Punjab expansion on track!

Admittedly, found through sahil sir’s tweet not screener.

16 Likes

I am new to the company. Done some research.

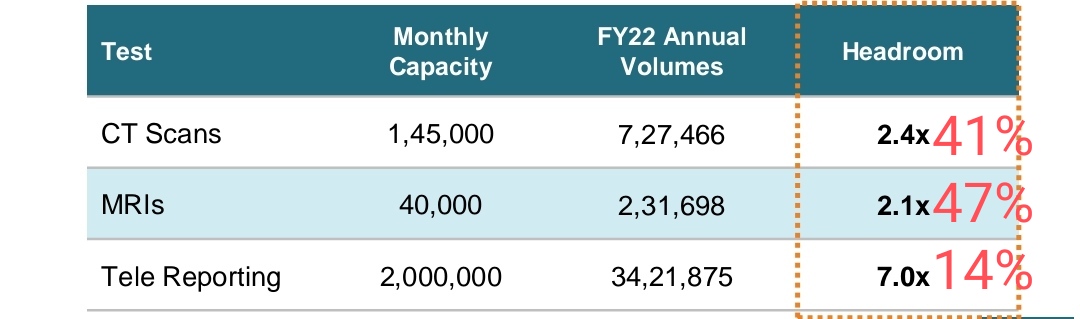

To people complaining about capacity utilisation not going up. It can be seen to improve YOY.

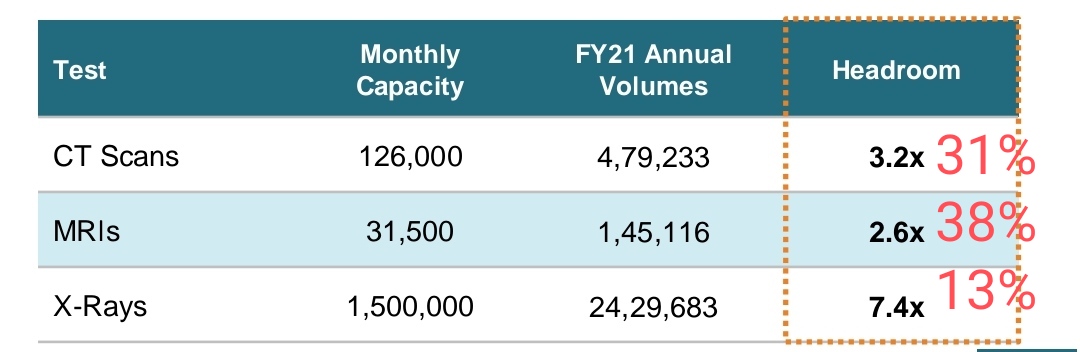

Here is radiology capacity utilisation in FY21 vs FY22, it can be seen to be increasing inspite of increasing capacity.

Now management has given very aggressive guidance of 30-40% growth. What I feel is they might not be able to achieve that much growth in FY23 but there will be decent growth due to new PPP projects going live and improving capacity utilisation (already visible).

Mgmt walking the talk or not?

So far in punjab only 4 diagnostic centers (don’t know radiology or pathology) have gone live in Q1FY23 as per the disclosures in BSE. But mgmt promised of 7 radiology centers going live in q4fy22 presentation. So even if we assume all 4 are radiology centers still it’s lower than 7. So it can be clearly seen that management is giving high guidance and under delivering. While it should be the other way around.

So it can happen that they might not achieve the aggressive guidances given for near term. I have no doubt about the growth opportunity and company achieving good growth in future due to runway for growth is excellent. I just doubt that it might be lower than what mgmt is guiding which is very aggressive.

Growth Drivers: Increasing capacity utilisation (already visible trend) + New PPP projects giving contribution (yet to be visible, though it’s bound to happen, might be some delay)

Anyway the stock has corrected a lot and consolidating since March lows. So it seems like lot of negative things of future is already priced in.Now lets see how much revenue they deliver in Q1. they have given guidance of 650-700 cr revenue in fy23. I’ll be happy even if they deliver 600 cr.

