https://www.bseindia.com/xml-data/corpfiling/AttachHis/ad3b1422-0e1f-45a9-b36c-f495de2c1060.pdf Promoters of Lincoln Pharma increases promoter group

holding by 4.9% during FY 20-21 to 37 .25%

2 Likes

Any one any idea about the recent massive surge in volume? Trying to break out all time high but retreated today. Guess the up ride is over? There were news that they were setting up the API plant. Any info on that? Further, still no clue on the business post EU approval in to regulated markets?

2 Likes

Lincoln Pharma Q4FY21 results update.

Godd results by the company.

- 32% increase in PBT yoy from Rs. 11.53 cr to 15.31 cr despite 48% increase employee cost in the quarter.

- Gross margins improved to 67% from 55% yoy and from 47% qoq.

- Good operating cashflows for the year at Rs. 70 cr.

- Cash and Liquid investments of Rs. 93 cr as on 31.03.2021.

- Exports for the year at 64.40% in FY21 compared to 60% in FY20. Company is witnessing good traction in the export business, which is expected to get further boost once EU operations begins. Company plans to enter the EU markets in FY22 with its dermatology, gastro and pain management products. Company currently exports to more than 60 countries and plans to expand to 90 plus countries.

- Going green, company has also set up a new Solar Plant of 1 MW at factory’s rooftop in addition to two windmills. This way we are producing renewable energy to our consumption nearly 65% resulting significant saving in the electricity cost and helped the company to become a self-sustainable and environment-friendly organization.

6 Likes

I recently came across this co. Although the npm and OPM margins are growings, topline growth is still sluggish. Positive that co became debt free and promoters increasing stake. but if sales growth is sluggish, the co would struggle in longer term.

On a side note, I checked the EU GMP website but I cannot find their approval for Lincoln pharma. Anyone knows how to verify that?

The promoters are increasing their stake. they bot 5% shareholding in Q4FY21 and in Q1 purchased 0.5% more. saw an interview of the MD recently where they are talking of exporting to europe and canada by Q3 FY22 and also doing capex of 35-40 cr. I think this the management is conservative and they are not going very aggressive on capex plans. Revenue growth has been stagnant in last 5 years but if exports to europe/canada pick up then we might see 10-15% increase in topline. They are also adding 150 ppl more to domestic sales force, increasing it to 800 ppl from 650.

3 Likes

the company has started exports to europe. first shipment happened in july. so finally they are exporting to europe, although the value is still small but this is a regulated market and the margins higher. further, they are very dependent on tanzania for their revenue, diversifying it to europe would derisk the revenue. hope that they start shipments to Canada soon.

6 Likes

8 Likes

Very good analysis again by @drvijaymalik. He has done some priceless work in investor education by his incisive analysis reports. Thanks for sharing!

1 Like

AR21 notes

-

Revenues grew by 8.1% from 397 cr. to 429 cr. with EBITDA and PAT increasing by 21% to 92.8 cr. and PAT 62.2 cr. In the last five years, PAT has grown at 20% CAGR. Became debt free

-

Revenue break-up:

o India: 163.55 cr. (vs 168.01 cr. in FY20)

o Export: 260.63 cr. (vs 218.48 cr. in FY20)

o 1 customer contributes more than 15.37% of revenue (vs 12.11% in FY20) -

Subsidiaries:

o Lincoln Parenteral: Sale 44.7 cr. | PAT 1.84 cr.

o Zullinc Healthcare: Sale 1.7 cr. | PAT 7.92 lakhs

o Savebux Enterprises Private Limited: Received order from NCLT for dissolution on March 26, 2021 and stands dissolved w.e.f. March 03, 2021 -

6 out of the 11 directors only attended 2 or fewer meetings (out of the 4). No sitting fees was paid during FY21

-

R&D expense 2.6% of sales (vs 3.14% in FY20)

o Capitalized: 0.86 cr. (vs 3.52 cr. in FY20)

o Expense: 9.36 cr. (vs 8.3 cr. in FY20)

o Secured a patent for Didofenac Rectal Spary

o Developed new NDDS formulations and introduced them for the first time in India

o 33 scientists, received 7 patents (up from 4 in FY19) and filed 25+ patents

o 1700 product registrations with 700 more in pipeline, developed 600 formulations -

90th rank in IQVIA (June 2021), 650 field force (MRs)

-

Launched Vitamin C + Zinc Chewable tablet as an Immunity Booster

-

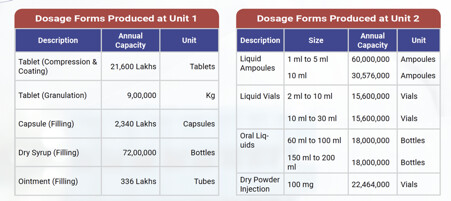

Manufacturing capacity at the 2 units

-

Has setup a new solar plant of 1 MW in addition to two windmills (2.7 MW) resulting in savings of nearly 65% of electricity costs

-

Received EU GMP certificate to conduct business in the European Union

-

Amalgamation of Lincoln Parenteral Limited and Lincoln Pharmaceuticals Limited

-

Set up an API production unit and Cephalosporin Plant

-

Promoter holding: Increased to 37.26% (vs 32.36% in FY20)

-

Number of employees: 1’246 (managerial remuneration increased by 3-4% and other employee by 10-11%), contractual workers: 700

-

KMP remuneration: 1.6 cr. (vs 1.46 cr. in FY20). Related party remuneration + commission is >3 cr.

