Initiating this thread on Linc Ltd. Putting in my notes for Q1FY24 concall. I believe that this is a good place to start researching a company. Looking forward to all of y’all inputs.

Pentonic Sales

Pentonic sales continue to grow, reaching over 36% market share.

Export revenue contributes over 16% to the company’s top line.

Revenue Growth

Operating revenue for Q1FY24 grew by 14.2% to INR 111.88 crores, compared to INR 97.94 crores in Q1FY23.

Pentonic’s contribution and stationary portfolio growth drive stronger top-line performance.

Writing Instrument Dominance

Linc maintains a strong presence in the writing instrument segment with a market share of approximately 7%.

Pentonic emerges as a leading brand in India’s affordable writing instrument industry, reaching INR 150 crores since its FY2019 launch.

Gross Profit Margin Expansion

Gross profit margin expands to 32.3% in Q1FY24, marking a 693 basis points increase from Q1FY23.

Gross profit grows by 45%, outpacing the 36.3% growth in overhead costs, demonstrating robust operating leverage.

Strong EBITDA Growth

Operating EBITDA increases by 65%, with the operating EBITDA margin expanding from 8.2% (Q1FY23) to 11.8% (Q1FY24).

Profit after tax rises to INR 7.39 crores compared to INR 4.38 crores in Q1FY23.

Formation of Morris Linc Private Limited

The company establishes a subsidiary, Morris Linc Private Limited, to initiate a joint venture with Morris, a global writing instrument and stationery player based in South Korea.

Linc will be the majority shareholder, with further details forthcoming in subsequent quarters.

Morris Linc products will be priced in the range of Rs. 30 to Rs. 50.

They will offer advanced features in the writing instrument segment.

The new products will not compete with existing ones in the portfolio.

The Morris product line includes markers, a category that Linc Limited is currently working on. Since Linc has minimal or no presence in this category, there is no expected cannibalization.

Expanding Market Reach

The company extends its presence in non-stationary outlets, including kiranas, medical stores, and Pan plus, reaching 1.44 lakh such outlets directly.

Total touchpoints surpass 2.45 lakh outlets, with a focus on further expansion.

Geographical Revenue Diversification

Revenue share from south and west zones increases from 27% (FY19) and 36% (FY23) to 43% in Q1FY24.

The company aims to expand its reach to more than 5 lakh touchpoints by FY25.

Focus on High-Value Products

Emphasis on high-value, high-margin products, with Pentatonic volume growing over 34% YoY.

Introduction of Pentonic G - RT, priced at Rs. 40, and development of three more Pentonic products within the financial year.

Deli Brand Success

Deli, the stationary brand, achieves a turnover of INR 6.4 crores in Q1FY24, up from INR 4.98 crores in Q1FY23.

Revenue share of Deli increases from 4.7% (Q4FY23) to 5.8% (Q1FY24), targeting a top line of at least INR 75 crores by FY25.

