Ideally lt food shouldn’t rerate coz of this

Krbl had corporate governance issue in the past as well

Ideally lt food shouldn’t rerate coz of this

Krbl had corporate governance issue in the past as well

Hello All,

Headwinds which I can see:

Please let us know your opinion on these points.

yes, you have pointed out some burining issues and I also think these are critical headwinds…now we have to monitor how managment steer clear through this doldrum

Headwinds 4.

US policy shift favouring import of Basumati from Pakistan

The positive to consider is Supreme court ruling on tariffs. They might be declared illegal.

will not that be compensated by daawat entering Saudi market ?

Pakistan alone cannot fulfill the demand of basmati for whole world. India share in basmati production is almost 70-80% of world requirements of I am correctly remembering the fact. And also keep in mind Pakistan is equally affected by recent floods in Punjab.

World of basmati is full of uncertainty, I may be wrong in my thesis. Till the time , we hear the management in concalls things are difficult to predict.

Disclaimer: Holding only CLSA.

I am little surprised to see, people r comparing Pakistan to India in terms of Basmati Production. I think, we need to go through couple of LT Food concalls, where they mentioned, total production of Pakistan, is significantly lower than India. What India cos hv done earlier, is buy Pak Rice at lower cost and traded ..but they stopped that practice nw.

Even assuming a 14-15% growth rate for LTFOODS, intrinsic valuation is only coming to around ₹240 per share. At current price, 25-27% growth is already priced in. Don’t see that happening.

Interesting acquisition. The company continues to expand value added products.

Valuations can fluctuate, but the underlying business is definitely on an upward trajectory. This would increase their addressable market size and possibly expand margins

Disclosure: Invested and biased

I was so happy that they bought something for ~0.25 times Valuation of Sales. Such amazing promoters !

How could they buy so cheap? Was it in trouble or is it low yield business?

