My notes from the recent concall:

Telangana unit commenced aug 2024

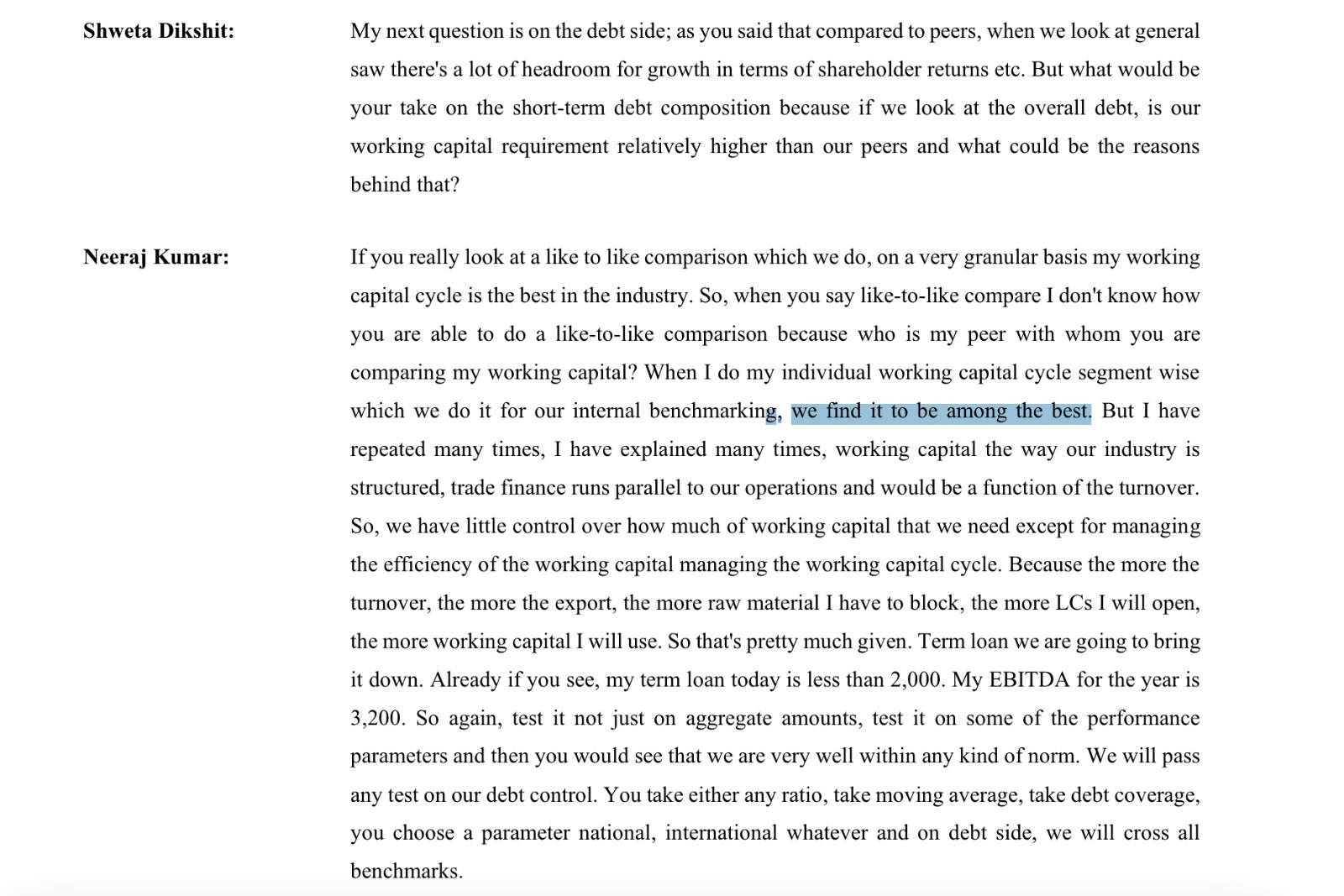

1300 cr investment, gross debt done, core operations and shareholder reward only to be used