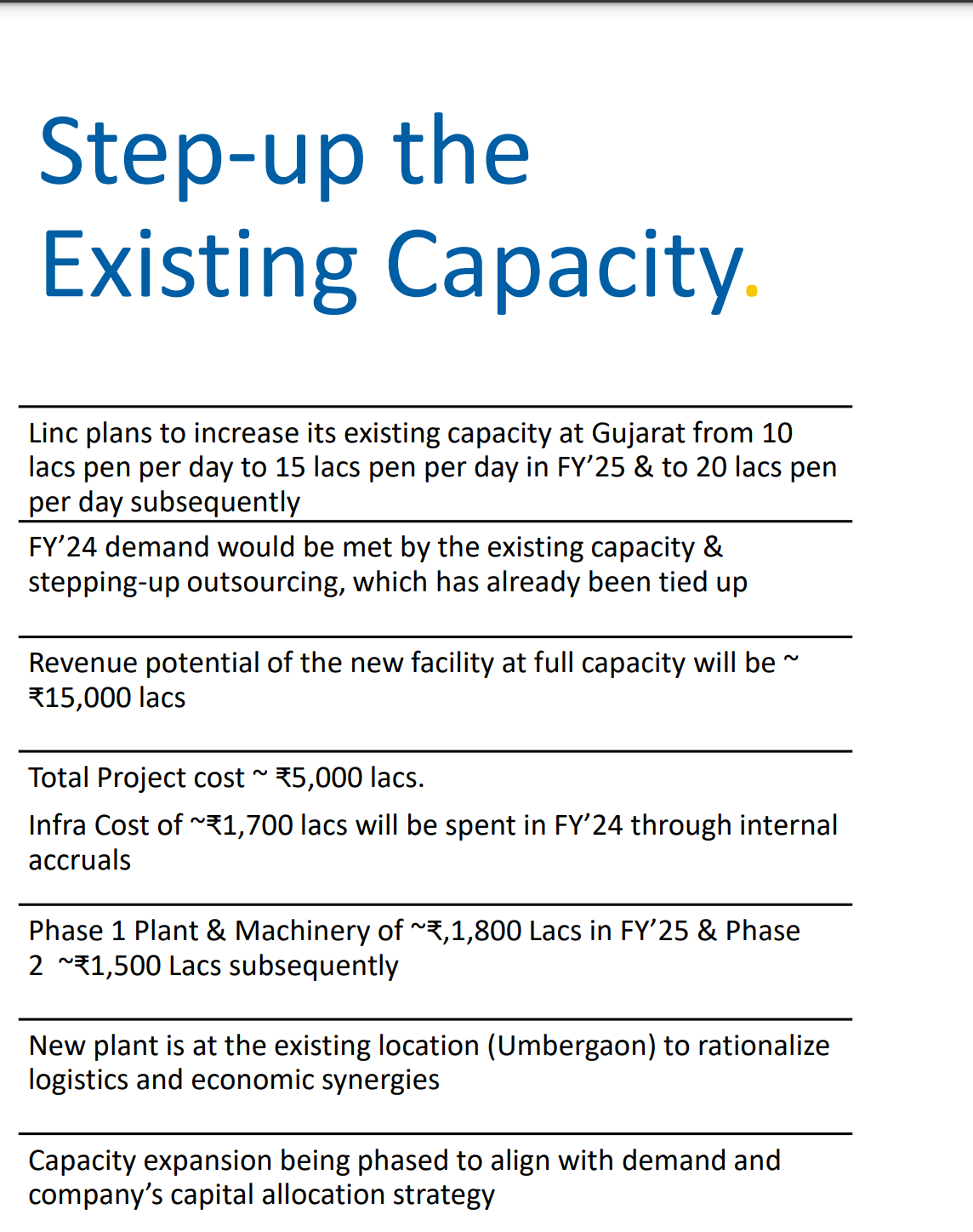

Expansion Plans

Plans to increase manufacturing capacity in Gujarat by establishing an additional facility adjacent to the existing factory.

Infrastructure creation for doubling production capacity to 20 lakh pens per day.

Total project cost expected to be approximately INR 50 crores. Initial infrastructure work costing INR 17 crores to be finished by FY24.

Debt Reduction and Cash Flow

The company effectively reduced its net debt over the past five years, becoming debt-free.

Free cash flow increased to INR 15.6 crores as of June 30, 2023.

Capacity Increase

First phase of equipment expansion to 50 lakhs pens per day expected in FY25, at a cost of INR 18 crores.

Second phase planned subsequently at an estimated cost of INR 15 crores.

Anticipated meeting FY25 demand through existing capacity and increased outsourcing agreements.

Revenue Growth Targets

Aims to achieve a top-line revenue of INR 750 crores by FY25, with a CAGR of around 25%.

Aims to achieve a top-line revenue of INR 600-625 crores by FY24

Expects Pentonic’s share of revenue to reach 40%, with an additional contribution from ally products.

To achieve a 25% growth target in the next three quarters after a 14% growth in Q1, Linc Limited is focusing on growing the Pentonic portfolio, which showed over 30% growth in Q1.

EBITDA Margin and ROI

Targets an annual operating EBITDA margin of about 15% by FY25.

Expects a return on investment (ROI) above 21%

Pentonic G - RT

Priced at 40 Rs

Recently tested in Bombay, Pune, Chennai, and Kerala.

Received excellent customer response during the test phase.

Linc Limited is ready to launch the gel pen nationwide.

Anticipated to be accessible throughout India in the next two to three months.

Exploring Export Market Opportunities:

Linc Limited prefers to promote its own brand in international markets.

White labeling is generally avoided due to potential margin challenges.

Open to white label opportunities if they offer long-term partnerships and substantial benefits.

