Starting my first topic in ValuePickr on a small-cap company by the name of Likhitha Infrastructure (BSE 543240, NSE LIKHITHA, CMP 354, PE - 16x, PS - 2.8x, EVEBITDA - 11x). Listed on exchanges in Oct, 2020. Claims to be only listed company in CNG pipeline laying space.

I discovered this company while running a screener of small-cap companies with significant promoter holding with a consistent history of Sales Growth over a decade and ROCE and ROE growth of > 20% for the last 5 years which were optically cheap (PE < 10x or PEG < 1x). This threw up a list of ~30 companies, of which Likhitha was one. Likhitha came to my attention once again when I noticed there was a possible CNG theme developing in India for the next 5-10 years and when Likhitha filed in BSE on 2nd Jan stating they had bagged a fresh 250 Cr order in Q3 from CGDs (City Gas Distribution Orgs).

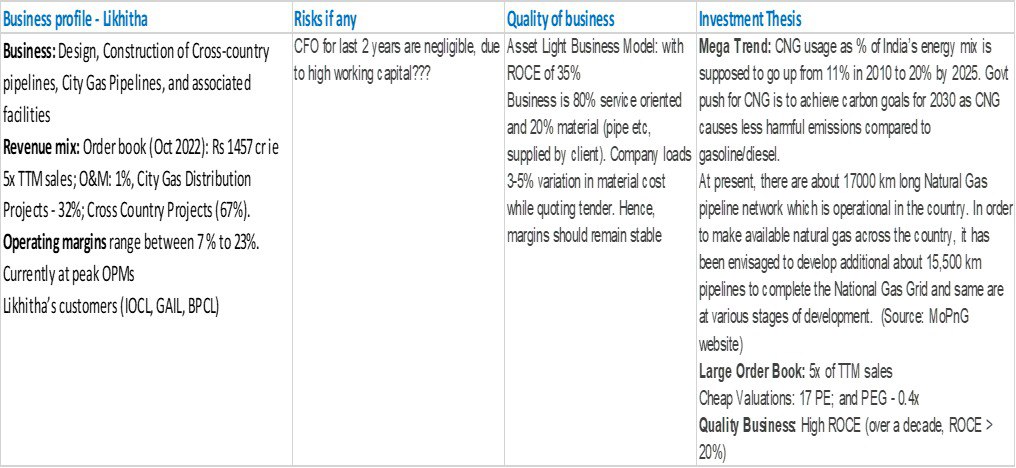

Thesis for investment: CNG usage as % of India’s energy mix is supposed to go up from 6% to 15% by 2030. MoPNG is aggressively increasing number of CGDs across the country to increase supply of PNG to households and industries and CNG to automobiles. Govt push for CNG is to achieve carbon goals for 2030 as CNG causes less harmful emissions compared to gasoline/diesel. Unlike gasoline/diesel, India has the capacity to supply 50%+ of its own CNG demand, thus CNG adoption will reduce forex outgo and increase energy security to an extent. Strong tailwinds appear to be present in favour of CNG for this decade in India. Likhitha being in the CNG infra space, will gain from CNG growth and adoption across industries - automotive, industrials, household.

Understanding the business:

Likhitha operates primarily in 3 verticals

Cross Country CNG Pipeline Laying - Company n its 20+ years of history claims to have laid 1000 KMs+ CNG pipeline in India

Pipeline laying for CGDs - MoPNG is aggressively increasing number of Geographical Areas under CGD services. O&G companies bid for these tenders and winning companies sub-contract the pipeline laying and project management work to specialist 3rd party companies like Likhitha. A list of Likhitha’s current projects and completed projects can be accessed via the links.

O&M Contracts (Operating and maintenance contracts) - Company provides maintenance services for already laid CGD networks.

Claimed competitive advantages/strengths of business model:

Access to growth capital being the only listed company in this space. Promoter stake is 74%, which can be diluted to an extent to raise growth capital for capturing larger projects

Claims to do capex in machinery used for pipeline laying as opposed to opex (machinery on rentals) by other companies giving them a cost advantage while quoting for tenders

Business model is inherently asset and capital light - Client (O&G) company sources max raw material and makes it available for laying work at site. Company’s procurement of raw materials are of low intensity and thus claim to be protected largely from r/m price fluctuations.

