Very strong results by Lumax auto technologies in Q1 again

revenue grew 27% YOY on a consolidated Basis

PBT rose by 68 % YOY

PAT rose by 67 % yoy

EDITDA at 32.3cr vs 20.17 cr YOY

EBITDA margins stood at 9.7 yoy vs 7.7 Yoy

Very strong results by Lumax auto technologies in Q1 again

revenue grew 27% YOY on a consolidated Basis

PBT rose by 68 % YOY

PAT rose by 67 % yoy

EDITDA at 32.3cr vs 20.17 cr YOY

EBITDA margins stood at 9.7 yoy vs 7.7 Yoy

Lumax Auto Tech 1Q19

Numbers & Others

Standalone business – Majority of revenue comes from lighting systems; major customer includes bajaj auto and HMSL. 100 new SKUs already launched in 1Q19 vs estimates of 200 new in FY19 – 202crs (112crs) 9.4%. Lighting business – Revenue stand at 80crs, growth of 7% due to accounting change by Bajaj Auto. Growth would have been +35% (adjusted for Accounting changes) on Like for Like basis. Margin in lighting is 10-12% and around 0.5% positive impact due to change in accounting. Topline to be lower by 60-70crs due to change in accounting at Bajaj. Revenue growth excluding the impact of total control of Gill Auston would be 36-37%. Impact of management control is ~11crs for the quarter.

DK auto – Revenue of 77crs/80crs and margins in mid double digit. Revenue declined due to change in accounting change. Like on like growth is +20%.

Gill Auston – Taken Management control in this business. In 1Q19 positive impact on revenue is ~11crs. Revenue would be higher by 50crs inFY19 due to this consolidation.

Accounting change impact - 1Q impact was around 15crs. We expect topline to be negatively impacted by 60-70crs and 25-30% growth on consolidated levels.

Gross margin – would be remaining protected from ups and downs.

EBITDA – expects margins to improve going ahead. This is sustainable. Expects +150bps margin expansion. Margins would be 11.5-12% . we would like to grow at a healthy pace.

Revenue at full capacity - Company expects at this capacity, they can do max 1400crs of revenue. Asset turnover is ~3-3.5x.

Bajaj Auto - contributed 360crs for Fy18. Bajaj’s focus on volumes won’t hurt our margins. On the other hand, we expect our volumes to increase in conjunction with Bajaj’s volume. Overall, we expect atleast 10% growth from Bajaj’s account.

Capex – This year we expect capex of ~60crs and don’t foresee anything significant over next two years. To meet demand from Bajaj, we would be spending 15-20crs in Pune and xxx (one more plant) and there we could generate 60-70crs of additional revenue due to this expansion.

Per vehicle contribution - with Bajaj ranges from INR 800 to 2500 currently on different model and expect it to increase further going ahead

Defense JV – we ceased management control and handed over the control to our JV partner

Product wise

Seat metal business - Business is expected to improve due to growth of Bajaj auto. We had added two new product in 3/4Q last year and now seeing traction for these products. These products would add to the topline. Management expects to clock 130-150crs and expect to grow in line with market growth from FY20 onwards.

Gear Shifter – Company currently has 70-75% market share. Growth was ~8%. Growth was subdued because Toyota used manual gears in new car. Also new Maruti plant in Gujarat has cars running on manual gears. Since manual gears have lower selling price hence topline also was lower despite increase in volume. However, management expects at early double digit growth in FY19. We are also targeting export market in Gear shifter for our existing customers.

After Market sales - In next 3 years we expect to double our sales. As a strategy we are expanding our products pipeline and have both frontend and backend strategy. Currently we have 7 products in after market and want to fully optimise market shares before we start launching new products. We have strengthened supply chains. Commit investments for development of our products. One of the participant had some scuttlebutt and said Lumax is clearly gaining more shelf space.

Acquisition of new business in SMT – This acquisition is directly linked to LED in auto space. Our customer remains Lumax Industries. We have started supplying to Activa through Lumax Industries from Feb 2018. Expects margins to be in mid double digits like margins in after market sales margins.

Oxygen sensors - This division will come in play for BS-VI in FY20. This is done for 2W market. We already have order book with 1 customer and 2 is still under approval. This will be aligned with customers launches.

EV - We are developing a product for Bajaj auto in EV space. We have great partnership with them and will develop products for them in future. We are evaluating product lines where regulations are governing and looking for growth in this segment.

Excellent results QoQ and YoY.

Very very strong set of numbers. This company has been very very steady in earnings.It will be a true compounder and rerating is much awaited,

Lumax Auto Tech recently sold its PCB unit to Lumax Industries. The PCB business had seen improvement of sales by 70%, contributed more than 10% of group sales, had higher EBITDA margins than group average, and contributed 21cr of EBITDA. Despite significant growth the decision to close the business and sell the assets for 22cr, for roughy 1x EBITDA multiple was made. As per the management this was done to address customer concerns (a large OEM) because of recurrence of certain quality control issues at Lumax Auto Tech in the PCB unit. Stanley Electric, one of the promoter shareholders in Lumax Industries, agreed to help provided the business was moved into Lumax Industries. Grateful for inputs from members on whether this could be a plausible reason or the sale appears to be a “value transfer” and a minority unfriendly move?

