Nice clarification about evaluating the insurance business.

http://www.livemint.com/Money/QkYShk1Sgr5DHR3POr8UEJ/5-metrics-to-evaluate-life-insurance-business.html

4 Likes

Well, this is sad

G1

1 Like

I have been reading several things to understand more on life insurance & following is potpourri of notes.

THE AIG STORY

I read the book titled “The AIG Story” by Larry Cunningham/Hank Greenberg (CEO of AIG till 2005) to understand the story of AIG (World’s largest insurer followed by bankruptcy). Quite frankly, I found the book to be average & I did not get exactly what I was looking for. But still, following are some interesting points.

-

Product Innovation - it is important to keep looking at new products & when one comes across a new area where risk is low & potential for underwriting profits - one has to act. This is particularly true for general insurers but also appliable to life insurers as well. Some examples of product innovations from AIG - 1) Open enrollments for health insurance for limited time frame - due to limited time, one gets good mix of high/low risk candidates. But if you increase time frame, your risk tends go up. 2) Insurance for airline passengers for delays etc. 3) Insurance against kidnapping 4) Collaborating with yellow hat manufacturers in Japan for accidental insurance.

-

Reinsurance - Sometimes it is better to pay reinsurance premium than to maintain capital for some upcoming losses. Reinsurance remains one of the most important tool in risk management for insurers and using it smartly (getting good deals, offloading concentrated risks) is a very good trait to have in managements.

-

Life vs. General Insurance - In general insurance, years of profit can be wiped out by natural calamity etc. & hence general insurance is not exactly capital light business. Due to this reason, at some point, life insurance business became very important for AIG. This is more stable business with longer term premiums and less concentration risks.

-

Profit Center Models - The book claims in other insurance companies, departments blamed each other in case of bad financial results e.g. underwriting team blamed investment team for bad investments or sales team for bringing in bad clients/bad pricing etc. AIG adopted a profit center model, where head of this center was responsible for all functions of insurance & eventually underwriting profit.

-

Bankruptcy - so why did AIG go bust? I think this is a very big topic in itself & there are several documentaries/books on the matter. To put it succinctly - The investment department of AIG went crazy & management did not understand/care for risks. Till the day of bankruptcy, the book claims that - insurance divisions were still making underwriting profits and were sufficiently capitalized. Two things happened - 1) Assuming people will never default on housing loan, AIG wrote large portion of credit default swaps (where AIG will have to pay money in case of default). There was no hedging and quality/risk of underlying asset was not looked into in depth. When housing crash really came, AIG had to pay large sums of money that it became question of survival. 2) There were several contracts written by AIG with other big financial institutions that they were required to pay money in case of change of value of these swaps - something called as collateral calls. As housing market started going down, a large number of collateral calls were made by these institutions (mainly Goldman Sachs).

So, mota mota, we get following list of qualitative aspects to look for in management of insurance company -

- One can look for whether management is doing products innovations, prima facie, HDFC Life seems to be doing better job than others.

- Does management understand underwriting risk & are there some clues of smart usage of reinsurance (ICICI Lombard seems an interesting case).

- How is asset side book of insurance company & are they going crazy? In India, with many restrictions from IRDAI, this is probably not risk in short term but have to keep tracking for long horizons of 15-20-30-40 years.

- Can profit center model be applicable in India & do regional managers understand things like - actuarial liabilities, high/low risk clients etc.?

ASSET-LIABILITY MISMATCH

If one wants to be a long term investor (10 years+) in life insurance business, then I am absolutely convinced that asset-liability mismatch is the biggest risk one has to look at. In life insurance, one commits to long term liabilities today & there is no repricing or variable repricing e.g. when one writes term protection plan, one commits to a liability which will grow at 5-6% for 30-40 years but it is very difficult to find such a long term assets. Most of the bonds, as I understand, are of smaller duration than these. This is unlike general insurance products where short term rates are well known & there is annual repricing of insurance contract based on developments e.g. motor insurance or health insurance.

Following is the interview of Sanjeev Pujari, actuary at SBI Life -

He very clearly says that finding long term asset for non-par products is hard.

TODO - I would like to spend sometime going through investment books of insurance companies and get some sense of kind of assets they have.

UNDERWRITING PROFITS

I have been absolutely obsessed with this question as to why - life insurance companies are not focusing on underwriting profit. As I am reading more stuff, my sense is that - underwriting profit concept is not strictly applicable to life insurance companies as it is an absolute holy grail for general insurance companies.

