I did not found any specific topic for LUPIN. Hence opening a new thread. This is my first thread on value picker and I am not an expert in equity analysis (in learning phase). Moderators/Admin please delete the post in case it do not suits the value picker community requirements.

Company Overview :

Lupin Limited is a pharmaceutical company based in Mumbai. It is the seventh-largest company by market capitalization and the 10th-largest generic pharmaceutical company by revenue globally.

Performance matrix :

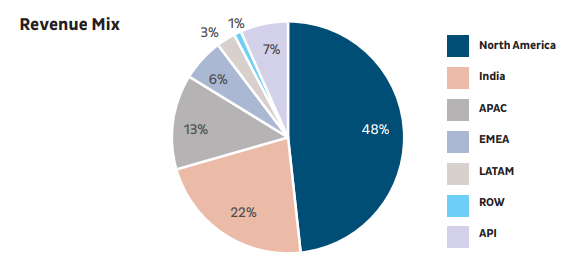

Revenue breakup-

US Markets :

US revenues surpassed the USD 1 billion mark, closing at USD 1,207 million. a growth of 37% over FY 2016 revenues of USD 883 million.United States remains Lupin’s largest and most important market with 48% share of total revenues.

The Company filed 37 ANDAs and one 505(b) (2) NDA in the US market during FY 2017 and currently has 154 ANDAs pending approval, addressing a total market size of over USD 74.9 billion. Of these, 28 ANDAs are first-to-file opportunities

addressing a market size exceeding USD 13.1 billion. This includes 14 exclusive first-to-file ANDAs targeting a market size of approximately USD 2.6 billion.

INDIAN Markets

During the year ended March 2017, Lupin’s Revenues reached ` 38,157 million, representing growth of

11% over the previous year and 15% CAGR over five-year period. With 3.3% market share, Lupin is the 6th largest player in the Indian Pharmaceutical Market.

JAPAN market:

Japan is Lupin’s 3rd largest market and contributed 10% to our global revenues during FY 2017.

TAX rate:

Company recorded Earnings per Share (EPS) of ` 56.69 during FY 2017. The Company’s effective tax rate for FY 2017 was 27.6%.

Risks :