Disclosure: Initiated tracking position. Planning to add more on numbers matching the narratives.

9 Likes

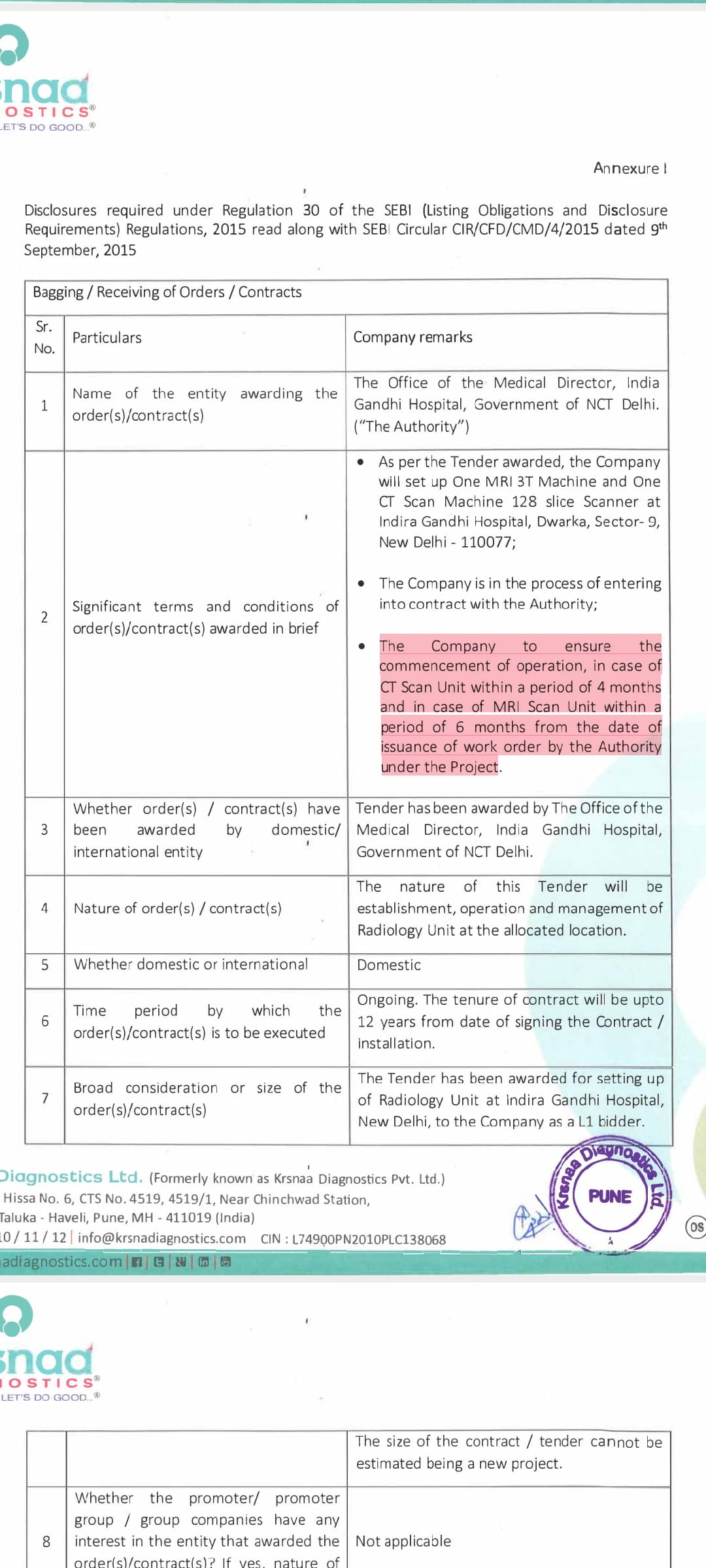

New tender has been awarded in Delhi. MRI&CT Scan to be operationslised within 6&4 months respectively.