Morgan stanley domestic india fund co has added

ICD- realise all of them by march 24= 78 crs march 23, 43 crs today

Liquid investment as increased by 25% in last 6 months

Corporate guarantee reduction on schedule, legacy guarantee to be done by sept 2024

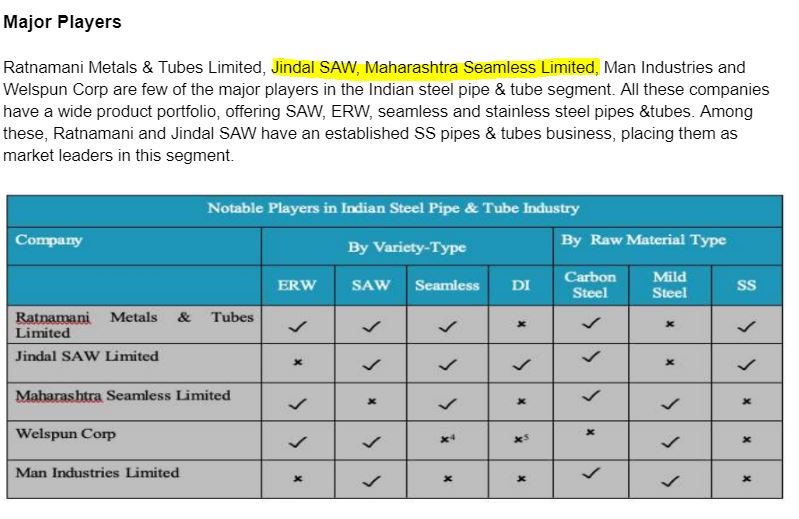

