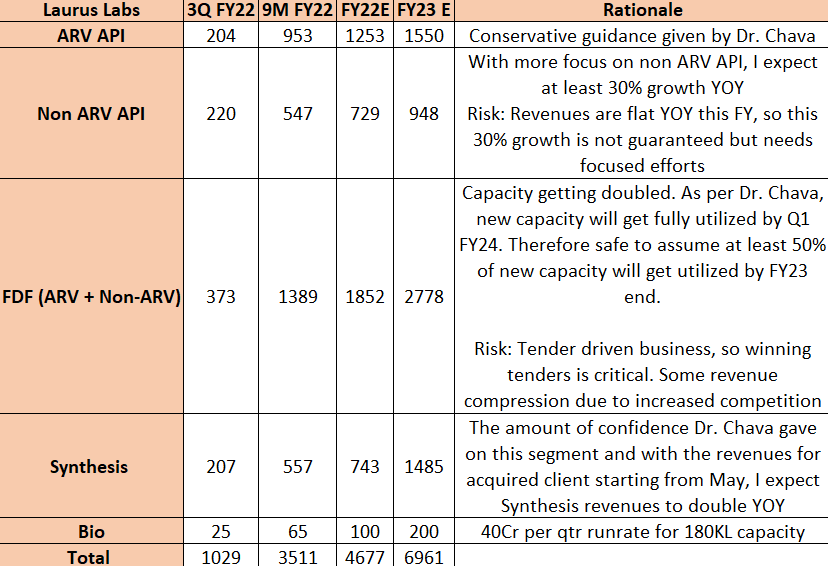

Re-assuring call for Laurus Labs. Based on what Dr. Chava indicated, these are my base case numbers for next FY:

In spite of such high operating de-leverage, Q-o-Q EBITDA margins have more or less held, thanks to higher gross margins from Synthesis business growth. Q3 gross margins are at 59%. As % of CDMO business moves to 25% by FY25, these gross margins can easily inch up towards 65-70%. USD 1bn in FY23 may be a bit of a stretch but falling short of that by a few 100Crs is far from a debunking of the investment thesis.

Key risk in this hypothesis is disruption of ARV business via injectables. Some questions needed to be asked to Dr. Chava today on the call regarding injectables, but I didn’t get the chance:

- Why doesn’t he view that as a threat in LMIC in the view of bullish commentary by sourcing/funding/approval agencies?

- By what year does he think injectables can become viable in LMIC and what are Laurus’s plans around that?

What will cause me to change my views on Laurus towards the negative?

- If ARV API revenues don’t clock at least 300 Cr in Q4

- If there is significant market share loss in ARV FDF which may cause new capacity to remain sub-optimally utilized in FY23 and FY24.

- Flat growth in non ARV APIs and formulations

- Gross margins reducing

Right now I think recent price action is a good opportunity to buy in tranches. Post Q4 results, situation needs to be re-assessed again. As I write this, Laurus has rebounded around 7-8% from its low today (Dr. Chava’s words?)

Invested at 500 levels, did not add at 450-460 levels as I was waiting for Q3 concall. Plan to add 10-20% of present holdings between now and Q4 results.