5 Likes

I found the tender documents, details of each bidder, how the financial and technical evaluation took place, and why Krsnaa was awarded the tender.

Tender Details

-

Awarded at the Indira Gandhi Hospital (IGH), Dwarka for a period of 10-12 years.

-

Patients will be referred by various departments of the hospital for MRI and CT scans. They have to be given highest priority amongst all patients served.

-

Krsnaa can enroll on schemes that allows them to also receive patients from other government hospitals. This will be billed monthly.

-

After all scans of patients from IGH are done, Krsnaa can bring in outside patients (private walk ins), but cannot give them priority over IGH patients.

-

Hospital provides space, Krsnaa pays for electricity and utilities in day to day running.

-

Krsnaa has to provide an in-house (tele?) radiologist and an emergency anesthetist on standby.

-

MRI will run Mon-Sat, 9am - 4pm on weekdays for IGH patients.

-

Medical college at IGH will have access to all radiology data to teach/academic reasons.

-

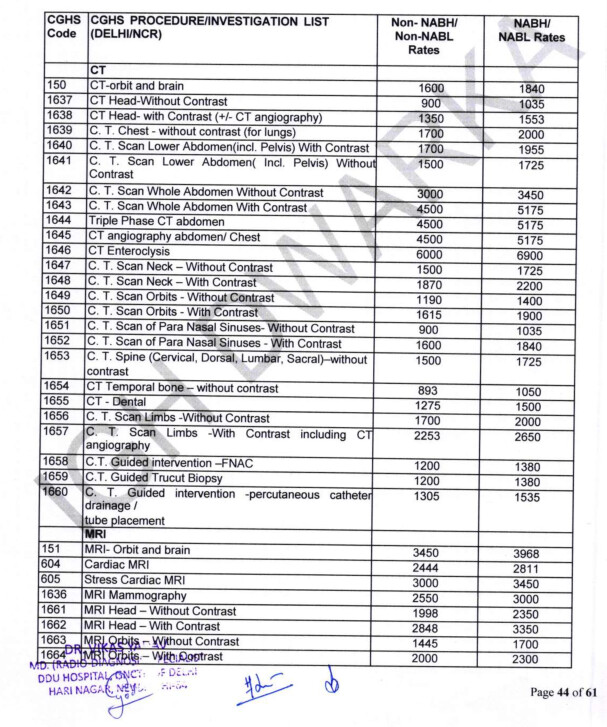

Rates will be CGHS rates, IGH will take 10% of revenue share from private walk ins. Bills will be shared with IGH monthly.

-

Unlike other tenders that evaluate on lowest cost basis, this tender asks diagnostics companies to pay a monthly fee, which rises at 2% annually. Highest bidder wins.

- Prices are a little lower than Krsnaa’s usual offerings (Brain CT at 2000 on investor presentation vs 1840 here).