This is primarily due to longer term contracts of life insurance products, lesser concentration risk & uncertainty as to long term rate of return for assets. In general insurance companies, short term rate of return on asset is well known & there is large concentration risk. For life insurance companies, one can move actuarial discount rate to 8-10% from 5-6% and there might be profit the P&L statement but that is probably meaningless.

I think getting to HDFC bank kind of numbers, 1.5%-2.5% of RoA & NIM/Spread of 4% with prudent actuarial assumptions, is probably best than can happen.

I can be wrong in above thought process.

LIC

The discussion of life insurance companies is incomplete without LIC. I am going through their annual reports. Following little bit dated report from Edelweiss gives some data on LIC.

https://www.edelresearch.com/showreportpdf-34033/LIFE_INSURANCE_-_SECTOR_UPDATE-SEP-16-EDEL

From Page 8 →

- LIC has < 1% of ULIP business as of FY16 & this space is completely catered by private insurers.

- LIC has negligible contribution from banca channel and 90%+ of its new premium comes from agency channel.

- LIC has pays ~5.8% of premium as commission compared to 4-5% range for private insurers.

- LIC’s opex ratio still lowest in all insurance players (8.5% vs. 9.2% for SBI Life & ~11% for ICICI Pru/HDFC Life)

What do things imply? →

- If LIC decides to enter ULIP business, then growth for private insurers might moderate given LIC’s reach & brand. Why it discontinued ULIP business in FY13 is an interesting question to research.

- if LIC manages to get good banca deal (a la Axis or Yes or India Post - if it gets license in future), given its brand & reputation, it will give tough competition to private players.

Private players taking market share from public players is a trend we have seen play out in several industries but one can not completely write off LIC yet.

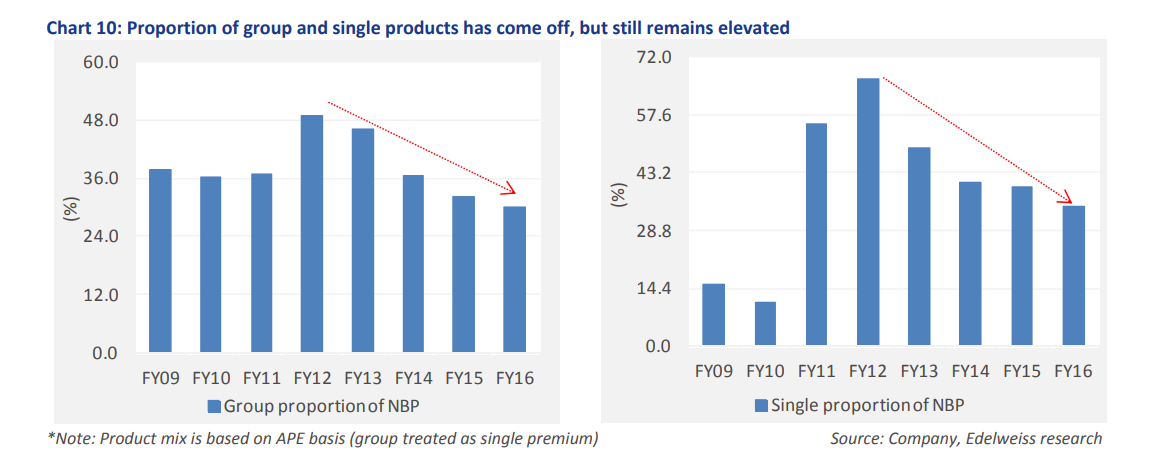

GROUP & SINGLE PREMIUMS

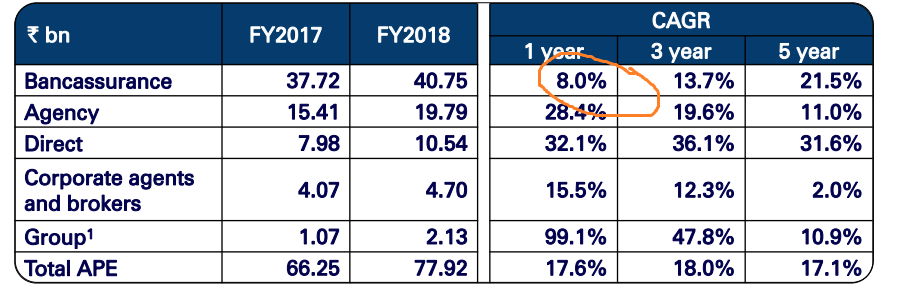

For HDFC Life, proportion of group & single premiums has been rising & one of the key components of growth.

