@inteliinv . Thanks for sharing twitter link. From there I got email address and sent some of my quesries to the company.

@COMLB26

Further to your observations, I sent an email to the company seeking certain points. Key highlights of reply from company IR are as under:

-

What is business model of the company? How company can generate operating margin of more than 40% during FY21 and FY22 when the large IT Firms operating margin remain in range Infosys (24-33% during FY11 to FY22 period), TCS (26-30% range during FY11-FY22 period) and relatively small companies like Persistent System (14-22% range during FY11-FY22 period)?

Reply: Provided link to NSE website for Q2FY23 results

-

The 40%+ operating margin are also considering the relatively lower cost of manpower (median salary of Rs 3,00,000 p.a.) as against Median salary of Rs 8,14,000 for Infosys during FY22; Rs 7,14,812 for Persistent System during FY22.What drive this superior margin for the company? Also, how much sustainable the growth in margins? Does management perceive same reaching normalization period (time when it would meet industry average) and what is management view of length of normalization period?

Reply: There must be some variation in calculation/ you might have taken the start of the year as the base. For FY 22 Our Median Remuneration is Rs. 3 lac and the Average salary is between Rs. 7 lac- Rs. 8 lac as we have a higher number of people at a lower level of the pyramid and is expected to be the same in near future.

-

The company has registered office in 317/276, Second floor, Lane No. 3, Mehrauli Road, Saidulajab, Saket, New Delhi-110030. The internal auditor M/s. RSAV & Company also have same office address 317/276 Second Floor Lane No.3, Mehrauli Road, Saidulajab, Saket, New Delhi-110030, India as per annual report. Further, despite company having registered office in Noida, what is specific reason to appoint Statutory auditor and Secretarial auditors having their main office in Jaipur? Normally, we find most of companies using service of auditors and CS which are normally located in same location to minimize logistic time and cost. I would appreciate if you revert on this point.

Reply: . At the time of inception to avoid any procedural delay, the company had started with the same registered office address. But apart from mailing purposes, the company has operational corporate offices in Noida, Indore, and Pune and in the future planning to shift the registered office either to Pune or Noida region.

The Statutory and Secretarial Auditors were appointed at the time of the IPO. At that time the situation was a nationwide lockdown. Both entities had been appointed after a good research and both have been found with a greater degree of knowledge in the area of audit and

secretarial than their peers. Having both entities in Jaipur has no impact on Audit procedures.

-

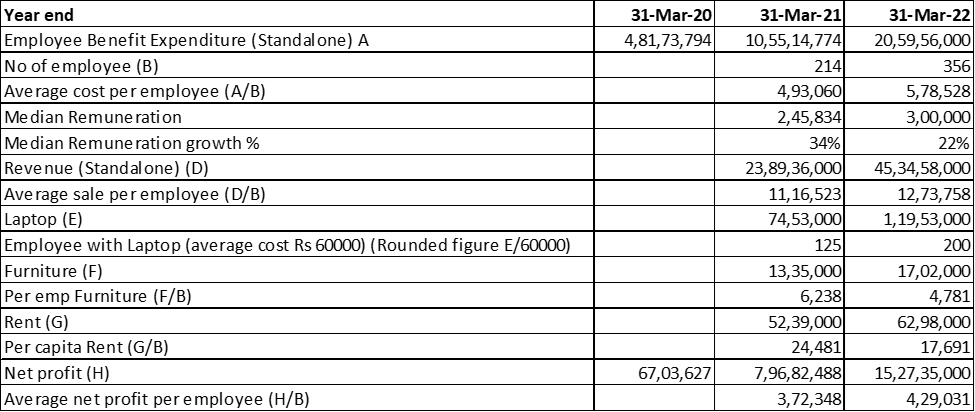

Last three-year average net profit (Standalone) as per my calculation of will be Rs 797 Lakhs (Rs 67 Lakhs in FY20, Rs 796 Lakhs in FY21 and Rs 1527 Lakhs in FY22). Annual report FY22 on Page 119 shown required CSR spend of Rs 5.87 Lakhs, which is 2%, so average profit being 50*5.87 Lakhs, i.e., Rs 294 Lakhs. Can you please look into calculation and revert?

Reply: Regarding CSR expenditure for FY 2021-22, the last three-year average net profit shall be calculated taking the year ending 2018-19, 2019-20, 2020-21

-

Some issue needs more explanation. For instance, Pg 82 says 100% of revenue is generated from Export sales (vs Pg 85: Revenue by geography: 74% is Exports and 26% domestic sales). Also, despite increase in employee strength (almost double) and increased revenue, we find in FY22, expenditures like Office expense decline. Further, increase in most head like Business Development, Office Rent expense, Electricity charge growth is very low as compared with increased level of activities. When employee strength increases almost by 50%, how can rent increase is just 20% in FY22?

Reply: There is certainly some typo error, 74% is Exports is the correct data. We shall convey this to the management.

Further, post covid, the electricity and rent expenses had been lowered due to work-from-home practices. New hiring did not burden these expenses. Very later the company started the hybrid model and in the near future, these expenses are expected to rise as a result of an increase in the higher ratio of work from the office.

-

Can you provide some press releases from large clients, for instance SalesForce partnership status upgrading to Silver (Ridge) from SalesForce website, or other public domain?

Reply: We had updated our investor regarding upgrading to SalesForce Silver (Ridge) partner. Disclosure can be found at link https://archives.nseindia.com/corporate/KSOLVES_03032022092745_SalesforceRidgeDisclosure.pdf

While the main question about superior operating margin remain unaswered, on other points, the company has provided explanation which I find acceptable, given the company started as SME company and justed moved to main board. In Microcap companies, we can not expect same process and system as we find in Mid Cap and Large cap, as they have limited management bandwidth, high growth propsect and past experience and methods of working as small Prop/Partnership firm set up.

Having said that, I am still not convince about robustness and sustianability of business model and whether the company can manage high growth with such high margin for next 2-3 years. Please note that my view may be biased and I am may wrong in my understanding.

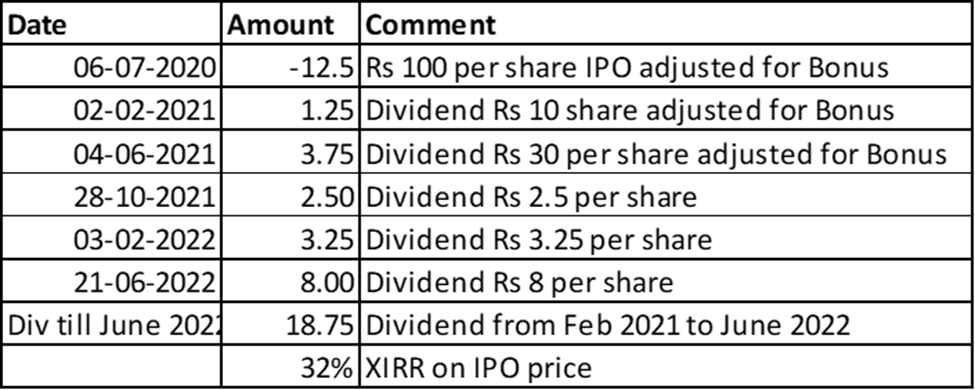

My working/calculation table for some points as enclosed

Discl: Not A SEBI registered advisor, Not recommending any investment actions, Biased due to my investment, Added small quanitity in last 10 days (invested around 1% of equity portoflio due to superior dividend yield and anticipating growing dividend with cashflow over next 2-3 years). I may exit from investment in case find superior opporunity or my risk profile change without informing the forum.