Krishna Diagnostics Limited (KDL) - Q3 FY25 Earnings Call Key Takeaways

Current Financial Performance (Q3 FY25 vs Q3 FY24)

Revenue: INR 1,745 million, up 10% YoY.

EBITDA: INR 466 million, up 23% YoY; EBITDA margin expanded by 279 bps to 27%.

PAT: INR 194 million, up 50% YoY; PAT margin expanded by 293 bps to 11%.

Diluted EPS: INR 5.9, up 48% YoY.

Receivables: Higher than usual due to delayed payments from Himachal Pradesh and Karnataka, averaging 60-65 days, with exceptions extending to 120 days. Management aims to reduce this to 90 days by fiscal year-end and normalize to 65-70 days in the next fiscal year.

Other Income: Elevated this quarter, attributed to gains from strategic capital reallocations, structured financial initiatives, and interest income from fixed deposits.

Current Financial Performance (9M FY25 vs 9M FY24)

Revenue: INR 5,311 million, up 17% YoY.

EBITDA: INR 1,416 million, up 39% YoY; EBITDA margin expanded by 417 bps to 27%.

PAT: INR 569 million, up 49% YoY; PAT margin expanded by 231 bps to 11%.

Diluted EPS: INR 17.3, up 47% YoY.

Receivables: Management has collected INR 300 million since January.