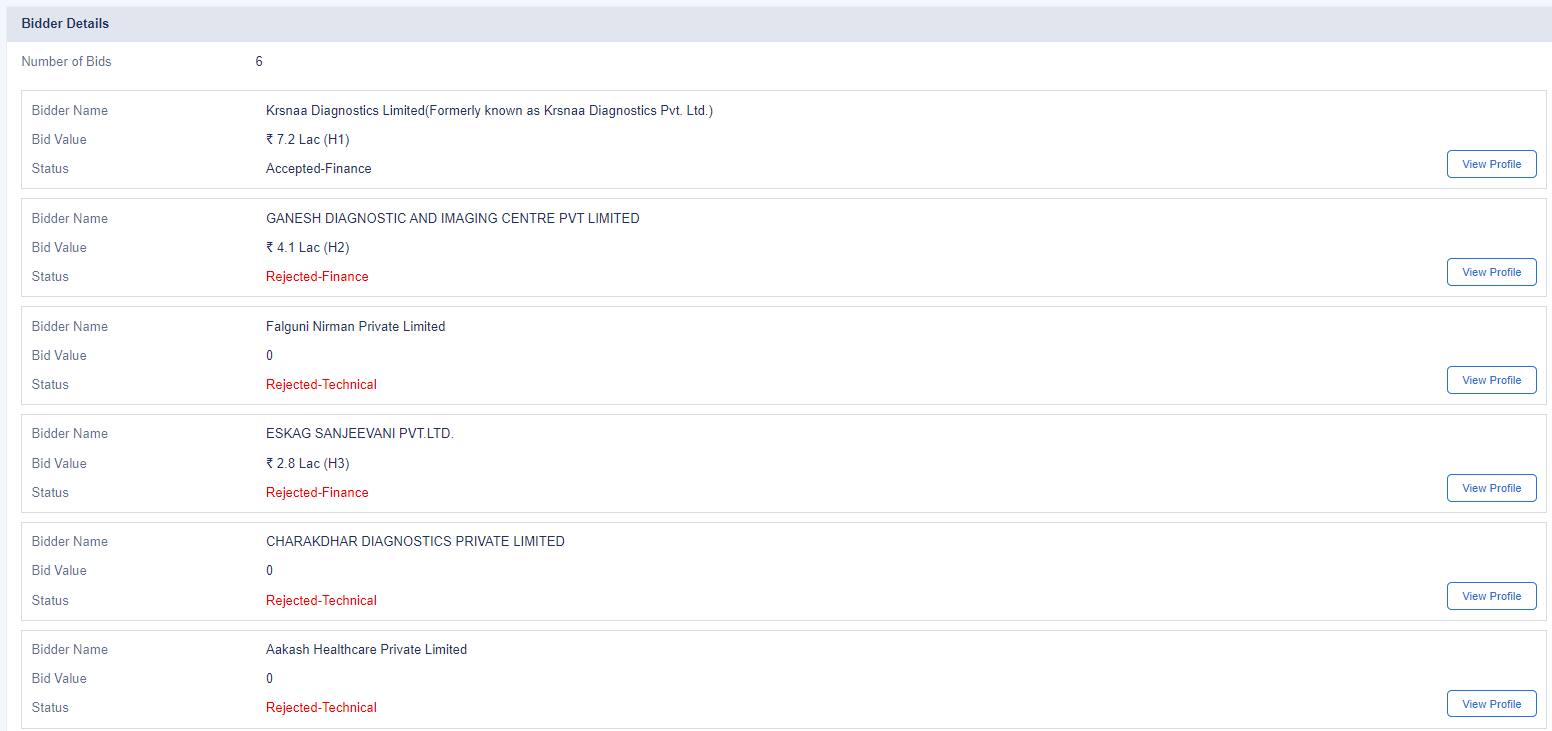

Financial and Technical Evaluation

-

Falguni Nirman did not have the correct certifications and was disqualified. Aakash Healthcare was also disqualified and did not make it to the technical evaluation round.

-

Krsnaa offered equipments from 3 different OEMs / vendors: Siemens, GE and Philips.

-

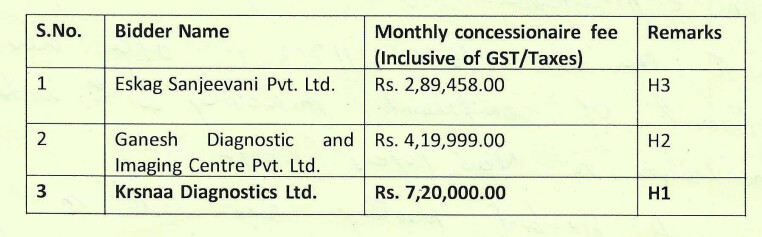

Here are the bidding details for the monthly fee:

Therefore to operate at this hospital, Krsnaa has to pay 86.4 lakhs a year (rising at 2% annually). This is siginficantly different from other tenders (to my knowledge), where they’ve been bidding for lowest price.