Number of projects and prestigious clients under their belt, which boosts their credentials in tenders. Their clients include - IOCL, GAIL, Indian Oil-Adani, AGL, IGL, ONGC, HPCL, Torrent Gas

Points in favour of company’s performance:

Consistent topline and bottom-line growth in 3-5-10 year horizon

Increasing operating margins - OPM has expanded from 11-13% pre FY19 to 20%+ since then. This coincides with the start of the expansion in the O&M segment which company claims is high margin

Order book of 1250 Cr (5x TTM revenues) with 20% belonging to O&M segment

Prestigious clients which are giants in the O&G/CNG space.

Red flags/Corporate Governance HLs:

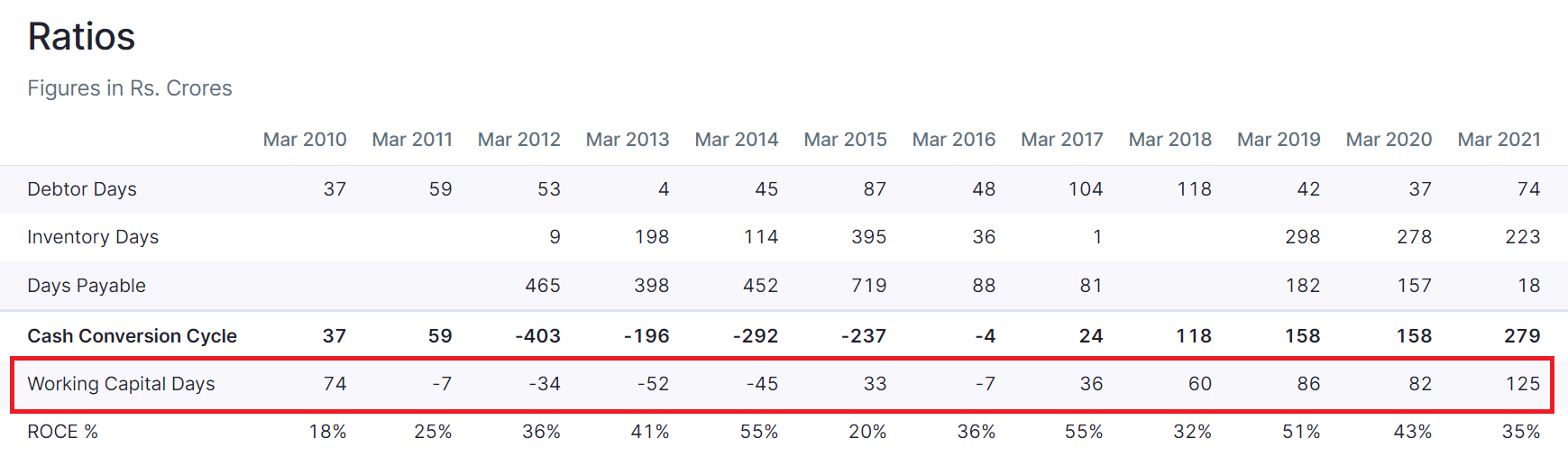

Very poor EBITDA to cash flow conversion. Conversion had improved in FY 20, but dipped badly in FY 21 owing to huge increase in WC

Company in its latest AR claimed to bring down Account Payables to almost 0 stating that they get 5-10% cash discount, but the cash discount doesn’t clearly reflect in COGS reduction from FY20 to FY21

Huge jump in inventory days from FY19. This coincides with expansion in O&M business but may not explain this steep a rise. In past also, WC discipline has been wayward in the company.

The daughter of the promoter has been appointed as CFO in the last few months. She seems adequately qualified (MS from Illinois University and experience in PWC) but is inexperienced. The last CFO was also appointed internally just before IPO, when the then CFO quit.

