attributes this to temporary factors and expects normalization in coming quarters

Concern: Delay in Telangana unit expansion

Response: Revised timeline provided, citing equipment order lead times

Concern: Low exports

Response: Focusing on high-margin markets, avoiding low-margin regions like the Middle East

Competitive Landscape:

MSL remains one of three major seamless pipe manufacturers in India, maintaining its market leadership position for 35 years. The company faces competition from Chinese imports in certain segments but is working to address this issue.

Guidance and Outlook:

No specific guidance was provided, management expects improvement in the coming quarters as temporary issues resolve. They do not anticipate significant further declines in realizations.

Capital Allocation Strategy:

Continuing with the planned Rs. 852 crore CAPEX program, though majority spending is now expected in FY26

Increased dividend payout in FY24 (quadrupled compared to FY22)

No current plans for share buybacks

Strong treasury position of Rs. 2,203 crores generating good returns

Opportunities & Risks:

Opportunities:

Expanding into new export markets for specialized products

Growing domestic demand in oil & gas and infrastructure sectors

Potential for margin improvement through focus on high-value products

Risks:

Continued pressure from Chinese imports

Raw material price volatility

Delays in capacity expansion projects

Regulatory Environment:

The company is engaging with authorities to address Chinese dumping issues. No other significant regulatory concerns were highlighted.

Customer Sentiment:

Customer demand remains strong, particularly in the oil and gas sector, as evidenced by the growing order book.

Top 3 Takeaways:

Q1 FY25 performance impacted by temporary factors; management expects normalization in coming quarters

Strong order book and demand from oil & gas sector indicate positive long-term outlook

Focus on high-value products and capacity expansion to drive future growth

I see this as a Breakdown (or emergency ) maintenance, because the maintenenace came in the way of essential/ high value (not prioritising against low value) deliveries… The acceptance of supply orders must essentially predefine a delivery timeline. Not adhering to this aspect points to, say, a cultural weakness @Maharashtra Seamless?

While the lower EBITDA for Maharashtra Seamless in the June 2024 quarter is primarily attributed to a decrease in net sales and overall profitability. Specifically, the company’s net sales declined by 5.88% year-over-year, from Rs. 1,222.94 crore in June 2023 to Rs. 1,150.98 crore in June 2024, I see this as a lack of commitment (read Quality of Management - poor execution).

Additionally, the company’s net profit also saw a substantial decline of 37.41%, further impacting overall financial performance.

I have a very basic question. Who is really running this company? The concall questions are answered by Mr Kuashal Bengani, who seems to be from investor relations/finance. Why does the MD, Mr. Saket Jindal, does not do it himself?

In the recent Q1 FY26 concall, the management mentioned maintaining ₹2,900+ crore of cash and equivalents, citing vague and long-term reasons such as future machinery replacement and undefined inorganic opportunities. However, only a small fraction (~₹150 crore) of the previously announced ₹852 crore capex plan has been executed, and major growth/modernization projects remain pending. The repeated shareholder concerns on low capital deployment, modest dividend distribution, and growing dependency on investment income were not addressed with specific timelines or measurable goals. It reflect a lack of strategic clarity or risk aversion .