Hey @ayushmit, do you still track this? It seems valuations are coming close to the 2013 levels when you first wrote about it (~1 P/book), only difference this time is the slightly higher debt on the balance sheet. A business which generates ROEs in excess of cost of capital should trade at a premium to their book. Thoughts?

Not sure if anyone is tracking this company of late. Want to highlight some interesting developments in last 6 months –

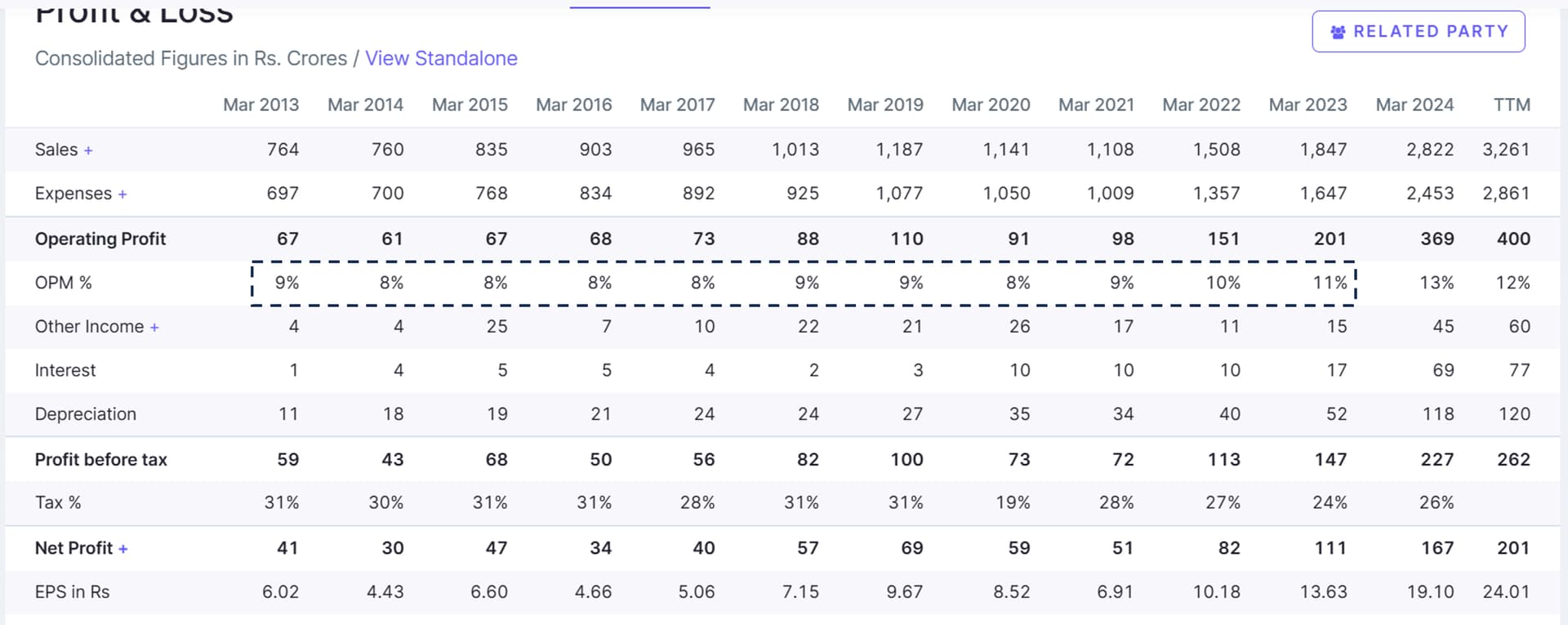

Comparison of key metrics over last 3-4 years

| FY 17 | FY 18 | FY 19 | FY 20 | FY 21 | TTM | ||

|---|---|---|---|---|---|---|---|

| Sales | 965 | 1013 | 1187 | 1141 | 1108 | 1297 | |

| No. of Plants | 27 | 27 | 29 | 29 | 33 | ||

| No of JVs | 8 | 8 | 8 | 9 | 9 | ||

| Margins | OPM | 8% | 9% | 9% | 8% | 9% | 10% |

| CFO | CFO | 64 | 95 | 56 | 76 | 98 | |

| CFO / EBITDA conversion | 88% | 109% | 52% | 84% | 100% | ||

| Valuations | M Cap / Sales | 0.77 | 1.15 | 0.60 | 0.44 | 0.93 | 0.72 |

| PE | 19 | 21 | 13 | 11 | 23 | 15 | |

| ROCE | 17% | 20% | 21% | 15% | 14% | ||

| Contribution of After market (higher margin biz) | 15% | 15% | 17% | 18% | 20% |

• Robust CFO and healthy conversion ratio

• Contribution of after market is growing steadily from 15% to 20% - company intends to double the revenue from after market in next 2-3 years. Thereby should also improve margin profile

• Valuations: seems to be similar to the valuations trading in FY 17

• Company has guided to outperform the industry. (SIAM estimates industry to grow at 14 to 15% while company is confident of growing at 20%+ - covered below in the key notes from the Q1 call.