Operational Performance

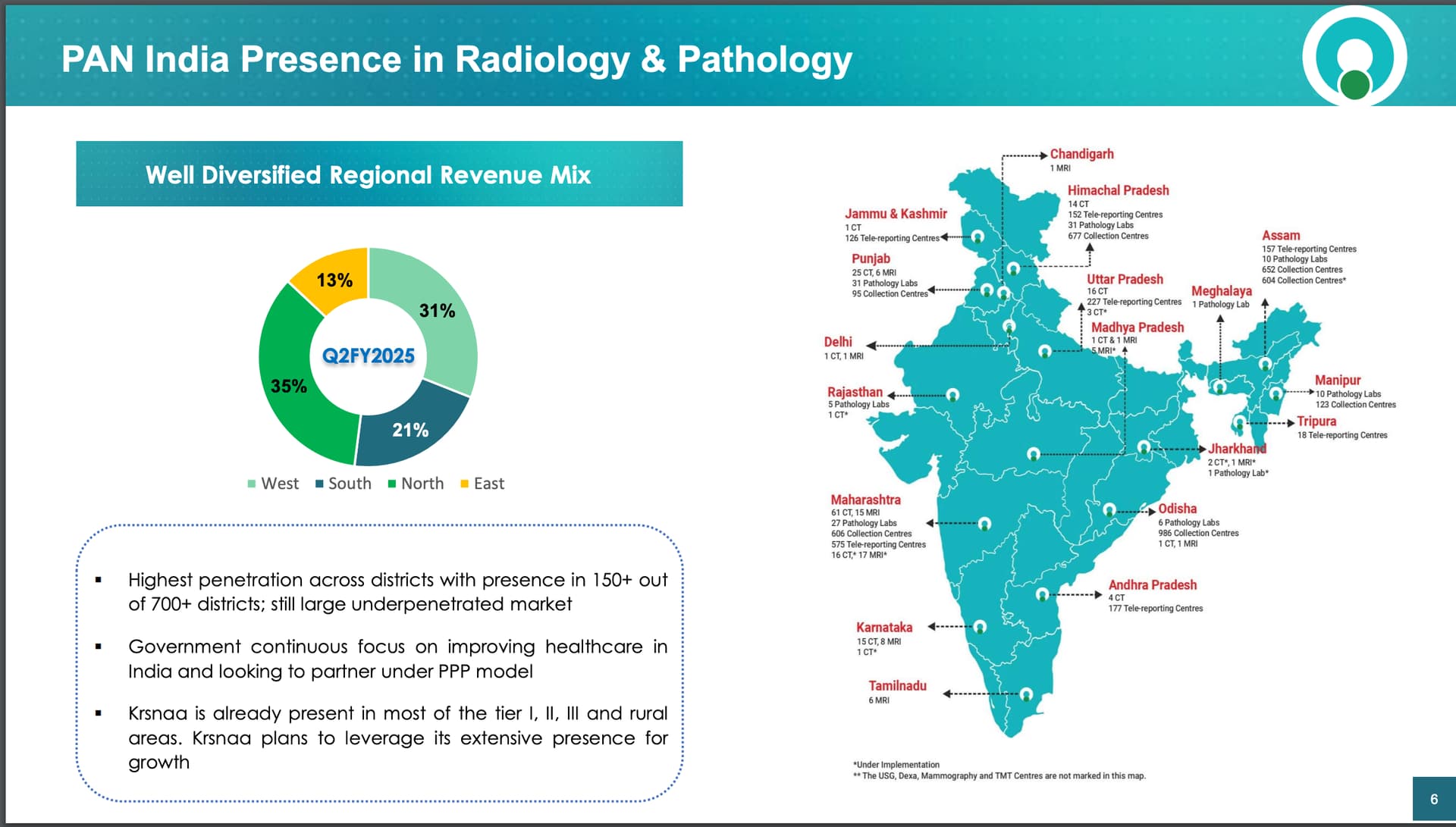

Radiology & Pathology Mix: Radiology contributed 49% of revenue, while Pathology contributed 51%, marking the first quarter where Pathology exceeded Radiology. Management aims to maintain a 50/50 balance.

Volume & Realization Trends:

Radiology: Increasing realization per test, while volume trends will be shared offline.

Pathology: Revenue mix shift due to new projects, but a balanced contribution is expected.

Center Growth:

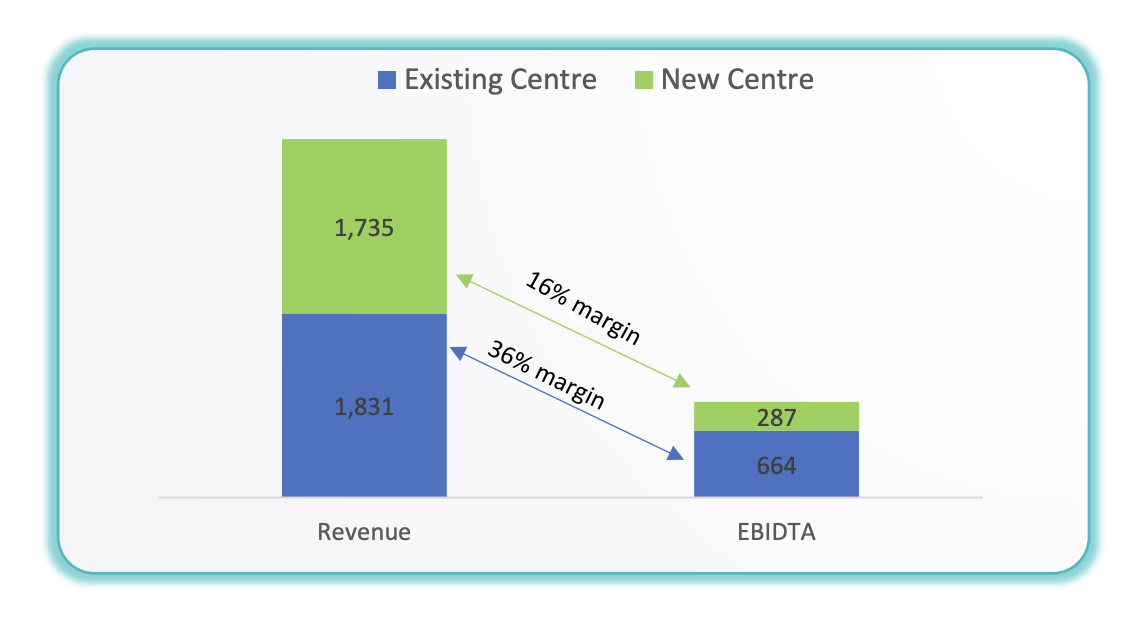

Existing Centers: Delivered a 36% EBITDA margin.

New Centers: Delivered a 17% EBITDA margin. Pathology centers typically mature in ~1 year, while radiology centers take ~1.5 years.

B2C (Retail) Centers: Launched under the RPL brand in four states, leveraging existing PPP infrastructure. Contributions expected to grow next fiscal year, with a target of 500 touchpoints by FY26.

