Hi Raj,

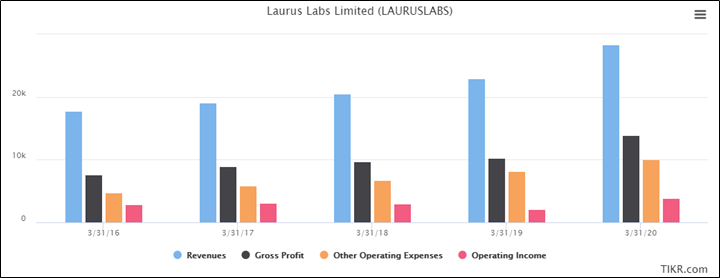

Yes that is indeed true. From the latest investor presentation (FY21Q1) it is evident that since 2019-20, the contribution from Generic FDF division has increased by manifolds. That has subsequently increased the net revenue steadily as can be seen in the Figure - 2 below.

What I also noticed is that the management has clearly written in the presentation that as part of their future outlook, they are focusing quite heavily on the Generic FDF division (more on that later) – stating that they are doubling their FDF capacity by FY22.

However, as can be seen in Figure – 2 that constantly increasing operating expense meant that the operating income from this increased revenue is yet to play out.

Now quickly focusing on their Outlook For FY21 and Beyond :

- Partnership with Global Fund offers higher volume contracts with reasonable predictability in FDF Tender business – which is a good news considering the Generic FDF business has now became a major contributor to the company revenue

- Have a healthy order book for FY 21 & beyond in FDF CMO business

- Robust growth in Other API segment to continue on the back of higher order book visibility

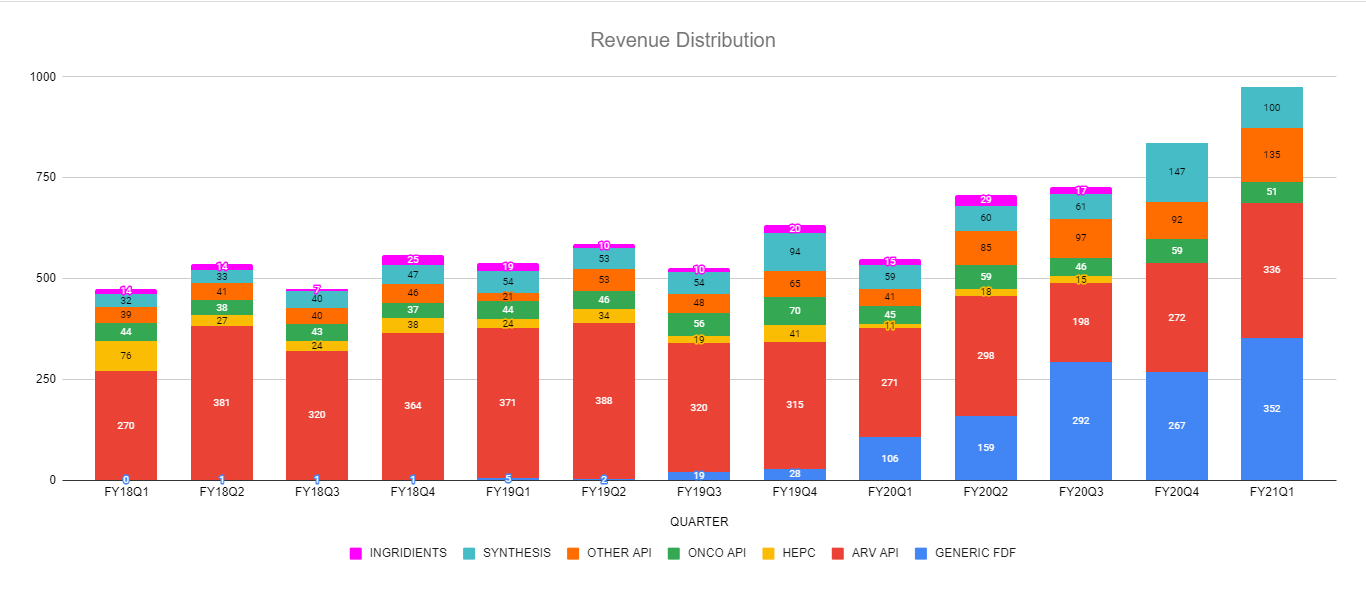

- Changing business mix to drive growth - Generic FDF segment contributed 36% in FY21Q1 total revenue as opposed to a mere 2% in FY19

- Non-ARV API business (HepC, Oncology & Others) to contribute significantly showcasing the speed of diversification of revenues.

- Scale up in engagement with Aspen

- Acquired Aspen’s South African Subsidiary, in order to get a foothold in worlds’ largest Generic Accessible ARV market – shows a lot of positive intent

- Acquired assets of an API Unit in Vizag to be used for backward integration and pre-clinical chemistry – once again shows that they are not going to sit pretty any time soon

- All the green field expansion have now turned Cash positive in FY20 with near maximum utilization

- Continue to undertake Brown Field Capex programs for Capacity addition in line with strong order book visibility and business outlook

Some other critical points which I have noted from the FY21Q1 investor presentation are below :

-

Generic API division showcased a healthy growth of 40% YoY

- Anti Viral segment recorded growth of 19% YoY

- Onco API revenue showed a growth of 13% (YoY)

- Other API revenue showed a robust growth of 207% (YoY)

-

Generic FDF Revenue Showcased a robust growth of 232% YoY

- The growth was led by higher LMIC Market volumes and increased volumes from North America and EU

- RoW (Rest of the World) Markets – Received approvals for TLE400 and TLE600 from the US FDA

- Entered into a long term partnership with a leading generic player in EU region for Contract Manufacturing Opportunities

-

Custom Synthesis division recorded a strong growth of 37%

- Total Number of Active Projects in the CDMO division stood at 47 as on Q1 FY21

- Incorporated Wholly Owned Subsidiary to give increased focus and eventually dedicated R&D and Manufacturing

- Commercial supplies started for 4 products

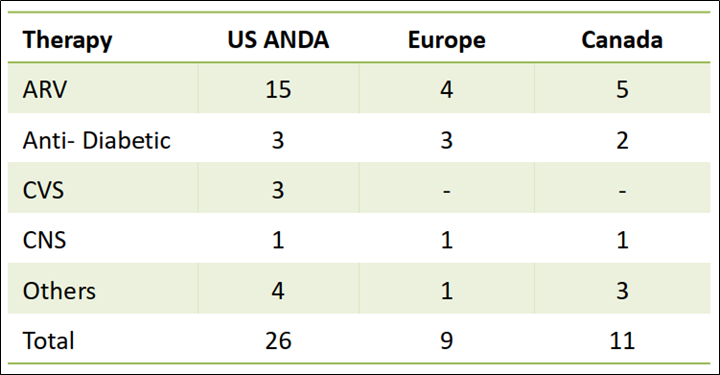

Finally let us focus on the number of fillings they currently have in their portfolio.

Edit : 15 Sep 2020

I have been able to assort the revenue distribution by segment from all the investor presentations available in the website of Laurus Labs.

I present the numbers in the chart below. I thought it was much easier for me to comprehend the prevailing investment thesis with this data. Hence sharing.

Disclosure : I am not invested in the company - but I intend to when the valuations are more attractive.