Key points from the Q1 call –

Business update

EV space – will take some time unless EV is able to penetrate in wider 2 wheeler mkt. No component is at risk owing to EV segment making inroads

Strategy of electronic & plastic - will help in some of the 2-wheeler EV models

Gear shifter business-

125 cr of revenue in last FY. Expecting good traction in this FY. Manual transmission (MT) - per vehicle realization is 350 to 500 Rs, depending on the model. Technology is changing towards AT. Expect 3x to 5x increase in revenue in the segment, as we move towards the Automatic AT technology . AT is only about 20% of the portfolio. 80% is Manual. So good headroom for growth

Urea tank – Lumax Cornaglia is the only segment that showed a growth in last FY despite Q1 being a washout. Has a good order book & looking at promising growth in coming years

Aftermarket

Alps Alpine JV

Alps Alpine Is a global player - 8-billion-dollar revenue. This will be one of the key cornerstone JVs for the future of company. This would probably the largest JV partner in terms of revenue. Product category is very futuristic.

Company is fundamentally going to focus on sensorization & electronification. In which Alps Alpine is a leader globally. They manufacture components which cater to this product line. Product category is mainly electric components.

Conducting feasibility study currently. Scalability of this JV will be much faster – as compared other JVs in the past. Already in talks with Maruti Suzuki.

Outlook on JVs & revenue contribution form JV

JV of subsidiaries contribute 20% of consolidated revenue. In next 3 to 4 years – JV & subsidiaries will garner 33% of total revenue.

Majority of the revenue from JVs is highly localized. There is no high dependability on import content. Most of them fully manufactured locally.

New order wins of 120 Cr this qtr

Electronic & plastics continue to be main foray

**Outlook for this FY –**Given the performance of last 45 days, if similar momentum were to continue – gave guidance of outperforming the industry.

SIAM estimates industry likely to grow at 15 to 18% full year. Has track record of beating industry growth - so hopeful of 20%+ growth in current year but can throw more light at the end of Q2

Export space

Exports continues to be a key focus area In the long term strategy. Through most of the JV partners, company is looking to utilize India’s production base for some of global plant requirements & derive some cost advantage. Looking to start exports through partners. Case in focus would be Lumax Mannoh (which has mkt leadership in domestic mkt). Some inroads made already through Cornaglia in Indonesia too.

Gross margin – While pricing pressure has impacted gross margin for OEM and other players, Lumax sequentially – has improved gross margin. Have been maintained around 32-33% mark. Have seen some escalation in raw material side. Don’t see any pressure on Gross margin as most of the OEM do compensate the company for the escalation in raw material.

Acquisition of majority stake in IAC India business

Key highlights

Q3FY24 results - https://www.bseindia.com/xml-data/corpfiling/AttachLive/4a93bd5d-47c7-46ad-8f3f-cc4704d5b74b.pdf