From above report,

For SBI Life, the proportion has come down but still remains high.

Logically, group business shall be a low margin business but we need to understand if HDFC Life has some edge in this business where they can make more profit than others.

SBI Life Q2 conf call said some interesting things on this matter →

- They have been consciously de-growing the group saving business. SBI Life’s quarterly results have to be looked in this context.

- SBI Life claims that this is a very volatile business which is given to the party which offers highest interest rate on annual basis. e.g. a company having a gratuity corpus of 1000Cr. might select SBI Life to manage that asset as it offered 6.8% interest rate.

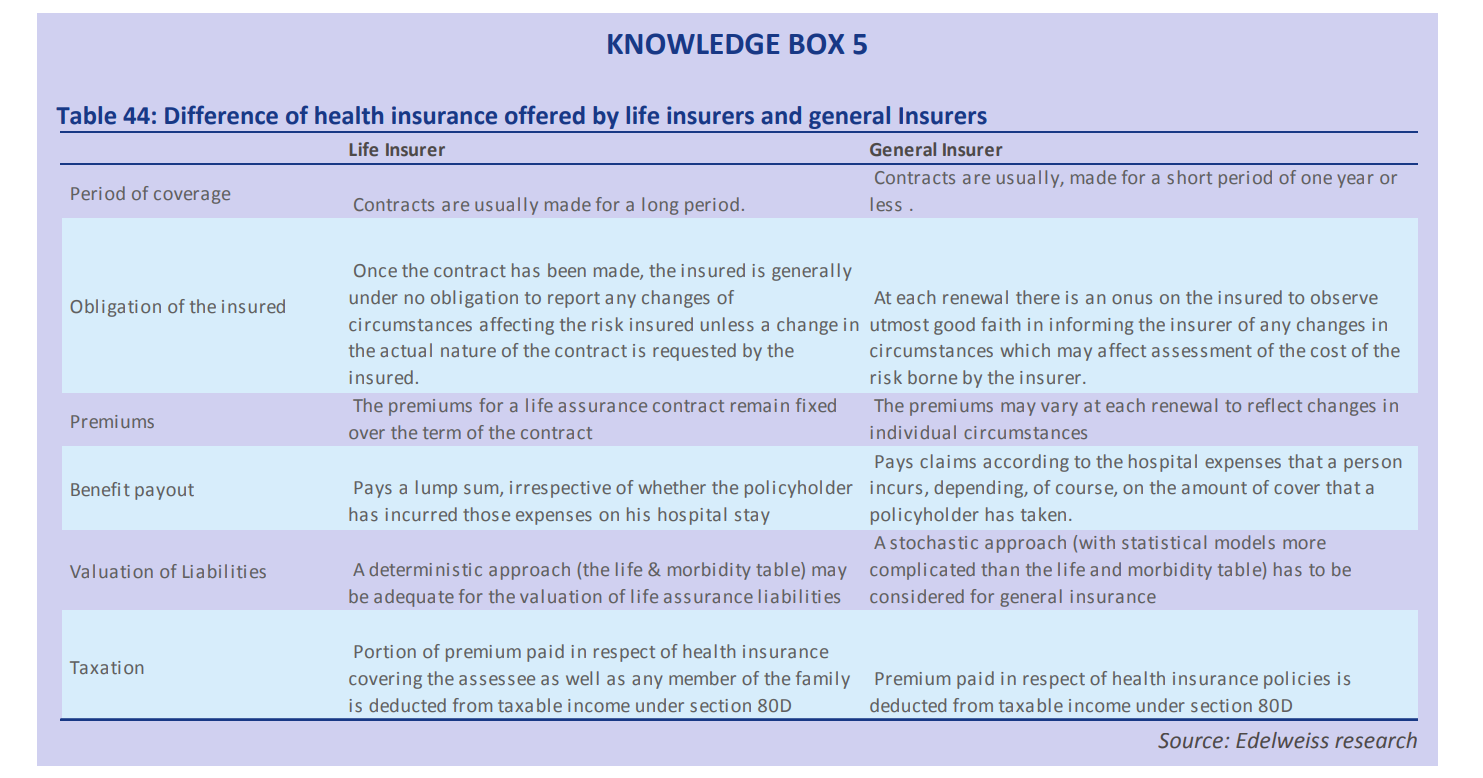

DIFFERENCE IN HEALTH PRODUCTS OF LIFE VS. GENERAL INSURERS

In summary, health products by life insurers are long term contracts with premiums fixed upfront for entire duration & payout is fixed lump sum amount unrelated to hospitalization cost. Whereas health products offered by general insurers are annual contracts where premiums vary at each renewal & payout is based on hospitalization cost.