Export Gross Margins:

Export gross margins are generally slightly better than domestic margins.

For instance, if domestic margins are around 40%, export margins could be approximately 44%-45%.

Major Export Markets:

Linc Limited exports to approximately 40 countries.

Prominent markets include Southeast Asia, neighboring countries, Africa, Middle East, Brazil, Russia, and North America.

Seasonality in Business:

Q1 is a lower quarter due to seasonal factors.

Summer vacations during Q1 result in reduced consumption, especially among primary consumers, school and college students.

Outsourcing vs. In-house Production:

Linc Limited is considering outsourcing as it aligns with industry trends where FMCG companies often maintain a 50:50 ratio of in-house and outsourced production.

Outsourcing provides flexibility and reduces asset commitment. It is recommended by investors and considered a balanced approach.

The current ratio of outsourcing to in-house production stands at 50:50.

Current approach includes careful selection of print media.

Campaign running in Times Of India (all editions).

Additional strategies: outdoor advertising in select cities, digital and social media.

Future plans may involve a TV campaign, likely in the next year when more budget is available.

Online Availability of Product Range:

E-commerce Potential: Online sales offer significant potential, especially with the Deli brand, known for a wide range of stationery.

Chinese Partner: Linc Limited’s Chinese principal company derives 50% of its sales from e-commerce, indicating substantial opportunities.

Current Share: Presently, e-commerce contributes only 3% to the company’s revenues.

Future Growth: Linc Limited sees substantial potential for growth in the e-commerce segment and is actively exploring opportunities to increase its share in India.

Positioning at Micro Retail Outlets:

Challenges: Positioning at micro retail outlets where consumers seek pens irrespective of the brand is challenging in India’s unstructured market.

Strategies:

Relationship Building: Sales teams work on building good relationships with retailers.

Visibility: Maintaining brand visibility through various media channels.

Point of Sale Displays: Providing retailers with attractive displays for product placement.

Consumer Demand: Popular brands like Pentonic are top-of-mind for consumers, and retailers prefer stocking such demanded brands.

Impact of Pentonic on Linc Brand Sales:

The Linc brand experienced a decline in sales for some legacy products in Q1 due to price increases.

While some products absorbed the price increase and are growing, others are yet to recover.

The company aims to limit the decline in legacy products and hopes for improved performance in the future.

Second highest margin: Uni-Ball and legacy products

Third highest margin: Deli brand (imported finished products)

Price Adjustment for Raw Material Costs:

In the Rs.10 pen range, there is limited room to increase prices when polymer prices rise.

Typically, there’s room for a 6%-7% price increase to the trade, but end-user prices remain relatively stable.

This strategy is employed to mitigate the impact of rising polymer prices.

Gelx India-Kenya Acquisition:

Market Expansion: The acquisition in Kenya serves the purpose of expanding Linc Limited’s market presence in East Africa, particularly in countries with tariff barriers that restrict imports from India.

Export Advantage: With a local unit in East Africa, Linc Limited gains the ability to export its products to neighboring markets without incurring duty costs.

Revenue Expectation: The company anticipates achieving a topline of approximately $2 million (around Rs. 15 crores) by FY25 through this expansion.

Nice write up and wondering why there wasn’t thread on Linc…Just to add, Mitsubishi Pencil (Uni Ball) holds 13.45% equity and I have very nice impression about promoters…Regular dividend paying except covid year. They have really cracked the code with Brand Pentonic. also, amicably settled shareholding among promoters just a few days back… https://www.business-standard.com/markets/news/sebi-exempts-two-trusts-from-making-open-offer-to-linc-s-shareholders-123081400810_1.html

This space is going tobe exciting with Cello and Flair filed for IPO…

Disclosure: holding since more than 10 years…7% of PF.

Pentonic seems to have changed the face of the company.

Mitsubishi Uniball having 13% share in the company tells a lot about the strong hold in Domestic market.

With newer products under Pentonic and with new Subsidiary for Morris linc, future looks interesting.

Any Idea exactly what changed after FY 2022? According to the management it was the introduction of Pentonic the revenues started seeing some growth. Any thing else I am missing out?

Few things worked in cos. favour IMO…1.Shifting product price point upward.Selling more products having price 10/- and more.