Q3FY24 earnings call recording - https://www.youtube.com/watch?v=tckyTAbLC4A

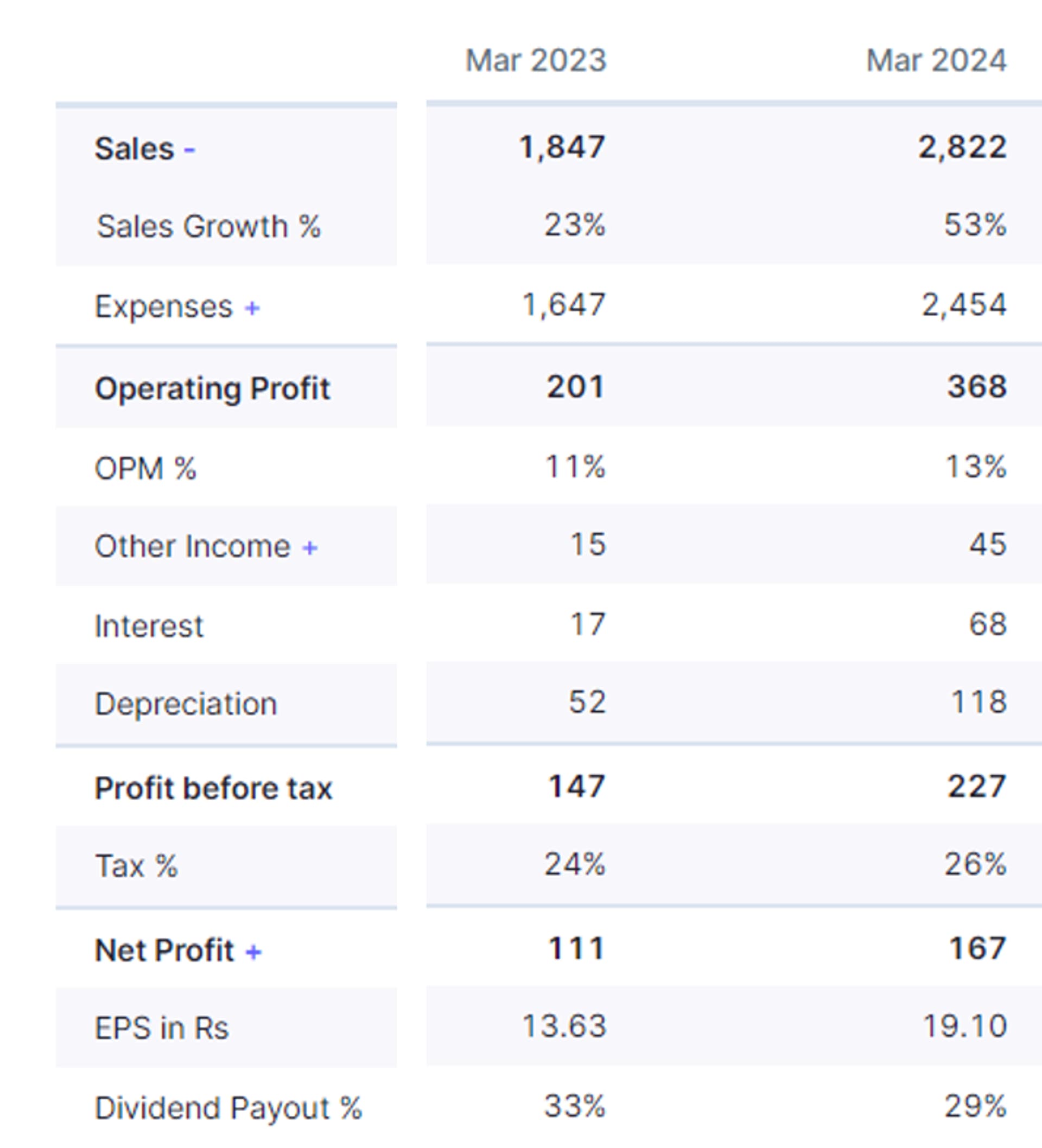

Sales have grown 65% YoY and OPM have expanded to 14%

Q2FY24 concall management had indicated the following

The total order book of Lumax Auto Technologies Limited is reported to be INR 1050 crores, with 93% of this being new business. The electric vehicle (EV) segment contributes to 40% of the total order book value.

Breakdown and Realization:

Some of the notable joint ventures other than IAC and their orderbook

Q3FY24 concall highlights:

Growth in the two-wheeler segment has been buoyed by the festive season and weddings, contributing to an uptick in demand. Nevertheless, Lumax’s standalone business for frame and plastic components has experienced a decline, attributed to weaker demand for Platina and CT models, witnessing a 15% and 40% decrease in demand, respectively. Despite this downturn, Lumax, as the exclusive supplier for certain components, reports robust demand in the premium bike segment. Lumax is strategically aiming to expand its share of the customer’s wallet by enhancing the value of its offerings, including the addition of paint or coating services for the chassis of these premium bikes. The company already boasts a partnership with KTM and supplies components for some of Bajaj’s electric vehicle (EV) variants. Efforts are underway to extend its supply chain to include the Pulsar platform, indicating Lumax’s commitment to diversifying its product line and capitalizing on new opportunities within the evolving two-wheeler market.

The tailwind in the auto sector are

a. Increased safety norms - e.g Bharat NCAP which will benefit large Tier 1

b. Emission norms.

The order book remains at 1100 Cr (IAC Orderbook being 600 - 650 Cr) and is expected to realise 50% by FY25 and 30% by FY 26.

40% of the orderbook is from EV - Mahindra Born electric and Bajaj EV.

The company expects a topline growth of 25% in FY25 driven by the JVs and IAC India.

chart also looks great with consolidation ongoing for the last 6 months and volumes are high as well.

disclaimer : Tracking, reading the company and updating this post on the go.

Keen to restart this thread on Lumax Auto . My understanding is that it one of the rare good Auto OEMs still available at reasonable valuations . Any Views pls

Sure

Lumax Auto Q4

Revenue at 757Cr vs 493 Cr YoY - excellent , QoQ flattish 3.4% up

PAT at 51Cr vs 23Cr YoY

OCF 226Cr vs 146Cr YoY

Registered certain FVOCI loss on finanial asset of 3.84Cr

Good dividend 5.5Rs /share , 275% on face value

Margin down sequentially but IAC was margin accreditive business so that’s disappointing . Not happy with the dividend payout being so high despite debt being high - let’s discuss futher after con call

