That is a great question. Do they have any moat?

We are primarily looking at a platform business. We need to check whether they have any network effect?

the term network effect refers to any situation in which the value of a product, service, or platform depends on the number of buyers, sellers, or users who leverage it. Typically, the greater the number of buyers, sellers, or users, the greater the network effect—and the greater the value created by the offering. In other words, the willingness to pay, for a buyer, increases as the number of buyers or sellers for the business grows.

Every platform has some amount of network effect. Say, to buy groceries we wish to use big basket, because they have more options. To buy books, we prefer Amazon beacuse they have greatest collection of books.

In the case of electronics/drone/robot parts, the network effect is higher because the customer needs many types of part supplies, and all parts ought to be compatible to each other. Further, the chances of parts malfunctioning is greater and a customer will typically prefer a reputed supplier with good after sale care. We can see that Robu.in has started well, and probably can grow well too.

The opportunity size is very high. Robu has 12000 odd SKUs, whereas Digikey has 1.6 million SKUs. Digikey revenue has crossed 5 billion USD with more than 1 billion net profit. Found somewhere that Digikey is operating on EBIDTA of higher than 40%! Thus, in my view, the company has the opportunity to grow. Whether they grow or not, we can only guess.

On competition, 3-4 weeks back i had done a quick search and found there are enough and more players in India who are in to similar business. I think some of them are traditional players (like those operating from Lamington Road, Mumbai or Delhi players traditionally in this area) who have setup websites as well.

Some of the competitors I had looked up are:

digikey.in

Some of the players heavily play the “discount” game by prominently highlighting it for many of their products on the website.

Robu’s return cost and obsolete inventory numbers look incredibly low. Not sure if we can believe these numbers on face value. Returns management is a headache for all e-tailers in general…and obsolete inventory numbers will keep shooting up as number of SKUs are increased

Business has a lot of promise, but dont have the conviction to enter given extremely small size of business and big lot size to take a minimum position.

Its also a play where they want to focus on (and how sales mix eventually evolves). B2B/ B2C (B2B could also morph into B2G, if enough govt cos come in).

Specifically in B2C, if the space heats up and starts growing, there is possibility of larger players coming in and investing (either in these cos we dscsd or setup their own operations). Typically when this happens, lot of things around better price, favourable/aggressive return policies, customer acquistion and activation spends (burns) come into picture, which will need a warchest (if they’ve to compete). CAC (customer acquistion cost) to LTV (life time value) will have to be looked at.

Anyways, If this happens, could be a good sign for this segment, given its a new category being created (in a way).

It would make sense to think more from a customer angle, as to what needs are being fulfilled by Robu today and how those needs will evolve over a period of time.

Disc: Studying, not invested.