Present CEO salary is very low (17 LPA) compared to promoter (MD) remuneration (370 LPA). Makes one question the seriousness of CEO appointment.

No concalls/investor presentations - high opacity

Key risks:

Requires sustained Govt. policy push for tailwinds to sustain

Max business dealings with PSUs, can put pressure on WC, margins

Corporate Governance risks as highlighted above

Status: I am tracking with a small position. Wait and watch approach right now.

I am trying to reach out to a Project Engineer/Site Engineer at one of the O&G companies where Likhitha has an ongoing Project to get their feedback. Will update if I receive some info. Looking forward to community members doing their own study to build on this and hopefully some folks in this forum can bring in some feedback on company operations on ground or feedback on management, which seems elusive to me right now.

Great inputs. Question : The cash conversion cycle was -403 in March 2012 vs +279 in March 2021. What are the main reasons for this deteriortation? Thank you.

This was on my radar since IPO, the reason I wrote it off as an investment opportunity is cause entire IPO proceed was for working capital requirements. If they company was at such advantage and tailwinds were present in the business, why did it need to do a 60cr IPO to raise working capital?

There isn’t much other information available about the company either apart from their IPO document (they don’t hold concalls, etc.)

On my watchlist, will share more info if I find anything.

Thank you for opening a thread on this

So, it appears that almost all proceeds from IPO is put into “investments” which appears to have changed from 6Cr in FY20 to 56Cr in FY21. What am I missing when you say entire proceed was for working capital requirements?

Gas transmission is a business that requires expertise and experience which can be a moat to the business. Any idea on who are the competitors and how they stack up against Likhitha. Order book is impressive around twice its market cap. If they have the required equipment for Piping as WC that should reduce rental and other expenses. Net profit of 10 to 12 % leads to profit of 150 crores for the order book. If CNG demand is projected to grow even at 6 to 10% and the order book grows at same rate it should be compounding it at least 15% CAGR.

Not sure about CG but the client names seem pretty rock solid and give some credibility.

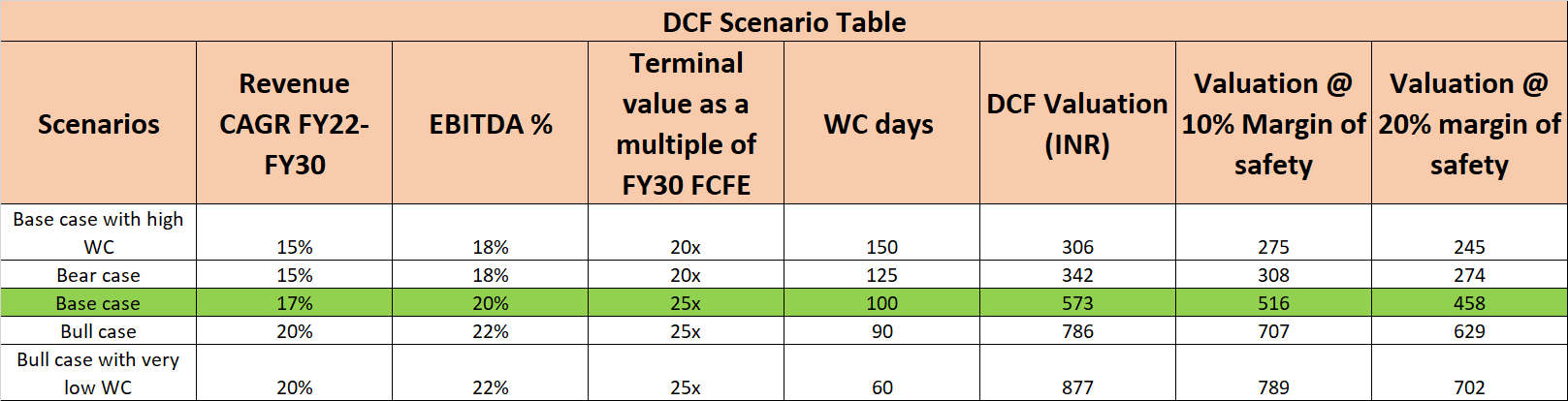

I re-did the DCF valuation today as I spotted a mistake in the one I had done yesterday. I will delete the earlier post shortly. The mistake was in the no. of WC days I had taken into consideration. WC days for base case should be in the 120-150 range, I had by mistake taken it to be double of that, oops!

