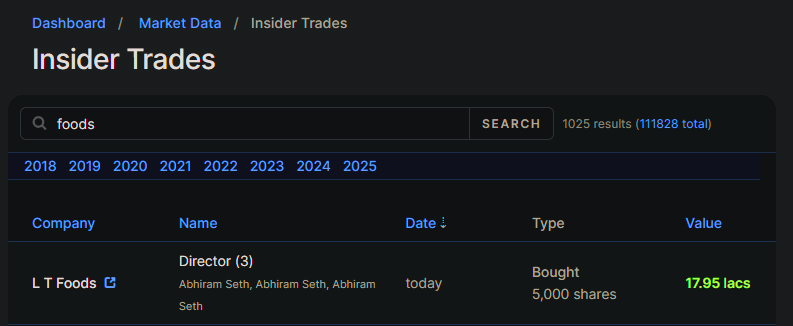

Anybody saw very high tax deduction on dividend from LT Foods? I am seeing 55% tax being deducted.

Other companies’s dividend email mentioned 0% tax deduction.

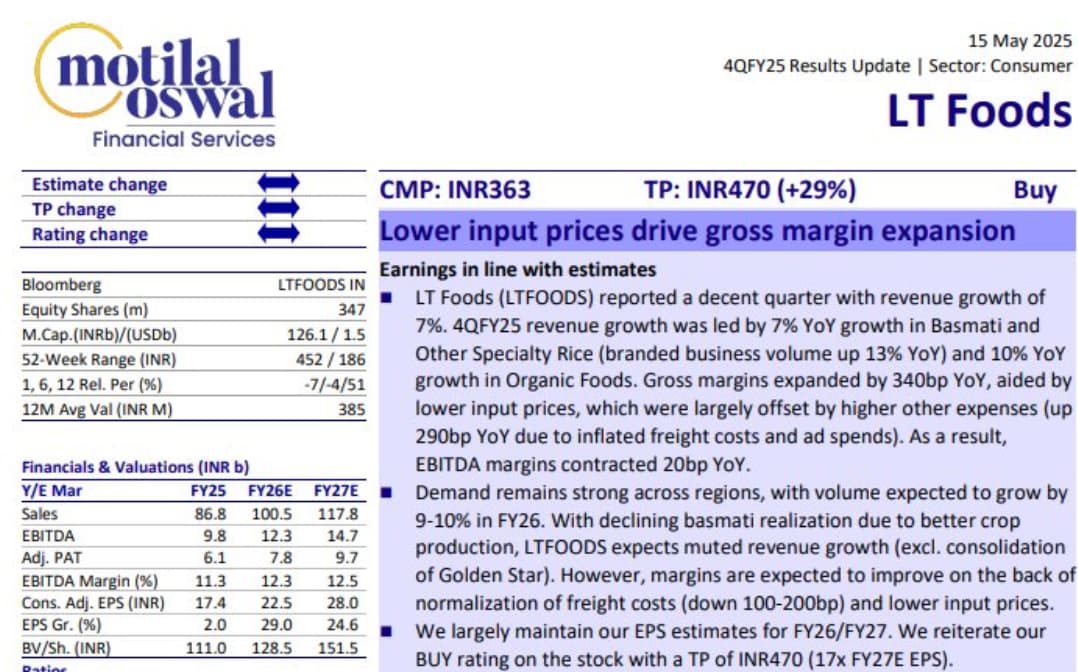

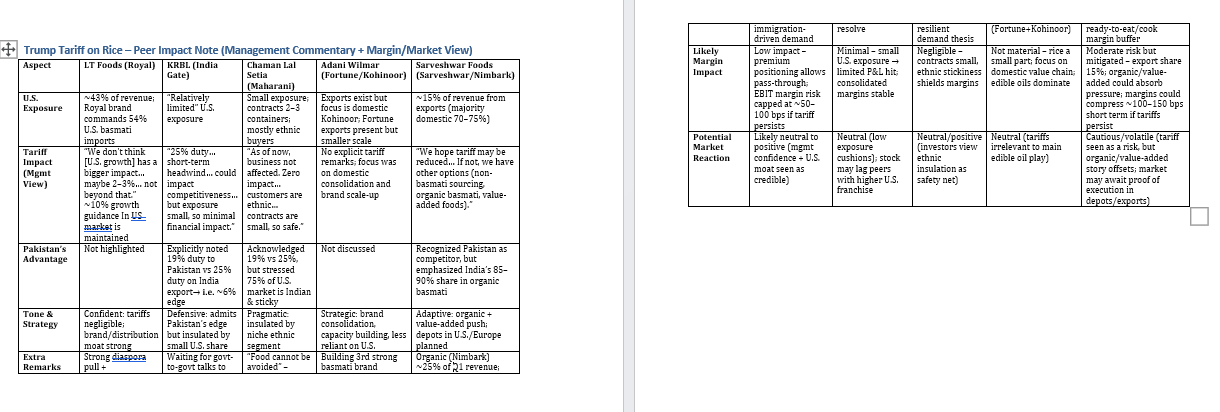

As per my understanding, Gross margin in the upper band!!! But Organic food & RTH / RTC will be contributing ~ 20% (currently 13%) ~ Suppose revenue mix 80 : 20 ratio, then GP Max ~36-37% !!! Interesting to watch future numbers

Nothing much to add here as we discussed almost everything before hand

I am expecting a major rally in next 1 year

Particularly when raw material cost impact is seen

Company has purchased 25% more paddy this year (refer concall)