Q4FY24 concall

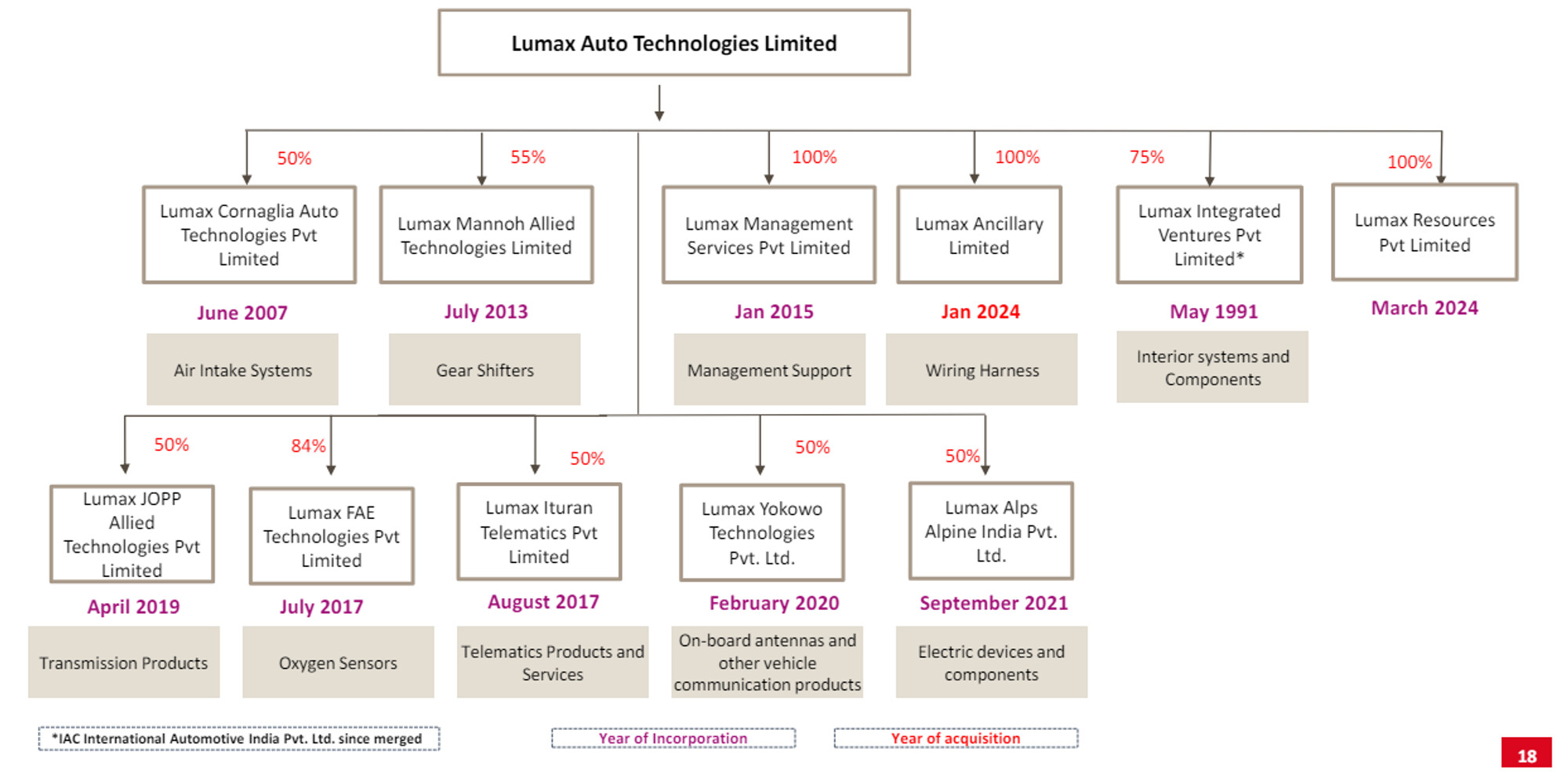

corporate structure of Lumax

[quote=“GourabPaul, post:49, topic:296, full:true”]Q3FY24 earnings call recording - https://www.youtube.com/watch?v=tckyTAbLC4A

Sales have grown 65% YoY and OPM have expanded to 14%

Q2FY24 concall management had indicated the following

The total order book of Lumax Auto Technologies Limited is reported to be INR 1050 crores, with 93% of this being new business. The electric vehicle (EV) segment contributes to 40% of the total order book value.

Breakdown and Realization:

Some of the notable joint ventures other than IAC and their orderbook

Q3FY24 concall highlights:

Growth in the two-wheeler segment has been buoyed by the festive season and weddings, contributing to an uptick in demand. Nevertheless, Lumax’s standalone business for frame and plastic components has experienced a decline, attributed to weaker demand for Platina and CT models, witnessing a 15% and 40% decrease in demand, respectively. Despite this downturn, Lumax, as the exclusive supplier for certain components, reports robust demand in the premium bike segment. Lumax is strategically aiming to expand its share of the customer’s wallet by enhancing the value of its offerings, including the addition of paint or coating services for the chassis of these premium bikes. The company already boasts a partnership with KTM and supplies components for some of Bajaj’s electric vehicle (EV) variants. Efforts are underway to extend its supply chain to include the Pulsar platform, indicating Lumax’s commitment to diversifying its product line and capitalizing on new opportunities within the evolving two-wheeler market.

The tailwind in the auto sector are

a. Increased safety norms - e.g Bharat NCAP which will benefit large Tier 1

b. Emission norms.

The order book remains at 1100 Cr (IAC Orderbook being 600 - 650 Cr) and is expected to realise 50% by FY25 and 30% by FY 26.

40% of the orderbook is from EV - Mahindra Born electric and Bajaj EV.

The company expects a topline growth of 25% in FY25 driven by the JVs and IAC India.

chart also looks great with consolidation ongoing for the last 6 months and volumes are high as well.

disclaimer : Tracking, reading the company and updating this post on the go.

[/quote]

Disclaimer - Invested

LATL Q1 Financial.pdf (5.4 MB)

LATL Q1.pdf (3.8 MB)

IAC International .Automotive India Private Limited: The Company will provide a Corporate Guarantee in lieu of the existing Corporate Guarantee to secure the refinancing of the loan provided / to be provided by Banks/ Non Banking Financial Companies (NBFCs)/ Financial Institutions to IAC up to a maximum amount of Rs. 250 Crores.

