These will add lot of depth to the questioning, when added at the right place/sequence.

Will do the needful when I am back on Monday, hopefully in time before Ayush’s meet.

Really happy at how this has shaped up - with the active collaboration between Ayush & you, and others.

-Donald

Ps: hope we can get enough people interested each time in companies that merit these kind of a close look, find a nice way to incentivise this properly in future

One more question may be added. Peter Lynch always questioned the Company representatives while concluding his meeting by asking**" Which is the competitor you admire in your industry"**. This would give him a new link to the competitor and how they are performing.

Hi All, please see the attached link below. Another big risk of investing in a small company like this where the promoters decide to route all their personal expenses through the company accounts.

May I add one more question - what is obsolescence risk? I’m seeing very rapid inroads being made by LEDs in automotives, could that overwhelm halogen based players?

Previously I have lost money and reputation by investing in technology-challenged companies like Moser Baer and Samtel. In case of Samtel, they undertook expansion of CRTs in the belief that flat panel tech is many years away from full penetration. That proved to be their undoing, and they are a sick company now.

The company has recently passed resolution waiving Rs.2.45 crores paid on behalf of the MD Mrs. Usha Jain for medical treatment in India and US. Another Rs. 2 crores has been sanctioned for future treatment. I would like to know whether this is an acceptable practice.

From investor stand point, this look totally unacceptable as Vivek said earlier, this is personal expense and hence why company should pay for it. Management quality gets to question by these acts…

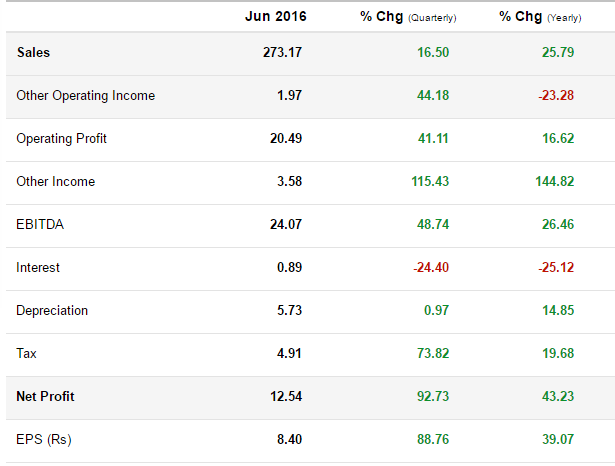

The Q4 results also look good (as the drop is only due to taxation). The stock looks interesting at 120 levels as it is available at 4 pe and 5% div yield.

Two independent directors have resigned simultaneously. Any idea why? Feeling a bit worried, since I am invested here. Sep-2013 results seem to be weak but in line with expectations.

A lot of good work was done here in the past but I see no activity over the last multiple quarters. I am invested in this stock and want to call out a few things for the group:

)- Co continues to earn decently even though not as high as in the previous year.

)- As BJP govt has come to power there is likely to be a pick up in the economy and the auto sector will lead the recovery.

)- Some of the significant capacity expansion that they have talked in the past should become more visible in FY 2015.

The big unknown of course is the management and how committed they are to rewarding the minority shareholders. I wonder if there has been any conversation with management on some of the questions that have been put together in this thread.

I bought this stock few months ago around Rs 115-120 range. Since then have made decent profit. Still holding but watching very closely. When I invested in this stock (or similar ones in the market) I look at these stocks as cigar butt stocks. The kind of stocks Graham, Schloss and Buffet (before 1960) would have bought fordiscrepancybetween price andintrinsicvalue. The amount of analysis and probing done on this thread is phenomenal. I saw this thread only today.

I look at this company as…commodity (without any Moat), totally cyclical, small, at the mercy of few big customers, with not-so-great corporate governance… kind of company. Just a Cigar butt. Period! Forensic analysis done by Anil Kumar and few others is apt for such stocks. Too long term forecasting of business prospects, revenues and profits do not make sense for such companies.

You enter into such stocks only to exploit price-value arbitrage and then get out before music stops.

Lumax Auto has 70% share in manual Gear market in India. They are getting into automatic gear which has great utility on crowded Indian roads. Right now Automatic Gear are 5% share in Indian market. So plenty of scope for automatic gear technology in India. That product will be game changer for this company. The revenue in this segment may grow at 30% CAGR for next few years. They have tie up with Mannoh which is tech leader in this segment.

9 new products developed exclusively for exports. They will fetch better margins.

70% capacity utilization at the moment. due to operating leverage PAT margin will grow more than sales growth.

Technology tie ups with gloabal leaders

a. Gear and Parking brake system- Mannoh, Japan

b. Exhaust system- Cornglia group, Italy

Trying to get into defense market with logistic support service offering for aerospace and defense. Services so No capex needed.

Air intake business is growing business and will be meaningful in next 2-3 years.

Seat frames and seat mechanism will be growth business. JV with global leader.

Supply of molded parts started to HMSI.

GOI has envisaged growth of 3.5 to 4 times growth for Indian auto component industry under Make in India. Policies and support from government should help the sector. By 2026 Auto components sector is projected to be $220B from $39B in 2015-16. Expected to grow at CAGR 19%.

10 Zero Net debt. In last 4 years Gross block increased by 160% all through internal accrual. All this investments should result in good sales growth in near future.

Working capital days are 25 days.

Net cash from operations was 49.15 Cr in FY2015-16. And Net Capex was 30 Cr.

Valuation:

My estimate of EPS for FY18 is between 45 and 50.

Lumax Auto holds 525,000 shares in Lumax Industries. At CMP of 775/- (28-Nov-2016) it is worth 41 Cr. Cash on books is around 16 Cr. in Q2 BS.

Key Concerns:

Bajaj Auto sales is 30-35% of sales. Lot of dependence.

Too many Related party transactions. Corporate governance seems questionable.

Q3 FY18 Consolidated Performance

Revenue (Net) up by 26% YoY to Rs. 277 Cr

EBITDA grew by 68% YoY to Rs. 30 Cr; Margin at 10.7%

PBT grew by 203% YoY to Rs. 23 Cr; Margin at 8.2%

PAT (after MI) grew by 208% YoY to Rs. 13 Cr ; Margin at 4.7%

The stock is cheap compared to other auto ancillaries for sure. But the TTM PE in screener shows 15. I am not sure where did you get this PE .May not be a consolidated PE.

LOGIES THIS QUARTER.

LOGIES THIS QUARTER.