-

Number of shareholders: 21’415, price (low): 118.05, price (high): 283.45

-

Audit fee: 11 lakhs (vs 11.15 lakhs in FY20)

-

Income tax dispute: 2.3 cr. (vs 2.19 cr. in FY20)

-

Trade receivables which have significant increase in credit risk reduced from 19.85 cr. to 14.63 cr.

-

Current loans given

o Inter-Corporate Loans 14 cr. (vs 0 in FY20)

o Loans and advances given to others 4.78 cr. (vs 15.88 cr. in FY20) -

Non-current loans given

o Inter-Corporate Loans 2.3 cr. (vs 2.5 cr. in FY20)

o Loans given to others 22.79 cr. (vs 12.28 cr. in FY20)

o Security Deposits given to Lincoln Parenteral 14.82 cr. (vs 16.74 cr. in FY20)

Disclosure: Not invested

8 Likes

Thanks.

Analysis on valuation, FY20 EPS is Rs 30.

Assuming 15% CAGR based on last few years, FY 21 EPS is around 35.

Stock trading at 390 implies a P/E ratio of 11x.

1 Like

FY21 EPS is expected to be Rs. 35, in fact they have done Rs. 8.85 in Q1, 2022.

If we look at historical valuation of the company, most of the times it has traded at below 10 P/E. The question is- is re-rating possible?

It looks like a re-rating is possible. The company has moved out of low margin segments. Further, export to highly regulated markets like EU has started. They are introducing new products- [quoting the MD from Annual Report]

“Going ahead, Lincoln Pharmaceuticals Limited is dedicated to expanding its product portfolio, gain more patents and increase focus on research and development. The Company is committed to developing value-adding products in the lifestyle and chronic segments, especially for women and skincare. Our presence in the acute segments presents a lucrative growth opportunity to gain more ground in the market. The company is looking forward to expanding its global footprint from 60 to more than 90 countries in the coming years, to impact more lives and spread health and well-being through our vast range of products.”

On the P/L side, margin is increasing. They claim to have introduced certain NDDS solutions for the first time in India. They are also working on API unit. If things goes well, p/e rerating is possible.

[Disclosure- Invested]

4 Likes

main positives i see are promoter is buying shares showing confidence in the company which is the ultimate north star. Promoters buying shares certainly means that they think the company shares are undervalued and they believe in the future prospects of the company.

Moreover it is hard to find companies with good fundamentals wih a P/E ratio of 11x in this market.

2 Likes

Lincoln Pharma and Lincoln Parenteral are getting merged now.

Lincoln has acquired a plant in Mehsana, Gujrat for 30 crores (including expansion). The plant is expected to contribute around 150 crores in topline in next 3 years.

0708a0f5-f416-45b8-87dc-02d2614c6b35.pdf (4.2 MB)

5 Likes

Anyone on top of the inter-corporate loans that the promoters has doled out in FY 21 too?

Lincoln Pharmaceuticals Ltd receives approval from

Australian Regulator, TGA

Can someone shine a light on this approval. Can it make a big difference?

Hi…its good to the see the increase in promoter holding. And the upcoming expansion and entry into Europe seems promising…though the sales look stagnant for the past 4-5 years on the face of it. But, if you look at the break-up of revenue then the management has reduced the highly competitive domestic business and replaced it with export business where they have earned better margins. So even though the turnover has remained range bound the underlying margins and profitability of the business has gone up 2.5X in this time period. And now with company further planning to spend money on capex and enter markets like Europe there can be growth on both topline and bottomline…which makes this company interesting.

Coming to the balancesheet side of things…they have been able to pay down debt and are now a cash surplus company…while the negative part is the inter corporate loans that the company has given out…I hope the management will take corrective action similar to how they have improved in terms of corporate structure and shareholding.

Regards,

Yogansh Jeswani

Disclosure: Invested

7 Likes

the only downside in the company is the intercorporate loans and the promoters not being aggressive enough for capacity/biz expansion. that said they have done well to diversify the business like u said from domestic to export oriented and would continue to focus on this. in last 9 months, they have increased shareholding from 33 to 40% and hopefully going forward we will continue them doing so.

with 355 cr of cash reserves, the co has enough capital to deploy in biz expansion. i think in 2-3 years we will see a very different balance sheet and income statement from the co. the exports to europe on trial basis already started from july 21 and some shipments going to france regularly. hoping to see them shipping soon to more european countries and canada/australia.

@lifetrix I don’t think the cash reserves are of 355 Cr…you are confusing it with the reserves.

Cash & cash equivalents are roughly as follows:

Cash & Bank of 10 Cr + MF investments of 80 Cr…so roughly 90 Cr

Investments in the form of inter corporate deposits and loans to other party is additional 40-43 Cr.

Regards,

Yogansh Jeswani

Disclosure: Invested