The good news is, this change makes the DCF calculations much much more attractive. Pasting below the updated DCF scenario table for various bull-base-bear scenarios. As you can see below, the base case has an upside potential of > 60% from current stock prices. Even with a 20% margin of safety, there is a 32% upside possible. This is very encouraging. It means, if management is honest and executes as per potential, then there is good value to be unlocked for investors in this business. Needless to say the bull cases are much more attractive.

Key determinants of the above scenarios playing out:

What will be the terminal multiple for CNG based businesses? My base case assumes 25x FY30 FCFE.

Will GOI follow through on its commitment to raise CNG as a % of India’s energy mix from present 6% to 15% in FY30 (Implied CAGR growth if this is achieved is ~15%) by creating an enabling atmosphere for CNG investments?

Its very easy to play around with, you can just modify the DCF and company parameters at the top to what you think are reasonable parameters and get to see the DCF price. I have bumped up the Discounting rate from earlier 9.9% to 11.8% which I think is closer to reality. Beta considered is 0.96 (Took it from Moneycontrol, my sense is this may be higher). I invite folks to download and play around with the DCF file and point out mistakes/improvements so that our collective conviction can become stronger on this.

I have also written to their Investor cell/CS today, asking clarifications about working capital, cash flow and their plans to conduct investor concalls. I hope they respond. Meanwhile, people who are interested in Likhitha, may I also request you to send emails to their Investor cell - (cs@likhitha.in,info@likhitha.in) - asking them to conduct concalls and release investor presentations? Sometimes, investor activism like this can work. Greater transparency is definitely needed to unlock value and allay corporate governance concerns in this scrip.

Entire proceeds of IPO was meant to be for financing WC, that’s what they declared in their DRHP. But I guess their WC did not expand as much as they were expected in FY21 and they parked the IPO proceeds in investments.

Is non-utilization of IPO proceeds in the same manner declared in DRHP considered to be a corporate governance red flag? Looking forward to experienced investors’ inputs on this. @Tar Any comments?

I did a deep dive on the AR and DRHP to look at Corporate Government issues and also find our more about the business model.

Corporate Governance

There were a couple of significant red-flags in addition to those I have already mentioned above