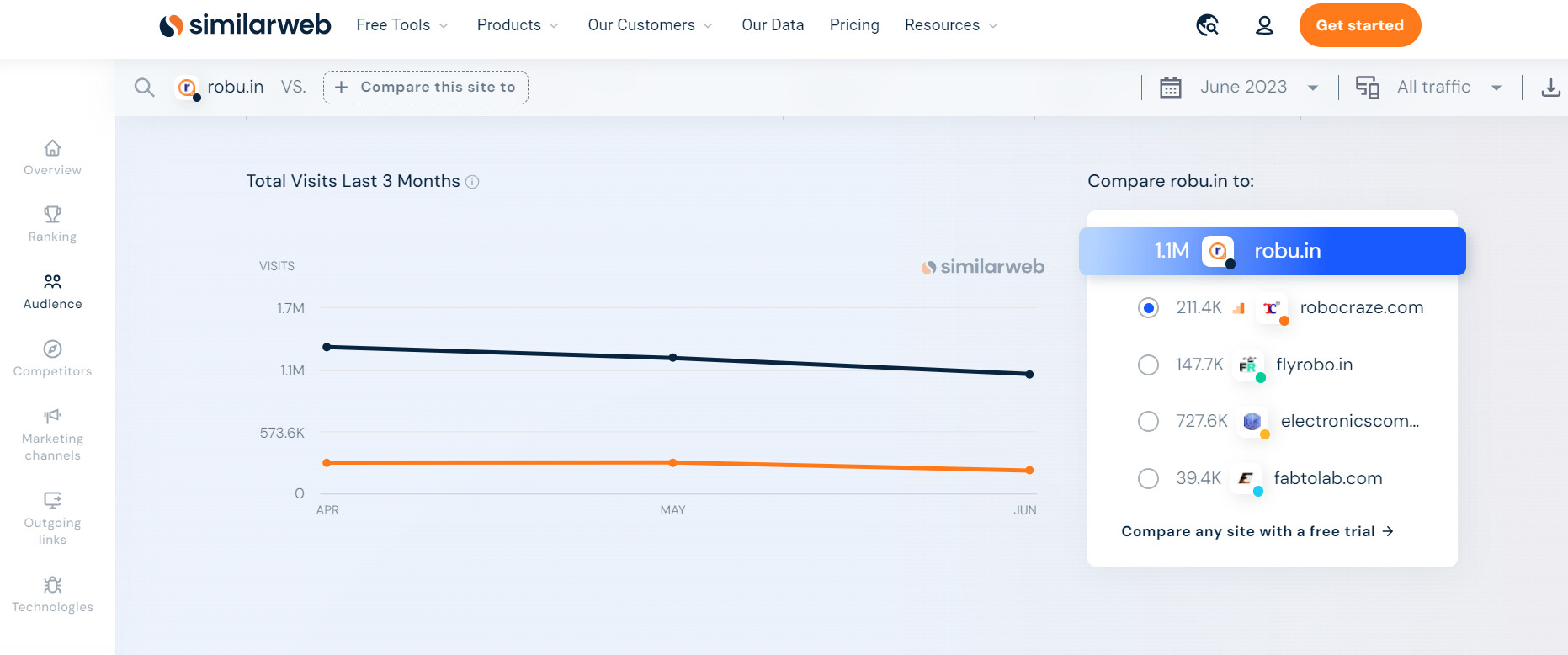

My sense of competition is, for an investor searching for them, it was not that difficult to find them. Just go to similarweb and search for robu’s statistics and it will show up all the competitor sites. One can compare some of the relevant statistics between all those players. Sahil has already posted some of those info in his post above.

But as an investor, we also have to understand that since the sector seems to have immense potential, we can’t rule out entry of other players. It’s not that kind of play. The play here is robu is well recognized player in this segment. The promoters with no background and funding have positioned themselves well on the basis of their merit. This business demands operational efficiency and lower cost is one of the parameters. Ultimately most of these players buy from someone and sell to others, mostly inventory stocking type model, managing inventory and working capital has a direct bearing on the results. Many times volume they buy will decide the price discount they manage to get from manufacturer and hence their costing. So big has good chance of becoming bigger.

On the aspect of product price deciding who emerges as winner, Imagine what %age of us directly go to flipkart/amazon for most of our needs vs checking every site possible to find the cheapest deal on each of the products we buy? This is a good example of 80-20 rule in practice. There might be 8 other sites which would have some of the products we buy available cheaper, yet most of us go to these 2 for most of our needs and don’t keep hopping from site to site for cheap price on each of our purchases.

We need some solid evidence to conclude this, isn’t it? Like similar nos. of others players ?

In vertical ecom sites, multiple players exist today doing well for themselves in their niche. Like BigBasket, Nykaa, indiamart etc etc… In theory anything can be done by big players since they have the money and sometimes these fears come true and these niche players can get destroyed or taken over. We have to keep our ears to the ground. But I think that’s not sufficient cause to avoid a nicely growing niche player out of fear of competition.

This is a good point. ~40% of customers are in 18-24 age category, most likely young engineers in college campuses (my hunch). This is a very important metric because most likely the brand name is getting passed on from senior students to juniors based on their experience. This lowers the customer acquisition cost, at the same time if something goes wrong in robu’s execution or some other stronger player emerges then this has equal chance to hurt. Bad experience news will spread faster. The customer base most likely has smaller communities and it won’t be just individuals like in other categories.

Its more like an early stage startup and needs more time to grow and competition is bound to come from big players as the electronics/semiconductors theme seems to be hot pick as of now.

This is like sub-sub segment of the whole electronics/EMS sector/theme. I think the current size of the market (what robu caters to) is smallish compared to what might be the market size in the electronics/EMS component buying space. The large EMS players might be buying lot of components directly from Chinese players/vendors. I don’t think that kind of sourcing will ever shift to robu kind of players. It’s the student, small startup, small volume govt institutions kind of players who will be customers of robu kind of players. That too is a growing space along with the broad sector. No, idea how big is the market consisting of offline only small players. Hope macfos can grow to 500cr revenue and 50 cr. kind of PAT in 4-5 years. That’s the bet here, in absence of growth all bets are off. No amount of theorizing can help.

As i mentioned earlier Macfos-Repro- Vaibhav Global are one and the same thing.

People are completely biased and crazy about their opinion on Robu.in in this thread.

See Repro and VGL are much stronger they have their own manufacturing, they are also niche.

But if u compare products durability(Robu’s products are such if god himself mfg’s 12000SKUs in same space, people will give him 3.2* on an avarage ![]() ) so robu’s products by nature complex. It will never allow it to grow at any sustainable manner.

) so robu’s products by nature complex. It will never allow it to grow at any sustainable manner.