MISCELLANEOUS

- HDFC Life has almost 3-4x credit protect business compared to ICICI Life/SBI Life (17bn Rs. vs. 3-4bn Rs.). In this product, HDFC life offers insurance against the loan in case of death/disability of personal who has taken the loan. The lender pays single premium to HDFC Life & gets premiums from person over multiple years. This is reported in group/single premiums.

- As established before, SBI Life has lowest non-claim expenses compared to ICICI Life/HDFC Life. There seems to be two reasons for this - 1) SBI, parent bank, seem to be less demanding in terms of commission than other private bank parents. 2) SBI Life follows model where selling is driven by SBI employees rather than SBI Life employees sitting in these branches (BNP Paribas, partner in SBI Life, follows this model). SBI Life has 2500 employees sitting in SBI bank branches of 25,000 vs. 4000-4500 employees for ICICI Life/HDFC Life against branch network of 4000-4500.

- HDFC Bank is no longer exclusive partner for HDFC Life. Due to open architecture, bank has signed up two other insurers, namely - Birla Sun Life Insurance & Tata AIA Insurance.

- SBI Life’s geographical concentration is less compared to HDFC/ICICI Life. Top 5 states contribute 38% in NBP for SBI Life compared to 50% for ICICI/HDFC Life. SBI’s premium per branch is quite low compared to other two and there is significant scope to move that number up for SBI Life.

Views invited.

Disc - same as last post

18 Likes

A good article on insurance sector

https://moiglobal.com/magic-of-insurance/

Another article giving good insight…

1 Like

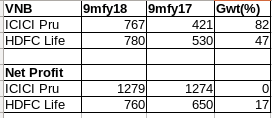

Today both ICICI Pru and HDFC Life came out with their results. I am presenting below the data which seems most striking to me.

1 Like

Find enclosed a good article on Global insurance market (Both Life and General) by McKinsey. Although it is dated, provide good insight about global market of insurance sector.

https://www.mckinsey.com/~/media/mckinsey/dotcom/client_service/Financial%20Services/Latest%20thinking/Insurance/Global_insurance_industry_insights_An_in-depth_perspective.ashx

1 Like

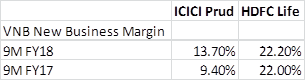

Add one more Parameter VNB Margin for 9 months

2 Likes

Hi @rupeshtatiya Thanks for your comments .For others I just clarified the Actuarial liability part where the Cost of float will be the Difference in the Actuarial liability from the PY and the CY . I just had a Few variables to make it easy for me to analyse

- Who is the Conservative Underwriter ? How do we know this ?

The cost of the Policies Underwritten , The Non-claim ones mainly as we know the Cost of acquiring a new business is a strain at the initial phase for a Non-participating product. The NON-Claim ratio is a important parameter here.

The Cost of operations , This would be the cost for Total Operations

Need not Quote buffet here but we know the Low cost Underwriter is an added advantage in the Insurance business .

is there an important variable on this part of the insurance business that we can use .

- Risk management ? The Portfolio of products Underwritten , The ULIPS tend to perform well in the Bull market phase but this does not have a Float and does not help the insurance company make any money , Its the Non-Part part which provides with the Float .

Assumptions , The Interest rate assumptions are an important parameter here. The return on investments both Policy holders funds and the Shareholders , How well are the portfolio of funds being managed .

We would like to see how the funds are performing when the market turns down , there will be a lower Investment income and withdrawals of ULIPS at a faster rate . So then the obviously growth will slow down and lower policy under-Written will lead to a Deficit instead of Surplus.

Companies shell out loans on the policies maturity value and ICICI has said this portion is good for them , So many default here , This is like the typical LAP portfolio of a NBFC .

The Cost of float and Spread are an important assumption as mentioned earlier by @rupeshtatiya .