To seek approval of the Shareholders with respect to the enhancement of limits for giving loan, guarantees, providing securities and making investments by the Company under Section 186 of the Companies Act, 2013 for an amount of Rs.1,000 Crores (Rupees One Thousand Crores only), as recommended by the Audit Committee.

will see , if any update on concall

Lumax Auto Technologies -

Q2 FY 25 results and concall highlights -

Q2 results -

Revenues - 842 vs 700 cr, up 20 pc

EBITDA - 118 vs 99 cr, up 18 pc ( margins @ 14 vs 14.2 )

PAT - 43 vs 28 cr, up 56 pc

H1 results -

Revenues - 1598 vs 1332 cr, up 20 pc

EBITDA - 223 vs 187 cr, up 19 pc ( margins @ 14 vs 14.1 pc )

PAT - 74 vs 50 cr, up 51 pc

Product wise revenue breakdown for H1 -

Advanced Plastics - 907 vs 775 cr, up 17 pc

Mechatronics - 46 vs 26 cr, up 76 pc

Structures and Systems - 338 vs 306 cr, 11 pc

Aftermarket - 187 vs 183 cr, up 2 pc

Others - 119 vs 41 cr, up 191 pc

Total - 1598 vs 1332 cr, up 20 pc

Segmental revenue breakdown for H1 -

2+3 Wheelers - 25 pc

PVs - 50 pc

After Mkt - 12 pc

CVs - 9 pc

Others - 4 pc

Customer Wise breakdown of revenues for H1 -

Mahindra & Mahindra - 26 pc

Bajaj Auto - 15 pc

After Mkt - 12 pc

Maruti Suzuki - 8 pc

Honda 2Ws - 5 pc

LIL - 8 pc

Tata Motors - 4 pc

Others - 22 pc ( Daimler, Toyota, VW, Fiat, MG )

Q2 demand was subdued due lower govt spending, prolonged monsoons, entire ‘shradh’ period falling in Q2. Oct onwards, the auto Industry is witnessing better demand trends and lowering of dealer level inventory levels

2Ws continue to do better. Expecting a recovery in CV cycle led by increased Govt Capex in H2

Company is focusing on areas like ADAS, Electronics Integration, Software Integration and HMIs as future growth areas

Increasing premiumisation in the 4W industry augurs well for the company’s advanced plastics division ( their biggest division ). This division draws 70 pc of its sales form 4Ws

Mechatronics division saw huge growth acceleration in revenues which grew by 76 pc in H1 ( @ 46 vs 26 cr ). Order book for this division stands @ 175 cr

Aftermkt sales are showing signs of sales pick up wef H2

Company’s total overbook ( across all divisions ) stands @ 1050 cr ( across all divisions ) with EVs contributing 40 pc to the order book

H2 prospects look bright with several new model launches that are lined up by OEMs

Capex lined planned for FY 25 stands @ 130-140 cr out of which 30 odd cr have been spent in H1

Company had acquired IAC India’s Operations from their parent in Feb 23. IAC is a tier -1 supplier of Interior and Exterior systems for companies like - Maruti Suzuki, VW, M&M etc. IAC’s facilities current capacity utilisation stands @ 85 pc or so and are doing 17 pc kind of EBITDA margins

Lumax Auto acquired 60 pc stake in Greenfuel Energy systems in Nov 24. Greenfuel specializes in high-pressure CNG and hydrogen systems as well as fire and smoke detection systems for the automotive industry. The company’s strong relationships with OEMs and established technology partnerships have made it a trusted name in the industry

Greenfuel is expected to clock 300-350 cr of topline for full FY 26. Greenfuel’s results will start to get reflected in Lumax’s books wef Q3

Expect to double the revenues of Mechatronis division this year and expecting another doubling in FY 26

Company has some exiting product launches lined up for H2 in the aftermarket space. This should help propel this Segment’s sales

Good growth shown by Honda 2Ws is helping the company. Their Honda 2W business grew by 21 pc in H1

Company has won full service supplier award for some of Tata models wef next FY ( via IAC India ) for plastic interior products and interior lighting. They are also in continuous dialogue with Maruti Suzuki, Honda 4Ws, VW, Skoda for increasing their wallet share per car + winning new business for new cars

Looking to do 50 cr kind of revenues from the window switches, window raising sensors, throttle position sensors and in vehicle infotainment systems ( for 2Ws ) for FY 25 ( which is 50 pc higher than LY ). In FY 26, looking to cross 100 cr revenues from these segments

Mechatronics is another area where company expects rapid growth, albeit on a lower base ( expect to grow 70-80 pc in current FY in this segment ). Next yr again, they expect to double revenues in this segment to 200 cr

Greenfuel Energy should help the company win substantial business with Maruti Suzuki for their CNG models

Company’s JV ( Lumax JOPP ) has won substantial per whiter towers business with Maruti Suzuki. Revenues should start to flow in FY 26. The JV is also pursuing to make the electronic shifters to become a supplier to VW and JLR. This JV should have strong business potential over next 3-5 yrs. Management will give more clarity about its future roadmap in Q3 ending concall

Company expects EBITDA margins to improve in H2 vs H1. They expect EBITDA margins to be closer to 15 pc in H2

Disc: holding, inclined to add more, not SEBI registered, biased, not a buy/sell recommendation

Some of the important parts:

Now, understand revenue math’s for the Year 25,

Page 3 of 15 of transcripts, Growth drivers of revenue

Number one, increasing our content per vehicle. We continuously aim to expand our range of offerings for each vehicle, each segment, enhancing the value we provide to our OEM partners and strengthening our presence in the

auto market.

Number two, introducing new product categories, which are EV agnostic through new joint ventures and new acquisitions with prime focus on improving the top line and the bottom line growth.

Number three, maintaining our position as a trusted single source partner for major OEMs and delivering cutting-edge technology by drawing on the expertise of our global joint venture partners.

And number four, lastly, to meet the evolving demands of OEMs and drive sustainable growth, we are enhancing our own R&D capabilities significantly focused on technologies like ADAS, electronics integration, HMIs and software.