Also markets sentiments are pretty favorable too

This was my post and admin flagged it appropriate

I don’t know why my posts being marked in appropriate

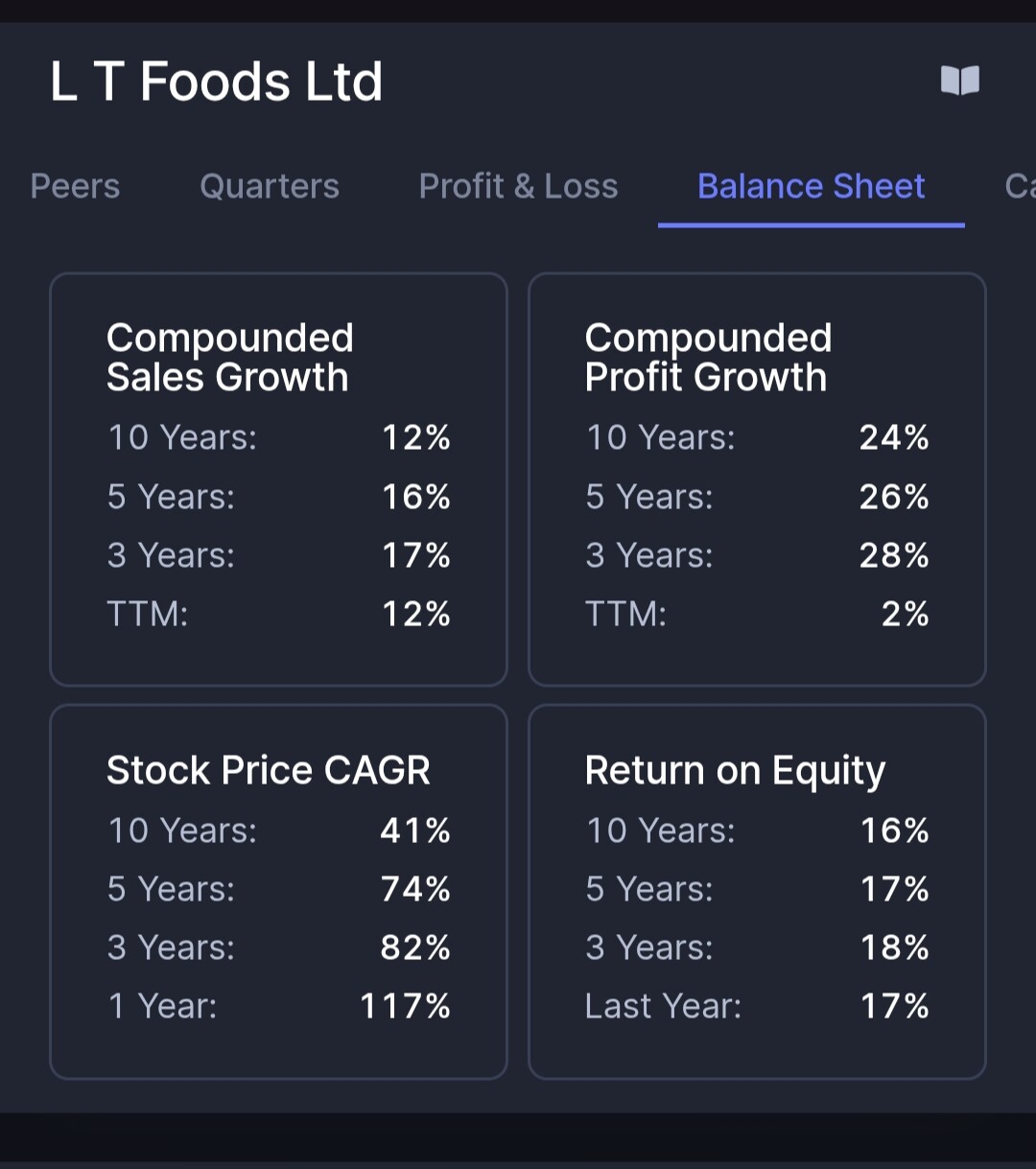

The way they have managed and reduced debt and maintained good enough ROCE was commendable, we are finally seeing the re-rating here.

Now that the commodity stamp on the company is removed, and debt is negligible, we can expect it to do well for the next few years..

they have already entered , Kari Kari already doing good , this is just expanding product portfolio

if you read through con call , saudi contributed only 55 Cr to revenue till date , there is massive opportunity but according to Mr Arora it will take 2 years to fully see effect , saudi is high margin business ,