Note :On actuarial liability need a clarification HDFC Standard Life - Change in Valuation reserve is 16055 and the Interest rate assumption is around 5.7% does this mean they expect this fund to grow at 5.7% ( Some one clarify this , am i interpreting it correctly )

To value a Insurance business mostly EV is used and so it depends upon the Actuary. Extrapolation or incorporating an Assumption on our own becomes a little difficult with Insurance companies . I have tried reading the Berkshire -Fair fax blog If anyone is a member can help with this , Have heard that there are good amount of experienced people who have written about Insurance business .

3 Likes

And a follow up on the above , As per the excel sheet in C16 the 16055 is the total Actuarial liability but what we want is the change on Actuarial liability so actual change is around 10127 and post which changes in Non -linked and linked portion will change and there will be a positive float and cost of float in C70 would be around 10 % rather than -5 % Uploading…

Any one tracking Max Financial here? Making new lows each day and market seems concerned about the huge capital raising plans to fund an acquisition. Any other views?

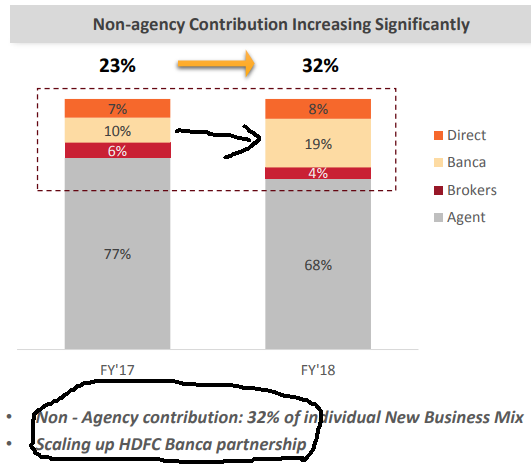

A look at how Banca channel is evolving

In the investor’s presentation of Aditya Birla Captial, there was a slide:

There is a big jump in Banca channel sourced NBP. Interestingly, they want to “scale up HDFC Banca partnership.” We know that IRDAI has permitted three partners now and going forward it is great news for certain non bank promoted insurance companies.

I feel that strength of banca channel will become a weak moat (or competitive edge) for an insurance company. IRDAI has permitted a bank/financial entity to have upto three insurance company partners to sell policy. This is good for non bank promoted companies like Aditya Birla Life, Bajaj Allianz Life or Max Life, etc.

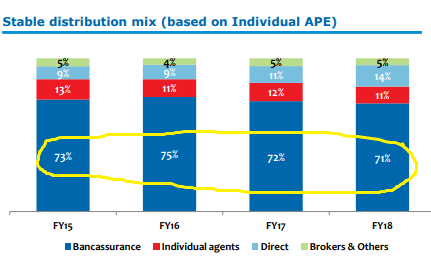

In fact, the share of banca in NBP is coming down for ICICI Pru Life:

It has come down from ~56% to ~51% of NBP. Also note that the growth of banca sourced NBP which has been moderating lately.

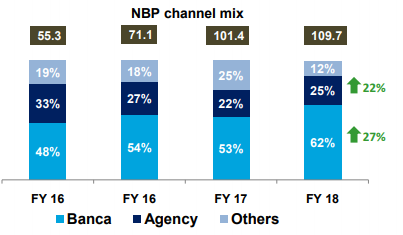

… and same for HDFC Life where banca share is coming down:

SBI Life is growing its banca sourced NBP which is understandable given there is a lot of potential to tap their SBI branches for protection plans. This would explain why SBI Life trades at a premium to ICICI Pru Life (though the gap has come down now) though it would be perceived as a quasi-PSU company.

We are seeing more banks and other financial institutions now listing all their banca partners. HDFC Bank itself lists HDFC, AB and Tata Life:

HDFC Life wanted to merge with Max Life earlier perhaps for their banca partners like Axis Bank and Yes Bank among others. Amitabh Chaudhry, MD&CEO of HDFC Life, mentioned that they are open to acquisition and one criteria apart from valuations would be to see if other player having a competitive edge like strong banca partner which they might be lacking. Axis Bank now lists Max as well as LIC:

DBS Bank lists all their three partners and they were the first to go beyond an exclusive partner and said they wanted to give choice to their customers.

ICICI Bank lists only ICICI Pru Life:

I checked others banks (who don’t have a Life Insurance Subsidiary) like RBL Bank (showing exclusive HDFC Life plans), Indusind Bank (showing exclusive Tata AIA Life plans) and Yes Bank (showing exclusive Max Life plans).