2Started expanding aggregately to neighbourhood grocery

stores (Kirana, Medical stores, Pan stores, etc.) since FY20 to

increase footprint

• Added over 1,80,543 touch points since FY’20; 14,969 over the

last 1 year. The company

expects to expand its overall reach to more than five lakh touch points by FY25 as stated earlier.

3.Rational polymer prices.

4. Pentonic has good margin.

5.Export market picking up.

Can you give the context for investing 10 years ago, in a business like this, what kind of a bet was this, and what has been your experience in holding for such a long time?

I cannot recollect instantly, anyone mentioning that holding businesses like these for 10 years, so asking.

Benchmark was French Stationery Major BIC’s valuation to Cello…Linc was damn cheap and Mitsubishi was holding a chunk into it…Thought Mitsubishi will do the same with Linc…though it didn’t happened, tracking company for few years builds conviction…consumer company,building brand,good management was enough for me hold for long…though topline was not growing…Pentonic changed that alongwith Deli distribution…future seems tobe exciting with Morris deal and Kenya Manufacturing…following para from Concall :

In the quarter gone by your company formed a subsidiary company, Morris Linc private limited the objective is

to form a joint venture between Linc and Morris. Morris which is a leading global writing instrument and

stationery player based out of South Korea having a portfolio of a few patented products in the writing instrument

category was looking to start get some manufacturing in India. They found Linc to be an ideal partner for this

venture. Linc will be the majority shareholder with an extra golden share.

The letter is addressed to three entities: The Calcutta Stock Exchange Ltd., BSE Limited, and the National Stock Exchange of India Limited.

Subject of the Letter:

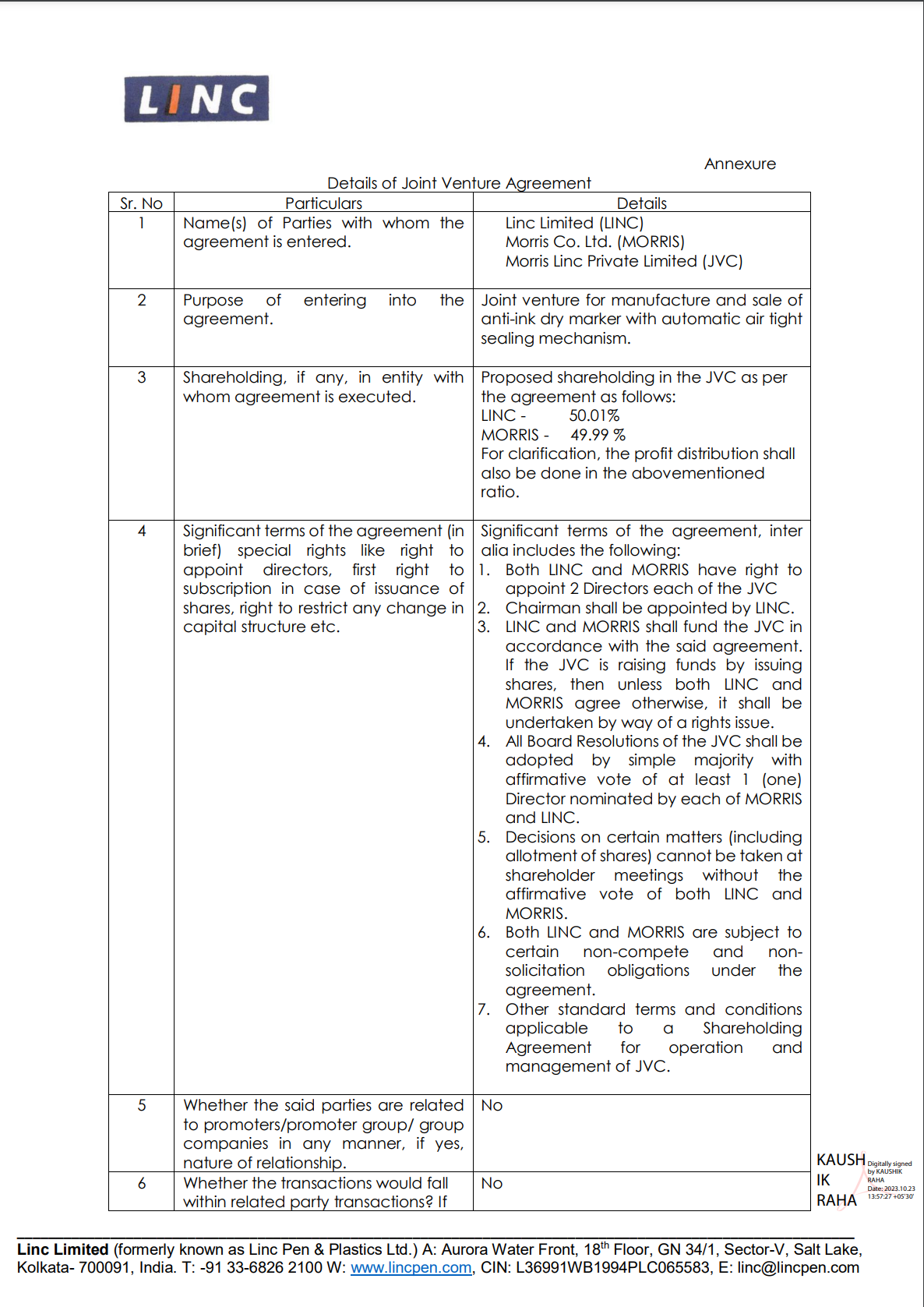

The letter is about the company entering into a Joint Venture Agreement with another company called Morris Co. Ltd.

Purpose of the Agreement:

Linc Limited and Morris Co. Ltd. are teaming up to create a joint venture company called Morris Linc Private Limited. They plan to manufacture and sell anti-ink dry markers with an automatic airtight sealing mechanism.

Shareholding:

Linc will own 50.01% of the joint venture, and Morris will own 49.99%. This means Linc has a slightly larger share of ownership.

Key Terms of the Agreement:

Both Linc and Morris will appoint two directors each to the joint venture company.

The chairman of the joint venture will be appointed by Linc.

Linc and Morris will provide funding to the joint venture according to the agreement.