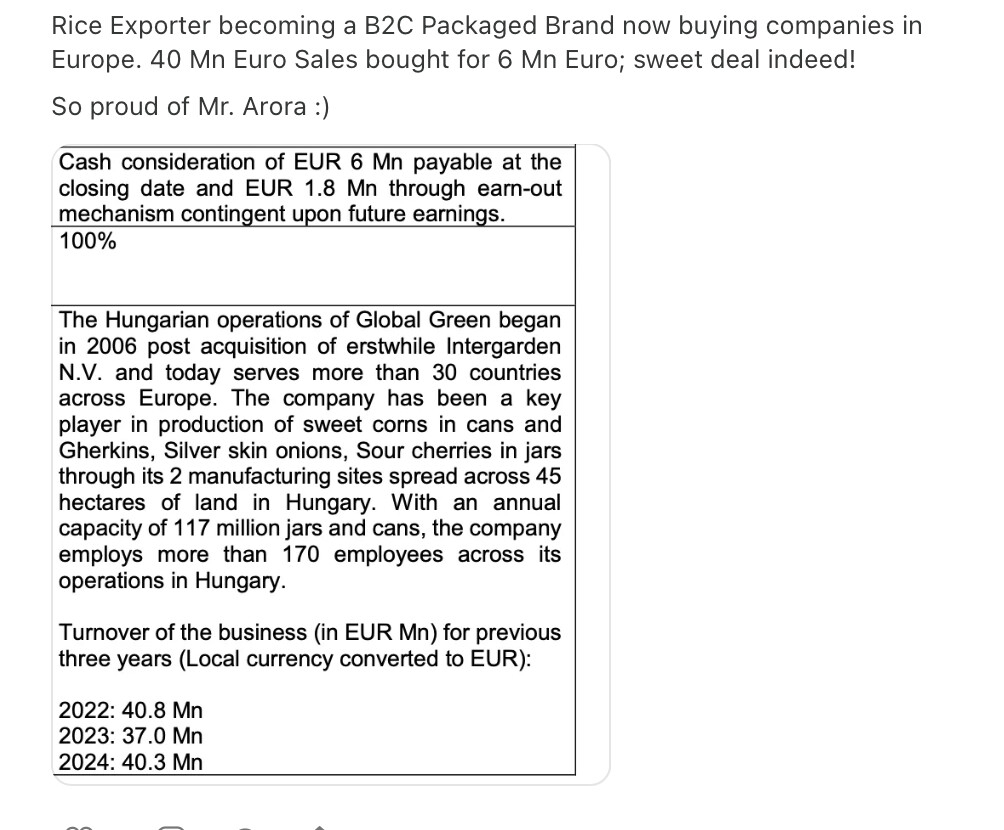

Deal Snapshot

| Parameter | Details |

|---|---|

| Buyer | LT Foods Europe Holdings Ltd. (wholly owned subsidiary) |

| Enterprise Value | € 25 million (~ ₹ 225 crore) |

| Equity Value / Cash Consideration | € 6 million upfront + € 1.8 million earn-out (based on future earnings) + assumption of borrowings |

| Funding Mode | All-cash, internal accruals |

| Expected Closure | Q3 FY26 (subject to FDI clearance in Hungary) |

| Ownership Post-Deal | 100% wholly owned step-down subsidiaries |

| Target Turnover (FY24) | € 40.3 million (~₹ 360 crore) |

| Workforce | 170 employees; 2 plants over 45 acres |

| Product Portfolio | Canned Sweet Corn, Gherkins, Silver Skin Onions, Sour Cherries in jars |

| Distribution Reach | > 30 countries in Europe |

**** Strategic Rationale

| Theme | Data-Based Insight | Investment Significance |

|---|---|---|

| Diversification | Entry into € 15 billion European shelf-stable fruits & vegetables market | Reduces dependence on basmati rice (~80% of revenues); adds a defensible second food vertical. |

| Geographic Expansion | Adds a third European manufacturing hub (after Netherlands & UK); strengthens Central & Southern Europe presence | Improves logistics reach and hedges geopolitical or currency risk within Europe. |

| Product Synergy | Canned foods fit into LT Foods’ RTH/RTE & processed-food roadmap | Enables product cross-selling through existing European retail network; complements Daawat’s distribution chain. |

| Cost Advantage | Hungary base offers lower labor & energy cost vs. Western Europe | Enhances competitiveness and gross margin potential for European portfolio. |

| Integration Platform | Leverages LT Foods’ European back-end (Royal Europe, Leev Organic) | Creates vertical synergies across sourcing, packaging, and supply-chain management. |

**** Financial & Operational Outlook

| Metric | Observation | Outlook Impact |

|---|---|---|

| Revenue Contribution | € 40 million turnover (~₹ 360 crore) ≈ 4% of FY25 consolidated revenue (₹ 8,770 crore) | Moderate top-line addition in FY26; meaningful from FY27 after integration. |

| EBITDA Margin Potential | Processed canned foods typically deliver 10–12% margin; below basmati’s 12–13% | Near-term margin dilution likely; offsets via scale + brand premium over time. |

| Capex/Investment Load | € 6 mn upfront (< ₹ 55 cr) manageable from cash balance (> ₹ 900 cr est.) | No material balance-sheet strain; efficient deployment of surplus cash. |

| ROCE Outlook | Short-term dip (integration costs), recovery as utilization scales > 70% | Incremental ROCE expected ≥ 15% post FY27. |

**** Key Risks / Challenges

| Risk | Description | Mitigation |

|---|---|---|

| Integration & Execution | Multi-country (HU-UK) integration; legacy borrowings to absorb | LT Foods has prior M&A track record (Golden Star, Jackson Rice); synergy plan already mapped. |

| Commodity Sensitivity | Input crops (corn, gherkin, cherries) are weather-sensitive | Hungary’s EU-regulated agri ecosystem offers moderate price stability. |

| Regulatory & FDI Approvals | Deal subject to Hungarian FDI clearance | Low probability of rejection; routine food-sector approval. |

| Margin Dilution Risk | Entry into lower-margin processed foods vs. rice | Offset by diversification benefit and scale economics. |

