I did some quick checks and made an attempt to find out if the current rally in the market is sustainable or not. The purpose of this post is to share my findings with everyone at VP and for me to come back to it in future to verify my current thought process. Sorry for long post. I hope this post will be worth the time you spend reading it. And if this post doesn’t belong here, please let me know, and I will move it to appropriate thread.

Date: 11th April 2020

Are we seeing a ‘head fake’ rally?

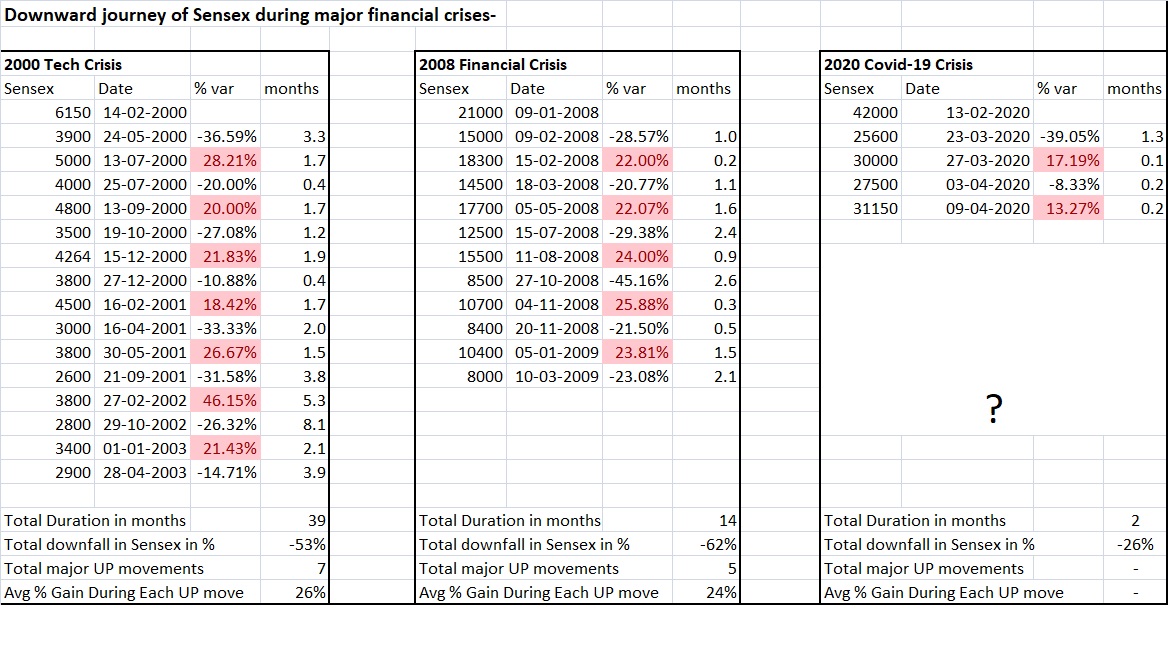

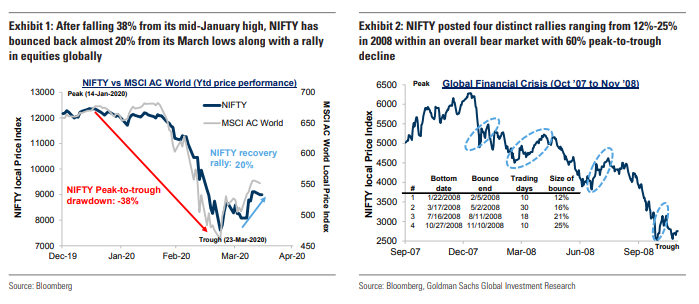

Indian market indices and most individual businesses made 52 week low on 24th of March 2020. Both Nifty & Sensex have made a nice pull back of 21.31% and 21.53% respectively from 24th March 52 week lows. This is good rally. But the big question is, is it ‘head fake’ rally OR an actual sustainable rally with longer and sustainable legs. I did some quick checks and made an attempt to find it out. Let’s take a look:

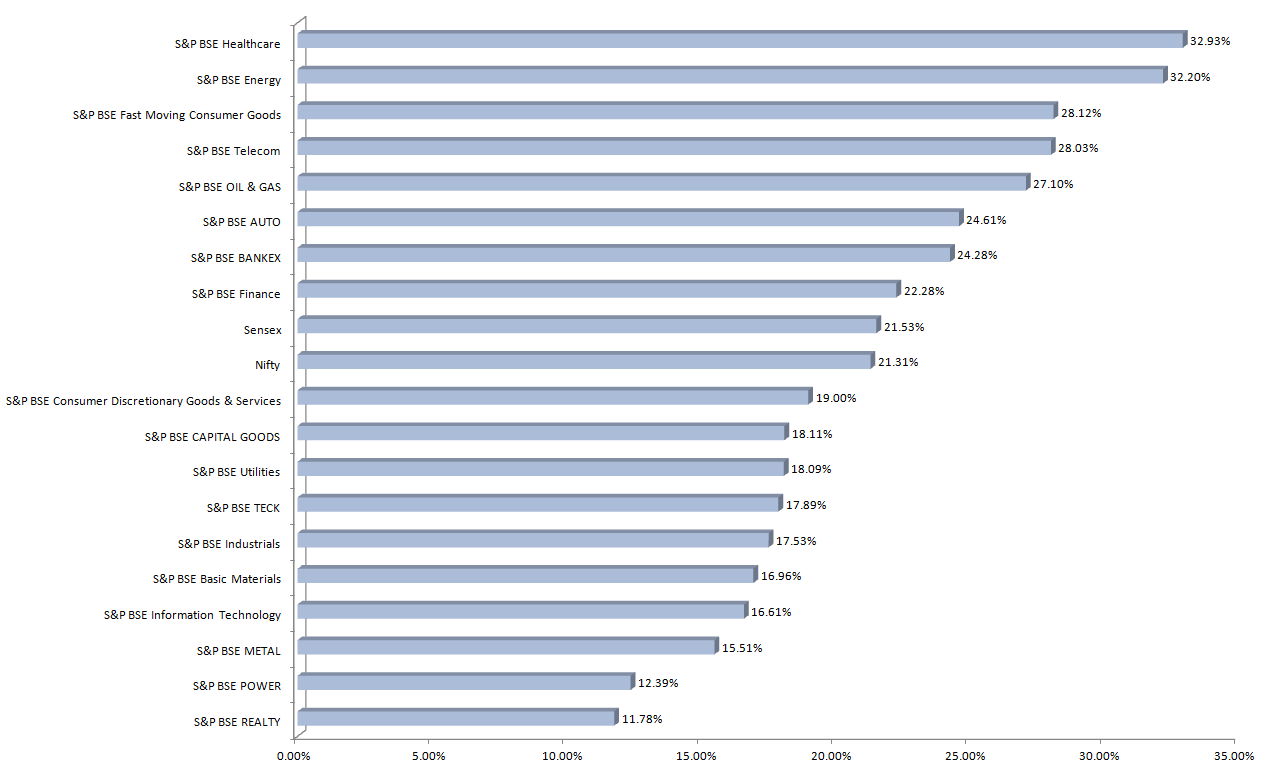

Below is how most BSE Sectors/Indices have moved UP from the 24th March lows.

| Defensives |

% Up from 52week Low |

| BSE Healthcare |

32.93% |

| BSE Fast Moving CG |

28.12% |

| BSE Telecom |

28.03% |

| BSE Oil & Gas |

27.10% |

| BSE Utilities |

18.09% |

| Sensitives |

% Up from 52week Low |

| BSE Energy |

32.20% |

| BSE IT |

16.61% |

| Cyclicals |

% Up from 52week Low |

| BSE Auto |

24.61% |

| BSE Bankex |

24.28% |

| BSE Finance |

22.28% |

| BSE Consumer Discretionary |

19.00% |

| BSE Capital Goods |

18.11% |

| BSE Industrials |

17.53% |

| BSE Basic Materials |

16.96% |

| BSE Metal |

15.51% |

| BSE Power |

12.39% |

| BSE Realty |

11.78% |

Most Gains Have Come From Defensive Sectors

Defensives are perceived to be “safe havens” in bear markets and as we can see from above that they have participated heavily in this rally. In fact we can clearly tell that Defenives have led the rally. All sectors except Utilities have outperformed SENSEX by very wide margin.

This shows that market participants are still possibly FEARFUL and CAUTIOUS and are opting to go with DEFENSIVES in these uncertain times.

Only 3 out of 10 cyclical Indexes have done well relative to SENSEX; Auto, Bankex, and Financials have done well. But Capital Goods, Industrials, Basic Materials, Metals, Power, and Realty have underperformed in this rally by big margin. Its always good to see leadership in rally coming from cyclical businesses that benefit higher from economic growth. Their participation in the rally shows investors are confident of the economic outlook. This has not been the case in this particular rally.

Unpromising Market Breadth

There are two things that I am looking at for checking Market Breadth; down-from-52-week-highs and up-from-52-week-lows. A query gives me total of about 3608 businesses on screener.in.

Up-from-52-week-lows

There is a good chance that most (but not all) of the stocks have made their 52 week low during this Corona crash. Both Nifty & Sensex have made a nice pull back of 21.31% and 21.53% from 24th March 52 week lows.

| Up by > 21.3% from 52-week-low |

1360 |

37.69% |

| Up by < 21.3% from 52-week-low |

2248 |

62.31% |

| Total |

3608 |

100.00% |

Numbers from above table are clearly in favor of less businesses participating in this rally.

In fact, there are 804 businesses who have gained less than 10% from their 52 week low which makes up about 22.28% of 3608 businesses. So your 22.28% of businesses have not even rallied half of Nifty or Sensex.

Down-from-52-week-highs

Both Nifty & Sensex are currently down 26.70% and 26.29% from their 52-week-highs.

| Down by > 26.70% from 52-week-high |

2971 |

82.34% |

| Down by < 26.70% from 52-week-high |

637 |

17.66% |

| Total |

3608 |

100.00% |

82.34% of the businesses have fallen more than the market so far.

Nifty and Sensex have rallied BUT underneath individual stocks are still beaten down and there is not much broader participation.

Valuation

Average historical Nifty PE is close to 16 times. Before the market crash, Nifty was trading at about 22 times. Now it’s trading little above 15 times (slightly below the historical average). The lowest PE level that has been seen is ~12 times in bear markets. So if we were to see Nifty bottom close to 12 times which means we will see Nifty close to 6500 levels and this is ~29% away from current level of 9111.90.

Bottom-Line

So let’s quickly review everything that we have seen so far:

-

Most gains have come from DEFENSIVES which shows participants are still possibly FEARFUL and CAUTIOUS. 7 out of 10 cyclical sectors have underperformed NIFTY/SENSEX by huge margin giving signs that participants are not too sure of economic recovery anytime soon.

-

62.31% of the screener businesses have not participated along with current NIFTY/SENSEX rally. And 82.34% of the businesses have fallen more than the market from their 52 week high when compared with NIFTY/SENSEX.

Nifty and Sensex have rallied BUT underneath individual stocks are still beaten down and there is not much broader participation.

-

Nifty PE is still far from generally low levels seen in the bear markets.

Based on above findings, my view is that there is a good chance that we are seeing a ‘head fake’ rally.