7 Likes

A discussion with HDFC LIFE’s Amitabh Chaudhry where he also talks about banca & agency model and how they plan to increase the agency part from current 11% to 25-30% in the future (quoting LIC’s model which has major sales coming in from agents)

Hii Rupesh, thanx a ton for the insights into the cost of float calculations…however i have following doubts -:

- As per your formula, Cost of Float = Non-linked (Premiums - Commission - Operating Expenses - Misc Expenses - Actuarial Liabilities) / Float

But shouldn’t it be only (Commission + Operating Expenses + Misc Expenses + Actuarial Liabilities)/ Float…

By simple logic cost of float should be directly proportional to the expenses borne and actuarial liability or in other words the cost of float is the cost incurred in maintaining the float…but with the given formula, the cost of float becomes inversely proportional to the expenses and actuarial liability i.e if expenses and actuarial liability increase the cost of float will reduce…

the second point is regarding the reserve and surplus of ICICI which is 2700 cr more than of HDFC…is it because of profits flowing from more no. of ULIPs to share holder reserve in case of ICICI than HDFC…

Request for your guidance…

Hi Sumit,

I think you are confused about sign i.e. result of above calculation can be negative (company has to pay money to generate float) or positive (people are paying company to manage float).

Cost of float is akin to interest one has to pay on borrowed loan every year. To calculate that what we have to do is take (present day income - all expenses - present day value of future liabilities).

In the formula as expenses go up, numerator becomes -ve i.e. company has to shell out money to generate float.

One thing to look for is - cost of float is lesser than actual interest rate on the loan that company can get from market. If company is losing 10% money every year in generating float - it is useless. They can rather borrow the money from bank & invest it.

Any “actuarial surplus” from various product lines of insurance (Par/Non-Par/ULIP etc.) gets transferred to reserves of the balance sheet. Some product lines make more losses in the initial years of policy than others and surplus is a function of product mix, growth rate & persistency. It may be possible that higher ULIP contribution is leading to higher surplus in case of ICICI Life. One would have to go through breakdown of surplus/deficit over the years & see which product lines have contributed in increasing of surplus.

Regards,

Rupesh

1 Like

thanx a ton Rupeshji…i have understood your point…actually i was wondering about the better spread for icici in last two years when compared to HDFC…so with my limited understanding, following points stand out-

-

ICICI has produced better yield on its investment during previous two years…may be due to their larger holdings of equity portfolio and good market returns in last two years…

-

ICICI has been able to control their cost of float much more than HDFC…in fact the difference here is much more than in case of yields…

| FLOAT | |||||||

|---|---|---|---|---|---|---|---|

| ICICI Pru Life | Non-linked Float | 33707 | 27732 | 24715 | 19792 | 16196 | 12580 |

| Growth of Float | 22% | 12% | 25% | 22% | 29% | 37% | |

| Cost of Float** | -3.90% | -2.20% | -7.40%** | -3.70% | -8.10% | -6.50% | |

| Yield on Float | 7.70% | 7.40% | 7.30% | 6.70% | 7.40% | 6.10% | |

| Spread on Float | 3.80% | 5.20% | -0.10% | 3.00% | -0.70% | -0.40% | |

| HDFC Life | Non-linked Float | 37937 | 28503 | 22104 | 16322 | 11561 | 8579 |

| Growth of Float | 33% | 29% | 35% | 41% | 35% | 42% | |

| Cost of Float** | -5.10% | -2.60% | -7.30%** | -8.30% | -4.20% | -6.80% | |

| Yield on Float | 7.20% | 5.70% | 9.90% | 7.10% | 7.20% | 6.60% | |

| Spread on Float | 2.10% | 3.10% | 2.60% | -1.20% | 3.00% | -0.20% | |

| SBI Life | Non-linked Float | 51258 | 41821 | 34574 | 27677 | 30409 | 18310 |

| Growth of Float | 23.74% | 3.48% | 21.73% | 7.72% | 0.30% | 7.90% | |

| Cost of Float | -6.40% | -6.30% | -7.30% | -7.70% | -6.10% | -7.00% | |

| Yield on Float | 8.10% | 8.00% | 8.40% | 8.10% | 6.20% | 7.70% | |

| Spread on Float | 1.70% | 1.70% | 1.10% | 0.40% | 0.10% | 0.70% |

This extract id from your spreadsheet…

-

When i looked deeper about the lesser cost of ICICI, following things emerge-

(a) There has been a steady decline in the claims for non linked policies in case of