also targetting around 13 % ebitda with 10Kcr + revenue in this FY

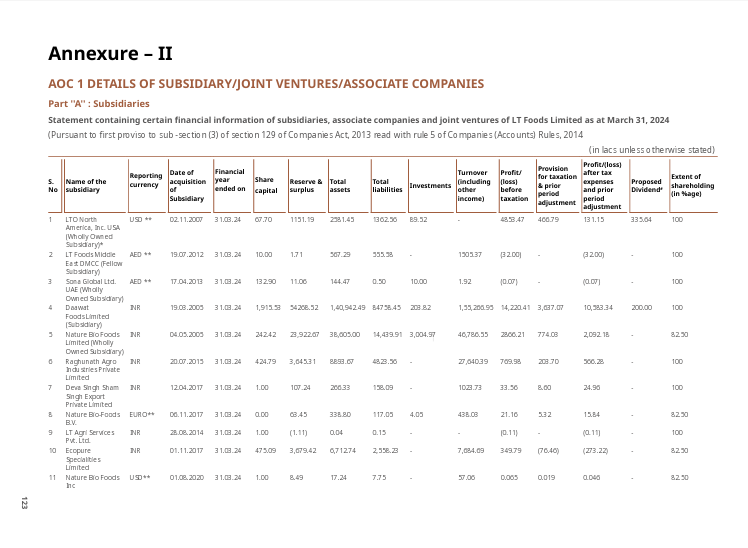

what was conveyed by the management on todays meeting regarding the duty imposed by the US Department of Commerce on the exports of organic soybean

meals by Ecopure Specialities Limited (a fellow-subsidiary of LT Foods) ?

Anyone has any idea if the UK FTA deal has any positive impact for LT Foods ? Will LT Foods exports including Basmati and other product lines be tariff free in UK ? They were supposed to invest in UK in some facility - what kind of facility was it and will they invest further there (it was supposed to be a multi year plan) - considering they might not need it anymore.