**** Investment View (Summary)

| Aspect | Assessment |

|---|---|

| Strategic Fit | Strong – aligns with long-term pivot from commodity rice to branded packaged foods. |

| Financial Impact | Neutral in FY26; accretive from FY27 onward as synergies unlock. |

| Balance Sheet Impact | Minimal leverage impact; internally funded. |

| Valuation Lens | Acquisition EV/Sales ≈ 0.6× – reasonable vs. EU food peers (0.8–1.2×). |

| Red Flags | None material; only execution and integration pace to monitor. |

These Hungarian units are part of another Indian group.

Manufacturing Profile - https://globalgreengroup.com/manufacturing/

Credit Rating - India Ratings and Research: Credit Rating and Research Agency India

Considering that 40 Mn Euro (~400 Cr Rs) was from these units, they constituted significant portion of selling group [Credit Rating - Consolidated 2023 Revenue = 786 Cr]

Highly likely that this is a distressed sale, hence the valuation.

But great acquisition from the management none the less. RTH revenue from FY25 = 188 Cr, will go to ~600 Cr by FY27 with this acquisition assuming 10% growth each year in existing business (~220 CR) and 400 Cr from new facilities over 5 quarters

Trump tariff threat on alleged dumping of Rice by India sends shockwave through Rice exporters like LT food, KRBL

Trump’s tariff threats on the Indian market aren’t new. While on interview, they specifically told India, Thailand and China dumping rice into country and announced 12 billion assistance to US farmers.

From LT Foods’ latest concall, 46% of revenue comes from North America, growing at 47% YoY. Their brands Royal and Golden Star are the #1 basmati and jasmine rice brands in the US, so losing this position won’t be easy but any long-term tariff pressure could create some setback. We need to check next quarter results and see how it pans out.

Meanwhile, the company continues to scale well in Europe and the UK, which now contribute 15% of revenue, growing at 37% YoY. They also announced a new manufacturing facility in the UK, which reduces dependency risk and improves local supply capability.

I think company also sourcing rice from Thailand too so it will impact on revenue if new tariff comes in place . Despite the news, stock well rebounded, means some how market acting smartly.

My view: According to management, the tariff impact has been fully passed on to consumers. We need to track this quarter and the next quarter’s sales closely.

Why was the company’s acquisition of global green group rejected? The doc states- In this regard, the Company has now received a decision dated 28th January, 2026, from the Ministry of National Economy, Hungary, rejecting the proposed acquisition on the grounds of identified national economic and sectoral risks.

Quarterly Performance/guidance tracker

| Column 1 | Column 2 | F | G | H | I |

|---|---|---|---|---|---|

| Guidance / Metric | Value as per Guidance + Announced in which Quarter Concall + Timeline | Q1Fy26 | Q2FY26 Status / Data (Only material info) | Q3 FY26 Actual / Latest Update | Status / Interpretation |

| Consolidated Revenue Target | ₹10,000 Cr by FY26 (Q4FY25 Concall)–>only 15% growth over FY25 8681 cr revenue | ₹2,500 crores (20% YoY growth)–> Exceeded | Q2: ₹2,765.7 Cr; H1: ₹5,273 Cr → tracking ahead of required run rate. | 9M FY26 revenue ₹8,085 Cr; Q3 revenue ₹2,812 Cr; growth +23% YoY | On track; current run-rate supports FY26 target |

| PAT Target | Maintain current PAT Groth of 21%(announced in Q1Fy26) | ₹168.50 crores (8.50% YoY growth)–> Missed | PAT growth ~+8.8% YoY → below target trajectory. | Q3 PAT ₹157 Cr (+8% YoY); growth lagging revenue | PAT growth slower due to brand & strategic investments |

