studied the result, spate of disappointments in past many quarters with the worst one this q, price action hinting towards a bottom made, management strong near & medium term commentary on expected nos going ahead, remains somewhat of a deep value play with a solid long term ‘not baked in’ pipeline

Its frustrating & easier to just sell out and buy something else with more certainty, which in my investing experience has often tended to be the worst time to do exactly that, this is the time to buy

Nos revived in Q2FY23 vs Q1, but are still flat on YOY basis. Management sounded very confident of revival in H2 with a spate of new launches in USA. Concall notes below.

FY23Q2

US revenues came at $159mn, growth over last quarter was due to albuterol + suprep and a stable base business. Expect strong flu season in H2FY23

Tarapur: got warning letters due to impurity in certain products (lactosamine, nitrosamine). No meaningful filings from Tarapur, current products not impacted

US oral solid: price erosion in high single digit currently

Acquired 2 inhalation brands (Xopenex HFA, Brovana) for $75mn

gDulera: received CRL for which they have filed a response

gSuprep was launched in September, so majority of growth will come in Q3

Albuterol market share: 21.3%

gSpiriva IMS revenues are still around $1bn and Lupin expects to be the sole generic (along with a probable authorised generic that might be launched by innovator)

India business growth (2.6%) was impacted due to loss of exclusivity in diabetes (cidmus brand, genericization of gliptins)

Will add 850 MRs in India in FY23

API: demand for cephalosporin is still muted

Oncology R&D: have 5 development assets, reduced manpower and will only spend on clinical trials. Tough markets to raise capital in this division

Disclosure: Not invested (no transactions in last-30 days)

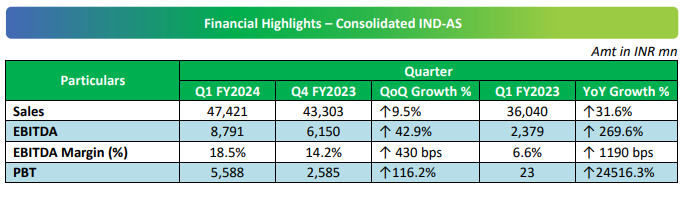

The drug maker has reported a drop of more than 25% sequentially in consolidated PAT which is attributable to owners in the March 2023 quarter. However, Q4 PAT was better on a year-on-year basis on the back of strong EBITDA growth and higher revenue.

Revenue from operations stood at ₹4,330.30 crore in Q4FY23, rising by 12% from ₹3,864.50 crore in the same quarter a year ago. However, revenue was up by 2.02% from ₹4,244.56 crore in Q3FY23.

India is back to double-digit growth after a tepid last year. Europe, Middle East, and Africa Sales up 11% in Q4. America is doing 175-180 million$

Margin improved from 6.9% to 13% on a YoY basis

Other Income: They are getting some funds from the government in the form of the PLI scheme. Mgmt is confident that it would be sustainable for the coming few quarters.

Management guided for an 18% margin going forward from the current 13%

Mgmt is confident of launching the Spiriva generic by July-August in the US market. It’s a medicine to treat asthma and thus comes in the chronic section.

Diabetes medicine is still a struggle as they lost exclusivity for one therapy.

Gastrointestinal, women’s health performing well in India.

Brazil and American subsidiaries are currently loss-making.

Looks like the stock is finally on track and couldn’t find any negative, their guidance of 18% is quite impressive

Excellent Q3 results. Crossed Rs.5000 crores in quarterly sales for the first time, and EBITDA margin crossed 20% after a long time. Surprisingly, Europe’s contributed strongly and US only grew marginally (I thought US sales would be better).

With their recent launches and approvals, the company seems set for a few good quarters unless some FDA issue strikes again or some goodwill write-downs are still left (don’t think so, but they did make a few small acquisitions recently).

The stock’s of course already run up a fair bit. Theoretically, seems fairly valued now, but with the growth momentum and improving margins, can go up some more. If one of their recent and upcoming launches translate into higher sales than anticipated, then it can go up substantially too.