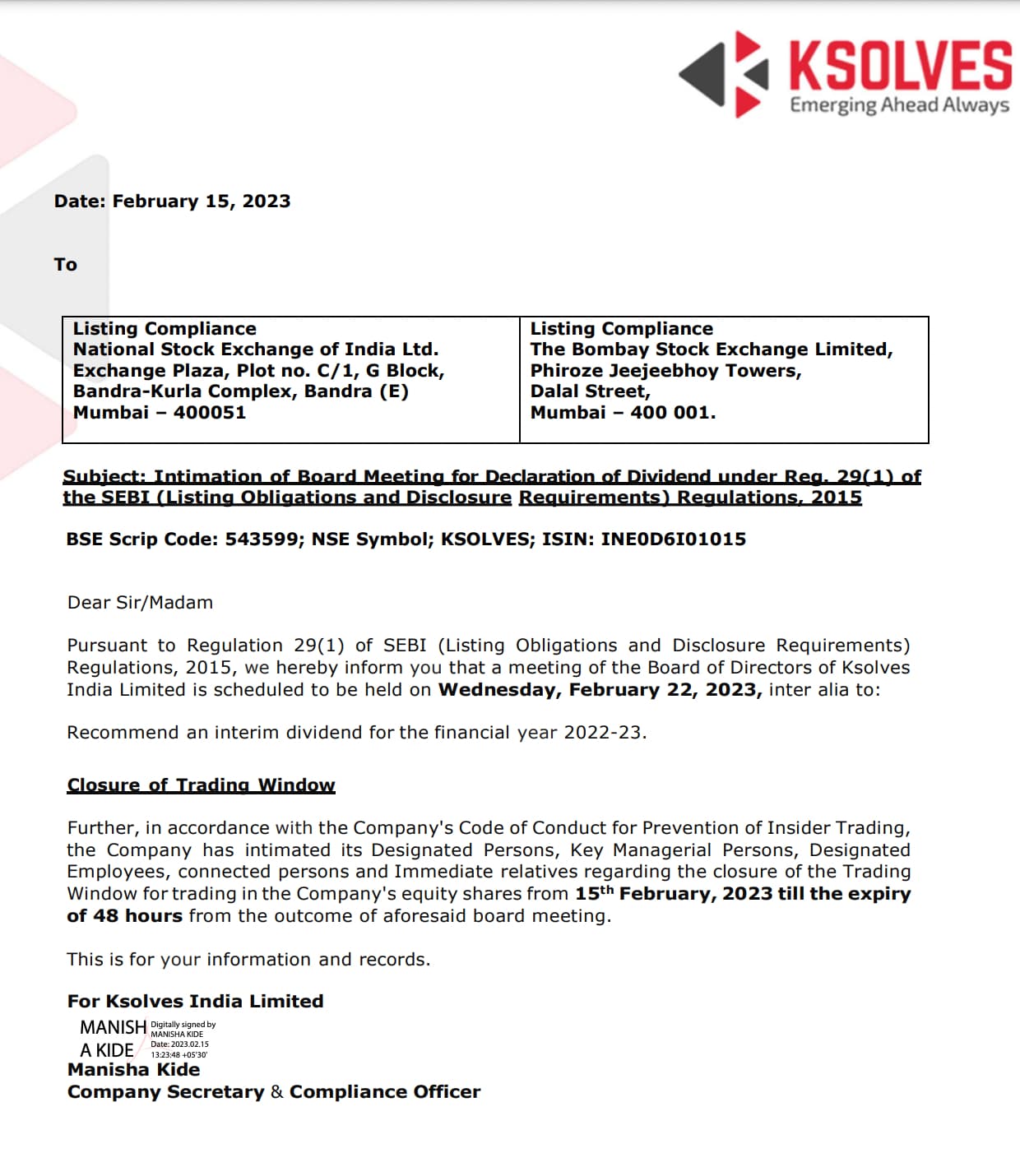

Was surprised when they did not consider to announce a dividend in the Q3FY23 board meeting.

Nevertheless, here it comes ![]()

Disc- Invested

Was surprised when they did not consider to announce a dividend in the Q3FY23 board meeting.

Nevertheless, here it comes ![]()

Disc- Invested

Good news from Ksovles. Ksovles becomes Salesforce Crest Partner. As per tweet, it mean being promoted from Silver to Gold partner for Salesforce.