Club from 1 to 4 Points @ at least 10% growth will be coming on full year basis PLUS

Q by Harshil Shah: Okay, sir. And sir, any update on the new acquisition? Like can you share first half top line EBITDA margins of GreenFuel Energy Solutions Private Limited.

A by Anmol Jain: So for, let’s say, on a full year basis, we are expecting anywhere between INR300 crores to NR350-odd crores of revenues with a stronger EBITDA margin than what we are looking at currently across the most of our subsidiaries and joint ventures.

So, from 1 to 4 + Green fuel = Rs 2860 + 10% = 300 + Green fuel 300 = Rs 3400-3500 Cr

EBITDA 12-13%

PAT 5-5.25%

EPS 23-24/-

RoCE 22%

Client end: MnM and Honda Motorcycle is doing good but some pressure from other clients.

Page 15 of 15

Q by Amit Hiranandani: Right. Sir, any internal targets to take this margin ahead for the next 3 years perspective?

A by Anmol Jain: Absolutely, I think as the top line grows, as I already mentioned, we should be able to get the top line growing organically 50% more than that of the industry growth. So if the industry grows, let’s say, at around 8% to 10%, we should easily be looking at a 12% to 15% growth organically. And for that, with that organic growth with better operational efficiencies with the new subsidiaries scaling up, we should be able to expand those EBITDA margins further, perhaps from 14% to 15%.

Q3 FY 25 Highlights

Business Highlights

24% growth in revenue YoY; highest ever single quarter revenue in history of company

75% growth in Mechatronics over 9M period

18% growth in Advanced plastics over 9M period

Flattish 3% growth in Aftermarket in 9 M period – industry wide sluggishness

Order book 1360 crore

a. 30% will be in FY 26, 40% in FY 27 and rest in FY 28.

b. EV contribution to order book at 40%

c. 90% are new orders; so will have incremental impact on topline

Share of PV is increasing at 50% vs last FY (47% in 9M FY 24; 2-3 wheelers share at 25%; After market at 12% . Penetration levels of EV within PV segment expected to further increase next FY

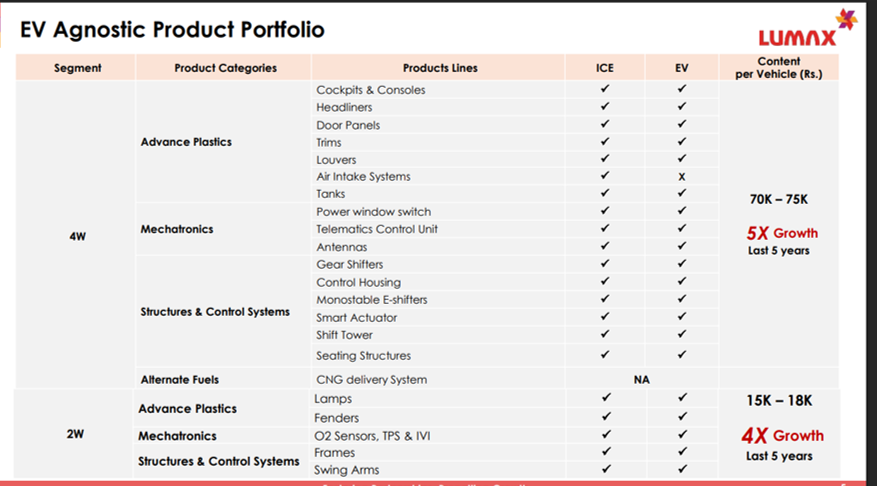

EV agnostic product portfolio

Segment wise deep dive

Other Highlights

OBD2 norms to be implemented from April 1 2025

What are OBD 2 norms?

| - | A welcome move from company’s perspective |

|---|---|

| - | Lumax FAE – has got into SOP with major 2 wheeler manufacturer in South |

| - | 50 to 70 cr revenue increase next FY – from secondary oxygen sensors which is mandatory from April 2025 |

| - | Full year capacity utilization likely to be 45% which was 10% last year. In talks with another OEM to fill up remaining capacity too. |

| - | Will increase content per vehicle for 2 wheeler by 800 to 1000 Rs per vehicle |

Future Outlook

My views and take

Also things seem to be changing / falling on right path for some of the other JVs

Likely tailwind - Increase in IT exemption limits announced in the Budget would mean higher disposable incomes. This coupled with the upcoming rate cut cycle should boost demand for auto sector in the near future.

Company seems to having multiple levers in place next FY, to ride the next leg of upcycle in Automotive sector

These metrics look good during the present volatile markets

Disc: Invested

Lumax Auto Technologies -

Q4 and FY 25 results and Concall highlights -

Segmental breakdown of revenues for FY 25 -

Advanced plastics ( like - cockpits & consoles, door panels, trims, air intake systems, tanks, headliners ) - 56 pc

Structures and Control systems ( like - gear shifters, control housing, smart actuators, shift tower, seating structures, swing arms ) - 20 pc

Mechatronics ( power window switches, antennas, telematics control units, O2 sensors ) - 3 pc

Aftermkt sales - 11 pc

Alternate fuels ( CNG delivery systems ) - 3 pc

Others - 7 pc

Customer wise breakdown of FY 25 sales -

Mahindra - 27 pc

Bajaj Auto - 14 pc

After Mkt - 11 pc

Maruti Suzuki - 8 pc

Honda Motorcycles - 5 pc

LIL - 8 pc

Tata motors - 5 pc

Others - 23 pc

PVs contribute to 53 pc of sales, 2/3 wheelers contribute - 22 pc, 11 pc come from Afermkt sales, 8 pc and 6 pc each from CVs and Others