Secondly, there doesn’t seem to be an annual price hike in tender documents. With these two in mind, this looks to be potentially of lower margin compared to earlier tenders.

However, we know Krsnaa’s management evaluates tenders and only bids for those where they’re confident of achieving a target margin profile. So do the volumes from IGH + nearby government hospitals potentially make up what’s lost in margins?

Edit: I have a feeling that this is the largest hospital in which Krsnaa has a presence, with over 1400 beds. Volumes could be very high from in house patients itself. Conceptually, this looks somewhere in between a revenue sharing model with private hospitals, and the PPP tenders they usually bid for.

Edit 2: I belive district hospitals usually have between 25-75 beds. I can compile a list of Krsnaa’s presence, sorted by the size of each hospital.

D: invested, biased

Documents here: https://drive.google.com/file/d/17Xh1jSYkgMCGp5r-WXCb7OoAgmSLhikD/view?usp=sharing

32 Likes

This is a question can be asked in next concall. Do the company reply if we mail to the investor relationship email?

I can add a little bit details here.

- I live in Dwarka so have some locus standi to understand the operations of this setup.

- Here is the hospital. THis is one of the largest hospitals one can find in Delhi, & probably India with 1200 beds. For context you can see here that largest hospital in india is Calicut medical college with 3000 beds. This college/hospital should also add a significant organic flow of patients given that its a large hospital. one of largest source of patients for large hospitals are smaller feeder hospitals nearby (complex patients are referred from nearby hospitals to the larger hospitals).

- Dwarka is one of largest sub-cities of delhi. One of the only structured/planned sub-cities. Dwarka did not have a large hospital until now. We would have to go to Safdarjung, AIIMS etc to visit large government hospitals. Dwarka (south west delhi) was planned for 1-2 million people. The catchment area around delhi is west delhi which is also densely populated & lacks a large government hospital (most of them are in south delhi). Dwarka is also where a lot of noveau-rich in delhi live (large structural residential sub-city). I dont think there would be a dearth of catchment area for large number of private walk-ins. Dwarka is by no means a tier 2 or 3 city. Its as tier 1 as it can get (with the exception of South delhi). Actually the reason i know this is a problem is that i wanted to get a CT scan done during covid wave 2 but had to go to a small lab where i had to wait for hours for getting a scan. I dont think demand would be a problem here, only the correct targeting/marketing/customer consciousness creation is needed.

- Once krsnaa’s diagnostics unit starts in 4-6 Months im happy to visit the hospital & ask around to do some on-ground scuttlebutt about the quality, quantity of the radiology unit (3km from my home).

Disclaimer: invested, biased

31 Likes

- Another interesting data point is the competition for these contracts - only other bidders were local chains, and no other P/E or vendor-funded rivals or listed players.

- The rates for procedures do not appear to be fixed but are linked to CGHS rates, which should rise in line with the costs quote “the prices quoted shall remain valid for the duration of the contract or till DGEHS/CGHS revises the rates for the said procedures; whichever is earlier”

Any idea on estimated revenues from this contract?

2 Likes

Perhaps I should have been clearer. We’d need to look at how often CGHS revises rates, and how much they change prices when they do.

Contract was for 1 MRI and 1 CT scan machine. Looking at the DRHP:

They’ll be doing 150 scans per day. If we say on average that a scan costs 2500 rupees and the site is running for 360 days a year, that’s a revenue of 13.5 Cr. This figure can be higher or lower depending on the volume mix, but will be in the range of 10 - 20 Cr.

So if they’re limited to 150 scans per day, it doesn’t matter if there are 150 people in queue, or 1000; they’re limited by throughput.