Dsiclosure: Not suggesting any investment action. Not a SEBI registered advisor. I increased my holding in the company from 1% of portfolio to 3% of portfolio post-Dividend declaration in February 2023. My view may be positively biased due to my investment. I have been wrong multiple times in past and very high probability that my past performance can be repeated in future as well. ![]()

Valuation wise, in all parameters the company looks okay. Its not cheap but Its not costly as per my opinion. But if we take a look at the P/B, it is 28.7 times. No IT company and barely any other company trades at that kind of P/B valuation. Why this kind of discrepancy?

I request experts if they can shade some light on this.

The company paid very high dividend (almost 100%) so no profit is added to accumulated reserve of the company. Due to this, Book value of company would see limited growth. However, same would also reflected in very high ROCE and RONW ratio, as net worth is very low and not growing, while profit is increasing. Further, generally in my understanding, high RONW business with growth are generally traded at relatively higher P/E multiples. My understanding may be wrong, so reader shall do his/her own due diligence.

Discl: Same as last post

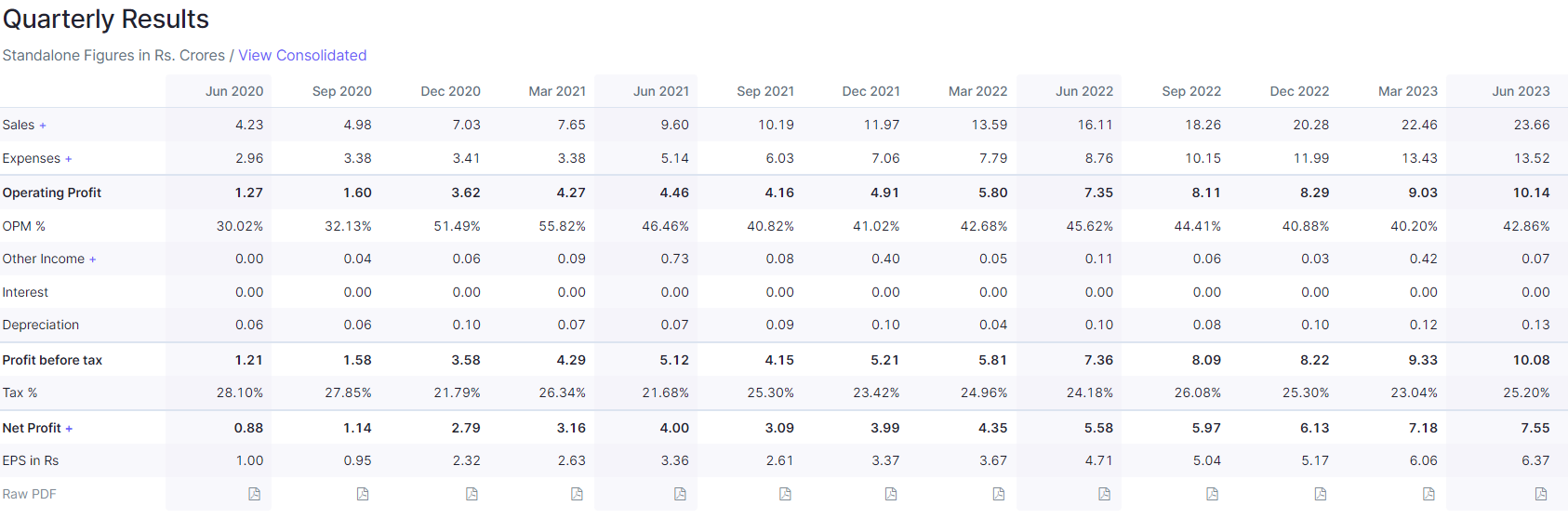

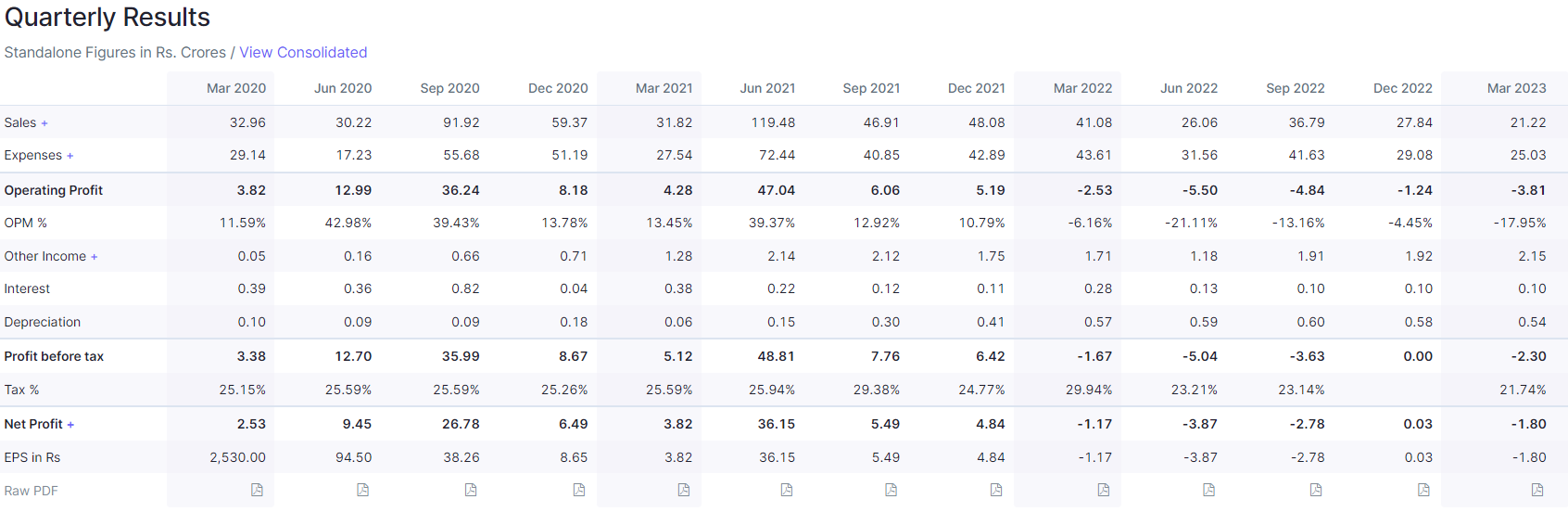

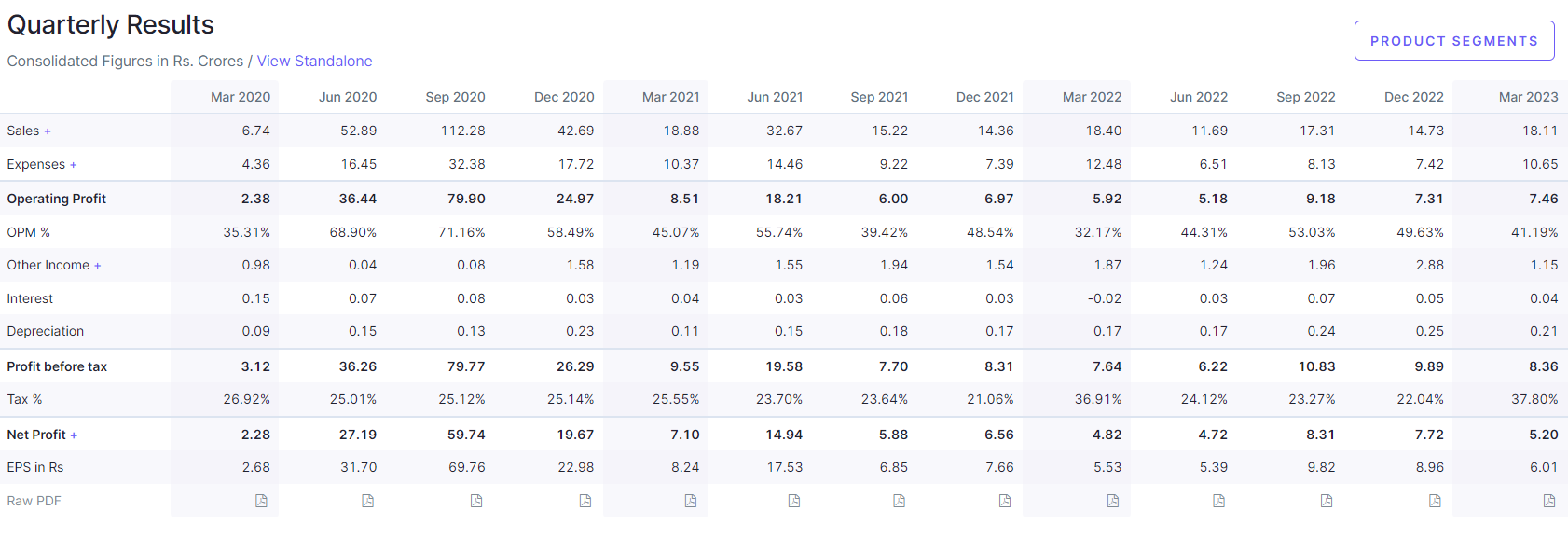

Good consistent set of results from Ksolves again!

Highlights of Financial Results:Q4’FY22-23

•FY 22-23, Total Revenue ↑ 66% YoY (78.31cr vs 47.07cr)

•FY 22-23, Profit After Tax (PAT) ↑ 56% YoY (24.72cr vs 15.89cr)

• Q4, Consolidated Revenue from Operations ↑ 60% YoY (22.7cr vs 14.2cr)

• Q4 PAT ↑ 66% YoY(7.33cr vs 4.42cr)

Also, Dividend of Rs. 8 per share is announced.

I would have loved to see the management commentary on the the results and future. But not provided this time as well.

Disclosure: Invested

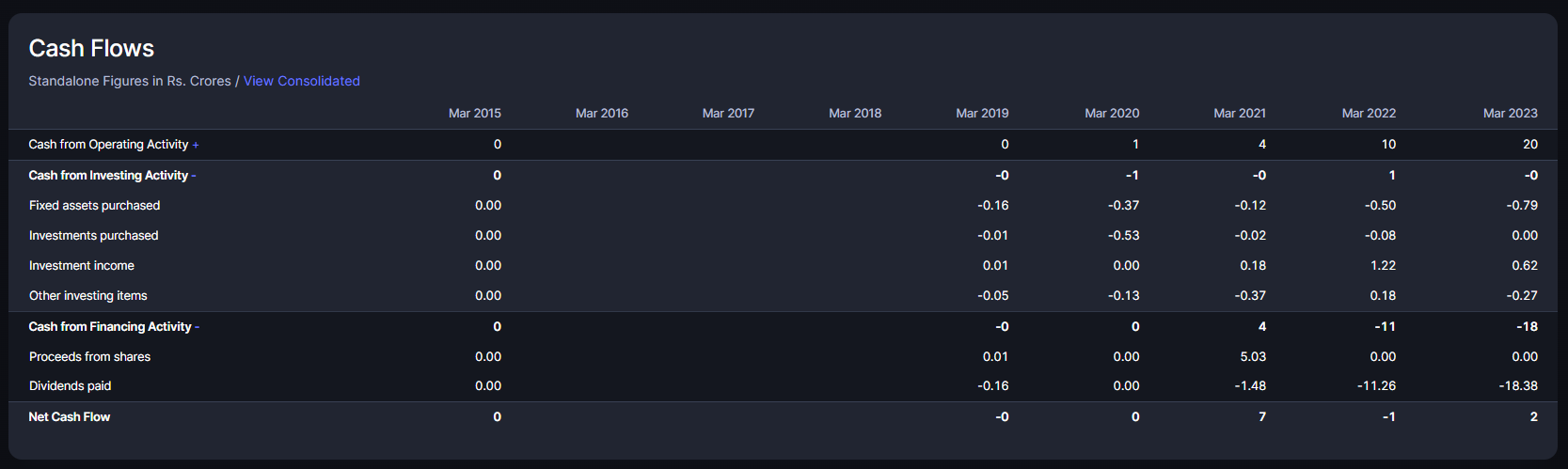

Observation from balance sheet & cash flow statements

Trade payables increased from 9.25 crores in FY 21-22 to 15.13 crores in FY 22-23. Which increases the working capital from 16 crores to 22 crores for the same period. However the growth in top line as well as bottomline exceeds the increase in working capital, because of which the cash flow from operations has doubled from 10 crores to 20 crores. And almost all of it is being distributed as dividend (there is no requirement of keeping higher cash on the balance sheet despite the company is in high growth phase)

This way the book value of the company will not rise commensurate to the profit growth which will lead to even further rise in ROCE (which is already above 100)

Though the company is still very small and it’s too early to form an opinion but the company appears to be in an different orbit. Many successful companies have grown fast on internal accruals without taking debt by having higher ROIC. But what is happening in Ksolves currently is beyond epic, as the company is growing fast without debt and even after distributing all the profits as dividends.