Lumax Auto acquired 60 pc stake in Greenfuel Energy systems in Nov 24. Greenfuel specializes in high-pressure CNG and hydrogen systems as well as fire and smoke detection systems for the automotive industry. The company’s strong relationships with OEMs and established technology partnerships have made it a trusted name in the industry. Greenfuel is expected to clock 300-350 cr of topline for full FY 26. Greenfuel Energy should help the company win substantial business with Maruti Suzuki for their CNG models

Company had acquired IAC India’s Operations from their parent in Feb 23. IAC is a tier -1 supplier of Interior and Exterior systems for companies like - Maruti Suzuki, VW, M&M etc. IAC’s facilities current capacity utilisation stands @ 85 pc or so and are doing 17 pc kind of EBITDA margins

Company has won full service supplier award for some of Tata models wef next FY ( via IAC India ) for plastic interior products and interior lighting. They are also in continuous dialogue with Maruti Suzuki, Honda 4Ws, VW, Skoda for increasing their wallet share per car + winning new business for new cars

Q4 outcomes -

Revenues - 1132 vs 757 cr, up 49 pc

EBITDA - 165 vs 110 cr, up 51 pc ( margins @ 14.6 vs 14.5 pc )

PAT - 80 vs 52 cr, up 55 pc

FY 25 outcomes -

Revenues - 3637 vs 2822 cr, up 29 pc

EBITDA - 516 vs 413 cr, up 25 pc ( margins @ 14.2 vs 14.6 pc )

PAT - 230 vs 167 cr, up 37 pc

Sales of 4 and 3 wheelers inclined by 2 and 7 pc respectively in FY 25. 2W sales inclined by 9 pc, CV sales declined by 1 pc in FY 25. Company was benefitted disproportionately because of increasing mkt trend towards premiumisation and company’s clients benefiting out of it

IAC has recently commissioned 2 new facilities in Pune for 2 of Mahindra’s best selling EV models - XEV 9 and BE 6E. Company also supplies cockpit assembly for That ROXX. IAC grew by 35 pc in FY 25 with EBITDA margins @ 17.5 pc. IAC is now a 100 pc subsidiary ( they acquired the remaining stake recently ). IAC’s FY 25 revenues stood @ 1218 cr

Segmental growth for FY 25 -

Advanced plastics - 27 pc ( led by deeper penetration in premium vehicle segments )

Structures and Control systems - 8 pc

Mecatronics - 80 pc ( on a small base )

Green energy solutions reported a revenues of 110 cr for FY 25 ( acquired in late FY 23 )

After mkt sales - 10 pc

Capex for FY 25 was @ 177 cr

Company aspires to reach 16 pc kind of EBITDA margins by FY 28 and aims to hit 20 pc margins by FY 31. Can be a huge wealth creator, if this materialises

Wrt guidance, they believe, they can double their absolute EBITDA to 1000 cr form the current levels of 500 cr by FY 28

Other subsidiaries like - Lumax Ituran ( makes Telematics, FY 25 revenues @ 33 cr ), Lumax Yokowo ( makes antennas and other comm equipment, FY 25 revenues @ 21 cr ), Lumax Alps ( makes electric devices, FY 25 revenues @ 49 cr ) - are expected to grow @ 30-40 pc CAGR for next 2-3 yrs

Expect to keep growing the topline @ 20 pc CAGR for next 2-3 yrs ( on a consolidated basis )

IAC should now grow @ 10-15 pc CAGR for next 2-3 yrs ( after huge growth bump ups in last 2 yrs ). 90 pc of IAC’s revenues come from supplying cockpit and door panels for Mahindra’s vehicles. Currently in discussions with Maruti and Tata Motors - hopeful of winning some orders in future from these 2 OEMs

Capex plan for FY 26 @ 175 - 200 cr for the consolidated entity

Long term Debt / Equity @ 0.51 ( at consolidated levels ) - should decline if company doesn’t make any acquisitions in FY 26. In case of acquisitions, may rise upto 0.8 kind of levels

Lumax Green fuel should be able to clock revenues of around 350 cr for FY 26 ( company holds 60 pc stake in this ). Revenue recognition in Lumax’s consolidated numbers for FY 25 was @ 110 cr @ 20 pc EBITDA margins ( because they made the acquisition in Nov 24 )

After mkt sales are showing good pickup wef Q4, continuing into FY 26 vs first 9Ms of FY 25 which were sluggish

Disc: holding from lower levels, inclined to add on dips, not a buy/sell recommendation, not SEBI registered

FY27 Revenue = 5238 Cr (+20% YoY)

Adv plastics : premiumization + new BEV models

Mechatronics - 4JVs - 80% cagr backed by order book

IAC - 10-12% cagr

Greenfuel - full year ramp up in FY26 - 20% growth aaegi in FY27

AfterMkt - 10-12% + new products

FY27 Ebitda = 812 Cr (15.5%) - Mngt n 16% aim by fy27 as per management words

FY27 Dep = 128Cr is right now so by fy27 it can be 160 ballpark ( due to 1750-200cr capex /Y)

PBT using all above - 562 approx

tax @ 25% PAT = 400-425 Cr