What I am surprised by is that a hospital of this size only required one CT / one MRI. Perhaps they’ll amend the contract to add on more should the lines run long, or add on path works through a separate PPP contract (Krsnaa won such a contract in Himachal where they provide path in hospitals where they had a radiology presence).

Contract could be very important for visibility too. We’ll learn more from the concall, and from a site visit from our resident Dwarka dweller. ![]()

11 Likes

The hospital being discussed is still to be inaugurated hence likely this is just a preliminary contract and may get bigger in future

This story is from April 1, 2022

Disc: invested

9 Likes

@Chins @Anish_Moonka Would appreciate if you can provide any details on the number of free tests that Krsnaa has to do as per PPP gov contracts. How much loss as a percentage of revenue and what percentage of total tests do they have to do and bear. The number should be small but with gov. interference, one doesn’t know what kind of stunts they may pull although all these details are pre-decided for 5-8 years as part of tenders.

Picked this from here:

- Some of our diagnostic centres are required, and other diagnostic centres may be required in the future, to provide free or subsidised diagnostic services to patients belonging to economically disadvantaged sections of the society and certain other patients. Under the terms of PPP agreements for the operation of our diagnostic centres, we are required to provide free or subsidised diagnostic services for certain tests to patients belonging to economically weak sections of the society and certain other patients. As of November 2020, free diagnostic laboratory services have been

implemented in 33 states and union territories. In 11 states and union territories these services have been implemented under the PPP mode while in 22 states and union territories it is under in-house model. In addition, free diagnostic CT scan services have been implemented in 13 states and union territories under the PPP mode while in 10 states and union territories it is under the in-house mode (Source: CRISIL Report).

Further, we may be required to provide free or subsidised diagnostic services for certain tests to specific sections or classes of patients with respect to the healthcare facilities in which we operate. We may also be required to provide free or subsidised diagnostic services at the existing diagnostic centres pursuant to any social welfare legislation enacted in this regard. The provision of free or subsidised diagnostic services may adversely affect our revenues and our business, financial condition and results of operations. Further, any failure to provide free or subsidised diagnostic services may be considered a breach of the relevant agreement and the public health agency may terminate such arrangements in the event of our failure to comply with their terms.

I might be over-focussing on this anti-thesis pointer but I’m simply trying to understand why is market punishing this business or is it simply being inefficient.

Disc: Not invested but very enticed by this business.

Another point on B2C side. Why are they trying to enter B2C side which is very different from their current model and they will have to compete with other players. I wasn’t satisfied or couldn’t understand from their response in Q4 concall ( also had to go and check transcript since voice of speaker sounded exactly like Mr. Jhunjunwala (found out it’s Utkarsh Maheshwari))(Interersting to see Lucky investments also tracking Krsnaa) . If you can shed some more light on how their B2C entrance will not see them competing with other traditional players like Dr. Lal on pathology side.

Exact timestamp response below

6 Likes

Not very good at TA, but as holders of krsnaa, a down trending stock today we see a bit of a reversal, holding up above these levels with volumes will be an indicator for a basing period/reversal.

Fundas are stronger than when I bought(punjab expansion complete), so looking to average down.

Disc - largest holding.

6 Likes

This is what management conveyed as per my understanding: For B2C side they want to leverage the existing infrastructure, which already have a lot of private footfall (read q3 concall).Most ppl came to know by word of mouth. Now imagine can be done with little bit of advertisement. That’s why they are foreying into B2C. They are already doing it without any advertising. Now they want to do that too.

My take from the concalls on competetion: The cities in which Krsnaa is present ppl are very conscious about cost. So they being the lowest cost service provider because of their business model already provides an edge. plus in the small towns players like tata 1 mg are absent.

6 Likes

Went through the thread. Yet again, a great, high quality deep dive into a small, new company’s business that only Valuepickr Community members can do ![]()

I have one question and one number where I need feedback.