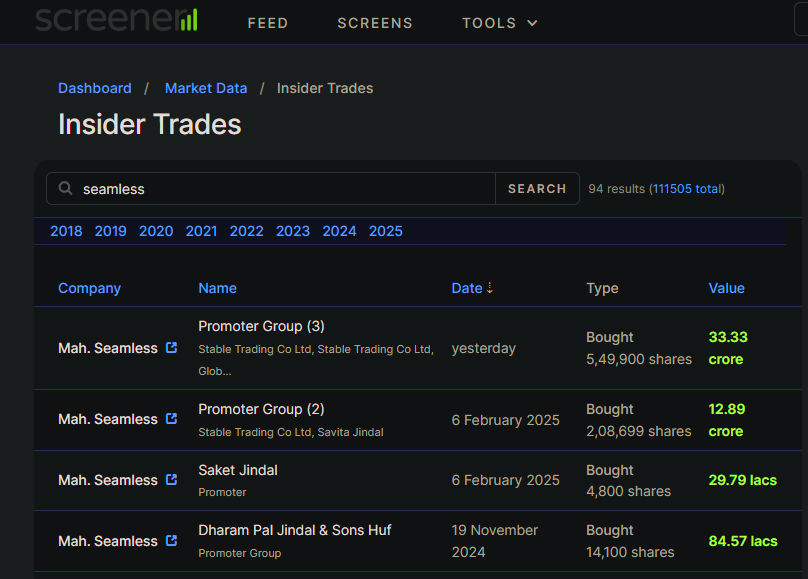

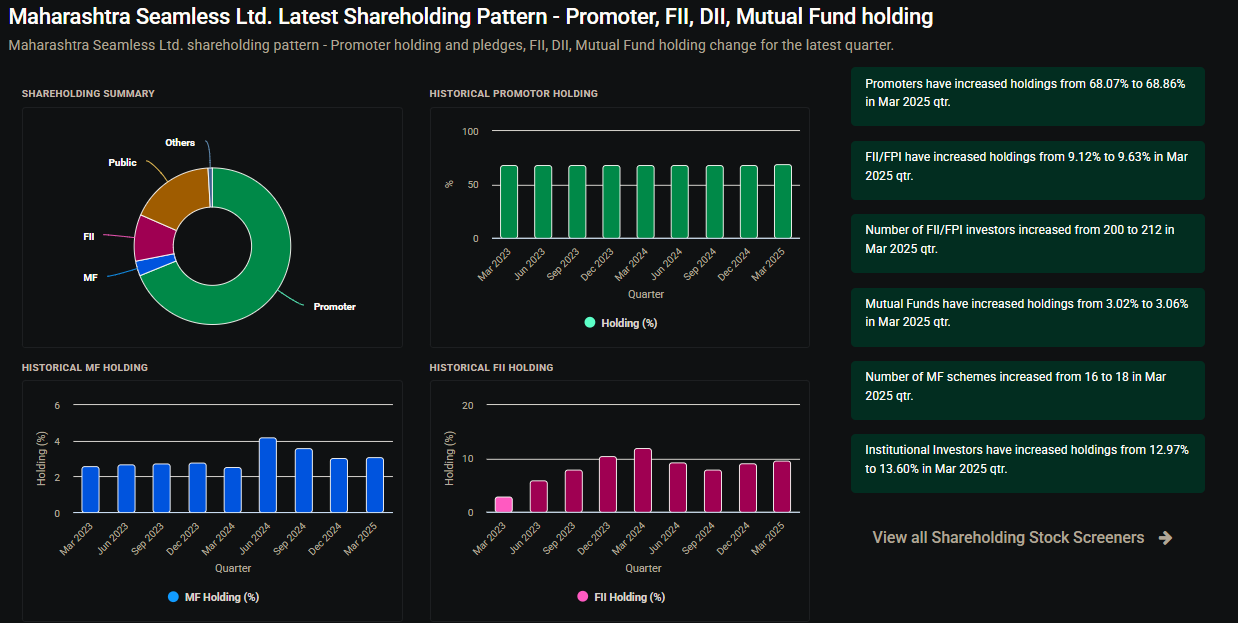

On the other end Promoter , DII ,FII are increasing their stake in a company which is not looking for growth , but generating income through investment (MF , bonds) .

is it like they know something which is not in public domian ? Can anyone throw some light on it ?

The company can only grow so much under domestic protection.

Our oil and gas industry is small, company is not competitive in exports ( chinese quality is better).

Company has more than enough capacity for PSUs and the remaining small SME manufacturing segment.

Till the Indian economy grows, there will not be enough areas for the company to increase revenue. Only markets where they were exporting is USA, and with trump that also looks difficult now.

The protection umbrella can work only upto a point. And with a promoter family driven company which is enjoying the protection , we shouldnt expect much.

They will enjoy the dividends. We as investors should look at better opportunities now.

Budget 2026 x Maharashtra Seamless: A “Seamless” Growth Story?

Yesterday’s budget kept the pedal to the metal on infrastructure. Public Capex is up to a massive ₹12.2 Lakh Crore. For companies like Maharashtra Seamless, more infra = more demand for specialized piping.

With ₹57,612 Cr allocated specifically for Exploration & Production (E&P), the lifelines for MSL, ONGC and Oil India (33% of its order book) are flush with cash. Expect a steady stream of orders for high grade drill pipes and casings.

The new ₹20,000 Cr Carbon Capture (CCUS) outlay is a sleeper hit. Refineries must now retrofit for decarbonization, requiring complex, corrosion-resistant seamless pipes. Maharashtra Seamless is perfectly positioned to capture this “green” demand.

While the industry pushed for a 20% duty hike on Chinese imports, the focus on Atmanirbhar Bharat and “Champion MSMEs” ensures domestic players get priority.

Robust E&P spends + City Gas expansion + the new Infrastructure Risk Guarantee Fund = A very healthy visibility for the ₹1,302 Cr+ order book. Long-term outlook? Structurally positive.