Second thing i dont find promotors profile so interesting …!!! correct me if wrong. I doubt on their ability to grow this beyond current stage. so according to me story is saturated ![]()

Disc. :- Not invested

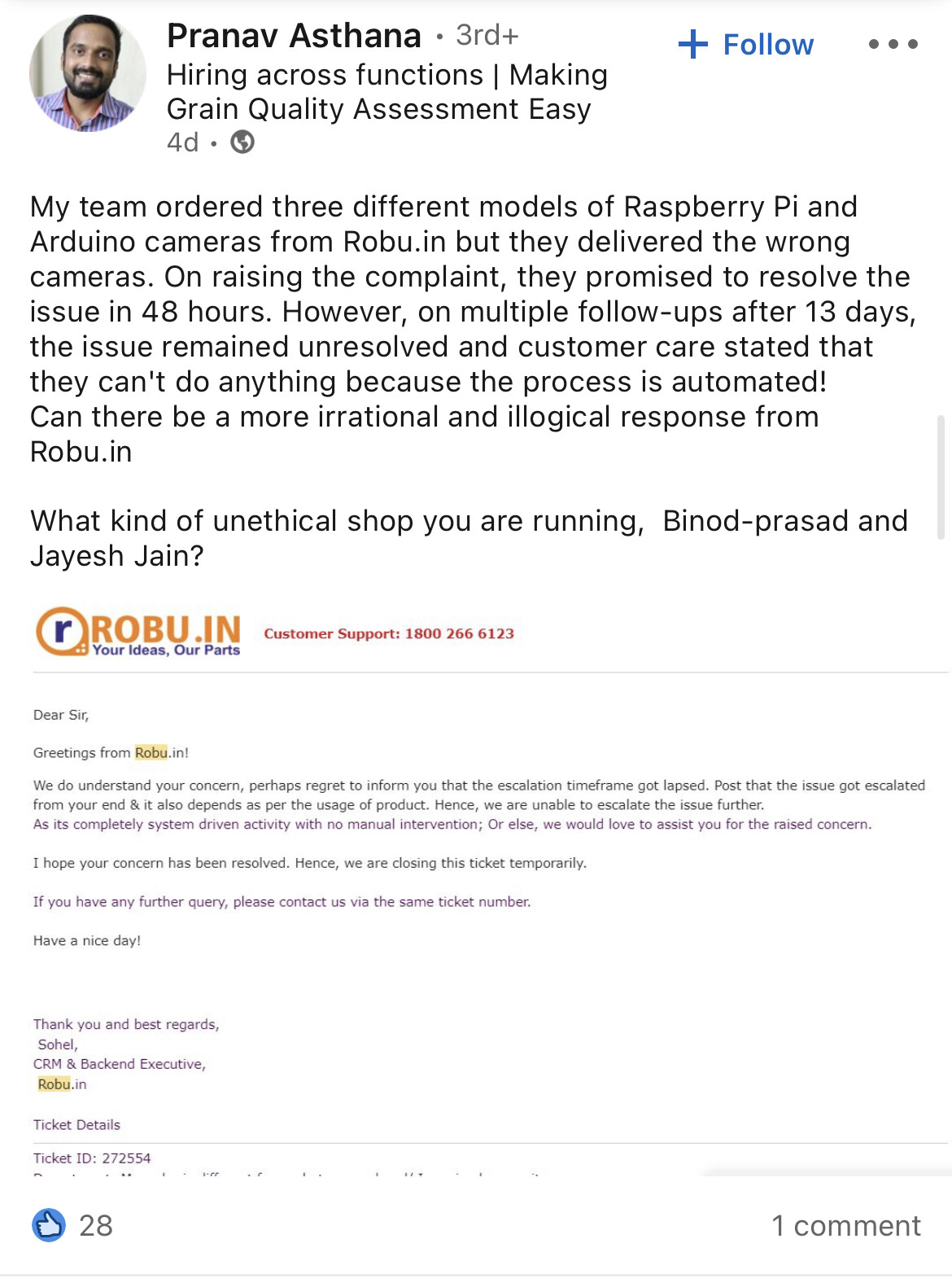

This is normal in an early stage company- hope they address customer’s complaint quickly. Customer care setup will also evolve as they grow.

Disc: not invested

My perspective as a customer

The areas where I find ROBU.IN very useful are

- Low lead time (I remember some hard to get electronic parts had a lead time of 10-15 days in ROBU, compared to 3-4 months in the competitor space )

- Their inventory is pretty rich and they are adding more SKUs. Also when we are building a system (say drone) Robu.in becomes a one stop shop.

Amazon is unreliable (my view) when it comes to electronics parts.

Robu is a good replacement for markets such as S.P Road (Bengaluru), Nehru Market (Delhi) etc.