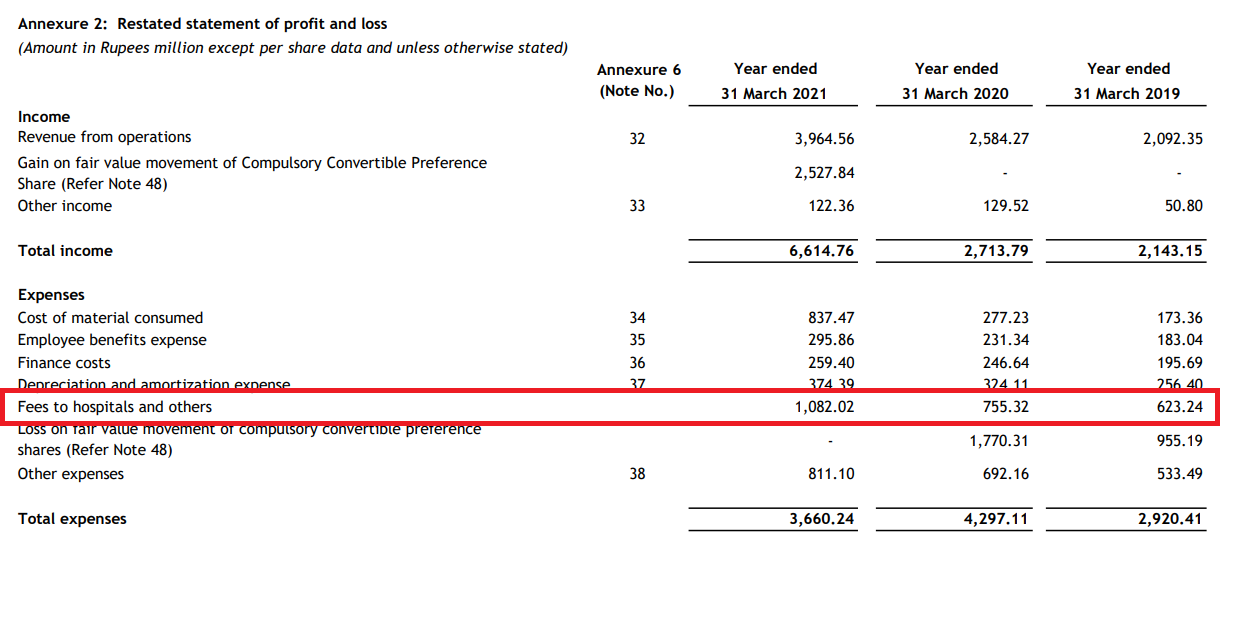

My question is around the fees to hospitals. What is this fee that Krsnaa is paying and where can I read more about it? I checked in the DRHP but couldn’t find any details about this line item. The good thing is that this line item as a % cost has come down from 30% of revenue in FY19 to 24% of revenue in FY22.

Secondly, I am trying to establish what can be Krsnaa’s steady state net-fixed-asset-turnover. Presently its 1.2x but there are is a lot of unutilized capacity, so this number or past NFAT numbers don’t help. I have tried to estimate this number in the following fashion.

As per @Dev_S’s calculations, presently Krsnaa is on-average doing 30 CT scans/day on its CT machines. The capacity is 100 scans/day, so average capacity utilization of a machine is 30%. As per latest concall, the best utilized clinics have a capacity utilization in the 60-80% range.

Assuming a 70% utilization for a CT machine this would mean 70 scans/day (I am using machine utilisation as a proxy for clinic utilisation - please help validate if this thinking is correct)

Avg cost of a CT machine for Krsnaa: 1 Cr (Please help validate - am I underestimating the CT machine cost?)

No, of scans in 1 year @ 70% utilisation : 25000 (70*360)

Revenue per CT scan : Rs 1750

Total revenue from CT machine for the year : 4.4 Crs

NFAT : ~4x

The NFAT would be lower for MRI machines, because they cost up to 5-6x of CT machines but the per scan revenue is only 2x the CT cost, so NFAT for MRI would be ~2x.