icici…this has resulted in lesser cost for them

For ICICI|Claims|932|1521|1721|953|

|%of Premium|16.7%|32.4%|42.3%|23.9%|

For HDFC

|Claims|1818|1564|1673|760|

|%of Premium|17.8%|20.6%|26.0%|14.9%|

For SBI life

|Claims**|4119|3354|2809|3517|**

|%of Premium|38.1%|38.2%|37.5%|55.2%|

Im not able to understand implications of lesser claims being paid…is this forcing ICICI to

be more conservative as they may have to pay more in future…or ICICI is lesser policy

holder friendly…or if we see the claims as % of premium, previously ICICI had higher share

of claims as compared to HDFC and now they have brought it in line with HDFC…SBI still

has quite high percentage of claims to total premium…this may mean that HDFC has been

strict in paying claims historically and now ICICI is following their league…but even than

HDFC has never shown such a decline in claim expense till now as ICICI is exhibiting…(b) Since the cost of float is effected by the denominator which is float we need to compare

it for ICICI and HDFC…ICICI has 11% lesser float than HDFC but its premium earned are

45% lesser than HDFC…this means that the numerator in the formula will decrease more

than the denominator, which will reduce the cost of float…

In other words, the ICICI is able to invest more float with lesser premiums than

HDFC…since the premiums earned are lesser, the non claim expenses also reduces and

cost is further reduced…

But what is the source of this float…to sum up i added all the premiums earned by ICICI and

HDFC till date…HDFC has earned a total of 41537 cr non linked premiums and their non

linked float is 37937 cr which means an expenditure of approx 3500 cr till date…

ICICI has earned total of 30831 cr of non linked premiums till date but they have 33707 cr

of non linked float…it means a large money have flown in from some other source to non

linked float…what is that source…

I am just trying ti understand the difference in strategy of two companies and the relation of

discount rate assumption to that strategy…Request for your comments…

Hello everyone…i am planning to invest in the insurance industry and comparing the two top players in terms of performance i.e HDFC and ICICI…im trying to understand the higher valuations of HDFC std life over ICICI…after my analysis following points of comparison stand out-

-

Product mix HDFC certainly has better product mix as it has higher share of protection products which provide higher margins…ICICI has higher ULIP share but they are also trying to increase their Protection share as told in this concall…but they have a long road to cover…

-

Distribution channel Both companies enjoy a strong banca channel and they are betting upon the direct online channel for future…however HDFC has shown greater growth in online distribution…HDFC seems to be quite strict about their margins while distributing through agents…

-

Acturial liabilities assumptions ICICI seems to be more conservative in their assumptions when compared to HDFC…but i feel IRDAI will ensure the solvency of these companies…so the aggressive assumptions by HDFC may not be a sign of worry…

-

Strategy ICICI is a retail focused company while HDFC has a larger share of group businesses…in terms of product mix, HDFC mgt says that their tgt is to keep ULIP share between 50-60% while ICICI mgt says that they dont have a tgt for product mix but it will depend on the opportunities…Retail products may have more margins than group buisness as disclosed by Rupesh in other thread but ULIP is certainly less profitable than Protection…

-

Protection business Industry is well aware that protection products have better margins and thus they are leaping towards increasing the share of protection products…however the segment is hugely under penetrated and competition may not be very effective for some time in future…so growth opportunity exists for both ICICI and HDFC in protection segment…

-

Cost efficiencies ICICI has reduced its expense ratio but for HDFC it has increased, mainly due to higher commissions to the agents…HDFC management has stated that they are working hard to create a strong agency channel with good margins…

-

Valuations HDFC has much higher valuation than ICICI even when the growth opportunity exists for both of the companies…HDFC ssems to be leading the show with better product mix, innovative products and a much clearer vision but even than its more than double valuation than ICICI is certainly on much higher side…however the brand factor may be playing a role into it as trust factor plays a very important role in Insurance…

But i believe that when we talk about the under penetrated market for protection products, the small and rural areas form a chunk of it where both the players might have similar brand value… -

Dividends I think ICICI has a policy of 40% dividend payout along with 20% special dividend while HDFC is paying out 30% of the profits…

So i feel that insurance as a theme as a good prospectus and it will be difficult to clearly select a winner out of two…for a investor like me who is entering market on a SIP kind of method, both of them can emerge as a good bet…

request for any other point of comparison and views from fellow members…

regards

9 Likes