Disc: Not invested yet but keeping a close watch.

good read on robu.in

they do 55% revenue B2B selling to large corporates.

Its easy to replicate Flipkart, Amazon, Zomato etc by your definition, its not easy otherwise somebody would have done it.

No one floating new E comm company now, winners are there already for us to invest.

No , bcoz these businesses don’t google and buy online from Macfos.

Please read the conf call and DRHP. B2B happening different way for them atleast the B2G bcoz they to tender it then get contract.

Every business can be replicated, we are living in free markets. Anybody can make a soap and compete with HLL or make noodles to compete with Nestle. That does not make HLL or Nestle worthless.

It is small cumulative advantages which creates moat for a business. A website itself is a brand, particularly in e-commerce business. Relationship with hundreds of vendors and thousands of customers itself is an advantage. Efficient inventory management, and understanding of customers need is an advantage. A group of young engineers creating a business from scratch, without much financial backing is management quality, which is in itself an advantage.

Do they have competitive advantage? Well ROCE/ROE figures are quantitive proof of competitive advantage a business is enjoying, at least in the present times. What will happen in future- well nobody knows.

The company has incorporated a wholly owned subsidiary in HongKong- Nuo Zhan Technolohy Limited. The business of the subsidiary is trading. This new entity formation would widen the solution offerings of the Company, and further strengthen the Company’s growth strategy.

549ebf61-b628-44fd-a62e-2432a63c7b2b.pdf (230.0 KB)

Being an e-commerce website, I believe a strong online presence is crucial for its future growth. Upon examining its website traffic, it is evident that it has been decreasing over the last three months. I consider this a clear indicator that robu.in is losing its popularity and market share.

One also needs to look the numbers in context of post covid impact. Ecomm in general is showing decelerating growth in multiple areas of retail business.

Also, traffic numbers is one metric but needs to be looked in conjunction with conversion rates and average basket size.

Just my 2 cents!

Disclaimer: Not invested, tracking from a distance to gain more understanding of the business

yes also 3-month data is not the correct way to see it, the IPO happened just months ago. Traffic might have gone up due to investors community checking the website out.

Some basic questions :-

They are not the Google , not the amazon or not even they are 1/10th of TOP 10 amazon sellers. than how and why they will grow at any substential rate.

And if they will not grow at any substantial level then why to take such a risky bet.

second there are plenty of oppurtunities r there in newely growing sectors where sectors itself grow at exponential rate. then why to take a call at decade old sector.

As a said earlier "If u have very strong product portfolio and having ur own manufacturing capabilities then and then u will manage the inventory and sectorial tailwinds. E.g. Repro and Vaibhav Global etc…

U r selling majority of chinese products and expecting people to give u good feedback which is impossible and without history of feedback how online website will grow…

Correct me if i am wrong

Disc. :- Not invested

My 2 cents.

- First, let’s see the business from it’s customer’s perspective. Customer is typcially a student/tinkerer/DIY kind of person, maybe doing his engineering degree and as part of course, he is supposed to or passionate to try out few hardware projects. Where does he go to buy the components ? If he is in a small city, then he is lucky to have 1-2 store dealing with such HW. But then timely availability of so many sku’s at such low volumes is a big deal for the physical store. Hence the necessity of online stores. If one is lucky to live in a big city like Bangalore with S.P,Road then things become easier, but the hassle of physically going there and fishing out the right product, price, return policy still remains a tough job. Hence the need for this category of online stores.

- Second category is, the Defense R&D PSU, Startups - The first category out of the 2 need transparent pricing (cheaper local store not providing formal bill won’t make the cut). Startups also need them quickly delivered. Price may not be that big a deal for first prototyping stage.

- Business of Vaibhav Global is not comparable with Macfos IMHO. From whatever little i know about them , it’s more dependent on luring customers to buy some knick-knacks, the product themselves may not have much real value for their customers. Easily replaceable. No one will bat an eyelid, if they shut shop. BUT, If one is working on a prototype of some product, having the components available, reliability, timely delivery, scalability of units, quality & compatibility of each of components, all these aspects are very important. There is knowledge involved in this process of selection of components as well.

- Chinese parts : That’s an unfortunate reality of electronics component industry, we and perhaps the whole world are way too behind the Chinese in this industry at the moment. I won’t hold that against Macfos. It’s not their doing and it’s not like they are deliberately promoting Chinese while Indian equivalents are available at comparable cost.

All said and done, if they grow below 40-50% then it may not be worth the risk, being a SME. The play here is for growth, hopefully matching the last 3 year rates. If that does happen, then we can see some good wealth creation. I think the risk to business model is not that serious. The risk from competitors will be there. No serious moat for Macfos either. Execution is the name of the game here.