At a blended level, steady state radiology NFAT would be ~2.5-3x assuming slightly more INR investments in MRI m/cs as compared to CT (Present ratio of CT:MRI is around 2.5:1 and price ratio is ~1:5). Pathology NFAT would be higher (3-4x) because its not as capital intensive - Metropolis/DLP NFAT would be a good proxy for this.

All in all, on a blended basis at a steady state (Maybe 5-7 years down the line from today), I am assuming a 3-3.5x NFAT for Krsnaa. Need your feedback on whether this is a reasonable assumption to make or not. Thanks.

12 Likes

@nirvana_laha , your calculations broadly looks right, have some additional thoughts on asset turn modeling.

On asset turns, think path lab have lots of industry peers so relatively straightforward. But better to look in isolation, reasons below

MRI and CT asset turns or thesis itself has some dynamic parts in my limited understanding as well as thesis

- Krsnaa broadly at product mix level moving in Radiology direction over few years - which may mean that asset turns will follow that path, within that MRI vs CT mix will further dictate.

- While theoritical capacity of CT/MRI may be X but fact is that most hospitals will have lean vs high usage shifts - e.g in a day 7 AM to 10 PM would be a better window to drive utilization than odd hours - thus theoretical capacity may not hold good in practical aspects - in other words location + footfall + timings play imp role to drive utilization( thus hospital selection/ due diligence if not done well - everything else may go for a toss)

- Also Krsnaa seem to be exploring per scan basis capex model - there were some conversations in last concall, again could be path breaking model and asset turns / RoCE will see meaningful change if successful.

Summary - asset turns will likely evolve/ stay dynamic based on above and belnded( path + radiology) may not be best way to look at may in my limited understanding. Also even if they have enough demand 100% utilization may not be possible, expert from field can guide but 60-70% seems optimist case IMO ( exceptions could be there).

6 Likes

Nfat is not right way to look imo. Going forward many machines would be on lease model. It is roce at mature center level & upcoming center level. Terminal roce is 35% but may stay depressed as the growth happens in the interim. The good thing is that the co has copius amounts of cash & no debt. So growth if funded from cash on books + internal accruals (this is actually a cash generation machine) .with government receivables improving, % of private increasing, the receivables should come down hence improving cashflow generation enabling even better funding of growth from internal accruals.

I don’t think that is the correct interpretation. This is the fees paid to hospital “and others” meaning this includes other expenses. My hope is we would get granular breakdown in the annual report. Absent which would need to check with management in concalls. The fees to hospital part you can see in pre ipo meet. This is the fees given to private hospitals as a cost of doing business (sort of like revenue sharing)

7 Likes

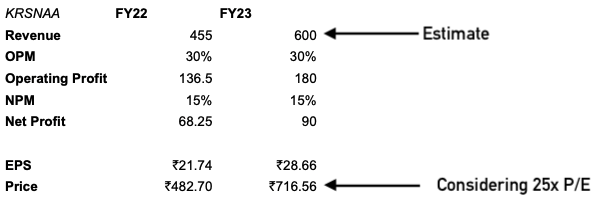

Hello everyone, I have done a simple calculation based on 600 Cr expected Revenue:

5 Likes

Company got contract of CT SCAN CENTRE at MES Medical College located at Churu Rajasthan for tenure of 10 years. Company will commence operation within 6 months.

8 Likes

The barrier to entry is none in this sector but very hard to scale. That’s the moat krsnaa has.

1 Like

Scaling is even harder in B2C space

But with their foray and focus on B2C, wont the margins come down, since they will be spending more on mobile app/IT, promotions, mktg, etc. Very little of these spends contributed to higher margins till now, but that seems to change going forward. Mgmt take is that they will continue to maintain/improve the margins.

What do VP members think?

1 Like