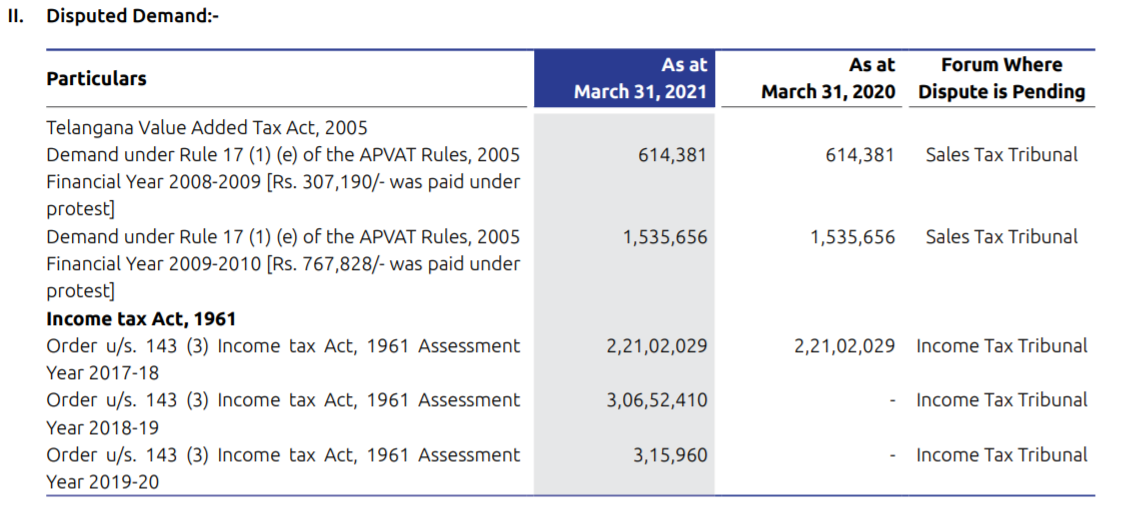

Biggest red flag is a disputed demand of INR 5.3 Cr of income tax by the IT Dept. This demand is across 3 assessment years - AY17-18 to AY19-20. Company has not paid any of the demanded taxes and has disputed them. The AY17-18 demand is for concealment of income or understating income. Company in its DRHP has stated about the AY17-18 demand - *"In addition to the aforesaid demand, the AO has pursuant to the assessment order passed, directed that penalty proceedings u/s. 274 read with section 271(1)(c) of the IT Act be initiated against our Company for concealing/ furnishing inaccurate particulars of income for the relevant assessment year."

The total IT demand as a proportion of TTM net profit is 12.3%, which is significant.

These coupled with other issues like the company being run mostly as a family owned firm (Promoters are a couple and CFO is their daughter; CEO seems to be inconsequential in terms of seniority and influence)

I have written to their Investor Relations/CS department regarding the pending IT demand issues and what the Company’s current stance is. Will update if there is a response.

Business Details

Couple of things caught my eye on business:

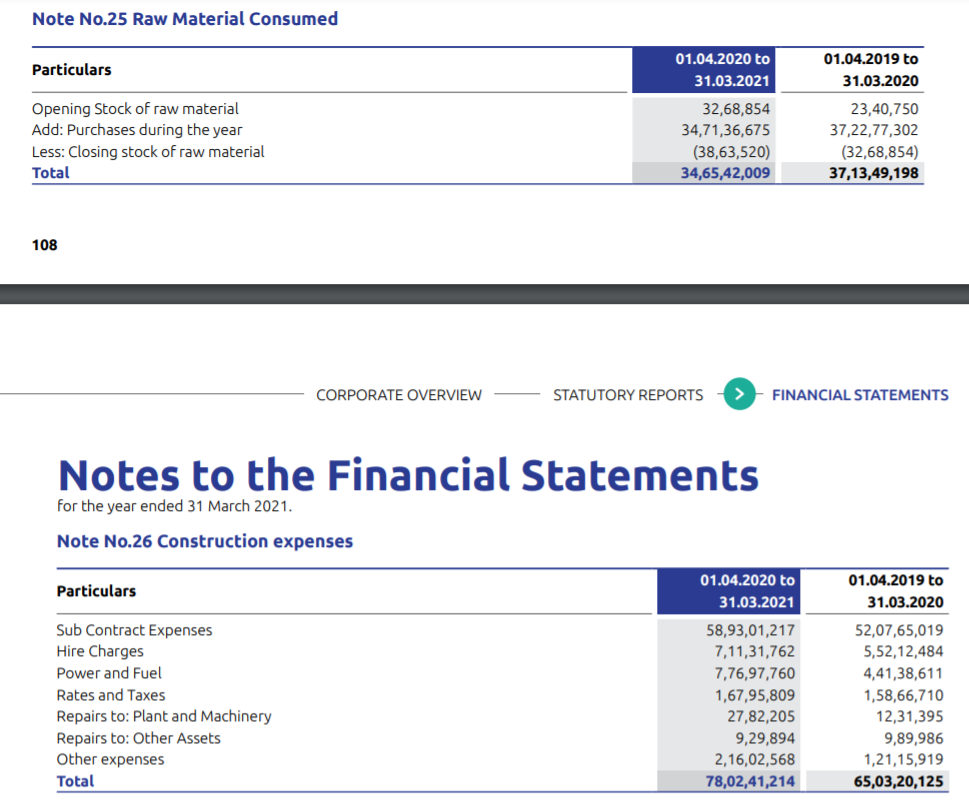

R/m expenses are ~20-25% of revenues and construction expenses are ~40% of revenue for this company. I notice that 75-80% of the total construction expenses are booked under the heading Sub-Contract expenses. If such a high % of their construction is sub-contracted, I wonder what is the material value addition that this company is doing in terms of laying pipelines? It already does not procure most of the R/M i.e. pipelines and now it seems most of the construction is also sub-contracted. Is this common in Infra and Engineering firms? I haven’t studied infra firms before this, can somebody let me know if this high proportion of subcontracting is standard for infra project management companies?