| EBITDA Margin (Consolidated) | 12-14% Targeted (Q3FY25 + Q4FY25 Concall) | 12.1%–>Decline because of brand promotion spending–> withing range but lower side | 11.4% → below guidance range. | Q3 EBITDA margin 11.3% (down from 11.5%) | Slightly below target due to higher brand spend |

| Organic Segment Revenue Target | ₹1,000 Cr by FY26 (Q4FY25 Concall), | ₹293 crores (32% YoY growth) | H1: ₹583 Cr → on-track. | 9M FY26 Organic revenue ₹807 Cr (+15% YoY) | Likely achievable by FY26 end |

| Organic Segment EBITDA Margin | >14% by FY26 (Q4FY25 Concall), margin recovery expected from H2 FY26 and return to last year’s profitability (Q2FY26) ie 11% | 10% (down 200 bps YoY) | Q2 est. ~3% (H1 = 7%; Q1 = 10%) → margin dipped due to Europe ramp-up. | Current EBITDA margin ~6% (9M FY26), however improved from 3% in Q2, but still far behind target value of 11% | Temporarily depressed due to Europe expansion costs |

| RTH/RTC Revenue contribution | RTH/RTC to accelerate from Q4FY26 once new US capacity starts | 48 cr, EBITDA margin = -15% | 9M FY26 revenue ₹138 Cr; EBITDA margin –9% | Still in investment phase; scale not yet achieved | |

| UK Facility Contribution | UK revenue target £100 mn (~₹1,050 Cr) in 5 years | 80 cr | Facility operational; Europe/UK +31% YoY and 4 new UK retailers; no ₹ disclosed. | UK operations running; capacity operational but ramp-up ongoing | Long-term growth driver; contribution gradual |

| Freight Cost % of Revenue | Expected to Normalize from Q1FY26 (Q3FY25 + Q4FY25 Concall) | 5.70% | stable | N/A | Normalized; no cost pressure now |

| Working Capital Days | Watch for pressure due to inventory increase (Q4FY25) | 195 | Payables improved by ~15 days YoY (working capital eased). | Reduced to 205 days (from 227 days) | Improving working capital efficiency |

| Inventory Days | 277 (FY25) - Increase due to low RM prices and volume planning | 277–> normal level due to aging requriement of basmagti rice | Inventory build seen (change in inv. +₹164.9 Cr); no new days disclosed. | Reduced to 255 days (from 268 days) | Normalizing; still structurally high but healthy |

| Revenue from Saudi Arabia | ₹55 Cr in FY25; ₹9,650 Cr target in 5 years (Q3FY25 + Q4FY25) | 16 cr → High entry barrier & matured market | H1: ₹28 Cr, Q2: 12 cr (part of MEA footprint). | 9M FY26 branded revenue ₹35 Cr, doubled YoY | Small base but strong growth; early-stage expansion |

| Marketing Spend | Increased Spend; Continuous for consumer growth (Q4FY25 Concall) | Higher brand & digital spend → margin impact. | EBITDA margin pressured due to sustained brand spend | Strategic investment phase ongoing | |

| Organic Soya Challenge | Shift to Uganda sourcing to offset U.S. anti-dumping (Q3FY25) ii. Provisional CVD of 340.27% on FY23 exports; limited impact (₹4-5 crore) (announced in Q1Fy26 ) | Ongoing; expects favorable ruling by December 2025 | Public hearing Sept 16; final decision due Nov 17. | Final CVD ruling delayed to Feb 2026; operations continue | Risk contained; sourcing diversification underway |

| Global Green Acquisition | Deal worth ₹200 Cr; Margins 6-7%; Post-synergy ROE target >20% (Q4FY25 Concall) | No data | Deal EV €25M; pipeline revenue £40M; closing in 2–3 months. | Acquisition rejected by Hungarian Ministry; deal withdrawn and will not proceed | Deal Rejected |