The risk involved here is “Till when this can continue” before company achieves a particular size and start facing competition from bigger companies. But even if the answer is few years, it can turn out to be a very rewarding investing experience.

Disclosure: invested from much lower levels and my opinions are likely to be biased.

Any take on Valuation on this? I have never studied any IT company, Just want to understand how one can value this company.

KSOLVES is in Additional Surveillance Measure (ASM) list for short term by SEBI.

Reference → https://www.nseindia.com/reports/asm

Definition of ASM →

Additional Surveillance Measures (ASM) are set on securities with surveillance concerns based on objective parameters like high-low price variation, client concentration, number of price band hits, price variation between closings, and P/E ratio.

Dis: I have a tracking position in the KSOLVES at lower levels.

We might value the IT company based on the dividend yield or PE ratio or both.

But considering that 40+ operating margin might not be sustainable, we might consider the future margins in the range of 20 - 30(like other service based it companies) percent for the guessing the company valuation in the future.

I was looking at annual metrics.

Look at the cash flows. Almost 20 cr of operating cash flows. 18.something paid out as dividend. About 50 lakh of Fixed assets purchased last year (from CFO), 45 lakh worth of laptops bought last year(presumably for employees; from AR):

One question people always ask me about this one is why their ROE & ROCE & NFAT is so high. Well, that’s coz

Disclaimer: invested, biased

A few things that need a deeper look -

At ~80 Cr annual revenue for FY23, employee base is around 500. Revenue per employee of INR 17-18 lakh and PAT per employee of ~5 lakh. Payroll expense for FY23 was ~35 Cr which means salary/employee of ~7 lakh. A large IT company does revenue/employee of INR 45-50 lakh and profit/employee of ~7 lakh.

What is it about Ksolves that they manage to retain such a high % of the per employee billing as PAT? Obviously a company can have an edge when it comes to cost management, especially if the work force is young and located in non metro cities. However this differential cannot be more than 15-20%, one can speak to employees based at cities like Mangalore, Mysore & Kochi and check this out

The client list is primarily IT organizations, which means Ksolves is just working as a staff augmentation player who can supply resources in specific technologies at a very short notice? But aren’t large IT companies supposed to have better bench strength, training programs and access to wider pool of people because of their brand name and bigger cash balance? Especially at an average salary of 7 lakh/employee, Ksolves is unlikely to have employees with superior technical skills. At best they can supply employees who are decent enough to get a simple job done at maybe 60% of the cost. If so, is this low end business model worth paying 30 PE for?

At employee payroll expense of 35 Cr per annum, monthly outgo on salary will be ~3 Cr. The business has more than 60% coming in from exports, hence the bulk of the money sitting as cash balance is needed by their bankers to ensure some sort of guarantee to do FX conversion activity. The provisions of 6 Cr+ are most likely provision for Income Tax on the balance sheet (FY23) and there is 15 Cr of AR pending at an average DSO of ~70 days going by the annual report.

All employee expense heavy companies prefer to have atleast 6 months of salary sitting in a liquid fund/FD so that they can pay salaries for sure even if they have a short term asset liability mismatch. But here is a management that wants to take out every single paisa that is possible as a dividend rather than create this much needed buffer on the balance sheet. This is very non-standard and deserves a very serious look.

Maybe the unsaid thing here is that promoters would rather have money in personal bank account than have it sitting on the company balance sheet where there are complicated contractual liabilities that can hit them any time? One of the biggest risks in IT business is the OTC nature of contracting where one can never know the real extent of liability that a service provider signs up for. As a junior engagement manager in my IT services stint, the first clause I would review was the limitation of liability clause followed by Indemnification & IP rights in case of custom development. What exactly is the scene at Ksolves? Why are the promoters so eager to swipe out money from the company rather than create a 6 month cash buffer in case of any exigencies?