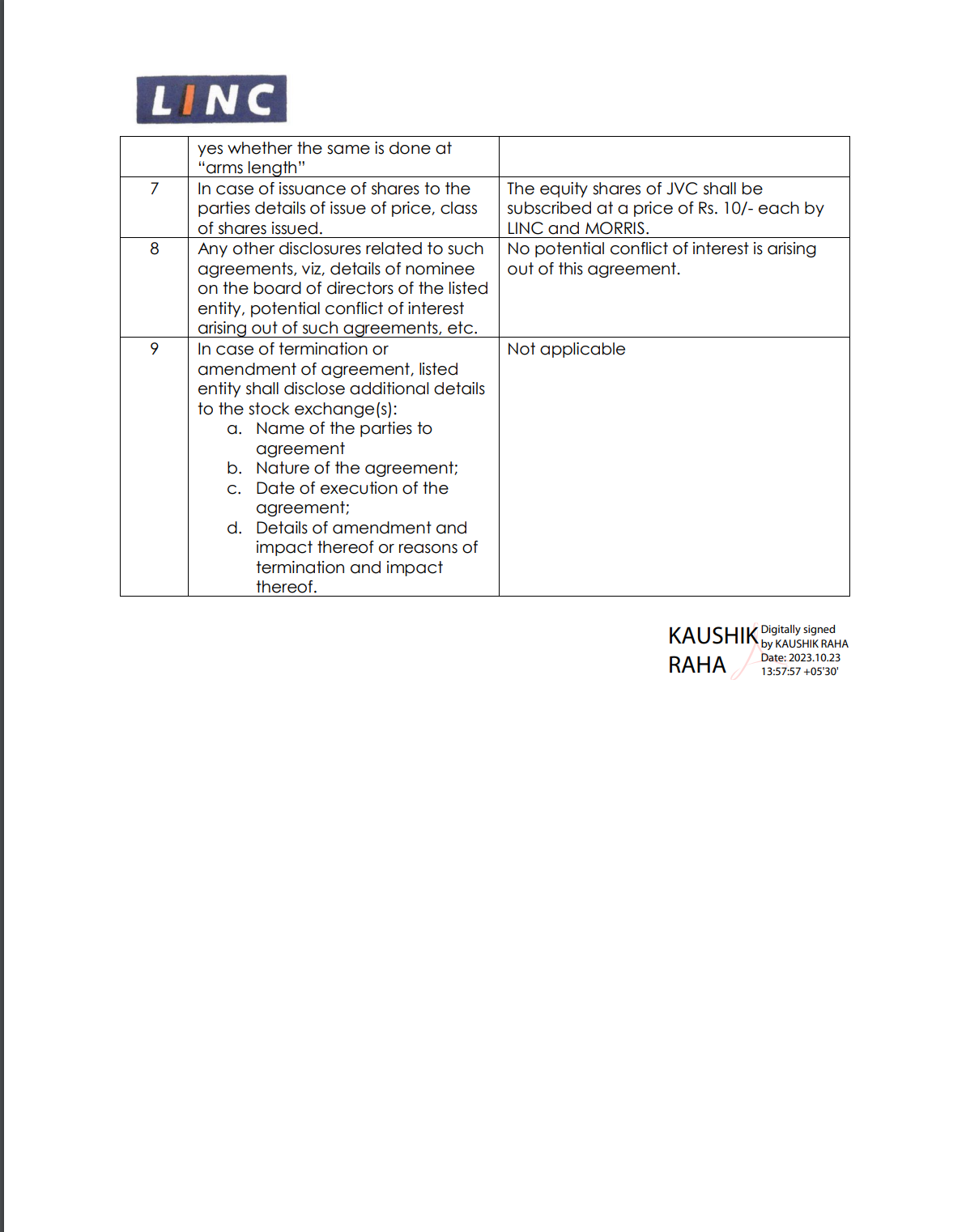

If the joint venture raises funds by issuing shares, it will be done through a rights issue unless both Linc and Morris agree otherwise.

Certain decisions regarding the joint venture can only be made with the agreement of both Linc and Morris.

There are some non-compete and non-solicitation obligations outlined in the agreement.

The agreement contains other standard terms and conditions for the operation and management of the joint venture.

Commenting on the results, Mr. Deepak Jalan, Managing Director, Linc Limited said:

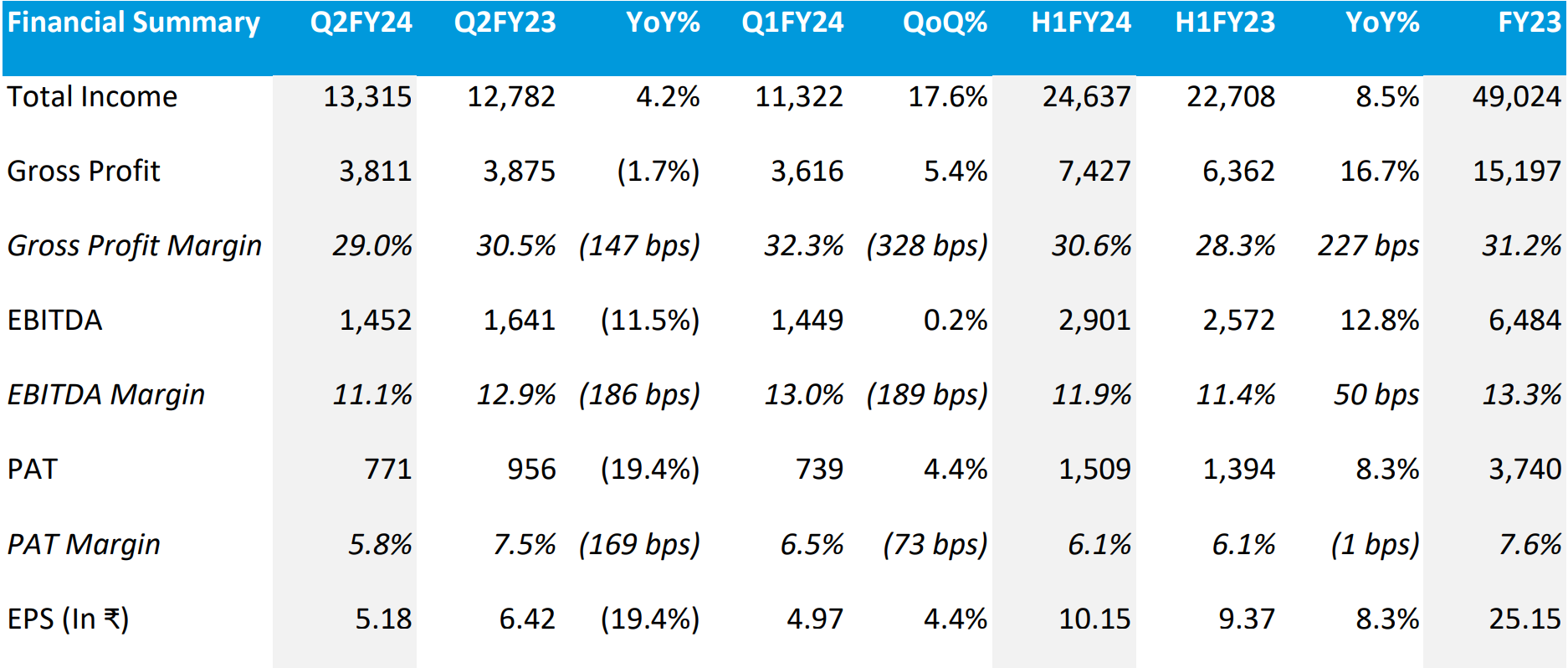

“In the quarter gone by, our company demonstrated remarkable resilience and adaptability in the face of challenges. Despite a decline in our relatively higher margin export revenues, which can be attributed to geo-political disruptions in some of our key markets, our domestic sector showcased a decent growth of approximately 12%. Our proactive response to this situation involves strategic diversification in our export initiatives, where we are actively exploring new markets and optimizing our presence in the existing ones.

Although our gross profit margin experienced a slight dip, reaching 29.0% from 30.5% in the same quarter of the previous year, we view this as temporary. Our unwavering confidence is bolstered by the strong demand we continue to witness for our Pentonic portfolio, the increasing popularity of our “Deli” stationery range, and the growing market share of our higher-margin products. Moreover, our innovative pipeline remains vibrant, promising exciting prospects on the horizon. Our margins were also affected during the quarter due to one-time prosperity rewards to employees, recognizing their dedication and hard work during the challenging Covid times which has been instrumental in making FY 23 our most successful year to date. This is over and above the impact of the annual increments.

As we move forward, we do so with unwavering confidence in our capabilities. Our focus on innovation, strategic market expansion, and employee motivation positions us strongly for sustainable growth. We are confident that these efforts will not only help us overcome current challenges but also pave the way for even greater achievements in the near future.”

Summarizing the growth triggers by the managment:-

1-Exapansion of new PENTONIC product portflio (launch starting from Q3FY24)

2-Growth in sales of Other stationery products (exluding writing) under the name of DELI

3-Market Share growth in higher margin products ultimately showing up on their GPM.

4-Leveraging their export network to introduce international markets (espicially Africa) to Linc products focusing on low ticket size and writing instruments.

Pentonic’s share reducing this quarter really stuck out to me. It can’t just be because of reduction in exports to Myanmar and Sudan. I might be wrong but I don’t think they sell mostly Pentonic in these countries.

The management seemed very defensive this time with their guidance as well. Revising it down to 700cr (assuming max growth of 20% on FY23’s base) in FY25 from the previous guidance of 750cr in FY25.

The Journey for sure from this stage (FY24) will not be as smooth for them which was a year or two later beacuse it was all pentonic led growth and export in new regions.

What we can expect (that would effect the share price) is a more sustainable growth with maket penetration gianing market share from their competitors like flair,cello,doms(which will be there soon in the listed place)

And if they want to achieve the robust growth it is only possible by either developing a new pentonic (grow new product portfolio) or massive sale of DELI products (because GPM on them looks decent)

The results were bleak and unexpected but so far from what I understand, Q2 was a difficult quarter for the entire industry as a whole…was just going through Kokuyo Camlin’s results. Not impressive either, Linc at least showed some top-line growth, Camlin didn’t even have that but surprisingly with a poorer ROCE, ROE, margins, etc… the company is still valued at a premium when compared to Linc. so I still have some hopes left…let’s see how things unfold.

Agree,Q2 is actually generally flattish for these companies the major ones are Q3 (because of festive and schools running on full pace) and Q1(School Projects and New FY for corporates).

Hopes are high and believe to seem some growth in the coming quarters

28% degrowth in high margin export market really dented this quarter…domestic market grown 12%

Going ahead its important to see how new launches at higher price point perform, how quick North America (Largest Market in the world) develops and Morris JV…interesting to note Mr. Jalan mentioned Morris will use India manufacturing base for export market…more details he promised to share post next quarter.

Also,Morris business not included in the guidance…

H2 is always better than H1 and Q4 is always the best quarter for the company…

Disc. Invested and biased…