Q2 FY19 UPDATE

The financial results of all the 4 listed life insurers are available.

Following are some thoughts/notes -

The most interesting thing I learned was about max Life-Axis Bank deal. Around 2015, Max issued 5% equity shares to the Axis Bank for the Banca deal. As a part of agreement, Max agreed to buyback 1% of shares every year till year 2020. The most interesting question to ponder is - how to account for any gains Axis Bank might make in the books of Max. Is it commission expense to Axis Bank? How does one account for this in the net worth and consequently in the EV calculation of Max?

Another interesting thing is that 54% of the APE of Max is through Axis Bank. With the former MD & CEO of best Indian life insurance company, HDFC Life, moving to Axis Bank - there is justified apprehension by the investor community towards Max Life. To deal with this channel concentration risk, Max is investing very heavily/aggressively into proprietary channels.

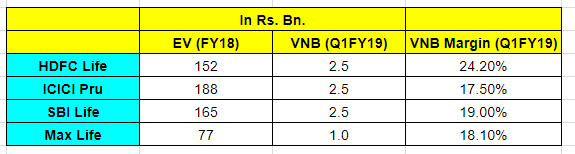

While going through sensitivity analysis of several insurance companies for several quarters, I noticed that increase in interest rates result in decrease in EV/VNB. This was always very counter-intuitive for me as I thought increase in interest rate would increase the spread between reference rate & actuarial reverse discounting rate leading to more value.

But the underlying asset value goes down when the interest rates go up & hence there is negative impact on existing asset value There is MTM adjustment in both the components of EV - Net Worth & Value of In-Force Business. e.g. SBI Life as MTM Loss of 1300Cr in EV in HY19.

In of the interviews, Mr. Bharat Shah explained that Gruh Finance deserves a better P/BV because of higher RoE, 30% dividend & ability to manage without equity dilution for considerable periods of time. I feel the EV multiple also need to consider this finer points. E.g. How does one look at EV multiple for higher dividend paying company vs. lower one. e.g. ICICI Life has dividend payout ratio of 50%+ for fast few years vs. 25% for HDFC Life & 15-20% for SBI Life.

Now coming to short term & long term business trends →

It looks like HDFC Life has built really strong business which can be evident from following observations -

HDFC Group took the decision to open up HDFC/HDFC Bank to other insurers ahead of other similar insurers with bank parentage. The decision to open your business for competition itself shows resolve to strengthen it. The contribution to new business from HDFC group is down to 28%. I think this number is much higher for ICICI Pru/SBI Life e.g. Major portion of credit protect business of SBI Life is from SBI. HDFC Life has created banca partnerships with ~200 partners & that is good first mover advantage over others.

Another thing is 30% of new business premium is from protection & that is huge! The protection contribution for SBI Life is around 11-12% & they have aspiration to take it to ~20% by FY20. With 200 partnerships (and 1/3rd of them exclusive for credit life) for HDFC Life, I think credit protect business will continue to grow at a decent rate. It looks like multi-year opportunity to me with growth rate mirroring credit growth rate over long term. When asked about credit life & protection opportunity, the new MD said that - If one looks at where China is in terms of protection (Mortality/Morbidity/Longevity), there is not even a comparison! She also felt that, the margins might improve further.

Another thing I realized is - not all single/group premiums are bad. If one gets all the premium upfront for credit protect product, the risk of persistency goes away & still the margins are decent for individual credit protect product. On group credit protect product, banks pay the bulk premium to insurer and collect it from individual. Does the banks have incentive to driver the prices of group credit protect products lower?

Now coming to numbers →

ICICI Prudential has reported degrowth in new business premium & hence the stock price has stagnated. Management said that post DeMo, they had growth rate of 50-75% in last H1 & hence it is difficult to better those numbers. HDFC Life/SBI Life has reported much better new business premium growth in the same period.

Renewal premium growth has been strongest for SBI Life & good for ICICI Pru. The number has been lower for HDFC Life but management said it will improve going further.

The VNB growth has come down for HDFC Life & SBi Life as base effect comes in for product mix. The growth has still continued for ICICI Pru because of strong protection growth with product mix changing in favor of protection.

Disc - Invested in ICICI Pru & Tracking position in HDFC Life. This is not a buy/sell recommendation, investors are advised to do their own due diligence.