For FY22 the top 5 clients were ~45% of the revenue which means revenue per customer of ~4 Cr within the Top 5. This is miniscule by any standards (as of date) and indicates that the business has minimal integration with things that are of importance to their customers. For an LTI Mindtree (listed as a client), a dependence of 4 Cr per annum on a vendor is inconsequential to say the very least.

If the bulk of the business is coming from IT companies, that indirectly implies that the business doesn’t have any direct customer connects at all. Most likely underinvested into sales teams and gets negotiated hard on everything by their larger IT peers (who understand business and technology far better than them).

The final point is the rent expense of ~63 lakh for FY22 that translates to ~18,000 per employee per year. One can understand that it will be a hybrid of WFH heavy model, hence rent is much lower. But the usual accounting practice is that any lease should show up on the balance sheet as a right to use asset (all other IT companies do this), which means the office space taken for use is not a long term lease but most likely a set of seats in a share workspace like a Wework. At an employee base of 350, most organizations would rather prefer a much cheaper dedicated space model on a long term lease (even if a dedicated floor within a wework) rather than stay on the rent model. The outlook here once again points to a short term view rather than a long term view on how to growing the business and securing good workplace assets for the team. I could be wrong here though, just that this needs a deeper look too.

Sometimes wonder why investors are happy to pay 30 PE for a business just because it has had 2 years of fast growth. This is nothing in this business that indicates longevity or differentiation at this point of time. Happy to hear counter points to this

Also, any acquisition will be margin dilutive. So, it is more efficient to grow organically.

One reason why investors are comfortable with this company is due their capital allocation policy. It becomes much more easier to trust numbers of smaller companies when all profits are distributed out. IPO fresh issue was also minute. (this is the one point which helped me alot despite them hiring a very young CFO who hardly has any experience )

Minimum Capex & other expenses

Complete off-shore model

Promoter taking out money via dividends only

Good growth momentum ( 1 year fwd PE at 23 + 3% div yield ) for older investors div yield is above 10%

Acquisitions don’t make sense as it will be margin dilutive.

All work is digital & no exposure to legacy systems (slow growth)

Employee cost is low as major employees are at the lower end of the pyramid ( this won’t be sustainable if they keep growing ). Also they do not have presence in main metro cities where the salary cost is the highest.

Disc- Invested & Biased

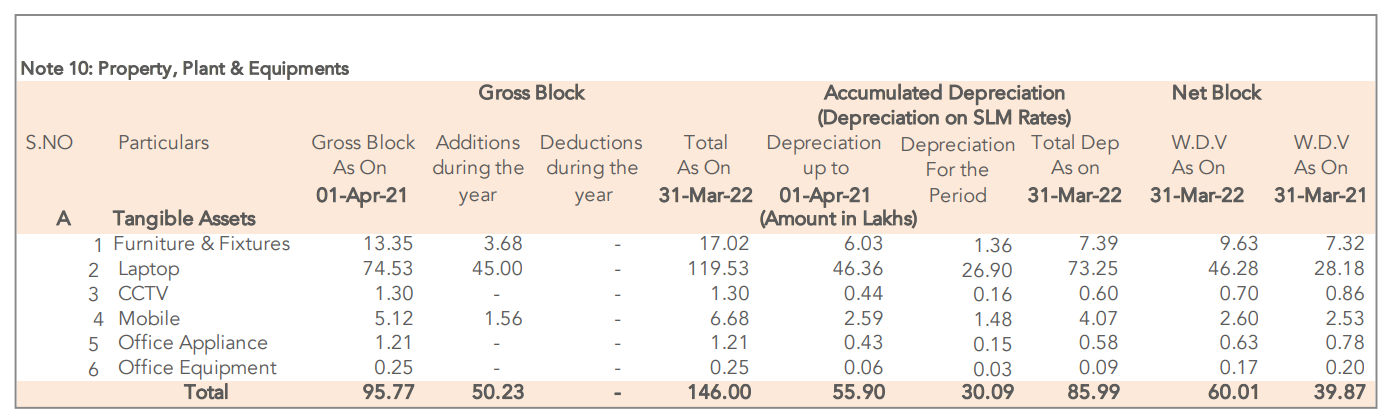

I did a quick check and what is bothering me are that the number of people with a dedicated laptop as a percentage of all employees.