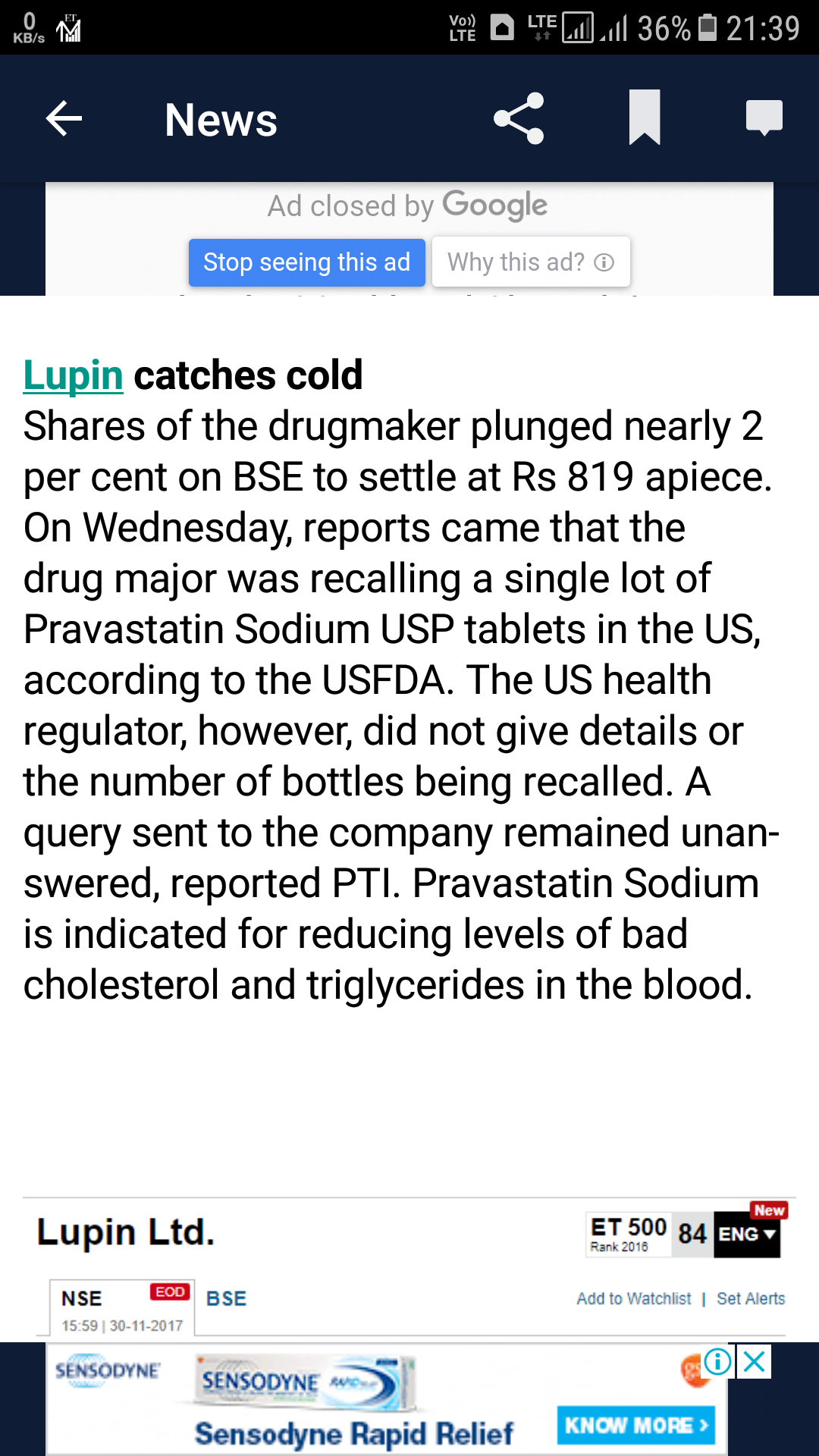

Regulatory Risks : Recently US FDA issues warning letter to Lupin’s manufacturing facilities at Goa and Indore for violation of good manufacturing practices.

Debt approx 7900 crores. However Debt to equity ratio is approx .6

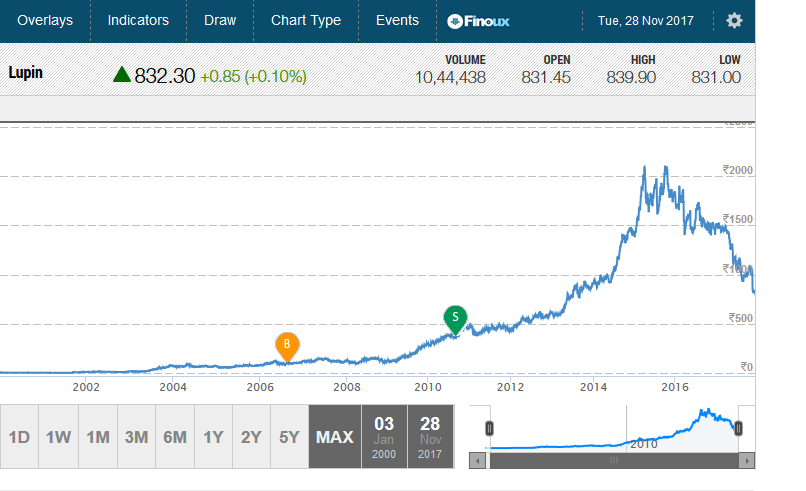

Stock has corrected approx 60% from All time high of 2100 to 830 in last 2-3 years. Whole pharma sector is in trouble from last 1-2 years , but I want to see if this can be a buying opportunity keeping holding period of 10+ years (expecting 12-15% CAGR return) considering managment is v good and they will come out of all troubles in long term.

Request people to share views on it.

Info Source - Annual report 2017

Disc : Invested