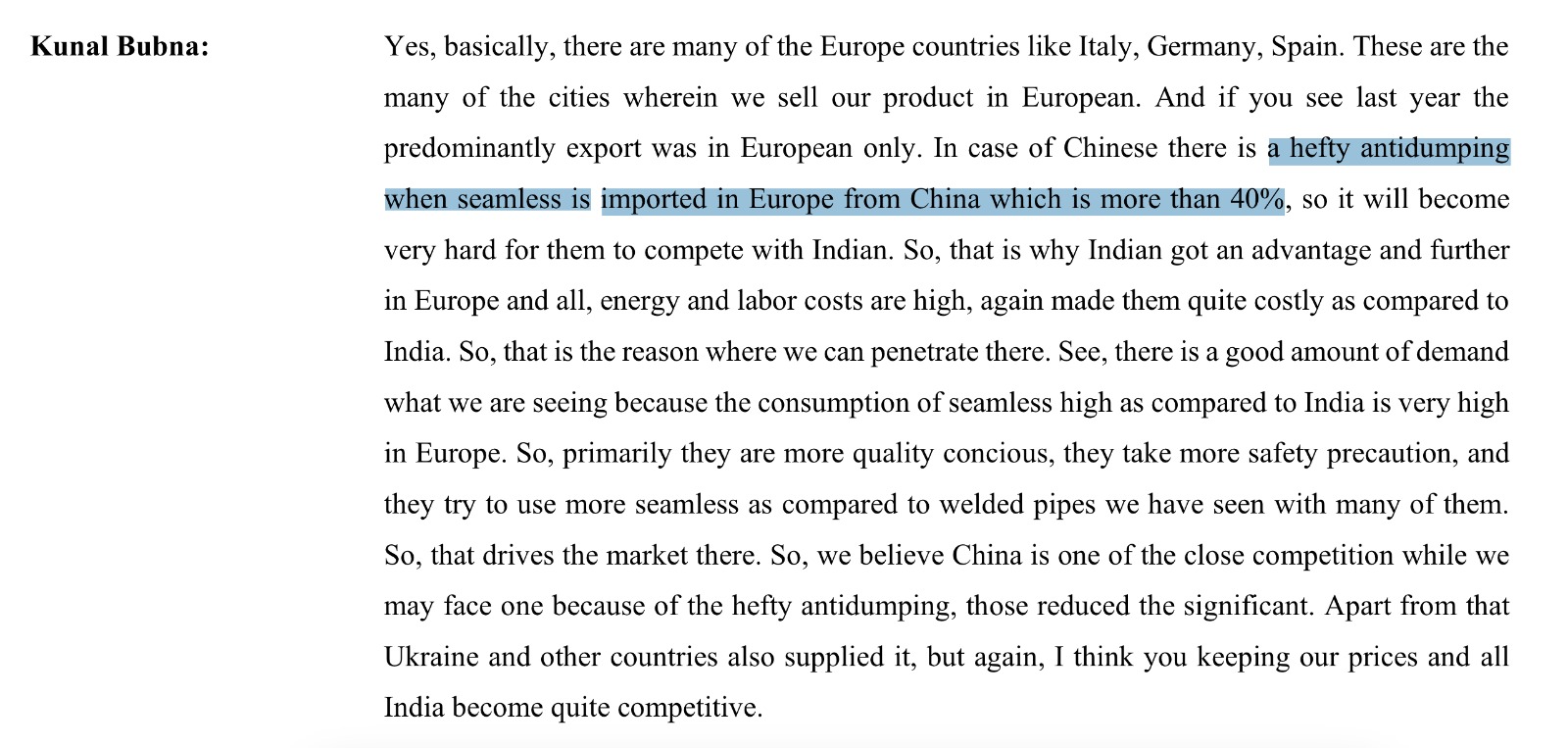

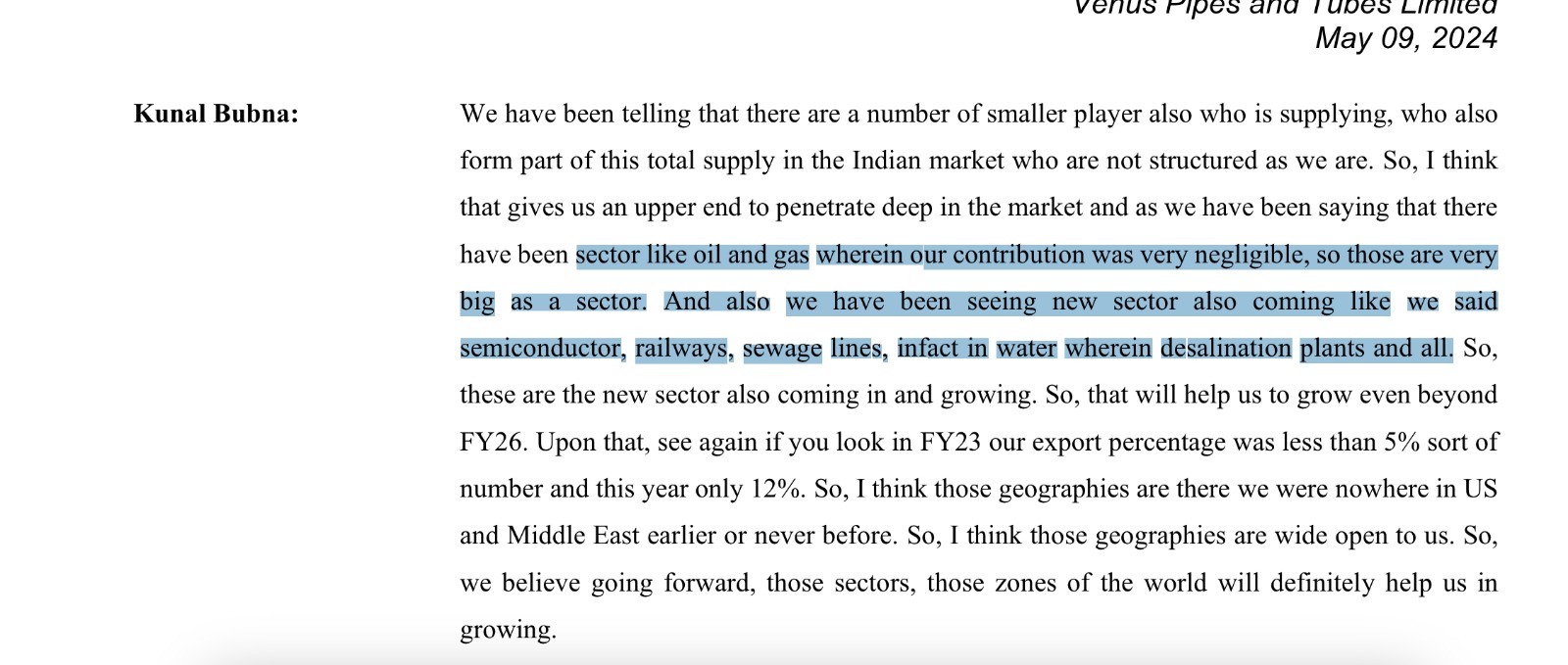

Oil sector contributed significantly

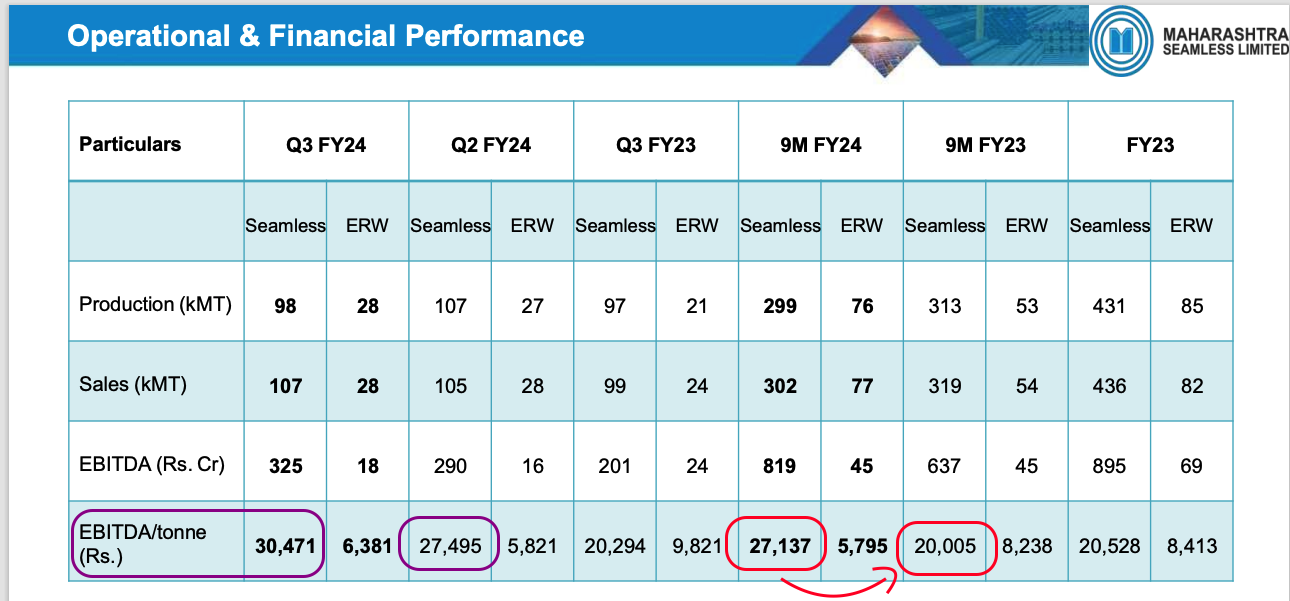

87% of ebitda is seamless

orderbook - 1468 crs, 325 crs confirmed but only in pipeline due to purchase order issuance pending dealer export and upstream segment,

Trend of ebitda per tonne 27495 rs, strong execution of order book, oil sector contri significantly, margins to remain good as seamless market is strong and co is well poised. Margins are expected as of now to remain good

