First a little Context in what we are trying to do here:

-

As you must be aware that insurance is a business of taking on risk for a fee. The underlying financials of most of the insurance companies are almost like greek and latin, even for the well versed in accounting.

-

The Insurance Industry and accountants simplify the whole financials in to simple monitorable parameters like VNB(Value of New Business), Mortality Rate, Types of Policies (Participating and Non-Par) etc. These figures take some facts and some estimates to get to the right answer. The problem lies in not being able to compare these estimates.

The problem I am trying to solve is three-fold:

- Make the financials comparable across the companies in the life insurance sector.

- Take the financial parameters which are as real and not as much subject to estimates as possible. If not at least the parameter must be well regulated (i.e. if the company falsifies the parameter then the promoters should be put in jail).

- Make it as easily understandable.

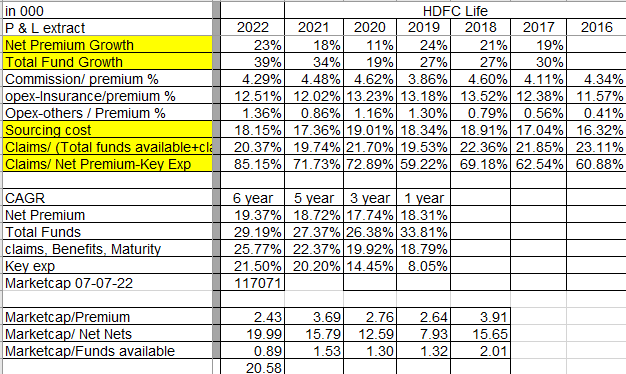

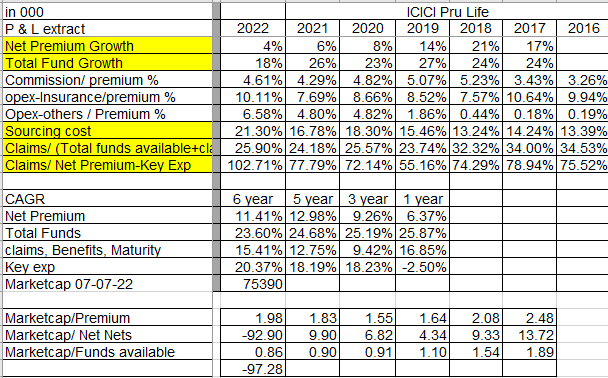

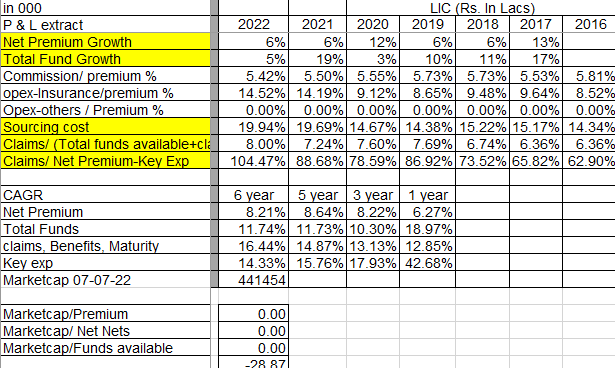

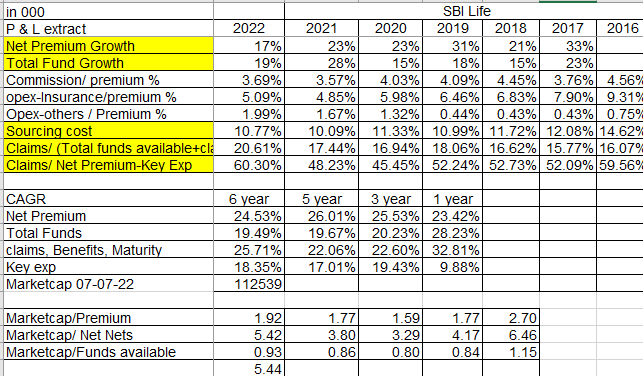

Some Context here : This year was particularly hard for the companies as the death claims during the 2nd covid wave indeed shot through the roof in India. So naturally all the companies showed record number of claims. LIC finally debuted on the exchange and it would be unfair to compare it’s Share performance.

We are evaluating the companies(SBI Life, HDFC Life, ICICI Pru, LIC) on 4 factors

-

You have to get max. premium so that you can easily pay your claims.

This Year HDFC Life was the top lead with SBI Life being in close lead at 17% -

You have to be the best in industry when growing funds with very good rates of return

HDFC Life grew very well like last year in fact it out grew every other company and ensured that the funds available for claims increased despite collecting lower premium. -

Being the best underwriter i.e. skewed underwriting where you prefer certain demographic like non-smokers, govt. employees (excl. police/army) etc.

Still no company shows such a skewed underwriting skill. In fact the regulator has indirectly not allowed such skewed underwriting. -

Low cost sourcing of policies and Low cost Operating Expenditure.

SBI Life leads the with lowest cost structure.

How did the market react to these financials in the last 1 year

SBI Life gave a decent performance while HDFC Life did have a fall. ICICI Pru Life fell.

From Market cap perspective we understand that SBI Life is relatively cheap and hence did not fall by a huge margin. SBI Life was also collecting decent amount of premium and a decent amount of growth.

HDFC Life’s fall was curtailed as it gave a top notch performance among big 4. The premium valuation came to haunt and reduce it’s price. Still HDFC life enjoys a premium over it’s peers.

ICICI Pru Life and LIC had negative Net Nets excluding taxes (Premium- Claims & Benefits - Expenses). However a look at it’s P&L does not show a Loss the reason is like banks the regulator makes you put aside provision every year, so that you can use it in such circumstances.