The company has 119 Lakhs tied up in laptops and assuming that each of them will cost ~ 60,000 (conservative estimate) we would get 198 odd employee who has a laptop.

The total number of employees are 356 .

Effectively 1/2 of employees have a dedicated laptop.

Disc: Not invested, but tracking for some interesting story in the next few months.

Hi, hope this adds value.

Mostly with smaller IT firms, their gadgets are rented from 3rd party. And while getting a machine on rent, you would have to deposit some 5-10k with the renting co.

So consider that deposit amount as locked in money for deposits

Maybe to save cost they have provided laptops to only half of the employees. The other half that works from home are working through BYOD(Bring Your Own Device) model. In BYOD what we really do is that we create a virtual desktop (consider it a dedicated virtual laptop) for each of the employees through a virtual workspace solution like AWS workspace. Employees log into their dedicated virtual workspace through their own personal laptop. It saves hardware cost for the company by a lot. It is easier to maintain and secure. Maybe Ksolves is working through BYOD model.

Some small companies give benefit to bring your own laptop as well…

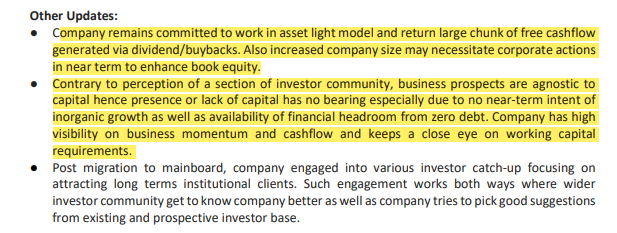

Ksolve Q1FY24 results are out.

The key highlight in release along with results, the company addressed sequential slow down during Q1FY24. It expects improvement in performance from Q2FY24.

I am also waiting for next corporate action( Dividend announcement/buyback announcement) for way forward.

I also take comfort from statement that “no near term intent of inorganic growth”. Generally, I do not like company which grow by acquisition.

Overall, results meet my expectation and commentary give good insight about medium term prospect. However, current valuation offer no margin of safety to new invevstor in my view. Hence, one shall do his/her own due diligence before making any investment decision. I am cautiously optimisitc and waiting for next corporate announcement.

Discl: Ksolve now account for 6% of my portfolio. I may change my investment decision without informing forum. I may be positively biased due to my investment. Not suggesting any investment action. I am also not SEBI registered advisor. Sold 10% of my holding due to tax planning. There are mutiple concern about missing points in Ksolve from business model, to salary of employee to high margin to internal auditor which need detailed due diligence in my view. Investor shall do detailed work before making any decision about the company in my view. Not recommeding any investment in the company.

If anyone has attended the AGM, please share the highlights.

Thanks in advance

A word of caution for all investors. A few months back I discussed KSolves with an IT veteran ex-Mphasis and ex-Cap Gemini. He was involved in salesforce implementation for Cap Gemini. He warned me about Ksolves. Not that the company is not genuine.

It just does plain vanilla Salesforce implementation. During Covid there was a boom in cloud services. Every company in the world which did not have an online presence had to have one. So there was a boom in AWS, Google Cloud, Azure, Salesforce etc.

So IT companies were throwing money to hire people implementing cloud services. Post the deluge of work the cloud work has normalized and decreasing. So they are firing people.

Ksolves is a tiny company, hence the revenues will disappear later as the base is small. The ramp up of revenues over last 3 year is not sustainable. It will come down over the next 3 years. The first sign of slowdown you have seen in the tepid QoQ growth over the last 3 quarters. Don’t get mislead by the YoY numbers. This is not a YoY comparison company.

This was a one time opportunity and that is why dividend payouts are so high. The promoters are aware the revenues wont be there in 3 to 4 years. So they are cleaning the coffers the right way by paying themselves and minority investors dividends (all clean and above board) -dividend payout ratio of 74%, 44% and 52% over the past 3 years. In the meantime whenever there is chance promoters will sell down stake to buyers who think this is the next big thing.

Let me draw 2 more parallels for you to understand.

So net net the terminal value of this stock is perhaps 0 unless they come up with a new sustainable business.

Even the type of technology stack they mention on their website suggest what they do is Commodity IT stuff like building simple Apps and running some cloud jobs, which for someone with IT background knows it’s pretty basic stuff.