In the same construction cost breakup, hire charges are mentioned as INR 7.1 Cr. I am assuming these pertain to equipment hiring charges. But I find this cost exorbitant because in the DRHP company has mentioned that one of its competitive strengths is that it owns most of the advanced equipment which gives it an edge over other companies which rent equipment via cost-reduction. But the Plant & Equipment net block for the year is only shown as INR 8Cr. The hire charges are almost as high as the net block of in-house equipment. This negates the company’s point about competitive advantage due to investment in equipment.

There does seem to be significant corporate governance and transparency risks in this company.

It is normal in infra projects to subcontract works to avoid more permanent employees. Manpower requirements will vary depends on stages/phases/life span of the project. Also, this will avoid keeping idle manpower during initial and final stages of the project.

Round 11 of CGD bidding awarded. MEIL from Hyderabad won 15 GAs followed by Adani-Total on 14 and IOCL with 9.

I think this is the first time MEIL has bid for and won CGD business. MEIL seems to have its O&G pipeline laying capacity but it seems to be on a small scale. They are also Hyderabad based like Likhitha (Is this to any advantage for Likhitha? Not sure).

Can any conclusions be drawn on what this means for awarding of pipeline laying sub-contracting projects to Likhitha? Difficult to gauge right now. Depends a lot on Adani and MEIL and what they do with their sub-contracts. Adani Total has not been a customer of Likhitha so far. Likhitha’s customers (IOCL, GAIL, BPCL) seem to have won 16 GAs between them against Adani & MEIL’s 29.

Revenues up by 10% both q-o-q and y-o-y. EBITDA margins at 23.5% (30 basis points higher q-o-q and 210bps higher y-o-y).

Some cautionary views : Quality of disclosures have come down. This Quarter they have only published P&L statement. In earlier quarters they were providing Balance sheet and cash flow statement as well. Board meeting lasted a grand total of 10 mins.

I am yet to hear anything from Investor relations cell of company about my queries (30 days since my email to CS)

Invested with a tracking position. Difficult to increase position unless disclosures improve.

Can some please explain what is in investment shown as 62 cr from 56 cr also all the infra epc companies show a poor operating cash flow even PSP projects what is the reason can some seniors show some light on this.