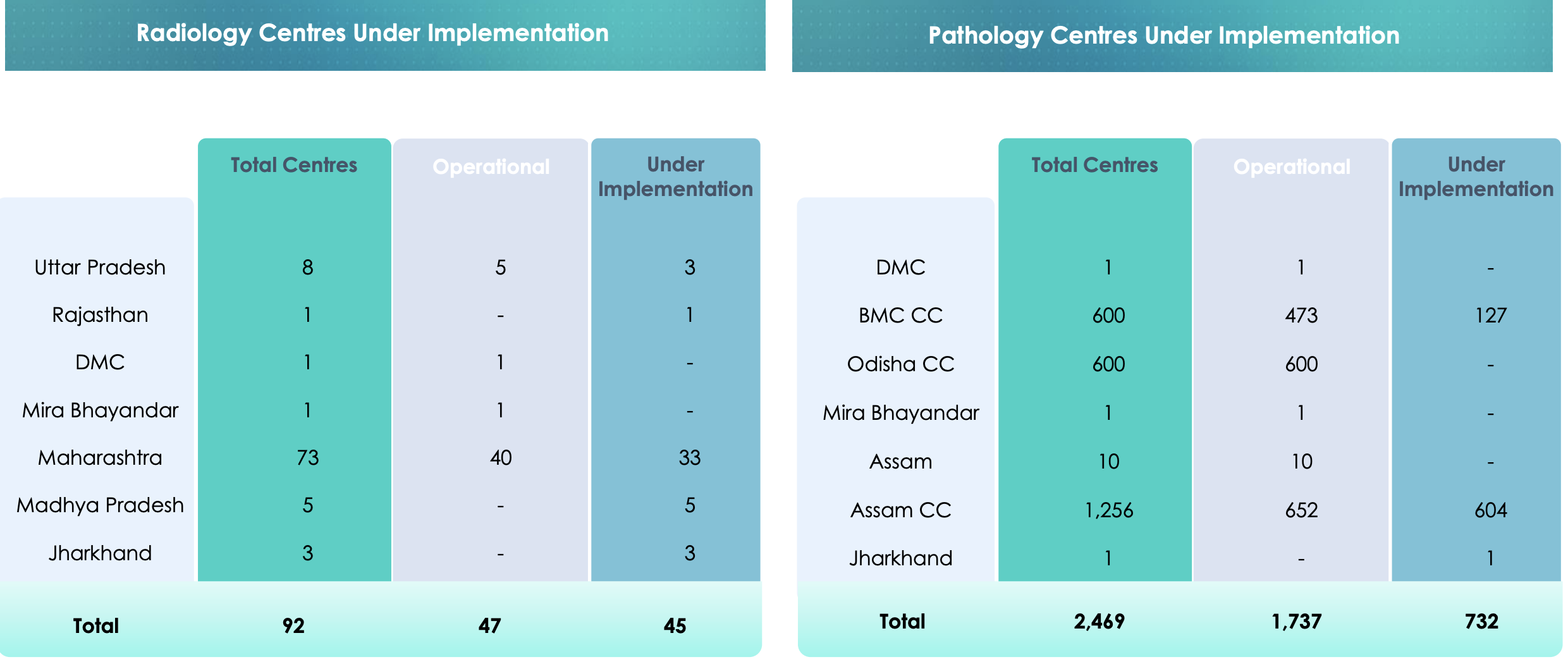

Project Execution: Delays in Maharashtra CT/MRI projects and Madhya Pradesh installations due to site handover issues; six centers are expected to be operational by Q4 FY25.

Operational Challenges:

Process automation challenges in Karnataka and Assam.

BMC project is on hold; KDL is participating in a new tender.

Equipment Procurement:

For Aapulki Hospital, seven pieces of equipment were ordered two received, with the rest expected by late February or early March.

Future Outlook

FY26 Guidance: Targeting 25% sales growth for FY25, confident of achieving it by Q4. Other income is expected to be ~INR 50 million quarterly.

Long-Term Growth:

Expanding the retail footprint in metro, tier 1, 2, and 3 cities.

Leveraging technology, AI-enabled diagnostics, and seamless online booking.

ROCE: Currently ~10-12%, with expectations for improvement through strategic initiatives, including an asset-light model, B2C expansion, and operational efficiencies.

B2C Contribution: Expected to increase as a share of total revenue.

Government Initiatives: Positioned to capitalize on healthcare reforms outlined in the Union Budget 2025-26.

Concerns

Delayed Project Rollouts: Continued site handover and operational challenges.

Receivable Collection Delays: High receivables in certain states raise concerns about timely cash collection.

Competition: Rising competition as the sector shifts toward preventive healthcare and digital solutions.

ROCE Improvement: Addressing the current low ROCE relative to past investments.

Other Important Points

Union Budget 2025-26: Emphasizes public-private partnerships, increased funding, and benefits for diagnostic service providers.

Rajasthan Tender: Ongoing discussions with the government; management remains confident in a favorable outcome.

Employee Focus: New initiatives launched for employee engagement, upskilling, and job satisfaction through comprehensive training programs.

AI generated content do your due diligence.

Disc:- tracking.