Uscpl amalgamated with co, do not provide individual numbers

Iocl order- 2 orders in sept of 23, oil india and iocl, 100-125 crs each, expect to get it done by q3

Share of export has not gone up

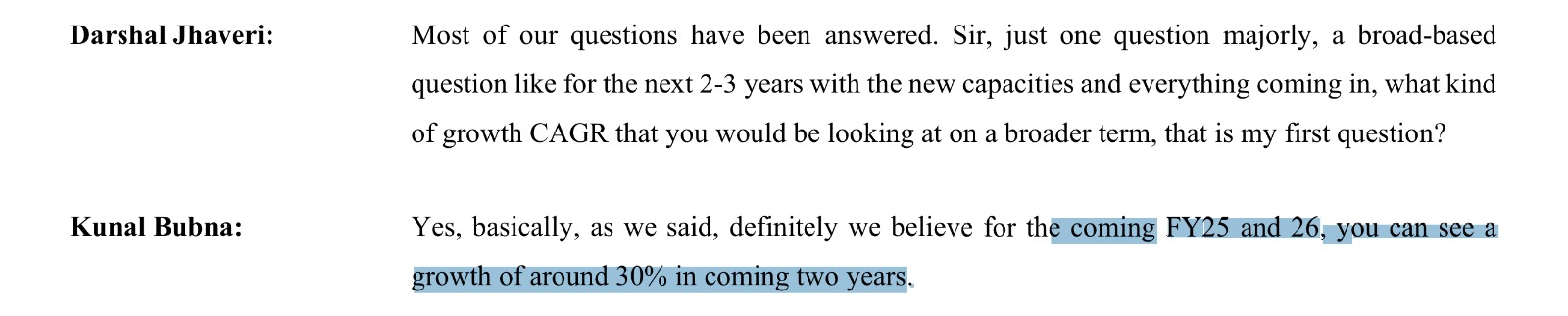

Min 5% sales growth fy24 was guided previously, seamless and erw combined will attain the same

Production loss in Q1 due to amalgamation

Interested in JV of someone, trials are ongoing with company

Capex? Down the line in next year

Win rate for ioc and oil= 50%+ business from them, and execution timeline FY25

25% steady tax

Exports are to revive from niv

Dispatches are inc 20%, 90k seamlessQ1, 106k Q2 Q3 more than q2

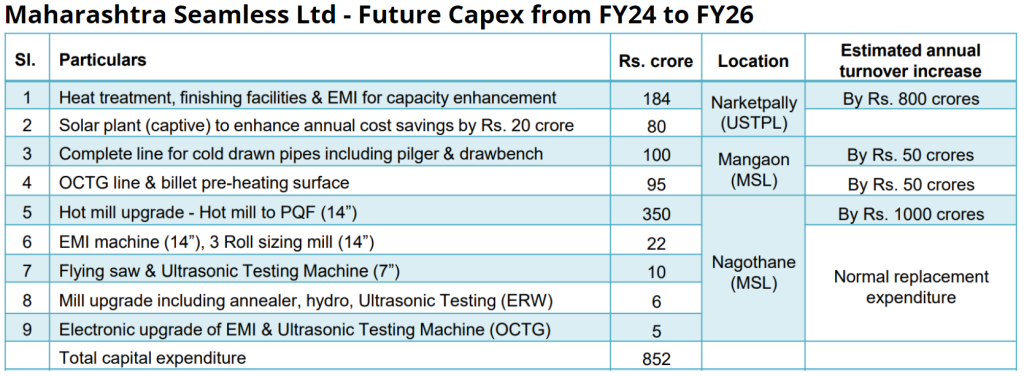

350 cr hot mill capex pending, 500 crs capex in the next 1 year

Rumour of US market opening up and tariff going down? Open to US market and 6 months ago also exported to north america can cope up, certainly opening up

Domestic market also goes up when US market is higher

Ongv 3500, oil india 500-700 cr to spend in FY25 on pipe procurement= 4200= 50% win rate 2100 crs

Disclosure: studying, not invested yet