Disl small qty invested

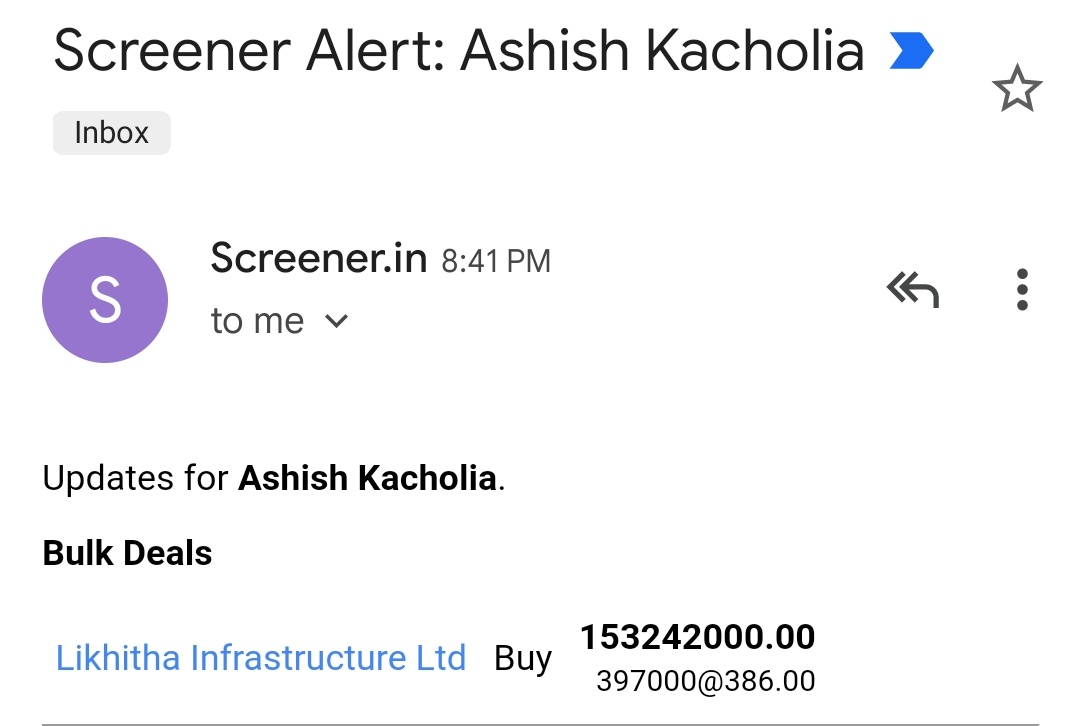

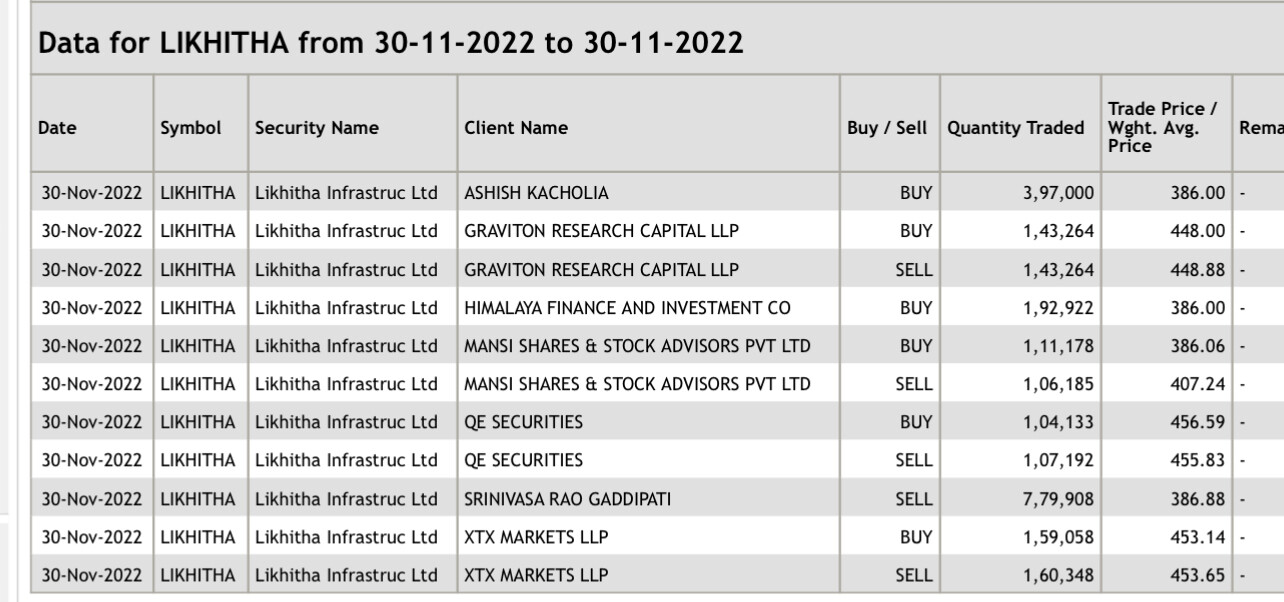

I assume the transaction happened in the block deal trading window.

Slightly off topic but I always thought bulk/block deals cannot be squared off within the same day but some of the following do not seem to obey it. E.g. QE, XTX. Thoughts?